Europe Autonomous Mobile Robots Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Application, End-User, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$1.40 BnMarket Estimate, 2026

$1.72 BnMarket Forecast, 2034

$8.86 BnCAGR, 2026–2034

22.75%Europe Autonomous Mobile Robots Market Report Summary

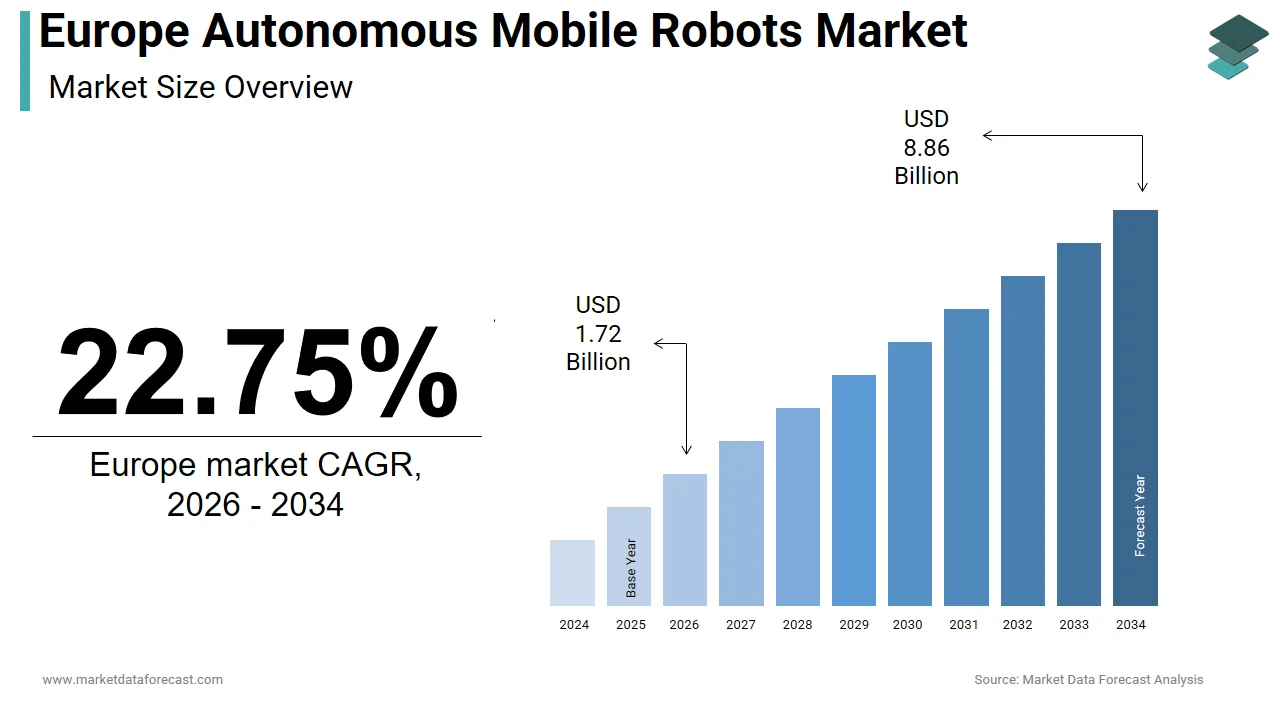

The Europe autonomous mobile robots market was valued at USD 1.40 billion in 2025, is estimated to reach USD 1.72 billion in 2026, and is projected to reach USD 8.86 billion by 2034, growing at a CAGR of 22.75% from 2026 to 2034. Market growth is driven by increasing automation in warehouses and manufacturing facilities, rising demand for efficient material handling solutions, and the rapid expansion of e-commerce across Europe. Autonomous mobile robots (AMRs) enhance operational efficiency, reduce labor dependency, and improve logistics workflows. Advancements in AI, machine vision, and navigation technologies, along with the growing need for flexible and scalable automation solutions, are further accelerating market growth.

Key Market Trends

- Rapid adoption of automation in warehouses and logistics operations.

- Increasing demand for efficient material handling and order fulfillment solutions.

- Growth of e-commerce and omnichannel retail logistics.

- Advancements in AI, machine vision, and robotic navigation systems.

- Rising focus on reducing labor costs and improving operational efficiency.

Segmental Insights

- Based on type, the goods-to-person (G2P) picking robots segment dominated the Europe autonomous mobile robots market by capturing 48.6% share in 2025, driven by efficiency in order picking processes.

- Based on application, the warehouse fleet management segment held the largest share of 39.2% in 2025, supported by the need for coordinated and optimized robotic operations.

- Based on end user, the warehouse & distribution centers segment led the market with 64.4% share in 2025, driven by high demand for automation in logistics and supply chain operations.

Regional Insights

The Europe autonomous mobile robots market is witnessing rapid growth across major countries due to increasing industrial automation and logistics modernization.

- Germany led the regional market in 2025 with 29.2% share, supported by strong manufacturing and logistics infrastructure.

- The United Kingdom followed with 17.1% share in 2025, driven by e-commerce growth and warehouse automation.

- France holds a significant position as a key hub for modernizing aerospace, automotive, and luxury goods supply chains.

Competitive Landscape

The Europe autonomous mobile robots market is highly competitive, with the presence of robotics manufacturers and automation solution providers. Market players are focusing on innovation, expanding product portfolios, and enhancing AI-driven capabilities. Strategic partnerships, acquisitions, and investments in advanced robotics technologies are shaping competitive dynamics across the region.

Prominent companies operating in the Europe autonomous mobile robots market include Material Handling Systems, Mobile Industrial Robots (MiR), Fetch Robotics, Inc., IAM Robotics, NextShift Robotics, Stanley Robotics, KION Group, Robotnik, Geek+, SESTO Robotics, HAHN Robotics GmbH, Vecna Robotics, AutoGuide Mobile Robots, and SoftBank Robotics.

Europe Autonomous Mobile Robots Market Size

The Europe autonomous mobile robots market was valued at USD 1.40 billion in 2025, is estimated to reach USD 1.72 billion in 2026, and is projected to reach USD 8.86 billion by 2034, growing at a CAGR of 22.75% from 2026 to 2034.

Autonomous Mobile Robots (AMRs) are intelligent, self-driving vehicles that can navigate and perform tasks in dynamic environments without human supervision or fixed infrastructure. Unlike traditional automated guided vehicles (AGVs), AMRs do not require fixed infrastructure such as magnetic tapes or embedded wires, enabling flexible deployment across warehouses, factories, hospitals, and retail spaces. The market is propelled by labor shortages, digital transformation mandates, and the EU’s push for resilient, future-proof supply chains. According to the EURES Report on Labour Shortages and Surpluses 2024, the EU continues to face acute labour shortages, with up to 98% of surveyed occupations reporting bottlenecks. In 2024, 80 percent of EU employers reported difficulties in recruiting workers with the right skills, particularly in manufacturing, logistics, and engineering. As per the European Commission's 'Path to the Digital Decade' 2030 targets, at least 75 percent of EU enterprises should adopt cloud computing services, big data, and/or Artificial Intelligence (AI) by 2030. Besides, over 90% of SMEs are expected to reach at least a basic level of digital intensity. This convergence of demographic pressure, policy incentives, and technological maturity positions AMRs not as experimental novelties but as essential enablers of operational continuity and competitiveness in a post pandemic, high-wage economy.

MARKET DRIVERS

Persistent Labor Shortages in Logistics and Manufacturing

The region’s aging workforce and declining interest in manual labor are accelerating AMR adoption as a strategic response to operational fragility, which acts as a major booster for the growth of the Europe autonomous mobile robots market. European manufacturing and logistics sectors face severe, widespread recruitment difficulties for production and warehouse roles in 2024–2025, with Germany experiencing a critical, deepening shortage of skilled labour across multiple industries due to demographic shifts. The problem is structural. The European Union is experiencing significant demographic aging, which is tightening the labor supply, while the logistics and warehousing sector faces challenges in attracting younger talent due to low interest and, in some cases, demanding work conditions. In response, companies like Zalando and Bosch have deployed fleets of AMRs to maintain throughput without expanding headcount. Research from the Fraunhofer Institute indicates that the integration of Automated Mobile Robots (AMRs) in e-commerce fulfillment centers is a key technology for enhancing productivity and mitigating the impact of labor shortages, particularly by automating repetitive, physically demanding tasks. This shift is not merely cost-driven but existential, ensuring business continuity in an era where human labor is increasingly scarce, expensive, and unreliable.

EU Policy Mandates for Digitalization and Supply Chain Resilience

The European Commission’s strategic frameworks are creating powerful tailwinds for AMR deployment across critical sectors, which further contributes to the expansion of the Europe autonomous mobile robots market. The Digital Europe Programme is investing a significant portion of its 2025–2027 budget, focused on AI deployment, to enhance the adoption of advanced technologies like robotics among European small and medium-sized enterprises. Simultaneously, the Chips Act and Critical Raw Materials Act emphasize secure, localized production, pushing manufacturers to automate internal logistics to reduce dependency on just-in-time global supply chains. The European Investment Bank is financing industrial automation and digitalization projects to strengthen the competitiveness and resilience of European companies. The Green Deal further incentivizes AMRs through energy efficiency criteria. Electric autonomous mobile robots offer higher energy efficiency for material handling compared to traditional forklifts, resulting in lower energy consumption per unit of transport. These overlapping policy levers transform AMR investment from a discretionary upgrade into a compliance and competitiveness imperative, particularly for companies seeking public funding or export certification.

MARKET RESTRAINTS

High Initial Investment and Integration Complexity

The total cost of ownership for AMR systems remains prohibitive for many small and medium enterprises, despite falling unit costs, which hinders the growth of the Europe autonomous mobile robots market. Studies indicate that a mid-sized Autonomous Mobile Robot (AMR) fleet requires substantial investment in hardware, software, and integration, often exceeding low-end cost estimates. Unlike plug-and-play machinery, AMRs demand Wi-Fi 6 coverage, digital twin modeling, and workflow redesign, often requiring external consultants. A survey of industrial companies found that a significant majority of small and medium-sized enterprises (SMEs) are delaying AMR adoption due to uncertainties regarding return on investment and a lack of in-house technical expertise. Furthermore, interoperability gaps between legacy warehouse management systems and new AMR fleets create data silos that undermine efficiency gains. These barriers confine large-scale adoption to multinational corporations and well-capitalized logistics firms, slowing the democratization of automation across Europe’s fragmented industrial base.

Fragmented Safety and Operational Standards Across Member States

Varying national interpretations of AMR protocols create compliance uncertainty and slow down the expansion of the Europe autonomous mobile robots market. This is the case despite the EU's harmonized machinery safety regulation 2023/1230. Countries like Germany enforce stringent requirements under DGUV V18 guidelines for human-robot interaction, while France and Italy apply more flexible risk-based assessments. Divergent implementation of safety standards across European member states complicates the cross-border deployment of autonomous mobile robots. Additionally, the lack of harmonized local safety certifications in cross-border logistics hubs frequently causes significant delays in the deployment of autonomous mobile robot pilot projects. Additionally, the absence of standardized metrics for performance benchmarking, such as obstacle avoidance latency or battery degradation under load, makes vendor comparison difficult. This regulatory patchwork increases time to deployment, inflates legal costs, and discourages startups from entering the market, ultimately fragmenting innovation and limiting economies of scale.

MARKET OPPORTUNITIES

Expansion into Healthcare and Hospital Logistics

Hospitals across the region are emerging as high-growth arenas for AMR deployment and the overall Europe autonomous mobile robots market. The need for infection control, staff retention, and operational efficiency drives this growth. Nursing staff in many European hospitals spend a significant portion of their shifts on logistical tasks, such as transporting materials, which reduces the time available for direct patient care. Karolinska University Hospital in Sweden has adopted robotic technology to manage logistical tasks, improving efficiency, reducing errors, and relieving staff of manual transportation duties. Similarly, Germany’s Charité hospital employs automated mobile robots to enhance the accuracy and efficiency of pharmacy logistics, reducing errors in medication delivery. The EU’s Health Emergency Preparedness and Response Authority now recommends autonomous logistics as part of pandemic resilience planning. The vast EU hospital market and increasing cost pressures create a high-stakes, lucrative opportunity for AMR vendors capable of meeting strict hygiene, noise, and cybersecurity standards.

Integration with Circular Economy and Sustainable Logistics

AMRs are increasingly positioned as enablers of green logistics and pave the way for new opportunities for the Europe autonomous mobile robots market. This aligns with the EU’s Circular Economy Action Plan and Corporate Sustainability Reporting Directive. Electric Autonomous Mobile Robots (AMRs) eliminate operational emissions and improve energy efficiency compared to traditional manual forklift alternatives, according to broader sustainability research. Companies like IKEA and Decathlon now use AMRs in reverse logistics hubs to sort returned goods for resale, repair, or recycling, processes that require precise item handling and traceability. Automated sorting technologies, including AMRs, are recognized as tools to improve reuse rates in e-commerce returns, notes the European Environment Agency. Furthermore, AMRs equipped with RFID and vision systems enable real-time material tracking, supporting extended producer responsibility schemes. Sustainability is increasingly becoming a board-level priority. Consequently, AMR vendors who embed circularity metrics, such as carbon saved per mission or waste diverted, into their software platforms gain a decisive edge in public and corporate procurement.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Connected Robot Fleets

The integration of AMRs into critical infrastructure creates new, perilous cyber vulnerabilities that negatively impact the growth of the Europe autonomous mobile robots market. These vulnerabilities could paralyze supply chain operations. Most AMRs rely on cloud-based fleet management systems and Wi-Fi networks, creating multiple attack vectors for ransomware or data exfiltration. According to ENISA, industrial IoT incidents in manufacturing and logistics sectors are rising, with threat actors frequently exploiting vulnerabilities in unpatched firmware and weak authentication protocols to disrupt operations. Security simulations and threat assessments conducted in smart manufacturing environments demonstrate that compromising Automated Mobile Robots (AMRs) can lead to critical physical disruptions, including operational stoppages and the creation of safety hazards within the facility. Current AMR security standards lack mandatory encryption or zero-trust architectures, leaving fleets vulnerable. The EU’s upcoming Cyber Resilience Act will require stricter design safeguards, but retrofitting existing units will be costly. Until robust, standardized cybersecurity is embedded by design, organizations remain hesitant to deploy AMRs in high-value or safety-critical environments.

Interoperability Gaps in Multi-Vendor Robotic Ecosystems

The absence of universal communication protocols hinders seamless collaboration between AMRs from different manufacturers, and thereby constrains the expansion of the Europe autonomous mobile robots market. It also prevents these robots from working effectively with other smart factory systems. Initiatives like the MassRobotics Interoperability Standard and VDA 5050 exist. However, adoption remains voluntary and inconsistent. Despite the development of industry standards, many autonomous mobile robot deployments continue to struggle with seamless integration into existing warehouse systems and different robot brands, according to industry trends discussed at robotics forums. This forces companies to standardize on a single vendor, limiting flexibility and inflating long term costs. Integrating autonomous mobile robots from multiple suppliers often involves significant custom software development, resulting in substantial, unforeseen integration costs for logistics providers. Without mandated open APIs and common data models, the vision of heterogeneous robot fleets working in concert remains unrealized. This fragmentation stifles innovation, locks customers into proprietary ecosystems, and delays the realization of truly adaptive, intelligent logistics networks across Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, End-User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Material Handling Systems, Mobile Industrial Robots (MiR), Fetch Robotics, Inc., IAM Robotics, NextShift Robotics, Stanley Robotics, KION Group, Robotnik, Geek+, SESTO Robotics, HAHN Robotics GmbH, Vecna Robotics, AutoGuide Mobile Robots, SoftBank Robotics, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The goods-to-person (G2P) picking robots segment led the Europe autonomous mobile robots market and captured a 48.6% share in 2025. The leading position of the segment is supported by its transformative impact on e-commerce fulfillment and retail distribution. The explosive growth of online shopping has intensified pressure on warehouses to reduce order cycle times while maintaining accuracy. According to Eurostat, the percentage of EU internet users buying online is growing, with rising consumer demand for fast delivery options. Goods-to-Person (G2P) automation, such as solutions from Geek+ and Locus Robotics, allows workers to remain stationary while inventory is brought to them, increasing picking rates and reducing walking time. Furthermore, Zalando has expanded its use of G2P robot technology to improve operational efficiency and decrease order processing times. Unlike manual picking or conveyor systems, G2P offers scalable throughput without facility redesign, making it ideal for seasonal demand spikes. Consumer expectations for speed and reliability are hardening. Consequently, G2P has become the de facto standard for high-volume, high-mix retail logistics across Western Europe. Warehouses in major European logistics hubs, including Poland and the Netherlands, face significant, ongoing challenges with high labor turnover and finding staff, leading to increased efforts in adopting automation to address these shortages. G2P robots reduce reliance on transient labor by simplifying picker tasks to stationary selection, lowering training time from weeks to hours. Studies on warehouse automation indicate that implementing Goods-to-Person systems improves worker well-being and reduces safety incidents by significantly decreasing the need for manual walking, bending, and heavy lifting. Companies like Decathlon and Otto Group now prioritize G2P not just for efficiency but for workforce retention, offering ergonomic, less physically demanding roles that attract older and part-time workers. This human-centric automation model aligns with EU social sustainability goals, ensuring G2P remains the cornerstone of warehouse modernization.

The autonomous inventory robot segment is expected to exhibit a noteworthy CAGR of 24.6% from 2026 to 2034 due to the need for real-time stock visibility and loss prevention. Retailers face mounting pressure to maintain accurate stock levels across physical stores, e-commerce, and click-and-collect channels. Inaccurate inventory leads to lost sales. Various sources indicate that inventory inaccuracies, including phantom inventory and stockouts, cause significant revenue losses and margin erosion for retailers. Autonomous inventory robots utilizing computer vision significantly improve inventory accuracy and frequency compared to traditional manual audit methods, which are prone to inaccuracies. Carrefour is upgrading its French hypermarkets with digital shelf technologies and IoT cameras to improve product availability and reduce inventory errors. EU consumers increasingly expect seamless omnichannel experiences. As a result, real-time inventory has become a competitive necessity, transforming these robots from experimental tools into core retail infrastructure. Modern inventory robots feed data directly into AI platforms that predict stockouts, optimize replenishment, and detect shrinkage patterns. The REWE Group is investing heavily in digital infrastructure, using cloud-based systems and AI to optimize inventory management, reduce overstock, and minimize markdowns. The system flagged unusual movement patterns, such as repeated handling without purchase, as potential theft, enabling targeted security responses. A significant portion of large retailers is accelerating the adoption of automated, AI-driven inventory systems to comply with enhanced supply chain transparency regulations, such as the Corporate Sustainability Reporting Directive. This convergence of loss prevention, sustainability, and predictive analytics positions autonomous inventory robots as the fastest-growing and most strategically vital AMR segment in European retail.

By Application Insights

The warehouse fleet management segment captured the majority share of 39.2% of the Europe autonomous mobile robots market in 2025. The supremacy of the segment is attributed to the critical need to coordinate heterogeneous robot fleets in complex logistics environments. Modern warehouses often deploy dozens of AMRs from different manufacturers, G2P units, tuggers, and forklifts that must operate without collision or congestion. Centralized fleet management software, such as that from MiR and 6 River Systems, uses AI to assign tasks, optimize traffic flow, and dynamically reroute robots around obstacles. VDMA reports indicate that consolidating heterogeneous robot fleets through unified fleet management software, rather than operating in silos, significantly enhances operational uptime and reduces idle time. DHL has implemented advanced orchestration technology in its European hubs to integrate robots from multiple vendors into a single control layer, improving coordination between various logistics zones. As AMR adoption scales beyond pilot projects, fleet intelligence becomes the primary determinant of operational success. In this phase, the capability of the individual robot is less critical than the overall coordination of the fleet. Fleet management platforms now incorporate predictive maintenance and battery optimization algorithms that extend hardware life and reduce downtime. By analyzing motor current, wheel slippage, and charging cycles, these systems forecast failures up to 72 hours in advance. DB Schenker is incorporating AI-driven predictive maintenance to better anticipate vehicle health issues, aimed at reducing unplanned downtime. Additionally, dynamic battery swapping schedules ensure continuous operation during peak shifts, eliminating the need for oversized fleets. According to Eurostat, industrial electricity prices in Europe, while remaining above pre-2022 levels, began stabilizing or slightly decreasing in 2024 after reaching extreme highs. As energy costs rise, these efficiency gains translate into significant cost savings, making fleet management software indispensable for ROI realization in large-scale AMR deployments.

The tugging application segment is predicted to witness the highest CAGR of 22.3% during the forecast period, owing to its versatility in manufacturing and cross-dock logistics. Tugger AMRs excel in moving carts, bins, and pallets between production lines, warehouses, and loading docks without fixed infrastructure. Unlike conveyors, they adapt instantly to layout changes, a critical advantage in industries like automotive and electronics, where product cycles shorten annually. BMW's plant in Munich integrates automated guided vehicles and autonomous mobile robots from various providers to automate internal logistics, supporting just-in-sequence delivery and optimizing employee tasks in production. A significant portion of automotive Tier 1 suppliers are adopting automated guided vehicles and autonomous mobile robots, including tugger variants, to enhance lean manufacturing and improve material flow. Their ability to integrate with existing industrial carts via standardized hitches lowers adoption barriers, making them the fastest path to automation for mid-sized manufacturers. In urban distribution centers, tugger AMRs shuttle goods from inbound trailers to outbound vans within tight time windows. Deutsche Post DHL is increasing the use of automation, including robotic solutions and electric transport, in its urban micro-hubs to optimize last-mile delivery and speed up parcel processing. With EU cities imposing stricter emissions and noise limits, over 300 low-emission zones are active in 2024 per the European Environment Agency, electric tuggers offer a zero-emission alternative to diesel tugs. Their compact size and precise navigation enable operation in narrow alleys and pedestrian zones, supporting the shift toward sustainable last-mile delivery. This dual applicability in both factory and city logistics ensures sustained high growth for tugging applications across Europe.

By End User Insights

The warehouse & distribution centers segment was the largest segment in the Europe autonomous mobile robots market and held a 64.4% share in 2025 because of e-commerce pressures and the relative ease of AMR deployment in controlled indoor environments. Warehouses offer predictable layouts, flat floors, and minimal dynamic obstacles, ideal conditions for AMR navigation using LiDAR and SLAM algorithms. Unlike factories with cranes, forklifts, and open pits, distribution centers require minimal facility modification for AMR deployment. E-commerce companies are increasing their use of Autonomous Mobile Robots to enhance speed and flexibility in logistics hubs, allowing for quicker deployment of automation, though full facility implementation often takes longer than a couple of weeks. The standardization of racking, bin sizes, and workflows further simplifies integration. A significant majority of leading online retailers in Europe are adopting Autonomous Mobile Robots and automated sorting technologies to achieve substantial gains in warehouse productivity. This low-friction adoption path makes warehouses the natural beachhead for AMR technology in Europe. E-commerce experiences extreme seasonality. The peak holiday shopping season, running from Black Friday through Christmas, generates a massive portion of annual e-commerce volume, placing extreme demand on logistics capacity in a short timeframe. AMRs provide unmatched scalability: robots can be leased, redeployed, or idled based on demand, avoiding the fixed costs of permanent labor or conveyor systems. E-commerce retailers are increasingly leveraging AI and automated warehouse technology, such as autonomous robots, to increase logistics throughput and boost operational efficiency during peak demand periods without relying solely on temporary staff. This elasticity is crucial in a labor-tight market where temporary workers are scarce and unreliable. As same-day delivery expands, warehouses must maintain high throughput year-round, cementing AMRs as essential infrastructure rather than optional automation.

The manufacturing end-user segment is estimated to register the fastest CAGR of 28.7% over the forecast period. The swift expansion of the segment is fuelled by Industry 4.0 mandates and resilient supply chain strategies. Modern manufacturing relies on lean principles where components arrive at assembly stations minutes before use. AMRs enable this precision by replacing scheduled forklift routes with on-demand delivery triggered by production line signals. Siemens' electronics manufacturing plants are utilizing autonomous mobile robots (AMRs) to automate PCB transportation, resulting in enhanced logistics efficiency, reduced work-in-progress inventory, and optimized floor space. EU manufacturers are increasing the integration of autonomous mobile robots with Manufacturing Execution Systems (MES) to enable real-time tracking of materials and improve shop floor efficiency. This integration minimizes bottlenecks and supports mass customization, critical for industries like automotive and machinery facing volatile demand. Geopolitical instability and pandemic disruptions have accelerated EU efforts to reshore production. The Chips Act and Critical Raw Materials Act incentivize local manufacturing, but high labor costs necessitate automation. AMRs offer a cost-effective path to automate internal logistics without a massive facility overhaul. Amidst high wage costs and global supply chain shifts, German manufacturers are increasingly investing in automation, including AMR deployment, to make reshoring initiatives economically viable. Companies like Bosch and Schneider Electric now design new factories around AMR workflows from day one, embedding charging stations and traffic rules into blueprints. Europe is building sovereign production capacity in semiconductors, batteries, and medical devices. Consequently, AMRs are becoming foundational to competitive, resilient, and future-proof manufacturing ecosystems.

COUNTRY-LEVEL ANALYSIS

Germany Autonomous Mobile Robots Market Analysis

Germany led the Europe autonomous mobile robots market and captured a 29.2% share in 2025. This position of the German market is propelled by its status as the manufacturing heartland of the continent and the birthplace of Industry 4.0. The market status in this region is showing a deep integration of autonomous mobile robots into complex automotive assembly lines and sophisticated logistics hubs where precision and reliability are paramount. A major driving factor is the severe shortage of skilled labor in the industrial sector, which has forced manufacturers to accelerate automation adoption to maintain productivity levels. According to the German Engineering Federation (VDMA), the robotics and automation industry faced a challenging domestic market in 2024 with a notable decrease in domestic orders, though export demand to specific regions provided some balance. The presence of global technology leaders like Siemens and KUKA fosters a robust ecosystem for research and development, ensuring continuous innovation in navigation algorithms and collaborative capabilities. Furthermore, the government's High Tech Strategy 2025 provides substantial funding for projects that integrate artificial intelligence with robotics, lowering the barrier for small and medium enterprises to adopt these technologies. Research from the Fraunhofer Institute (IPA) and other research bodies highlights that while the use of autonomous mobile robots for internal logistics is a top priority for large manufacturers, widespread deployment remains focused on specific high-volume sectors like automotive and electronics. This combination of industrial necessity, technological prowess, and supportive policy ensures Germany remains the dominant force in the regional landscape.

United Kingdom Autonomous Mobile Robots Market Analysis

The United Kingdom followed closely behind in the Europe autonomous mobile robots market and occupied a 17.1% share in 2025. This growth of the UK market is fuelled by its rapid adoption of automation within the e-commerce fulfillment and healthcare sectors. The UK market sees a surge in demand for flexible logistics solutions capable of handling the volatility of online retail volumes and addressing critical staffing gaps in the National Health Service. A major driving factor is the post-Brexit labor market constraints which have made it difficult for warehouses and hospitals to recruit sufficient manual workers, thereby accelerating the shift toward autonomous operations. Data from Automate UK (BARA) indicates that while the manufacturing sector reached record installation levels recently, the adoption of autonomous mobile robots in distribution centers is growing as retailers seek to improve efficiency in the face of persistent labor challenges. The healthcare sector has also emerged as a unique growth vector, using these robots for transporting linen, meals, and medical supplies to free up nursing staff for patient care. Analysis from the Office for National Statistics (ONS) continues to show labor shortages in the logistics sector, which industry experts identify as a primary driver for the increased adoption of automated picking and sorting systems. Furthermore, the strong presence of innovative startups and research universities drives the development of advanced perception systems tailored for dynamic human environments. Through initiatives like the Advanced Manufacturing Plan, the UK government provides support for high-tech innovation, aiming to establish the country as a leader in autonomous systems and robotic integration across the supply chain.

France Autonomous Mobile Robots Market Analysis

France plays a vital role in the Europe autonomous mobile robots market by serving as a critical hub for the modernization of its aerospace, automotive, and luxury goods supply chains. A nationwide strategic initiative characterizes this region's market, which promotes the digital transformation and automation of conventional manufacturing processes. The primary driver is the need to enhance competitiveness against global rivals by reducing production costs and improving supply chain resilience through flexible automation. The Alliance for Industry of the Future (AIF) show that France is experiencing a steady rise in industrial automation investments, with a significant emphasis on integrating mobile robotics into large-scale manufacturing and logistics hubs. The aerospace sector, dominated by giants like Airbus, utilizes these robots for moving heavy components across vast assembly halls, requiring high payload capacities and precise navigation. Additionally, the booming e-commerce sector in France has led to the construction of massive automated fulfillment centers near major urban areas, driving demand for swarm robotics solutions. According to the Federation of Mechanical Industries (FIM), the food and beverage sector has emerged as a key adopter of autonomous mobile robots, driven by the need to maintain high hygiene standards and address a shortage of specialized labor. The government's France 2030 investment plan specifically allocates funds for robotics and AI, fostering a conducive environment for both domestic manufacturers and international integrators to expand their operations.

Italy Autonomous Mobile Robots Market Analysis

Italy is moving ahead steadfastly in the Europe autonomous mobile robots market because it is known for its specialized application of autonomous systems in the fashion, food and beverage, and ceramic tile industries. The Italian market is unique due to the prevalence of small and medium-sized enterprises that require scalable and cost-effective automation solutions to maintain their global export competitiveness. A key driving factor is the need to modernize historic manufacturing districts without disrupting existing layouts, making flexible autonomous mobile robots an ideal choice over fixed conveyor systems. The ceramic tile cluster in Sassuolo has become a global showcase for autonomous logistics, where fleets of robots manage the movement of heavy materials in harsh environments. According to sources, the average age of the workforce in traditional manufacturing sectors has prompted companies to invest in cobots and mobile robots to assist aging employees and reduce physical strain. Furthermore, the strong design culture in Italy influences the development of aesthetically pleasing and user-friendly robotic interfaces. As per studies, the integration of autonomous mobile robots with enterprise resource planning systems is becoming standard practice, allowing Italian manufacturers to achieve real-time visibility and optimization of their internal logistics flows.

Sweden Autonomous Mobile Robots Market Analysis

Sweden is anticipated to grow notably in the Europe autonomous mobile robots market over the forecast period. The country is functioning as a pioneer in the development and deployment of autonomous solutions for intralogistics and sustainable supply chain management. The market status in this region is defined by a strong cultural emphasis on innovation, sustainability, and early adoption of cutting-edge technologies across all industrial sectors. A major driving factor is the presence of global logistics and retail giants like IKEA and H&M, who are aggressively automating their distribution networks to meet consumer demands for speed and transparency while adhering to strict environmental goals. Research indicates that the country has one of the highest densities of operational autonomous mobile robots per capita in Europe, with widespread use in warehouse order picking and material handling. The Swedish government's commitment to becoming a carbon-neutral nation has spurred interest in electric and energy-efficient autonomous platforms that optimize route planning to minimize power consumption. Furthermore, the collaboration between leading technical universities and industry players fosters a vibrant ecosystem for testing and refining new navigation technologies in real-world scenarios. As per sources, public funding programs continue to support projects that demonstrate the potential of autonomous robots to enhance productivity and working conditions, ensuring Sweden remains a vital and innovative segment of the European market.

COMPETITIVE LANDSCAPE

The Europe autonomous mobile robots market features intense rivalry among European innovators, global logistics technology firms, and agile startups. Established players like MiR and KION leverage deep industrial integration and compliance with EU safety standards, while international entrants such as Geek+ compete on AI sophistication and cloud scalability. The market is increasingly defined by software differentiation, fleet intelligence, predictive maintenance, and energy optimization rather than hardware alone. Fragmentation persists due to varying national interpretations of machinery safety directives, though harmonization efforts under the EU Machinery Regulation are progressing. Competition is also shaped by the ability to offer end-to-end solutions, including integration services and training, which are critical for ROI realization in complex environments. As adoption moves beyond pilot projects to enterprise scale, vendors with robust ecosystems, local support, and open architectures are gaining a decisive advantage in this rapidly evolving landscape.

KEY MARKET PLAYERS

The leading companies operating in the Europe autonomous mobile robots market include:

- Material Handling Systems.

- Mobile Industrial Robots (MiR)

- Fetch Robotics, Inc.

- IAM Robotics

- NextShift Robotics

- Stanley Robotics

- KION Group

- Robotnik

- Geek+

- SESTO Robotics

- HAHN Robotics GmbH

- Vecna Robotics

- AutoGuide Mobile Robots

- SoftBank Robotics

TOP PLAYERS IN THE MARKET

- Headquartered in Denmark, Mobile Industrial Robots is a leading European developer of autonomous mobile robots for industrial and logistics applications. MiR’s fleet of AMRs, including the MiR250 and MiR1350, are deployed in numerous countries, serving automotive, electronics, and e-commerce sectors with flexible material transport solutions. The company emphasizes open software architecture and seamless integration with existing ERP and warehouse management systems. It also expanded its European training academy network to certify integrators in Germany, France, and Poland, accelerating deployment speed and ensuring standardized implementation across the region.

- Although founded in China, Geek+ has established a strong European footprint through its regional headquarters in Germany and fulfillment centers in the Netherlands and Spain. The company specializes in goods-to-person and sorting AMR solutions for retail and e-commerce clients, with deployments at major brands like Decathlon and Zalando. Geek+ leverages AI-driven fleet optimization to maximize throughput in high-density environments. Its localized support teams and compliance with EU data privacy regulations have strengthened trust among European enterprises seeking scalable, cloud native automation.

- Based in Germany, KION Group is a global leader in intralogistics, integrating AMRs through its subsidiaries Dematic and Egemin Automation. The company offers end-to-end solutions combining self-driving forklifts, tugger AMRs, and warehouse execution software tailored for manufacturing and distribution. KION’s strength lies in its deep integration with industrial supply chains and legacy material handling equipment. It also partnered with Siemens to embed AMR traffic management into the Xcelerator digital ecosystem, enabling real-time synchronization with production lines and energy systems across smart factories in Europe.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe autonomous mobile robots market are prioritizing open software architectures to enable interoperability with third-party robots and legacy systems. They are investing in AI-driven fleet orchestration platforms that optimize task allocation, energy use, and traffic flow in real time. Companies are establishing regional training academies and certified integrator networks to accelerate deployment and ensure quality implementation. Strategic partnerships with industrial automation leaders like Siemens and SAP enhance integration with broader digital factory ecosystems. Additionally, manufacturers are localizing data processing and support services to comply with EU cybersecurity and privacy regulations while building customer trust in mission-critical operations.

MARKET SEGMENTATION

This research report on the Europe autonomous mobile robots market has been segmented and sub-segmented into the following categories.

By Type

- Goods-to-person Picking Robots

- Self-driving Forklifts

- Autonomous Inventory Robots

- Unmanned Aerial Vehicles

By Application

- Sorting

- Pick & Place

- Tugging

- Warehouse Fleet Management

- Others

By End-User

- Warehouse & Distribution Centers

- Manufacturing

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe autonomous mobile robots market?

The Europe autonomous mobile robots market delivers self-driving material handlers for warehouses using laser guidance and AI pathfinding. Germany leads adoption in automotive logistics.

How does the Europe autonomous mobile robots market operate?

The Europe autonomous mobile robots market operates through integrators deploying fleets with central software. Real-time fleet optimization maximizes throughput in dynamic environments.

What drives growth in the Europe autonomous mobile robots market?

Growth in the Europe autonomous mobile robots market stems from e-commerce expansion and labor shortages. Intralogistics automation addresses rising order fulfillment demands efficiently.

Which countries lead the Europe autonomous mobile robots market?

Germany and Netherlands lead the Europe autonomous mobile robots market with advanced logistics hubs. Sweden follows via robotics research and manufacturing excellence.

What types dominate the Europe autonomous mobile robots market?

Goods-to-person and tugger AMRs dominate the Europe autonomous mobile robots market for picking and towing. Collaborative models work alongside human operators safely.

How does navigation work in the Europe autonomous mobile robots market?

Navigation in the Europe autonomous mobile robots market uses SLAM, LiDAR, and QR codes. Natural feature recognition enables deployment without facility modifications.

What role does warehousing play in the Europe autonomous mobile robots market?

Warehousing drives the Europe autonomous mobile robots market optimizing order picking and inventory transport. Multi-robot fleets handle peak season volumes effectively.

How does regulation shape the Europe autonomous mobile robots market?

Regulation via Machinery Directive governs the Europe autonomous mobile robots market ensuring collision avoidance. ISO safety standards enable human-robot coexistence safely.

What trends define the Europe autonomous mobile robots market?

Trends in the Europe autonomous mobile robots market include 5G connectivity and edge AI processing. Modular payloads adapt robots for diverse material handling tasks.

What challenges face the Europe autonomous mobile robots market?

Challenges in the Europe autonomous mobile robots market involve mixed traffic navigation and battery management. Advanced sensors resolve dynamic environment complexities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com