Europe Bulk Food Ingredients Market Segmented By Type (Primary Processed (Grains & Seeds, Herbs & Spices, Sugar, Salt, Oilseeds, Nuts And Others), Secondary Processed (Dry Fruits & Nuts, Grains & Seeds, Flour, Herbs & Spices, Sugar, Salt And Others), Application (Ready Meals, Bakery Products, Confectionery Products, Snacks & Spreads And Others), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) – Size, Share, Trends, Growth, Forecast (2026 to 2034)

Market Size, 2025

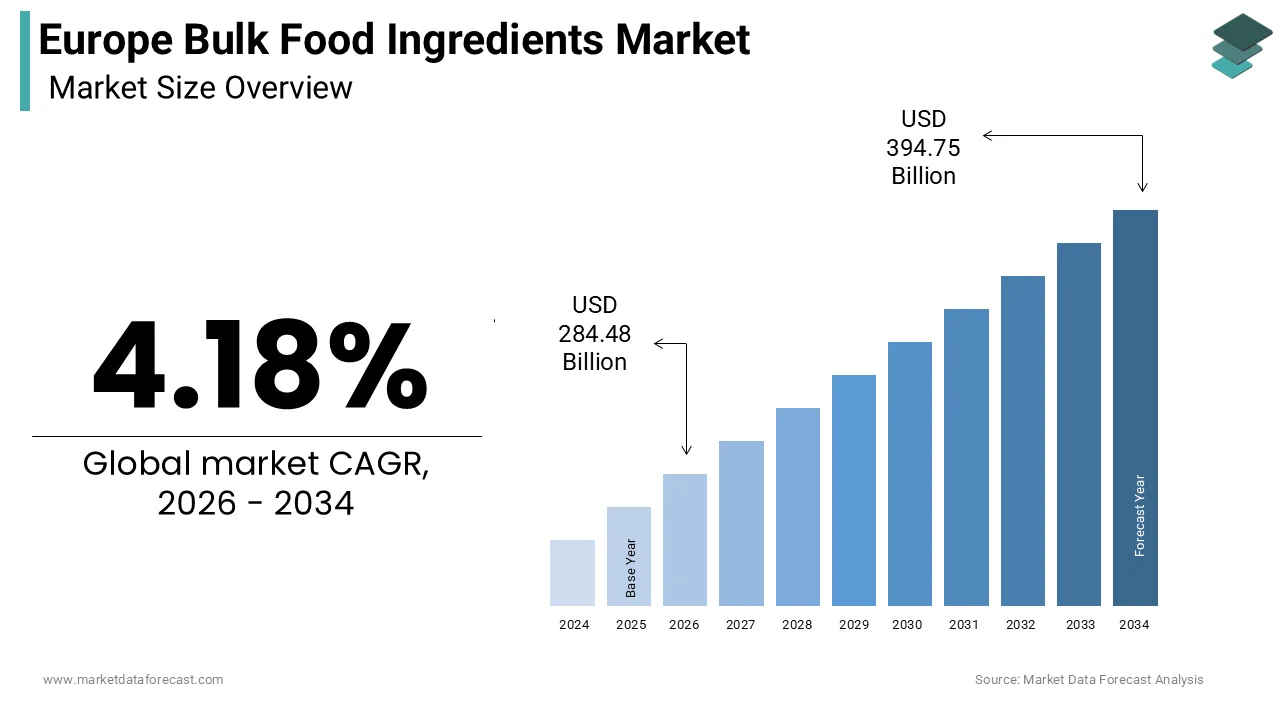

$273.07 BnMarket Estimate, 2026

$284.48 BnMarket Forecast, 2034

$394.75 BnCAGR, 2026–2034

4.18%Europe Bulk Food Ingredients Market Size

The Europe Bulk Food Ingredients Market size was calculated to be USD 273.07 billion in 2025 and is anticipated to be worth USD 394.75 billion by 2034, from USD 284.48 billion in 2026, growing at a CAGR of 4.18% during the forecast period.

Bulk food ingredients include large volume unpackaged or minimally packaged raw materials and functional components such as starches, proteins, sweeteners, emulsifiers, acids, and fibers supplied to food and beverage manufacturers for industrial-scale production. These ingredients serve as foundational elements in products ranging from baked goods and dairy alternatives to processed meats and ready meals. Unlike retail food items, bulk ingredients are traded based on technical specifications, purity, and functional performance rather than branding. The market operates within the European Union’s stringent food safety framework under Regulation (EC) No 178/2002 and the Food Information to Consumers Regulation, which mandate full traceability, allergen disclosure, and compositional standards. As per Eurostat, the EU food and beverage manufacturing sector processes vast volumes of raw agricultural materials annually, with bulk ingredients forming the critical intermediary layer between farm outputs and finished goods. Concurrently, the European Commission’s Farm to Fork Strategy targets a reduction in added sugars and salt by 2025, accelerating demand for functional alternatives like enzymatically modified starches and plant proteins. This regulatory and industrial context positions bulk food ingredients not as commodities but as engineered solutions enabling reformulation, sustainability, and compliance across Europe’s processed food ecosystem.

MARKET DRIVERS

EU Mandates for Sugar, Salt, and Fat Reduction Driving Reformulation Demand

The European Union’s binding nutritional targets under the Farm to Fork Strategy are a primary catalyst for bulk ingredient innovation, which is compelling food manufacturers to reformulate products using functional alternatives and propelling the expansion of the European bulk food ingredients market. As per the European Commission, member states must achieve a 10% reduction in added sugars and salt in processed foods by 2025, with parallel efforts to limit saturated fats. This policy shift has intensified demand for bulk ingredients such as inulin, polydextrose, and resistant starches as sugar replacers, and potassium chloride or yeast extracts as sodium substitutes. Reformulation trends in Western Europe show that many new breakfast cereals and dairy desserts incorporate bulk soluble fibers to offset sweetness loss. Similarly, bakery manufacturers in Germany have reported measurable reductions in salt use by applying enzymatically modified wheat proteins that enhance dough strength without sodium. National front-of-pack labeling systems like France’s Nutri-Score penalize high sugar and salt content, further incentivizing reformulation. This regulatory pressure transforms bulk ingredients from passive inputs into active tools for compliance to ensure consistent and growing demand across major processed food categories.

Expansion of Plant-Based and Alternative Protein Production Across Europe

Europe’s rapid shift toward plant-based diets has created substantial demand for bulk protein isolates, texturized vegetable proteins, and functional starches used in meat and dairy alternatives, which is further supporting the growth of the European bulk food ingredients market. As per the European Plant-Based Foods Association, retail sales of plant-based products reached 7.8 billion euros in 2024, with production scaling to meet institutional and food service demand. This growth requires industrial volumes of pea protein, soy concentrate, fava bean isolates, and methylcellulose, as these are the ingredients sourced in bulk for cost efficiency and process consistency. According to the European Alternative Proteins Partnership, more than 100 new plant-based production facilities opened in the EU between 2022 and 2024, primarily in Germany, France, and the Netherlands. Furthermore, the EU’s Protein Plan aims to reduce soy import dependency by promoting domestic legume cultivation, spurring investment in pea and fava bean processing infrastructure. Companies such as Roquette and Cosucra now supply bulk plant proteins under long-term contracts to major brands, including Oatly and Beyond Meat. This structural transformation of Europe’s protein supply chain ensures sustained demand for high-volume, functional bulk ingredients tailored to alternative food manufacturing.

MARKET RESTRAINTS

Stringent EU Regulations on Novel Food and Ingredient Authorization Delays

The European Union’s Novel Food Regulation (EU) 2015/2283 imposes lengthy and costly approval processes for new or modified bulk ingredients, which significantly delay market entry and innovation and restrain the regional market growth. As per the European Food Safety Authority, the average time to obtain Novel Food authorization exceeds 18 months, which requires extensive toxicological, compositional, and exposure data. In 2024, only a limited number of new ingredient applications were approved, while many were rejected or returned for additional data. This bottleneck particularly affects emerging ingredients such as precision-fermented proteins, algae-based emulsifiers, and enzymatically tailored fibers that lack historical consumption data. Companies must invest substantial sums per dossier, which is a barrier that deters small ingredient innovators and limits the diversity of available bulk solutions. Moreover, post-Brexit, the UK maintains a separate authorization process, fragmenting the European market. Consequently, food manufacturers often stick to a narrow set of approved ingredients such as wheat starch or soy lecithin, even when novel alternatives offer superior functionality, stifling reformulation progress and slowing the adoption of next-generation sustainable ingredients across the continent.

Price Volatility and Supply Chain Disruptions in Agricultural Raw Materials

The Europe bulk food ingredients market is highly susceptible to fluctuations in agricultural commodity prices and logistics disruptions, which directly impact input costs and formulation stability. As per the European Commission’s Agricultural Markets Task Force, wheat prices rose significantly in 2023 due to Black Sea export constraints and poor harvests in Eastern Europe. Similarly, sunflower oil prices surged following the Ukraine conflict, affecting emulsifiers and lipid systems derived from this crop. These volatilities cascade into bulk ingredient pricing, with the European Starch Association reporting that native and modified starch costs increased in 2024, squeezing margins for food manufacturers. Furthermore, extreme weather events such as droughts in Spain and Italy reduced pea and soy yields, tightening the supply of plant proteins. Without long-term supply contracts or vertical integration, many formulators face unpredictable costs and batch inconsistencies, leading to reformulation delays or product discontinuities. This external vulnerability undermines the reliability of bulk ingredient sourcing in an era of climate uncertainty and geopolitical instability.

MARKET OPPORTUNITIES

Integration of Upcycled and Circular Sourcing Models for Sustainable Ingredients

Europe’s Circular Economy Action Plan presents a significant opportunity for bulk food ingredients derived from food processing byproducts to align with both sustainability mandates and consumer demand for eco-conscious products. As per the European Commission, millions of tons of food waste are generated annually in the EU, much of which contains valuable fibers, proteins, and starches suitable for ingredient recovery. Companies are now commercializing bulk ingredients from previously discarded streams, including citrus fiber from juice pulp, potato protein from starch processing, and oat beta-glucan from milling residues. The EU’s Upcycled Food Certification pilot recognized these materials as eligible for sustainability labeling, enhancing brand value. Südzucker and Tereos are leading this shift, producing bulk dietary fibers from sugar beet pulp and wheat bran at scale. Furthermore, the Farm to Fork Strategy encourages valorization of side streams, with national grants in the Netherlands and Denmark supporting upcycling infrastructure. This circular model reduces raw material costs, lowers carbon footprints, and meets EU green public procurement criteria, positioning upcycled bulk ingredients as a high-growth, policy-aligned segment in Europe’s sustainable food transition.

Growth of Clean Label and Non-Synthetic Formulations in Processed Foods

The rising consumer preference for simple, recognizable ingredients is driving demand for bulk food components that replace artificial additives while maintaining functionality, which is another prominent opportunity in the European bulk food ingredients market. As per the European Food Information Council, a majority of European consumers actively avoid products with “chemical-sounding” ingredients, prompting manufacturers to reformulate using natural alternatives. This trend has accelerated the adoption of bulk ingredients such as native starches instead of chemically modified variants, fruit juice concentrates as colorants, and lecithin from sunflowers rather than synthetic emulsifiers. In Germany, many new processed food launches carry “free from” claims, primarily targeting artificial colors and preservatives. Furthermore, the EU’s positive list of approved food additives is shrinking, with substances like E171 (titanium dioxide) banned in 2022. Companies such as BENEO and Ingredion now supply bulk clean-label texturizers and stabilizers derived from chicory, tapioca, and peas. With national dietary guidelines and retailer policies rewarding clean label products, bulk natural ingredients are becoming essential for market access and consumer trust across Europe.

MARKET CHALLENGES

Fragmented National Standards and Lack of Harmonized Specifications

Despite EU-wide food safety regulations, the absence of harmonized technical specifications for bulk ingredients creates inconsistency in quality, labeling, and interchangeability across member states, which is challenging the growth of the European bulk food ingredients market. As per the European Federation of Food Ingredients, food manufacturers often receive the same ingredient, such as wheat gluten or soy lecithin, from different suppliers with varying particle size, moisture content, or protein purity, leading to production inconsistencies. For example, a bakery in Italy may require gluten with higher protein levels for pan bread, while a French manufacturer needs slightly different specifications for baguettes, yet both are supplied under the same generic EU food additive code. This lack of standardization forces manufacturers to revalidate formulations for each supplier, increasing R&D costs and time to market. Additionally, national allergen thresholds differ, with Germany mandating stricter gluten limits for “gluten-free” claims than Greece, which is complicating cross-border production. Without EU-level monographs for functional bulk ingredients, the market remains fragmented, increasing operational complexity and limiting scalability for both suppliers and food producers across the single market.

Logistical and Handling Constraints in Bulk Ingredient Distribution

The physical nature of bulk food ingredients poses significant logistical and hygiene challenges in storage, transport, and handling across Europe’s diverse manufacturing landscape. As documented by the European Hygienic Engineering and Design Group, cross-contamination risks are elevated in shared bulk transport systems, with residues from allergens such as soy or gluten persisting in tanker trucks and silos. Audits in 2024 found that a notable share of bulk ingredient deliveries to food processors showed trace allergen contamination due to inadequate cleaning protocols. Furthermore, hygroscopic ingredients such as maltodextrin and lactose absorb moisture during summer transport in Southern Europe, causing clumping and microbial growth that compromise functionality. Many small and medium-sized food manufacturers lack dedicated bulk handling infrastructure, relying on manual scooping that introduces variability and safety risks. The EU’s food hygiene regulations require documented cleaning and segregation procedures, but enforcement is inconsistent. Until standardized bulk logistics protocols and dedicated transport networks are established, the efficiency and safety of bulk ingredient use will remain compromised, hindering adoption in sensitive applications such as infant nutrition or allergen-free foods.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.18% |

| Segments Covered | By Type, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Tate & Lyle, Tate & Lyle PLC, Associated British Foods plc, Ingredion Incorporated, Cargill Incorporated, DMH Ingredients, Olam International, E.I. du Pont de Nemours and Company, Archer Daniels Midland Company, EHL Ingredients, and Community Foods Limited |

SEGMENTAL ANALYSIS

By Type Insights

The grains & seeds segment dominated the market by accounting for 33.6% of the regional market share in 2025. Grains and seeds serve as the cornerstone of Europe’s food manufacturing sector due to their irreplaceable function in bread, pasta, breakfast cereals, and animal feed. As per Eurostat, the European Union produced hundreds of millions of metric tons of cereals in 2024, with wheat accounting for a significant share, primarily sourced in bulk by millers and food processors. The German Federal Ministry of Food and Agriculture reported that most domestic wheat output is channeled into industrial flour production, which in turn supplies bulk starches, proteins, and fibers to downstream manufacturers. National dietary guidelines in France, Italy, and Spain promote whole grain consumption, driving demand for bulk whole wheat, rye, and oats in reformulated products. Furthermore, the EU Common Agricultural Policy provides direct support to cereal farmers, ensuring a stable supply and price moderation. This deep integration into Europe’s agricultural, industrial, and nutritional fabric ensures that grains and seeds remain the largest and most structurally embedded category in the primary processed bulk ingredients market.

The oilseeds segment is another major segment and is expected to be fastest growing segment in this regional market during the forecast, showcasing a CAGR of 8.08%. The growth of the oilseeds segment in this regional market is likely to be driven by the EU’s strategic push to reduce dependency on imported soy through the European Protein Plan that promotes domestic cultivation of rapeseed, sunflower, and fava beans. As per the European Commission, oilseed production in the EU increased in 2024, with rapeseed alone reaching millions of metric tons, which is primarily processed into bulk protein meals and oils for food and feed. Companies such as Avril and Tereos now supply bulk rapeseed protein isolates to plant-based meat manufacturers across France and Germany, replacing imported soy. The Netherlands hosts numerous alternative protein facilities that consume thousands of metric tons of oilseed protein annually. With the EU allocating significant funding through the Common Agricultural Policy to support oilseed processing infrastructure, this segment is transitioning from commodity crop to strategic food security asset, which is fuelling sustained growth in bulk ingredient demand.

The flour segment held a share of 35.9% of the regional market in 2025. Flour remains the dominant secondary processed bulk ingredient due to its non-substitutable role in Europe’s bread, bakery, and pasta traditions. As per the European Flour Millers Association, EU mills processed tens of millions of metric tons of wheat into flour in 2024, supplying industrial bakers, artisanal producers, and pasta makers across all 27 member states. Germany operates hundreds of industrial bakeries producing billions of loaves annually, all reliant on consistent bulk flour deliveries. National food cultures further entrench demand; Italy’s Protected Geographical Indication system recognizes hundreds of traditional pasta and bread varieties, each requiring specific flour types with defined protein and ash content. The French National Federation of Bakers and Pastry Chefs mandates the use of T65 or T80 flour for traditional baguettes, ensuring standardized bulk specifications. With most European households consuming bread daily, as documented by Eurostat, flour is not a discretionary ingredient but a daily necessity. This cultural and industrial indispensability ensures flour’s continued dominance in the secondary processed bulk ingredients landscape.

The dry fruits and nuts segment is estimated to record a CAGR of 10.4% over the forecast period, owing to their dual function as natural sweeteners and textural ingredients in reformulated snacks, bakery goods, and breakfast cereals. As per the European Food Information Council, many European consumers prefer products sweetened with fruit concentrates or dried fruit purees over refined sugar. Companies such as Kellogg’s and Nestlé now use date paste, raisin syrup, and apple fiber in bulk to replace sucrose in granola bars and cereals, reducing added sugar. As per the German Federal Centre for Nutrition, almond and hazelnut meals are increasingly used as clean-label fat replacers in low-calorie baked goods. Furthermore, the EU’s Nutri-Score system penalizes added sugars but rewards whole fruit and nut content, creating strong formulation incentives. With thousands of new “no added sugar” products launched in Europe in 2024, dry fruits and nuts are transitioning from premium inclusions to mainstream functional ingredients, which is accelerating bulk demand across multiple categories.

By Application Insights

The bakery products segment commanded the leading share of 33.3% of the regional market in 2025. Bakery products dominate bulk ingredient consumption due to the scale and cultural embeddedness of bread, rolls, pastries, and cakes in European diets. As per Eurostat, the average European consumes dozens of kilograms of bread annually, with Germany, France, and Italy leading per capita intake. According to the German Federal Statistical Office, billions of loaves were produced in 2024, requiring millions of metric tons of bulk flour, sugar, fats, and emulsifiers. Industrial bakeries operate continuously with automated mixing systems that rely on consistent bulk deliveries of ingredients such as wheat gluten, enzymes, and yeast. National regulations further standardize inputs; France’s bread decree mandates that traditional baguettes contain only flour, water, salt, and yeast—ensuring high volume demand for these core bulk items. With hundreds of thousands of bakeries across the EU, as documented by FoodDrinkEurope, the sector represents a stable, high-throughput channel for bulk food ingredients that is resilient to economic fluctuations due to the essential nature of staple baked goods.

The ready meals segment is another promising segment and is expected to exhibit a CAGR of 9.12% over the forecast period, owing to the demographic and lifestyle shifts, including rising urbanization, dual-income households, and aging populations seeking easy meal solutions. As per Eurostat, most of the EU population now lives in urban areas, with many adults reporting insufficient time for meal preparation. The UK’s Office for National Statistics documented a significant increase in ready meal sales in 2024, driven by premium lines featuring clean label ingredients and global cuisines. Manufacturers are responding with bulk-sourced vegetables, legumes, whole grains, and plant proteins to enhance nutritional profiles. For example, Nestlé’s Buitoni range in Italy now uses bulk lentil flour and pea protein to boost fiber and protein content. With national dietary guidelines in Sweden and the Netherlands promoting balanced convenience meals, ready meals are shedding their unhealthy image, which is creating robust demand for functional bulk ingredients that deliver taste, texture, and nutrition in a single-serve format.

REGIONAL ANALYSIS

Germany Bulk Food Ingredients Market Analysis

Germany accounted for the highest share of 25.6% of the regional market in 2025 owing to its massive food processing industry, strong agricultural base, and leadership in clean label reformulation. As per the German Federal Ministry of Food and Agriculture, the country operates thousands of food manufacturing facilities, including some of the world’s largest bakery and confectionery clusters. Germany processes millions of metric tons of wheat annually into flour, starch, and protein ingredients for domestic and export markets. The nation is also home to leading ingredient producers such as J Rettenmaier and Südzucker, which supply bulk fibers, sweeteners, and oilseed proteins across Europe. National policies such as the National Reduction and Innovation Strategy mandate salt and sugar reduction in processed foods, driving demand for functional bulk alternatives. With robust infrastructure, stringent quality standards, and high consumer demand for natural products, Germany remains the hub of Europe’s bulk food ingredients ecosystem in both volume and technological sophistication.

France Bulk Food Ingredients Market Analysis

France held the second biggest share of the European bulk food ingredients market in 2025. The growth of France in the European market is attributed to its diverse agricultural output, strong bakery tradition, and proactive nutritional policies. As per FranceAgriMer, the country is a leading producer of wheat, sugar beets, and sunflower seeds, providing a stable domestic supply of bulk grains, oils, and sweeteners. France’s artisanal and industrial bakeries consume millions of metric tons of flour annually, with strict adherence to traditional formulations under national decrees. The government’s Nutri-Score system and Eco-Regime payments incentivize reformulation with whole grains, fibers, and plant proteins, creating consistent demand for functional bulk ingredients. Companies such as Tereos and Roquette leverage domestic crops to produce bulk starches, inulin, and pea protein for global brands. With deep integration of agriculture, food manufacturing, and public health policy, France maintains a balanced and expanding market that blends heritage with innovation in bulk ingredient sourcing and application.

United Kingdom Bulk Food Ingredients Market Analysis

The United Kingdom had a prominent share of the European bulk food ingredients market in 2025. The growth of the UK in the European market can be credited to its large ready meal sector, strong snacking culture, and post-Brexit regulatory autonomy. As per the UK Department for Environment, Food and Rural Affairs, the country’s food manufacturing sector processes vast volumes of raw materials annually, with ready meals, snacks, and bakery products leading consumption. The UK’s Responsibility Deal with food businesses has driven widespread reformulation, reducing salt and sugar in key categories. The independent UK Novel Foods regime now offers faster approval for functional ingredients such as algal proteins and upcycled fibers, accelerating innovation. Major manufacturers such as Associated British Foods and Tate & Lyle source bulk ingredients globally, but increasingly from European suppliers to ensure supply chain resilience. Despite Brexit, the UK remains a high-value market due to its scale, consumer trends, and agile regulatory environment that supports rapid adoption of clean-label and plant-based bulk ingredients.

Italy Bulk Food Ingredients Market Analysis

Italy is anticipated to hold a notable share of the European bulk food ingredients market during the forecast period, owing to its pasta dominance, strong confectionery sector, and growing plant-based innovation. As per the Italian National Institute of Statistics, the country produces millions of metric tons of pasta annually, requiring large volumes of durum wheat semolina sourced in bulk from domestic and Mediterranean suppliers. Italy is also a major consumer of sugar, cocoa, and nuts for its world-renowned chocolate and confectionery industry, with Ferrero and Perugina driving bulk demand. The National Recovery and Resilience Plan allocated significant funding in 2024 to modernize food processing infrastructure with emphasis on clean label and circular economy practices. Southern regions are expanding legume and almond cultivation to supply bulk plant proteins and nut flours for export-oriented brands. With deep food heritage and increasing alignment with EU sustainability goals, Italy maintains a significant and evolving role in the European bulk ingredients landscape.

Netherlands Bulk Food Ingredients Market Analysis

The Netherlands is projected to showcase a healthy CAGR in the European bulk food ingredients market over the forecast period, owing to its role as Europe’s agri-food logistics hub and leader in plant-based and upcycled ingredient innovation. As per the Netherlands Enterprise Agency, the country exports tens of billions of euros worth of food annually, with bulk ingredients flowing through Rotterdam and Amsterdam ports to numerous countries. The Netherlands is home to major processors such as Cosucra and ADM, which convert domestic sugar beets, peas, and oilseeds into bulk fibers, proteins, and oils for global markets. The government’s “Protein Shift” and circular economy policies incentivize the upcycling of potato and citrus byproducts into functional bulk ingredients. Numerous plant-based production facilities have opened in recent years, consuming thousands of tons of bulk pea and fava protein. With world-class infrastructure, research institutions, and progressive policies, the Netherlands punches above its size as a strategic gateway and innovation center for bulk food ingredients in Europe.

COMPETITION OVERVIEW

Competition in the Europe Bulk Food Ingredients Market is characterized by a mix of large agro-industrial cooperatives and specialized ingredient innovators competing on scale, sustainability, and functional performance. The market is highly influenced by EU regulatory frameworks, including the Farm to Fork Strategy, Novel Food Regulation, and Circular Economy Action Plan, which shape ingredient innovation and sourcing. Differentiation arises through clean label credentials, plant-based positioning, upcycled content, and alignment with national nutritional policies such as France’s Nutri Score or the UK’s salt reduction targets. While commodity ingredients like wheat starch and sugar remain price sensitive, premium segments such as pea protein, beet fiber, and enzymatically modified starches command value-based pricing due to reformulation benefits. Competition is intensified by the need for consistent quality, allergen control, and bulk logistics capabilities across diverse manufacturing environments. Companies that combine agricultural integration, regulatory agility, and sustainability credentials gain preferential access to major food manufacturers and private label programs. The landscape rewards those who can translate agricultural raw materials into reliable, scalable, and policy-aligned functional solutions across Europe’s complex and dynamic food processing ecosystem.

KEY MARKET PLAYERS

A few major players of the Europe bulk food ingredients market include

- Tate & Lyle

- Tate & Lyle PLC

- Associated British Foods plc

- Ingredion Incorporated

- Cargill Incorporated

- DMH Ingredients

- Olam International

- E.I. du Pont de Nemours and Company

- Archer Daniels Midland Company

- EHL Ingredients

- Community Foods Limited

Top Strategies Used by the Key Market Participants

Key players in the Europe Bulk Food Ingredients Market focus on vertical integration by controlling agricultural sourcing, processing, and functional modification to ensure supply security and quality consistency. They invest in clean label and non-GMO certifications to meet consumer demand for transparent and natural ingredients. Companies align product portfolios with EU policy mandates, including sugar, salt, and fat reduction under the Farm to Fork Strategy and circular economy principles through upcycled ingredients. Strategic partnerships with food manufacturers enable co-development of reformulation solutions that meet Nutri Score and national front-of-pack labeling criteria. Expansion of production capacity for plant protein fibers and alternative sweeteners supports the growing plant-based and health-oriented food sectors. Sustainability is embedded through carbon-neutral production, renewable energy use, and waste valorisation, enhancing brand value and regulatory compliance across Europe’s evolving food landscape.

Leading Players in the Market

- Tereos Group is a leading European agro-industrial cooperative with significant operations in France, Germany, and Belgium, specializing in bulk food ingredients derived from cereals, sugar beets, and oilseeds. The company contributes to the global market by transforming agricultural raw materials into high-volume starches, fibers, sweeteners, and plant proteins used in bakery, confectionery, and plant-based food manufacturing. Tereos supplies both the food and feed sectors with non-GMO and organic certified ingredients that align with EU sustainability standards. Recently, the company strengthened its position by expanding its pea protein and wheat starch production capacity in Vic-sur-Aisne, France, to meet rising demand from plant-based meat manufacturers. It also launched a new range of upcycled fiber ingredients from sugar beet pulp under the EU Circular Economy Action Plan, enhancing its portfolio of clean-label functional bulk materials for European food processors.

- Südzucker AG is a Germany-based multinational and one of Europe’s largest producers of bulk food ingredients, including sugar, specialty carbohydrates, proteins, and dietary fibers sourced from sugar beets and cereals. The company contributes globally by offering functional solutions for sugar reduction, texture enhancement, and clean label formulation across bakery, dairy, and ready meal applications. Südzucker operates integrated biorefineries that valorize side streams into high value ingredients, supporting EU circular economy objectives. To reinforce its market presence, the company upgraded its fiber and protein extraction lines at its Ochsenfurt facility in 2024 to increase the output of beet fiber and wheat protein isolates. It also partnered with major food brands in the Netherlands and Sweden to co-develop bulk ingredient systems that meet Nutri Score and front-of-pack labeling requirements, ensuring alignment with evolving European nutritional policies.

- Roquette Frères is a French family-owned company and a global leader in plant-based ingredients, with a strong footprint in the Europe Bulk Food Ingredients Market through its portfolio of pea proteins, starches, polyols, and dietary fibers. The company contributes to the global food industry by enabling clean-label, plant-based, and sugar-reduced formulations using ingredients derived from peas, wheat, and corn. Roquette’s facilities in Lestrem and Lilla Edet supply bulk ingredients to food manufacturers across Europe’s bakery, confectionery, and alternative protein sectors. Recently, the company enhanced its position by inaugurating a new pea protein isolate production line in France with an annual capacity exceeding 25,000 metric tons. It also achieved carbon-neutral certification for its fiber production sites under the EU Green Deal, strengthening appeal among sustainability-focused brand owners and reinforcing its leadership in functional bulk ingredients for the European market.

MARKET SEGMENTATION

This research report on the Europe bulk food ingredients market has been segmented and sub-segmented based on type, application, and region.

By Type

- Primary Processed Food

- Grains & Seeds

- Others

- Nuts

- Oilseeds

- Salt

- Sugar

- Herbs & Spices

- Secondary Processed Food

- Dry Fruits & Nuts

- Grains & Seeds

- Flour

- Herbs & Spices

- Sugar

- Salt

- Others

By Application

- Ready Meals

- Bakery Products

- Confectionery Products

- Snacks & Spreads

- Others

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the market?

Growing processed food demand, expansion of the bakery and confectionery sectors, and increasing demand for convenience foods are major growth drivers.

2. What are the major types of bulk food ingredients?

The market includes grains, sweeteners, edible oils, spices, dairy ingredients, cocoa products, starches, and food additives.

3. Why are natural food ingredients gaining popularity in Europe?

Consumers are increasingly demanding clean-label, organic, and minimally processed food products with natural ingredients.

4. What role does sustainability play in the market?

Manufacturers are focusing on sustainable sourcing, eco-friendly packaging, and reducing food waste to meet environmental regulations and consumer expectations.

5. What challenges does the market face?

Raw material price fluctuations, supply chain disruptions, and strict food safety regulations are major challenges.

6. How is technology impacting the bulk food ingredients market?

Automation, advanced processing technologies, and digital supply chain management are improving efficiency and product quality.

7. Which distribution channels are important in the market?

Direct supply contracts, wholesalers, distributors, and online B2B platforms are major distribution channels.

8. What trends are shaping the Europe bulk food ingredients market?

Plant-based ingredients, functional food ingredients, clean-label products, and sustainable sourcing are key market trends.

9. How are changing consumer eating habits influencing the market?

Demand for healthier, protein-rich, and convenience food products is encouraging manufacturers to innovate ingredient offerings.

10. What is the future outlook for the Europe bulk food ingredients market?

The market is expected to grow steadily due to increasing processed food consumption, product innovation, and rising demand for natural and functional ingredients.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com