- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

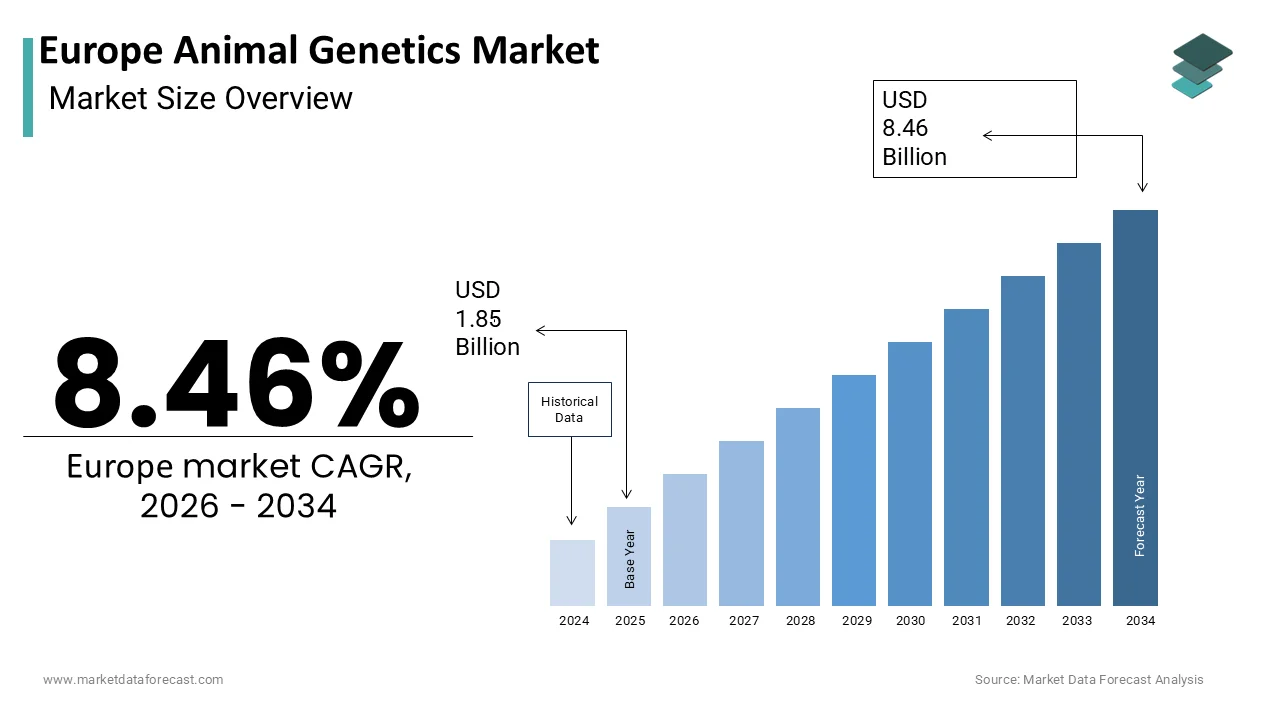

Market Size, 2025

$1.85 BnMarket Estimate, 2026

$2.01 BnMarket Forecast, 2034

$8.46 BnCAGR, 2026–2034

8.46%Europe Animal Genetics Market Insights

The europe animal genetics market was valued at USD 1.71 billion in 2024, is projected to reach USD 1.83 billion in 2025, and is expected to grow to USD 3.12 billion by 2033, registering a CAGR of 6.9% from 2025 to 2033. Growth is driven by genomic selection adoption, demand for disease-resistant stock, precision livestock farming, and genetic innovation in aquaculture.

Europe Animal Genetics Market Highlights

- 2024 Market Size: USD 1.71 billion

- 2025 Market Size: USD 1.83 billion

- 2033 Forecast: USD 3.12 billion

- CAGR (2025–2033): 6.9%

Europe Animal Genetics Market Data Book

2024 Market Size – USD 1.71 billion

2025 Market Size – USD 1.83 billion

2033 Market Forecast – USD 3.12 billion

CAGR (2025–2033) – 6.9%

Largest Product (2024) – Genetic Material (semen/embryos)

Fastest-Growing Product – Live Animals – 6.4% CAGR

Largest Testing Service (2024) – Genetic Disease Tests – 40.9%

Fastest-Growing Testing Service – Genetic Trait Tests – 8.89% CAGR

Largest Country (2024) – Netherlands – 20.9%

Key Segment Insights

- Genetic Material dominated in 2024 due to AI and embryo use.

- Live Animals are growing fastest as organic/regenerative farms acquire foundation stock.

- Genetic Disease Tests lead testing services (40.9%).

- Genetic Trait Tests are rising fast (≈8.9% CAGR) for feed efficiency, methane reduction, and welfare traits.

Country-Level Highlights

- Netherlands: Market leader (20.9%), strong dairy & export infrastructure.

- Denmark: High integration via cooperative/vertical systems (pig & dairy).

- Germany: Large dairy herd, broad genomic testing adoption.

- France & UK: Significant roles with breed conservation, welfare-focused selection, and growing sovereign genetics programs.

Market Drivers And Restraints

Drivers: Genomic selection, disease-resilience breeding, precision livestock data integration, and aquaculture genetics.

- Restraints: Strict EU rules on gene editing, public welfare concerns, fragmented national policies, and high costs for small farms.

Key Market Players

Genus Plc; Hendrix Genetics BV; Alta Genetics; CRV Holding B.V.; Neogen Corporation; VetGen; Animal Genetics; Zoetis.

Europe Animal Genetics Market Size

The Europe Animal Genetics Market is projected to grow from USD 1.85 billion in 2025 to USD 2.01 billion in 2026 and reach USD 8.46 billion by 2034, registering a CAGR of 8.46% during the forecast period from 2026 to 2034.

Animal genetics is the science and commercial application of selective breeding, genomic selection,n, and advanced reproductive technologies to enhance productivity, health, and sustainability in livestock and aquaculture species. This includes genetic improvement programs for cattle, swine, poultry, and farmed fish focused on traits such as feed efficiency, disease resistance, carcass quality, and reproductive performance. Unlike commodity-based agricultural input, its animal genetics operates high-valuevalue knowledge knowledge-intensive segment underpinning long-term herd and flock performance. Europe’s approach is distinguished by rigorous regulatory oversight, strong emphasis on animal welfare, and integration of genomic data into national breeding schemes. A large share of dairy cattle in the EU are enrolled in performance recording programs that link phenotypic data with genomic predictions. The EU maintains hundreds of millions of livest,oc k forming the biological foundation for genetic services. Many member states have implemented mandatory animal identification and traceability systems, enabling precise pedigree and trait tracking. This institutional and biological infrastructure positions animal genetics as a strategic pillar of Europe’s sustainable protein production strategy.

MARKET DRIVERS

Genomic Selection Adoption in National Breeding Programs Accelerates Genetic Gain

The integration of genomic selection into national livestock breeding schemes across Europe is a primary driver of market growth as it significantly shortens generation intervals and enhances accuracy in trait prediction. Unlike traditional pedigree-based methods, genomic selection uses DNA markers to evaluate young animals before phenotypic expression, enabling earlier and more reliable selection decisions. A large majority of dairy bulls used in artificial insemination across Germany, the Netherlands, and Denmark are now selected based on genomic estimated breeding values. In cattle, adoption of genomic selection has substantially increased annual genetic gain for milk yield compared with conventional methods. National agencies such as France’s Génétique Elevage now genotype hundreds of thousands of calves annually, with costs often subsidised under the Common Agricultural Policy’s rural development pillar. Similarly, in swine, genomic selection for feed conversion ratio has been shown in trials to reduce feed costs per unit of gain. This publicly supported yet commercially delivered model ensures rapid diffusion of genetic technologies while aligning with EU sustainability goals for efficient resource use.

Rising Demand for Disease-Resistant Livestock Drives Investment in Genetic Solutions

Growing pressure to reduce antimicrobial use in European livestock has intensified demand for animals with inherent disease resistance traits developed through genetic selection, which is further boosting the regional market growth. The EU’s ambitious target to cut antibiotic sales for food-producing animals by 50% by 2030, as outlined in the Pharmaceutical Strategy for Europe, has made genetic resilience a strategic priority. According to the European Medicines Agency, veterinary antimicrobial sales declined by 47% between 2011 and 2021, yet disease outbreaks remain economically damaging, which is prompting breeders to seek genetic alternatives. In poultry, companies like Hendrix Genetics have developed layer lines with enhanced resistance to Salmonella and E coli infections, which is helping reduce flock losses. In swine, the selection for the CD163 gene variant conferring resistance to Porcine Reproductive and Respiratory Syndrome has gained traction in Spain and Germany, where the disease costs the sector hundreds of millions of euros annually. Public research initiatives such as the EU-funded GenRes Bridge project further validate genetic markers linked to mastitis resistance in dairy cows. This convergence of regulatory pressure, economic loss mitigation, and scientific validation positions disease resilience as a cornerstone of modern animal genetics in Europe.

MARKET RESTRAINTS

Stringent EU Regulations on Genetic Modification and Gene Editing Limit Innovation Scope

The European Union’s restrictive regulatory framework governing genetic modification and emerging gene editing techniques, such as CRISPR Cas9, is one of the key restraints to the European market growth. Unlike conventional selective breeding, these advanced tools remain classified under the 2001 GMO Directive, which imposes prohibitive approval requirements, effectively halting commercial application in food animals. According to the European Court of Justice, a 2018 ruling reaffirmed that gene-edited organisms fall under GMO regulations regardless of whether foreign DNA is introduced. This contrasts sharply with policies in the United States, Brazil, and Argentina, where gene-edited hornless dairy cattle and disease-resistant pigs are already in field trials. Industry resistance to European animal genetics firms reports that regulatory uncertainty has discouraged R and D investment in precision breeding tools. The European Commission’s 2023 proposal to relax rules for certain gene-edited plants notably excludes animals, leaving the sector without a viable path for next-generation innovation. Consequently, European breeders rely solely on slower conventional methods while global competitors accelerate trait development.

Public Opposition to Intensive Breeding Practices Constrains Trait Selection Priorities

Persistent societal concerns about animal welfare and biodiversity loss have led to increasing scrutiny of intensive genetic selection practices, particularly those prioritizing productivity over health and adaptability, which is further hindering the animal genetics market growth in Europe. Consumer and NGO campaigns in countries like Germany, Sweden, and the Netherlands have pressured retailers and policymakers to restrict the use of genetics that contribute to welfare compromises such as fast growth in broilers or extreme leanness in pigs. According to Eurobarometer, a majority of EU citizens in 2023 agreed that breeding should prioritise animal health over higher yields. This sentiment has translated into policy as the Netherlands banned the use of certain high-performance broiler lines in 202, citing lameness and heart failure risks as confirmed by the Dutch Ministry of Agriculture. Similarly, the EU’s Farm to Fork Strategy calls for revising breeding goals to include robustness and longevity metrics. According to the reports from the European Food Safety Authority, current selection indices in poultry allocate limited weight to welfare-related traits. This misalignment between industry metrics and public expectations forces genetics companies to recalibrate breeding objectives often at the cost of short-term productivity gains, thereby slowing genetic progress in key commercial traits.

MARKET OPPORTUNITIES

Expansion of Precision Livestock Farming Creates Demand for Data-Integrated Genetics

The proliferation of precision livestock farming technologies across Europe is generating unprecedented demand for animal genetics that can be seamlessly integrated with real-time phenotypic data streams, which is a promising opportunity for the European animal genetics market. Sensors, automated feeders, and computer vision systems now continuously monitor individual animal behavior, ur health, and performance, enabling data-driven management decisions that require genetically informed baselines. According to the European Commission’s Digital Europe Programme, around 30% of large dairy farms in the EU utilised automated activity and rumination monitors in 2023, which is a figure projected to exceed 50% by 2027. This digital infrastructure creates value for genetics firms that link genomic predictions with on-farm sensor outputs. For instance, CRV’s Horizon platform in the Netherlands correlates genomic breeding values with milking robot data to predict feed efficiency at the individual cow level. Similarly, in poultry companies like Aviagen use camera-based weight estimation is used to validate growth genetics in real time. As per the studies from Wageningen University, farms using such integrated systems report higher lifetime productivity due to better matching of genetics to management. This convergence of biotechnology and digital agriculture opens new revenue models based on performance-based genetics rather than fixed product sales.

Growth of Alternative Proteins Spurs Genetic Innovation in Aquaculture Species

The rising investment in alternative protein systems has redirected attention toward genetic improvement of farmed aquatic species, which offer lower environmental footprints thaterrestrialtr,ial livestock, and this is further offering lucrative growth opportunities for the European market. Europe’s aquaculture sector, though modest compared to Asia, is strategically important for food security and is receiving targeted support under the EU’s Blue Economy agenda. According to the European Environment Agency, EU aquaculture production reached 1.1 million tonnes in 2023. Genetic advancements are critical for disease control and feed efficiency, as genomic approaches are being applied to address vibriosis challenges in species such as gilthead seabream. Additionally, the EU-funded AquaIMPACT project developed genomic and nutrition tools to improve feed conversion in salmon, which supports reductions in reliance on marine-derived feed ingredients. As per the European Commission, the Common Fisheries Policy promotes sustainable, science-based, and innovative aquaculture, including support for genetics-related advances. With global demand for seafood outpacing wild catch, this niche offers high-margin opportunities for specialized animal genetics firms aligned with Europe’s blue growth strategy.

MARKET CHALLENGES

Fragmented National Breeding Policies Undermine Cross-Border Genetic Exchange

The lack of harmonized breeding regulations across member states, which impedes the free movement and validation of genetic material, is a significant challenge to the European animal genetics market. While the EU established Zootechnical Regulation 2016 1012 to standardize breeding programs, national authorities retain significant discretion in approving breeding organizations and recording standards. According to the European Commission’s 2025 Single Market Scoreboard, several countries, including Italy, Poland, nd and Hungary, maintain additional national requir, eme,nts for semen and embryo imports that can hinder cross-border trade. As per the European Association of Cattle Breeders, this fragmentation increases administrative costs for multinational genetics firms and reduces genetic diversity in local populations. In Eastern Europe, inconsistent pedigree recording further limits the reliability of estimated breeding values. The absence of a centralized EU database for genomic data sharing hampers large-scale meta-analyses. Until full regulatory convergence is achieved, genetic progress will remain uneven and market access unpredictable across the European single market.

High Cost and Long Payback Periods Deter Small Producers from Adopting Advanced Genetics

The economic structure of European livestock farming creates a significant barrier to the adoption of premium genetic technologies, which further challenges the growth of the European animal genetics market. Advanced semen embryos and genomic testing often carry high upfront costs with benefits realized over multiple production cycles, which many smaller farms cannot afford. A majority of EU livestock farms operate on less than 20 hectares and have limited annual revenues, which limits investment capacity. The cost of a single genomic test for a dairy calf and elite beef semen per straw can be significant for small farms. National subsidy schemes exist, but coverage is inconsistent as few member states fully reimburse genomic testing under rural development programs. Consequently, many smallholders continue using locally available or older genetic lines despite lower long-term returns. This economic stratification not only slows overall genetic progress but also exacerbates productivity gaps between large commercial operations and traditional farms, thereby undermining the EU’s goal of inclusive agricultural modernization.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Animal Genetic Product, Testing Service, and Region. |

| Various Analyses Covered | Global, Regional , and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Genus Plc, Hendrix Genetics BV, Alta Genetics, CRV Holding B.V., Neogen Corporation, VetGen, Animal Genetics, Zoetis |

SEGMENTAL ANALYSIS

By Animal Genetic Product Insights

The genetic material segment accounted for the dominating share of the European animal genetics market in 2025. The dominance of the genetic material segment in the European market is driven by the widespread use of artificial insemination and embryo transfer technologies across dairy, beef, and swine sectors, which rely on cryopreserved semen and embryos for rapid genetic dissemination. In the EU, most dairy cows are artificially inseminated annually with premium genetics accessed through imported or domestically produced frozen semen. A key factor is cost efficiency, as elite dairy bulls can sire very large numbers of offspring via semen distribution compared to natural mating. National breeding organizations in countries like the Netherlands and Denmark operate large-scale semen collection and processing centers that supply both domestic and export markets. Additionally, the EU Zootechnical Regulation ensures standardized certification and traceability of genetic material, facilitating cross-border trade. The logistical advantages of storing and transporting frozen straws further reinforce this segment’s leadership over live animal transfers, which face higher costs, regulatory hurdles, and welfare concerns.

The live animals segment represents the fastest-growing segment in the European animal genetics market and is anticipated to grow at a CAGR of 6.4% over the forecast period, owing to the rising demand for foundation stock in emerging organic and regenerative farming systems that prioritize closed herd management and animal adaptability. Unlike conventional dairies that rely on I, elite live animals are sought after for their robustness, ess fertility, and pasture-based performance. According to FiBL, the EU’s organic farmland reached 10.9% of total agricultural area in 2023, with Germany,y Fra, and Sweden among the leaders in organic expansion. These systems often require live purchases to establish breeding nuclei, as artificial insemination is restricted under certain organic standards. Additionally, the rise of agro-tourism and non-farm direct sales in Southern Europe has increased demand for visually distinctive and docile live animals that enhance consumer experience. New small-scale livestock farms have been registering primarily in mountainous regions where live animal transport is more practical than liquid nitrogen logistics. This niche yet expanding demand repositions live animals as a strategic growth vector.

By Testing Service Insights

The genetic disease tests segment captured 40.9% of the regional market share in 2025. The growth of the genetic disease tests segment in the European market is attributed to the mandatory and voluntary screening programs aimed at eradicating hereditary disorders that compromise animal welfare and farm economics. Across EU breeding schemes, routine testing for monogenic diseases in cattle is widely implemented. National programs offer substantial incentives. In Germany, regional breeding associations reimburse testing costs for registered herds participating in disease eradication initiatives. Similarly, in swine, testing for Porcine Stress Syndrome is commonly required for AI boars in Denmark. The integration of disease markers into genomic selection indices further embeds testing into routine workflows. With the EU’s One Health framework emphasizing zoonotic risk reduction, farms increasingly adopt pre-breeding screening to prevent vertical transmission of pathogens. This regulatory and economic alignment ensures sustained demand for diagnostic genetic testing across species.

The genetic trait tests segment is promising and is estimated to witness a promising CAGR of 8.89% over the forecast period in the European market, owing to the shift toward multi-trait selection that balances productivity with sustainability and welfare metrics. Modern breeding goals now prioritize feed efficiency, methane emission reduction, meat tenderness, and longevity as these traits are measurable only through genomic markers. In dairy, the inclusion of methane-related evaluations in the Nordic Total Merit Index has increased trait test uptake since 2021. Similarly, in poultry, Aviagen’s European customers now routinely select broilers using genomic scores for leg health and feathering to comply with retailer welfare standards. The decreasing cost of high-throughput genotyping has democratized access even for mid-sized farms. Furthermore, the EU’s Farm Sustainability Tool for Nutrients requires farms to report on efficiency metrics that align directly with genetically influenced traits. This policy-driven demand transforms trait testing from a premium service into a mainstream management tool.

COUNTRY LEVEL ANALYSIS

Netherlands Animal Genetics Market Analysis

The Netherlands dominated the animal genetics market in Europe in 2025 by occupying 20.9% of the regional market share. The dominance of the Netherlands in Europe arises from its world-class dairy and poultry breeding infrastructure, centred around globally active cooperatives like CRV and Hendrix Genetics. The Netherlands exports genetic material to many countries, with bovine semen exports totaling around 32 million euros in 2023. The integration of national herd recording with genomic evaluation has also contributed to market growth in the Netherlands. A large share of Dutch dairy farms participate in the MPR performance recording system, which feeds data to the CRV genomic platform. The nation also hosts one of Europe’s largest AI stations in Heerenveen, processing millions of semen doses annually. Public-private partnerships such as the Top Sector Agri Food initiative allocate substantial annual funding to precision breeding R&D. This synergy of cooperative models, data infrastructure, and export orientation cements the Netherlands as Europe’s genetic innovation hub.

Denmark Animal Genetics Market Analysis

Denmark is a promising market for animal genetics in Europe and holds a substantial share of the European market in 2025. The growth of Denmark in the European market is attributed to its vertically integrated pig and dairy sector, where genetics are tightly aligned with production and processing chains. Danish Crown is a leading pork exporter and mandates the use of Landrace and Yorkshire genetics proven for lean meat yield and feed efficiency across its supplier farms. In dairy, Seges, a farmer-owned innovation body, manages the VikingGenetics alliance, which pioneered the Nordic Total Merit Index, now adopted by Sweden and Finland. The majority of breeding sows undergo mandatory genetic disease screening, ensuring a high health status. The nation also leads in methane efficiency genetics; research has shown measurable reductions in enteric emissions from genomically selected dairy cows. This combination of export leverage, cooperative governance, and climate-smart breeding sustains Denmark’s top-tier position.

Germany Animal Genetics Market Analysis

Germany occupied a notable share of the European animal genetics market in 2025. The dual focus of Germany on high-performance Holstein genetics in the north and robust dual-purpose breeds like Fleckvieh in the south, reflecting regional farming systems, is driving the German animal genetics market growth. Germany maintains Europe’s largest dairy herd, which is driving consistent demand for AI services and genomic testing. Strong public funding is also contributing to the German market expansion, with the Federal Ministry of Food and Agriculture supporting genomic selection in organic and grass-based systems. Additionally, consumer pressure for animal welfare has spurred the adoption of longevity and claw health traits now integrated into the German Holstein index. The presence of major genetics firms like VitusVet and LKV Bayern ensures nationwide service coverage. This balance of scale diversity and policy responsiveness maintains Germany’s central role in continental animal genetics.

France Animal Genetics Market Analysis

France is predicted to account for a considerable share of the European animal genetics market over the forecast period, owing to its emphasis on native breeds and grass-based systems, which shape unique selection priorities. Many officially recognized local breeds are managed under national conservation and improvement programs funded by the Common Agricultural Policy. In dairy, the Prim’Holstein program genotypes large numbers of animals annually, focusing on traits like udder health and pasture adaptability as per INRAE. France also leads in dual-purpose cattle genetics with widespread use of sexed semen in dairy herds to manage surplus male calves. The National Institute for Agricultural Research validates welfare-related genetic markers, ensuring alignment with the French Animal Welfare Strategy. This blend of heritage conservation, modern genomics, c,s, and ethical breeding secures France’s influential and distinct market role.

United Kingdom Animal Genetics Market Analysis

The United Kingdom is estimated to exhibit a healthy CAGR in the European animal genetics market during the forecast period. Post Brexit, the UK has intensified ed focus on genetic self-sufficiency and climate resilience to reduce import dependency and meet net zero targets. The Agricultural Transition Plan incentivizes the use of genetics and other innovations for methane reduction and improved efficiency. In sheep, the UK leads European development of the scrapie-resistant genotypes with a high prevalence of ARR alleles, as confirmed by the Animal and Plant Health Agency. Poultry genetics is dominated by Aviagen’s Ross lines, which supply a large share of UK broilers and are bred at the company’s Edinburgh headquarters for European welfare standards. The UK Genetics Partnership coordinates data sharing across farms to accelerate genetic gain. This strategic pivot toward sovereign sustainable genetics reinforces the UK’s enduring relevance despite regulatory divergence from the EU.

COMPETITIVE LANDSCAPE

The European animal genetics market features a concentrated yet dynamic competitive landscape dominated by cooperative models, farmer-owned entities, and multinational innovators. Unlike the commodity market, competition centers on genetic accuracy, service integration, and alignment with regulatory and societal expectations on animal welfare and sustainability. Leading players differentiate through proprietary genomic evaluation systems, data-driven advisory services, and breed-specific trait libraries validated under European conditions. National breeding programs in countries like the Netherlands, Denmark, and Germany create both collaboration opportunities and entry barriers for external firms. The absence of commercial gene editing approval maintains a level playing field, favoring firms with deep conventional breeding expertise. However, rising demand for climate-smart and welfare-oriented traits is encouraging partnerships between genetics companies, feed manufacturers, and food retailers to create end-to-end value chains. This evolving ecosystem rewards scientific depth, transparency, and the ability to translate complex genetic data into actionable on-farm outcomes.

KEY MARKET PLAYERS

Companies that play a significant role in the europe animal genetics market profiled in this report are

- Genus Plc,

- Hendrix Genetics BV,

- Alta Genetics,

- CRV Holding B.V.,

- Neogen Corporation,

- VetGen,

- Animal Genetics,

- Zoetis.

TOP LEADING PLAYERS IN THE MARKET

- CRV Holding B.V. is a leading cooperative in the European animal genetics market with deep roots in the Netherlands and operational reach across Germany, Belgium, and the United Kingdom. Specializing in dairy and beef cattle genetics, cs CRV offers genomic testing, artificial insemination, and herd management software. In 2023, CRV launched its Horizon Next platform, real-time farm data with genomic predictions to optimize breeding decisions. The company also expanded its sexed semen production capacity to support gender balanced herd strategies in response to EU animal welfare guidelines. CRV’s farmer-owned structure ensures alignment with producer needs while its export of elite genetics to over 80 countries reinforces its global influence in sustainable dairy breeding programs.

- Hendrix Genetics B.V. plays a pivotal role in the European animal genetics market through its multi-species portfolio covering poultry, swine,e salm, and turkeys. Headquartered in the Netherlands, the company operates research and breeding centers across France, Spain, and the United Kingdom. In early 2025, Hendrix Genetics introduced its TRAITS platform,m, which uses machine learning to predict welfare and efficiency traits in laying hens using genomic and phenotypic data. It also partnered with Norwegian aquaculture firms to deploy genomic selection for sea lice resistance in Atlantic salmon. These initiatives underscore Hendrix’s commitment to science-driven breeding that addresses both productivity and ethical concerns across global protein supply chains.

- Genus plc maintains a strong presence in the European animal genetics market primarily through its PIC division for swine and ABS division for dairy genetics. The company serves major pork and milk producers in Denmark, Germany, and Spain with advanced genomic and reproductive technologies. In 20,23 Genus completed the rollout of its Porcine Genomic Predicti3.03 0 model, which improves accuracy for feed efficiency and disease resilience traits. It also established a dedicated gene editing research unit in the UK focused on PRRS-resistant pigs, though commercial deployment remains pending regulatory clarity. Genus leverages its global R and D network to tailor solutions for European sustainability mandates while contributing foundational genetics to international breeding programs.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European animal genetics market are intensifying integration of genomic data with on-farm digital platforms to deliver precision breeding recommendations aligned with individual herd performance. Companies are expanding sexed and gender specific semen offerings to support animal welfare and resource efficiency goals under EU sustainability frameworks. Strategic collaborations with national breeding associations and research institutes are accelerating validation of novel traits such as methane emission reduction and disease resilience. Investment in high-throughput genotyping infrastructure is reducing testing costs and broadening access for mid-sized farms. Additionally, firms are developing multi-species genetic platforms that enable cross-commodity data insights while navigating regulatory constraints on gene editing through conventional genomic selection. These strategies collectively enhance value delivery while reinforcing compliance with Europe’s ethical and environmental standards.

MARKET SEGMENTATION

This research report on the europe animal genetics market has been segmented and sub-segmented into the following categories

By Animal Genetic Product

-

Live Animals

- Poultry

- Porcine

- Canine

- Bovines

- Other Animals

- Genetic Material

- Semen

- Bovine semen

- Porcine semen

- Canine semen

- Equine semen

- other animals

- Embryos

- Bovine embryo

- Equine embryo

- Other animals

- Semen

By Testing Service

- DNA Typing

- Genetic Trait Tests

- Genetic Disease Tests

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe