Europe Autonomous Vehicles Market Size, Share, Trends, and Growth Analysis Report, Segmented by Vehicle Type, Application, Level of Autonomy, and Country – Industry Forecast From 2026 to 2034

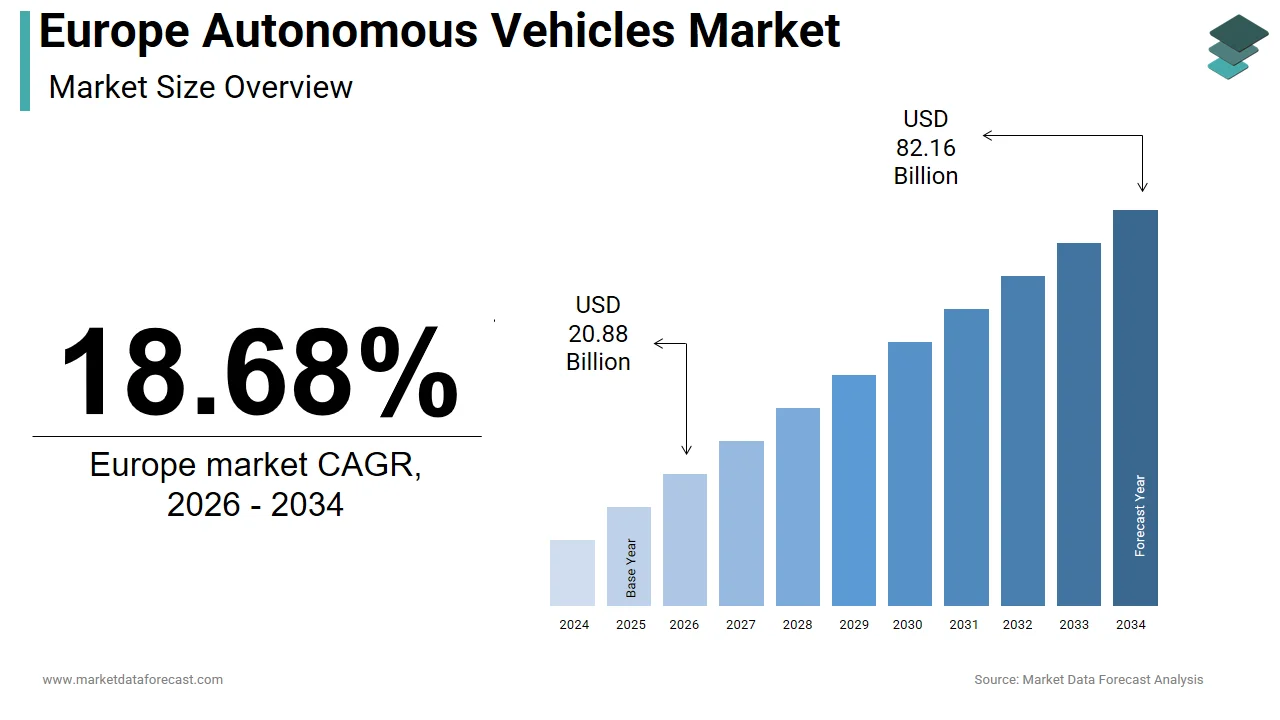

Market Size, 2025

$17.59 BnMarket Estimate, 2026

$20.88 BnMarket Forecast, 2034

$82.16 BnCAGR, 2026–2034

18.68%Europe Autonomous Vehicles Market Report Summary

The Europe autonomous vehicles market was valued at USD 17.59 billion in 2025, is estimated to reach USD 20.88 billion in 2026, and is projected to reach USD 82.16 billion by 2034, growing at a CAGR of 18.68% from 2026 to 2034. Market growth is driven by rapid advancements in artificial intelligence, sensor technologies, and connected vehicle infrastructure. Increasing investments by automotive manufacturers and technology companies, along with supportive government regulations for autonomous mobility, are accelerating adoption. Additionally, rising demand for safer and more efficient transportation systems and the development of smart cities are further supporting market expansion.

Key Market Trends

- Rapid advancements in AI, sensors, and autonomous driving technologies.

- Increasing focus on vehicle safety and accident reduction.

- Growth in connected vehicles and smart mobility ecosystems.

- Rising investments in autonomous mobility and R&D initiatives.

- Supportive government policies and pilot programs across Europe.

Segmental Insights

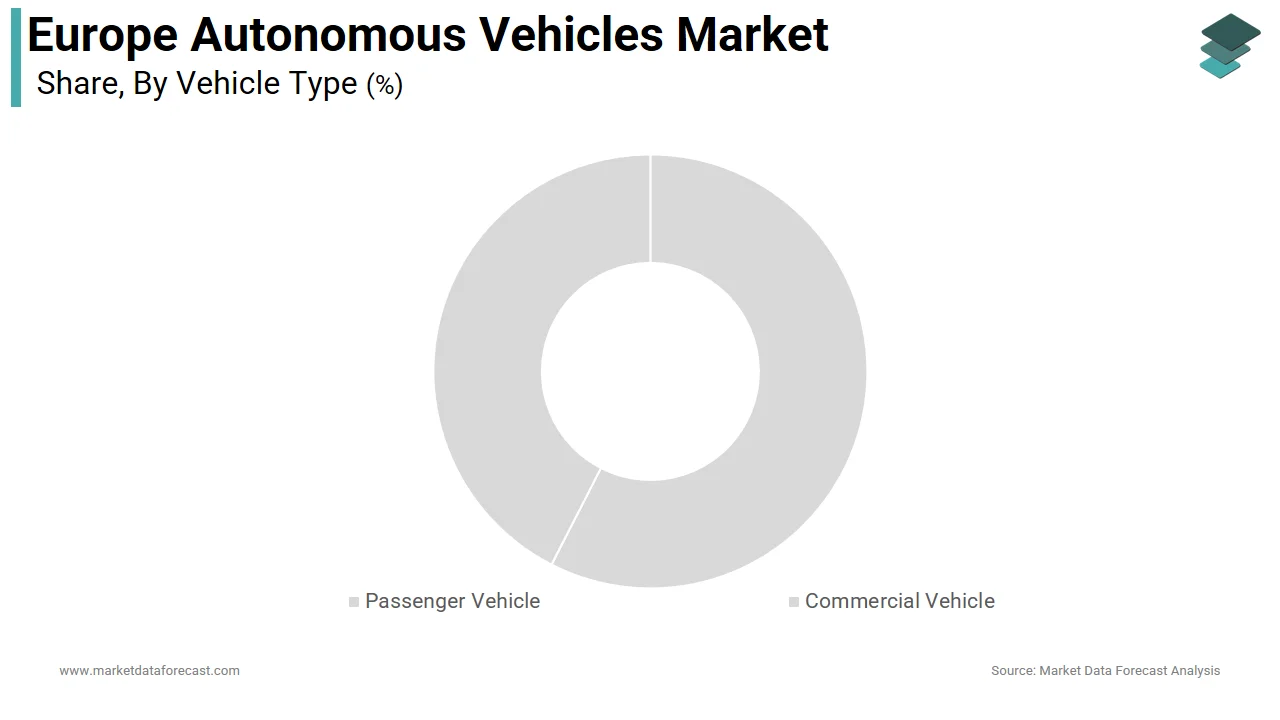

- Based on vehicle type, the passenger vehicles segment dominated the Europe autonomous vehicles market by capturing 60.8% share in 2025, driven by high consumer demand and production volumes.

- Based on application, the transportation segment held the largest share in 2025, supported by increasing adoption in mobility services and logistics.

- Based on level of autonomy, the Level 2 autonomy segment led the market with 50.7% share in 2025, reflecting widespread adoption of advanced driver assistance systems (ADAS).

Regional Insights

The Europe autonomous vehicles market is witnessing strong growth across key automotive hubs.

- Germany led the market in 2025 with 25.6% share, driven by its strong automotive industry and technological innovation.

- The United Kingdom followed with 18.4% share in 2025, supported by active pilot programs and regulatory support.

- France holds a notable position due to government initiatives and a strong domestic automotive sector.

Competitive Landscape

The Europe autonomous vehicles market is highly competitive, with a mix of established automakers and emerging technology companies. Market players are focusing on innovation in autonomous driving systems, partnerships, and large-scale testing to gain a competitive advantage. Strategic collaborations between automotive and technology firms are shaping the market landscape.

Prominent companies operating in the Europe autonomous vehicles market include AUDI AG, BMW Group, Ford Motor Company, Mercedes-Benz Group, Nuro, Inc., Pony.ai, Tesla, Toyota Kirloskar Motor, Volkswagen Group, Waymo LLC, and Zoox, Inc.

Europe Autonomous Vehicles Market Size

The Europe autonomous vehicles market was valued at USD 17.59 billion in 2025, is estimated to reach USD 20.88 billion in 2026, and is projected to reach USD 82.16 billion by 2034, growing at a CAGR of 18.68% from 2026 to 2034.

Autonomous vehicles (AVs), also known as self-driving or driverless cars, are vehicles capable of sensing their environment and operating without human involvement. This market includes various levels of automation ranging from driver assistance systems to fully autonomous robotic taxis and freight solutions. The region is distinguished by its rigorous regulatory framework and strong emphasis on safety and data privacy which shapes the deployment strategies of original equipment manufacturers and technology providers. According to the European Commission the transport sector accounts for approximately 25 percent of the European Union greenhouse gas emissions driving the push for automated electric mobility as a key component of the Green Deal. Furthermore, European Commission data indicates that road traffic crashes resulted in approximately 20,400 deaths in the European Union in 2023, highlighting the potential of autonomous technologies to enhance road safety by addressing human error, which is estimated to play a role in 95 percent of accidents. The market is supported by substantial investments in smart infrastructure including 5G networks and vehicle to everything communication protocols. Nations such as Germany France and the United Kingdom are leading pilot programs for autonomous shuttles and logistics fleets. The presence of established automotive giants alongside innovative tech startups creates a dynamic ecosystem focused on developing robust software stacks and sensor fusion technologies. Current developments emphasize the transition from level 2 autonomy to level 4 capabilities in controlled environments such as highways and urban hubs. This evolution is critical for addressing congestion improving accessibility for elderly populations and optimizing supply chain efficiency across the continent.

MARKET DRIVERS

Stringent Road Safety Regulations and Government Initiatives Accelerate Adoption

The implementation of stringent road safety regulations and proactive government initiatives contributes to the growth of the Europe autonomous vehicles market. Official safety regulators recognize that the vast majority of traffic incidents are linked to human factors, creating a strong impetus for the development of automated systems designed to minimize these risks. Projections from the European Transport Safety Council suggest that the widespread implementation of advanced driver assistance technologies and autonomous features could significantly lower the total number of accidents caused by human oversight. Under the General Safety Regulation, the European Union has implemented a phased mandate requiring features like intelligent speed assistance and lane monitoring for all newly registered vehicles in the region. This legislative framework creates a foundational layer of automation that facilitates the transition to higher levels of autonomy. Additionally governments are funding large scale pilot projects to test autonomous public transport and logistics solutions. For instance the German Federal Ministry for Digital and Transport has allocated significant budgets for the development of automated driving test beds on public roads. These initiatives provide a controlled environment for validating technology and building public trust. The alignment of national policies with EU wide safety goals ensures a coordinated approach to deployment. By prioritizing the reduction of fatalities and injuries regulators are effectively creating a favorable environment for the integration of autonomous technologies. This regulatory push not only enhances safety but also stimulates innovation among manufacturers who must comply with evolving standards while seeking competitive advantages through superior automated capabilities.

Growing Demand for Efficient and Sustainable Urban Mobility Solutions

The increasing demand for efficient and sustainable urban mobility solutions is also boosting the expansion of the Europe autonomous vehicles market. Rapid urbanization has led to severe traffic congestion and pollution in major European cities prompting authorities and citizens to seek alternative transportation models. Demographic data from Eurostat emphasize that most of the European population is concentrated in urban centers, a trend that is expected to intensify and drive demand for autonomous mobility solutions. Autonomous shared mobility services such as robotaxis and shuttle buses offer a viable solution by optimizing route planning reducing the number of private vehicles on the road and lowering carbon emissions. These services can operate continuously and efficiently addressing the first and last mile connectivity challenges that plague traditional public transport systems. Cities like Paris and Helsinki are actively integrating autonomous shuttles into their public transit networks to improve accessibility and reduce operational costs. The integration of autonomous vehicles with electric powertrains further aligns with sustainability goals by minimizing the environmental footprint of urban transport. Moreover the convenience of on demand autonomous transport appeals to younger demographics who prioritize access over ownership. This shift in consumer behavior supports the business case for mobility as a service providers. By offering seamless and eco friendly transportation options autonomous vehicles address critical urban challenges. The synergy between automation electrification and shared mobility creates a powerful impetus for market expansion as cities strive to become smarter and more livable.

MARKET RESTRAINTS

Complex Regulatory Landscape and Liability Issues Hinder Commercial Deployment

The complex and fragmented regulatory landscape regarding liability and insurance is a major limiting factor to the Europe autonomous vehicles market. Unlike traditional vehicles where driver liability is clear autonomous systems introduce ambiguity regarding responsibility in the event of an accident. Determining whether the manufacturer software provider or vehicle owner is liable requires new legal frameworks that are still under development across different European jurisdictions. As per the European Insurance and Occupational Pensions Authority the lack of harmonized rules on liability for automated driving creates uncertainty for insurers and manufacturers alike. This uncertainty complicates the underwriting process and increases the cost of insurance premiums for autonomous fleets. Furthermore the approval process for level 4 and level 5 vehicles varies significantly between member states leading to delays in cross border operations. While the European Union is working towards unified guidelines the pace of legislative change often lags behind technological advancements. Manufacturers hesitate to deploy large scale commercial services due to the risk of costly litigation and regulatory penalties. The absence of a clear liability framework also affects consumer confidence as users may be reluctant to adopt technologies where legal protections are unclear. Until comprehensive and harmonized laws are established the market will face hurdles in scaling operations. This regulatory fragmentation increases compliance costs and slows down the realization of the full economic potential of autonomous vehicles in Europe.

High Development Costs and Infrastructure Investment Requirements Limit Scalability

The high costs associated with research and development and the need for extensive infrastructure upgrades are among the main obstacles to the growth of the Europe autonomous vehicles market. Developing reliable autonomous systems requires significant investment in sensors such as LiDAR radar and cameras as well as powerful computing units and sophisticated software algorithms. According to industry analysis from McKinsey and Company the development of a fully autonomous driving stack can cost billions of euros per manufacturer creating a high barrier to entry. Additionally the deployment of autonomous vehicles necessitates upgrades to existing road infrastructure including the installation of smart traffic lights high definition mapping and robust 5G connectivity. The European Court of Auditors has noted that many member states lag in digital infrastructure readiness which is critical for vehicle to everything communication. The financial burden of these upgrades falls on both public authorities and private entities straining budgets. Small and medium sized enterprises often lack the capital to compete with larger conglomerates limiting innovation diversity. Furthermore the maintenance and calibration of sensitive sensors add to operational expenses for fleet operators. These high initial and ongoing costs delay the return on investment making it challenging for companies to achieve profitability in the short term. Without substantial financial support or cost reductions in technology components the scalability of autonomous solutions remains constrained. This economic reality forces many players to limit their operations to specific high value niches rather than broad commercial deployment.

MARKET OPPORTUNITIES

Integration of Autonomous Logistics and Freight Transport Offers Significant Growth Potential

The integration of autonomous technologies in logistics and freight transport provides avenues for the Europe autonomous vehicles market. The e commerce boom has increased demand for efficient and reliable delivery services while the logistics sector faces chronic labor shortages. Autonomous freight vehicles can operate for longer hours without fatigue improving supply chain efficiency and reducing delivery times. Pilot projects such as those conducted by DHL and Volvo Trucks on European highways demonstrate the viability of platooning and autonomous long haul transport. These systems optimize fuel consumption and reduce operational costs by maintaining consistent speeds and distances. The standardization of routes in logistics allows for easier implementation of level 4 autonomy compared to complex urban environments. Furthermore the use of autonomous delivery robots for last mile logistics in cities offers a solution to congestion and parking issues. Companies like Starship Technologies have already deployed thousands of robots in European campuses and urban areas. The ability to streamline the entire supply chain from warehouse to doorstep creates significant value for retailers and consumers. The logistics sector is set to lead in adopting autonomous solutions as technology and regulations evolve. This transformation will drive major market growth and operational excellence.

Advancements in Vehicle to Everything Communication Enhance Safety and Efficiency

Advancements in vehicle-to-everything (V2X) communication technology are creating a promising opportunity for the European autonomous vehicles market. This technology enables seamless interaction between vehicles, infrastructure, and pedestrians. V2X technology allows autonomous vehicles to receive real time data about traffic conditions road hazards and signal timings enhancing situational awareness beyond the range of onboard sensors. As per sources, the deployment of 5G networks in Europe is accelerating providing the low latency and high bandwidth required for effective V2X communication. This connectivity enables cooperative adaptive cruise control and intersection collision avoidance systems which significantly improve traffic flow and safety. Smart cities initiatives in places like Amsterdam and Barcelona are integrating V2X infrastructure into urban planning creating an conducive environment for autonomous operations. The ability to communicate with traffic lights allows vehicles to optimize speed and reduce idling thereby lowering emissions. Furthermore V2X supports the coordination of mixed traffic flows including human driven and autonomous vehicles ensuring smoother transitions during the adoption phase. The European Union supports these developments through funding programs aimed at creating a connected and automated mobility framework. By leveraging V2X technology autonomous vehicles can achieve higher levels of efficiency and reliability. This technological synergy not only enhances the performance of individual vehicles but also contributes to the overall optimization of the transportation network offering a compelling value proposition for stakeholders.

MARKET CHALLENGES

Cybersecurity Threats and Data Privacy Concerns Pose Critical Risks

The increasing connectivity of autonomous vehicles introduces severe cybersecurity threats and data privacy concerns that challenge the Europe autonomous vehicles market. As vehicles become software defined they are vulnerable to hacking malware and unauthorized access which could compromise safety and user privacy. The General Data Protection Regulation imposes strict requirements on the collection and processing of personal data generated by autonomous systems including location history and biometric information. Compliance with these regulations requires robust encryption and secure data management practices which add complexity and cost to development. A single security breach can damage brand reputation and erode public trust hindering adoption. Manufacturers must implement over the air update mechanisms and intrusion detection systems to protect against evolving threats. However the rapid pace of technological change often outstrips security measures creating vulnerabilities. The lack of standardized cybersecurity protocols across the industry further complicates efforts to ensure uniform protection. Addressing these risks requires continuous investment in security research and collaboration with cybersecurity experts. Failure to adequately protect vehicles and data could lead to regulatory sanctions and liability claims. Thus cybersecurity remains a paramount challenge that must be addressed to ensure the safe and trusted deployment of autonomous vehicles.

Public Acceptance and Ethical Dilemmas Impede Widespread Adoption

Public acceptance and unresolved ethical dilemmas surrounding autonomous decision making inhibit the expansion of the Europe autonomous vehicles market. Many consumers remain skeptical about the safety and reliability of self driving cars particularly after high profile accidents involving autonomous vehicles globally. Ethical questions arise regarding how algorithms should prioritize safety in unavoidable accident scenarios such as choosing between protecting passengers or pedestrians. These moral dilemmas lack clear consensus and complicate the programming of autonomous systems. The opacity of artificial intelligence decision making processes also raises concerns about accountability and transparency. Building public trust requires extensive education and demonstrable safety records which take time to establish. Negative media coverage of incidents can disproportionately influence public perception slowing down adoption rates. Furthermore the potential displacement of jobs in the transportation sector raises social and political concerns that policymakers must address. Engaging with communities and involving them in pilot programs can help alleviate fears but resistance remains a hurdle. Until societal concerns are adequately addressed and ethical frameworks are established the widespread acceptance of autonomous vehicles will remain limited. This social challenge is as critical as technological and regulatory barriers in shaping the market trajectory.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Vehicle Type, Application, Level of Autonomy, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Audi AG, BMW Group, Ford Motor Company, Mercedes-Benz Group, Nuro, Inc., Pony.ai, Tesla, Toyota Kirloskar Motor, Volkswagen Group, Waymo LLC, Zoox, Inc., and Others. |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

In 2025, the passenger vehicles captured the prominent share of 60.8% of the Europe autonomous vehicles market. This supremacy of the segment is largely supported by the increasing consumer demand for advanced driver assistance systems that enhance safety and driving convenience. Modern car buyers prioritize features such as adaptive cruise control lane keeping assist and automatic emergency braking which are foundational steps toward full autonomy. The desire to reduce driver fatigue during long commutes and traffic congestion further fuels this demand. Manufacturers are responding by integrating level 2 and level 3 autonomy features into mid range and premium vehicles making them accessible to a broader audience. The psychological comfort provided by these systems appeals to urban dwellers who face stressful driving conditions daily. Furthermore the integration of smart connectivity allows passenger vehicles to communicate with infrastructure enhancing route efficiency and safety. The competitive landscape among automotive brands drives continuous innovation in user experience ensuring that autonomous features remain a key selling point. As technology matures and costs decrease the penetration of these systems in passenger cars will continue to expand solidifying their market dominance. The domination of the passenger vehicle segment is further supported by stringent regulatory mandates requiring the inclusion of advanced driver assistance systems in new vehicles. This legislative push ensures that every new passenger car contributes to the growth of the autonomous vehicles market by default. Automakers must comply with these standards to sell vehicles in the European market leading to uniform adoption across brands. The regulation covers technologies like intelligent speed assistance and drowsiness detection which rely on autonomous sensing and control algorithms. This regulatory framework creates a stable and predictable demand environment for suppliers of autonomous components. It also accelerates the development of higher levels of autonomy as manufacturers build upon these mandatory baseline features. The alignment of legal requirements with technological capabilities ensures that passenger vehicles remain at the forefront of autonomous vehicle deployment in Europe.

The commercial vehicles segment is likely to experience the fastest CAGR of 18.5% from 2026 to 2034 due to severe labor shortages in the logistics and transportation sector which threaten supply chain stability. Autonomous trucks and delivery vans offer a viable solution by operating continuously without the need for rest breaks thereby increasing productivity and reducing dependency on human labor. Companies are investing heavily in autonomous freight solutions to maintain service levels and meet growing e commerce demands. The ability to automate long haul routes allows human drivers to focus on complex last mile deliveries where their skills are most needed. This strategic shift improves overall operational efficiency and reduces costs associated with driver recruitment and retention. The economic imperative to address labor scarcity makes commercial autonomy a priority for logistics providers. As technology proves its reliability in controlled highway environments adoption rates are accelerating. This structural change in the workforce dynamics ensures that commercial vehicles will experience the highest growth rates in the autonomous market. The accelerated growth of this segment is also fueled by the potential for significant efficiency gains in supply chain operations and last mile delivery. Autonomous delivery robots and drones are being deployed in urban areas to streamline the final stage of logistics which is often the most costly and time consuming. These systems can operate around the clock navigating sidewalks and bike lanes to deliver packages directly to consumers. Major retailers and logistics companies in Europe are piloting these technologies to improve customer satisfaction and reduce carbon emissions. The precision of autonomous routing minimizes fuel consumption and traffic congestion contributing to sustainability goals. Furthermore autonomous trucks equipped with platooning technology can travel in close formation to reduce air resistance and save fuel. This optimization of resources aligns with corporate sustainability targets and regulatory pressures to lower emissions. The scalability of autonomous commercial fleets allows businesses to handle peak demand periods without proportional increases in labor costs. The commercial segment is set for rapid growth as technologies mature and regulatory frameworks adapt. Such expansion is fueled by the compelling operational and economic benefits provided.

By Application Insights

The transportation application segment was the largest segment in the Europe autonomous vehicles market and occupied a substantial share in 2025. This supremacy of the segment is supported by urgent urban mobility challenges including congestion pollution and the need for efficient public transport solutions. European cities are increasingly adopting smart city initiatives that integrate autonomous vehicles into their transportation networks to improve accessibility and reduce environmental impact. Autonomous shuttles and robotaxis offer flexible and on demand transport options that complement existing public transit systems. These services can operate in dedicated lanes or mixed traffic providing seamless connectivity for residents and tourists. Cities like Helsinki and Paris are leading the way with pilot programs that demonstrate the feasibility and benefits of autonomous public transport. The ability to reduce the number of private vehicles on the road through shared autonomous mobility helps alleviate congestion and free up urban space. Furthermore the integration of autonomous vehicles with electric powertrains supports sustainability goals by lowering emissions. The strong focus on improving quality of life in urban centers ensures that transportation remains the primary application for autonomous technologies. Government support and public private partnerships further accelerate the deployment of these solutions in major metropolitan areas. The leadership of the transportation segment is further supported by changing consumer preferences towards shared mobility services over private vehicle ownership. Younger demographics in Europe are increasingly favoring access to transportation rather than owning cars due to cost convenience and environmental concerns. The shift creates a robust market for autonomous ride hailing and car sharing services which rely on self driving technology to operate efficiently. Mobility as a Service platforms integrate various transport modes including autonomous shuttles into a single user friendly interface enhancing convenience. The reduction in operational costs for shared fleets due to the elimination of driver wages makes these services more affordable and attractive. Additionally, the ability to optimize fleet utilization through artificial intelligence ensures that vehicles are available when and where needed. This efficiency improves customer satisfaction and encourages wider adoption. The trend towards urbanization and digitalization reinforces the appeal of shared autonomous mobility. Trust in the technology is growing and services are becoming more widespread. Consequently, the transportation segment will continue to dominate the application landscape, driven by consumer behavior and economic viability.

The defense application segment is the fastest growing category in the Europe autonomous vehicles market with a projected CAGR of 15.2% during the forecast period owing to strategic investments in unmanned ground vehicles for surveillance reconnaissance and logistics support. European nations are increasing defense budgets to enhance national security and operational capabilities in response to geopolitical tensions. Unmanned ground vehicles can operate in hazardous environments reducing risk to personnel while providing real time intelligence. These systems are equipped with advanced sensors and artificial intelligence to navigate complex terrains and identify threats autonomously. The ability to conduct persistent surveillance without fatigue offers a tactical advantage in modern warfare. Military organizations are also exploring autonomous logistics vehicles to streamline supply chains in conflict zones. The integration of these technologies enhances situational awareness and decision making capabilities for commanders. The focus on force protection and operational efficiency drives the adoption of autonomous systems in defense applications. As technology matures and becomes more reliable the use of unmanned ground vehicles will expand further ensuring robust growth in this segment. The quick growth of the defense segment is also fueled by the development of autonomous combat and support systems that enhance military effectiveness. Nations are investing in next generation platforms that can perform complex tasks such as mine clearance explosive ordnance disposal and perimeter security without human intervention. These systems reduce the exposure of soldiers to dangerous situations improving survival rates and mission success. The modularity of autonomous platforms allows for rapid adaptation to different mission requirements enhancing versatility. Furthermore the integration of autonomous systems with manned units enables collaborative operations that leverage the strengths of both. This human machine teaming approach improves overall operational performance and flexibility. The emphasis on technological superiority in defense strategies drives continuous innovation in autonomous capabilities. Governments are collaborating with private sector partners to accelerate development and deployment. The strategic importance of maintaining a technological edge ensures sustained investment in autonomous defense technologies. These systems are becoming integral to modern military operations. Consequently, the defense segment will experience significant growth driven by security needs and technological advancements.

By Level of Autonomy Insights

The level 2 autonomy segment led the Europe autonomous vehicles market and captured a 50.7% share in 2025. This prominence of the segment is attributed to the widespread availability and affordability of level 2 systems in mass market vehicles. These systems provide simultaneous automated steering and acceleration/deceleration under specific conditions requiring the driver to remain engaged. The relatively low cost of implementation compared to higher levels of autonomy makes it accessible to a broad range of consumers. Automakers include these features as standard or optional extras to enhance vehicle appeal and competitiveness. The technology is mature and reliable offering tangible benefits in terms of safety and comfort without the complexity of full automation. Drivers appreciate the reduced fatigue during highway driving and traffic jams which are common in European urban areas. The regulatory framework supports the deployment of level 2 systems as they do not require significant changes to liability laws. This ease of integration and consumer acceptance ensures that level 2 remains the most prevalent form of autonomy. As production scales up costs continue to decrease further solidifying its market leadership. The leadership of the level 2 segment is further reinforced by its alignment with regulatory compliance and safety standards. The European Union General Safety Regulation mandates the inclusion of several features that constitute level 2 autonomy such as intelligent speed assistance and lane keeping systems. Level 2 systems allow manufacturers to comply with these regulations while providing added value to customers. The clear definition of driver responsibility in level 2 operations simplifies legal and insurance frameworks facilitating smoother market entry. Unlike higher levels of autonomy where liability issues are complex level 2 requires the driver to remain attentive reducing legal risks for manufacturers. This clarity encourages broader adoption among consumers who may be hesitant about fully autonomous systems. The incremental nature of level 2 technology allows users to build trust and familiarity with automated features. This gradual introduction prepares the market for future advancements in autonomy. The supportive regulatory environment and established safety protocols ensure that level 2 autonomy remains the dominant segment in the Europe autonomous vehicles market.

The level 4 and 5 autonomy segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 22.3% between 2026 and 2034. This rapid growth of the segment is mainly driven by technological breakthroughs in sensor fusion and artificial intelligence that enable vehicles to operate without human intervention in specific or all conditions. Advances in LiDAR radar and camera technologies provide high resolution data that allows vehicles to perceive their environment with greater accuracy. These technologies enable vehicles to handle complex urban scenarios including unpredictable pedestrian behavior and intricate traffic patterns. The ability to process vast amounts of data in real time ensures safe and efficient operation. Companies are investing heavily in developing robust software stacks that can manage edge cases and ensure reliability. The reduction in sensor costs due to mass production also makes level 4 and 5 systems more economically viable. As these technologies mature they unlock new applications such as robotaxis and autonomous freight. The promise of fully autonomous mobility drives significant interest and investment ensuring rapid growth in this segment. The swift expansion of the level 4 and 5 segment is also fueled by the establishment of pilot programs and regulatory sandboxes for testing autonomous vehicles. European countries are creating designated areas where fully autonomous vehicles can operate legally allowing companies to validate their technologies in real world conditions. These initiatives provide valuable data on performance and safety helping to refine systems and build public trust. Cities like Munich and London are hosting large scale trials of autonomous shuttles and taxis demonstrating the feasibility of these technologies. The insights gained from these pilots inform policy decisions and standard setting accelerating the path to commercialization. Public private partnerships play a crucial role in supporting these efforts by providing funding and infrastructure. The success of these programs encourages further investment and innovation in high level autonomy. As regulatory barriers are lowered and technical confidence grows the deployment of level 4 and 5 vehicles will expand rapidly. This supportive ecosystem ensures that the highest levels of autonomy experience the fastest growth in the market.

COUNTRY LEVEL ANALYSIS

Germany Autonomous Vehicles Market Analysis

Germany dominated the Europe autonomous vehicles market and accounted for a share of 25.6% in 2025. This dominance of the German market is driven by its strong automotive industry and advanced engineering capabilities. The country is home to leading original equipment manufacturers such as BMW Mercedes Benz and Volkswagen which are at the forefront of autonomous vehicle development. Germany has established several test beds including the A9 motorway which is equipped with sensors and communication infrastructure for autonomous vehicles. The presence of a robust supply chain and skilled workforce further strengthens the market. The country's focus on Industry 4.0 facilitates the integration of digital technologies in manufacturing enhancing production efficiency. Regulatory frameworks in Germany are progressive allowing for the testing of level 4 vehicles on public roads. This supportive environment encourages innovation and attracts international players. The strong domestic demand for premium vehicles with advanced features also drives market growth. Germany's leadership in automotive technology and policy ensures its dominant role in the regional autonomous vehicles market.

United Kingdom Autonomous Vehicles Market Analysis

The United Kingdom was the second largest player in the Europe autonomous vehicles market and occupied a 18.4% share in 2025 because of strong research institutions and innovative startups. Besides, the UK is a hub for artificial intelligence and software development which are critical for autonomous vehicle systems. Cities like London and Manchester are piloting autonomous shuttles and delivery robots to improve urban mobility. The UK's regulatory approach is flexible encouraging experimentation and rapid iteration. The presence of leading universities and tech companies fosters collaboration and innovation. The country also benefits from a strong financial sector that provides capital for autonomous vehicle ventures. The demand for efficient transport solutions in densely populated areas drives adoption. The UK's exit from the European Union has led to independent regulatory developments which may offer unique advantages. The combination of technological expertise and supportive policies maintains the UK's strong position in the market.

France Autonomous Vehicles Market Analysis

France holds a notable position in the Europe autonomous vehicles market owing to government initiatives and strong automotive presence. The country is home to major manufacturers like Renault and Peugeot which are actively developing autonomous technologies. France has established several test sites including the Saclay plateau near Paris where autonomous vehicles are tested in real world conditions. The country focuses on sustainable mobility integrating autonomous vehicles with public transport systems. Paris is implementing smart city projects that include autonomous shuttles to reduce congestion and emissions. The regulatory framework in France is evolving to accommodate higher levels of autonomy. The strong emphasis on innovation and sustainability drives market growth. France's strategic location and industrial base ensure its continued relevance in the European autonomous vehicles landscape.

Sweden Autonomous Vehicles Market Analysis

Sweden maintains a noteworthy share in the Europe autonomous vehicles market. It is known for its focus on safety and sustainability. The country is home to Volvo Cars and Scania which are pioneers in autonomous vehicle technology. The city of Gothenburg serves as a living lab for autonomous transport solutions including buses and trucks. Sweden's commitment to zero vision which aims to eliminate traffic fatalities aligns with the safety benefits of autonomous vehicles. The country invests heavily in research and development collaborating with universities and tech firms. The cold climate conditions provide a unique testing environment for validating vehicle performance in adverse weather. Sweden's strong infrastructure and digital connectivity support the deployment of autonomous systems. The focus on ethical and safe automation enhances public trust. Sweden's innovative approach and industrial strength secure its significant role in the market.

Netherlands Autonomous Vehicles Market Analysis

The Netherlands is expected to showcase a promising CAGR in the Europe autonomous vehicles market over the forecast period due to driven by its advanced infrastructure and logistics sector. The country is a key hub for international trade and logistics making it an ideal test bed for autonomous freight solutions. The Port of Rotterdam is implementing autonomous trucks and ships to improve efficiency and sustainability. The Netherlands has a dense network of smart roads equipped with sensors and communication devices. Cities like Amsterdam are experimenting with autonomous shuttles and delivery robots. The country's flat terrain and well maintained infrastructure facilitate easy deployment of autonomous systems. The Dutch approach emphasizes collaboration between public and private sectors. The focus on innovation and efficiency ensures that the Netherlands remains a key player in the European autonomous vehicles market contributing to regional growth and development.

COMPETITIVE LANDSCAPE

The competition in the Europe autonomous vehicles market is characterized by intense rivalry among established automotive giants agile technology startups and emerging mobility service providers. Traditional manufacturers leverage their engineering expertise and production scales while tech companies bring superior software and artificial intelligence capabilities. The market sees frequent collaborations and joint ventures as no single entity possesses all necessary competencies for full autonomy. Competition is driven by the race to achieve higher levels of automation particularly level 4 and level 5 which promise transformative mobility solutions. Regulatory compliance acts as a significant differentiator with companies striving to meet stringent European safety and data privacy standards. Intellectual property rights regarding algorithms and sensor technologies are fiercely contested. The entry of new players specializing in specific niches such as last mile delivery or highway trucking adds complexity to the competitive landscape. Brand reputation and consumer trust are critical assets as safety concerns remain paramount. Companies must balance innovation with reliability to gain market acceptance. The dynamic nature of this sector ensures continuous evolution with technological breakthroughs and policy changes reshaping competitive positions regularly.

KEY MARKET PLAYERS

The leading companies operating in the Europe autonomous vehicles market include:

- AUDI AG.

- BMW Group

- Ford Motor Company

- Mercedes-Benz Group

- Nuro, Inc.

- ai

- Tesla

- Toyota Kirloskar Motor

- Volkswagen Group

- Waymo LLC

- Zoox, Inc.

TOP PLAYERS IN THE MARKET

- Volkswagen Group is a pivotal entity in the Europe autonomous vehicles market leveraging its massive scale and diverse brand portfolio to accelerate self driving technology development. The company contributes globally by investing billions in software subsidiaries such as Cariad which focuses on creating unified operating systems for automated driving. Recent actions include strategic partnerships with mobileye and horizon robotics to enhance sensor fusion capabilities and accelerate level 4 autonomy deployment. Volkswagen is also testing autonomous shuttle services in major European cities to validate real world performance. These initiatives strengthen its market position by ensuring technological sovereignty and reducing reliance on external suppliers. The group aims to launch fully autonomous electric vehicles integrating advanced driver assistance systems across all brands. This comprehensive approach ensures Volkswagen remains a leader in both hardware manufacturing and software innovation within the rapidly evolving autonomous mobility landscape.

- BMW Group stands as a leading innovator in the Europe autonomous vehicles market with a strong focus on premium automated driving experiences. The company contributes to the global market by developing proprietary level 3 autonomous driving systems that are already approved for use on German highways. Recent actions include expanding its collaboration with Qualcomm and Arriver to create next generation software defined vehicle architectures. BMW is actively testing level 4 autonomous taxis in Munich demonstrating its commitment to commercial mobility solutions. The company also invests heavily in artificial intelligence and data analytics to improve decision making algorithms. These efforts strengthen its market position by offering customers cutting edge safety and convenience features. BMW’s strategy emphasizes gradual automation progression ensuring regulatory compliance and user trust. BMW is integrating autonomous capabilities into its luxury vehicle lineup. In doing so, the company maintains its competitive edge and influences global standards for high-end automated driving.

- Mercedes Benz Group AG is a frontrunner in the Europe autonomous vehicles market renowned for being the first manufacturer to receive international approval for level 3 conditional automated driving. The company contributes globally by setting new benchmarks for safety and liability in autonomous operations. Recent actions include launching the Drive Pilot system in Germany and expanding its availability to other European markets. Mercedes Benz collaborates with NVIDIA to develop high performance computing platforms for future autonomous fleets. The company is also piloting autonomous trucking solutions to enhance logistics efficiency. These initiatives strengthen its market position by establishing brand leadership in certified automated driving. Mercedes Benz focuses on integrating seamless user experiences with robust safety protocols. Its proactive approach to regulatory engagement and technological innovation ensures it remains at the forefront of the autonomous revolution shaping the future of premium mobility in Europe and beyond.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe autonomous vehicles market primarily employ strategies focused on strategic partnerships and vertical integration to accelerate technology development. Companies collaborate with tech firms and semiconductor manufacturers to secure supply chains and enhance computational capabilities. Investment in proprietary software platforms is a common approach to differentiate products and control user experience. Manufacturers also engage in extensive real world testing through pilot programs in selected cities to validate safety and gather data. Regulatory engagement is crucial as firms work closely with governments to shape laws governing autonomous operations. Additionally companies pursue mergers and acquisitions to acquire specialized talent and intellectual property in artificial intelligence. Sustainability is integrated into strategies by combining autonomy with electrification. These approaches enable participants to mitigate risks reduce development time and establish competitive advantages in a complex and rapidly evolving technological landscape.

MARKET SEGMENTATION

This research report on the Europe autonomous vehicles market has been segmented and sub-segmented into the following categories.

By Vehicle Type

- Passenger Vehicle

- Commercial Vehicle

By Application

- Transportation

- Defense

By Level of Autonomy

- Level 1

- Level 2

- Level 3

- Level 4 & 5

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe autonomous vehicles market?

The Europe autonomous vehicles market includes vehicles that use AI, sensors, and software to drive with reduced human input. It is expanding as Europe adopts safer and smarter mobility.

How does the Europe autonomous vehicles market function?

The Europe autonomous vehicles market functions through LiDAR, radar, cameras, AI, and connectivity systems that help vehicles sense surroundings, make decisions, and operate safely.

What drives growth in the Europe autonomous vehicles market?

The Europe autonomous vehicles market grows due to safety demand, smart mobility adoption, infrastructure investment, and supportive regulation for testing and deployment.

Which countries lead the Europe autonomous vehicles market?

The Europe autonomous vehicles market is led by Germany, followed by the UK and France, because of strong OEM presence, testing activity, and technology partnerships.

What vehicle types define the Europe autonomous vehicles market?

The Europe autonomous vehicles market includes passenger vehicles, commercial vehicles, robotaxis, and freight-focused autonomous platforms for mobility and logistics.

What technologies shape the Europe autonomous vehicles market?

The Europe autonomous vehicles market is shaped by LiDAR, radar, cameras, machine learning, sensor fusion, and V2X communication that improve perception and 7control.

How does regulation influence the Europe autonomous vehicles market?

The Europe autonomous vehicles market is shaped by safety rules, public-road testing approvals, and EU policy frameworks that support responsible deployment of autonomous systems.

What trends affect the Europe autonomous vehicles market?

The Europe autonomous vehicles market is influenced by electrification, V2X, robotaxis, fleet automation, and stronger collaborations between automakers and tech firms.

What challenges face the Europe autonomous vehicles market?

The Europe autonomous vehicles market faces public trust issues, infrastructure gaps, legal complexity, cybersecurity risks, and high technology development costs.

How do robotaxis impact the Europe autonomous vehicles market?

The Europe autonomous vehicles market benefits from robotaxis because shared autonomous mobility creates new demand for commercial fleets and urban transport services.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com