Europe Collaborative Robots Market Size, Share, Trends and Growth Forecasts Research Report, Segmented By Payload, Component, Application, End-User Industry, Programming Method and Country – Industry Analysis (2026 to 2034)

Europe Collaborative Robots Market Report Summary

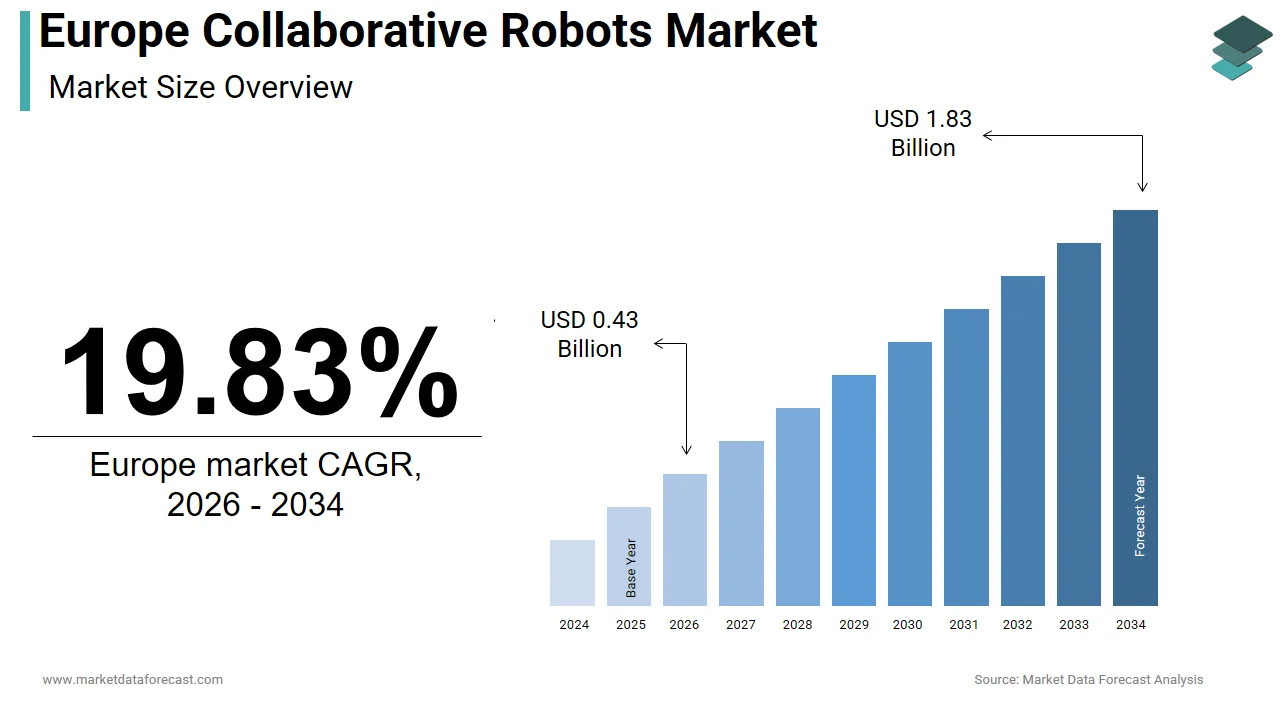

The Europe collaborative robots market was valued at USD 0.36 billion in 2025, is estimated to reach USD 0.43 billion in 2026, and is projected to reach USD 1.83 billion by 2034, growing at a strong CAGR of 19.83% from 2026 to 2034. Growth is driven by Europe’s labor shortages, the regulatory push for human-centric automation, and increasing adoption of flexible, safe robotic systems across manufacturing, healthcare, laboratories, and logistics. Updated EU Machinery Regulations and industrial digitization initiatives continue to accelerate the deployment of collaborative robots as safer, energy-efficient, and more adaptable alternatives to traditional automation.

Key Market Trends

- Rising demand for robots as a response to skilled labor shortages across manufacturing sectors.

- Strong regulatory tailwinds promoting human–robot collaboration through ISO/TS 15066-aligned safety pathways.

- Growing adoption of robots in non-traditional sectors, including healthcare, agriculture, and laboratories.

- Increasing importance of Green Deal–aligned automation, prioritizing energy efficiency and sustainable operations.

- Expansion of AI-enabled robot programming, path planning, and remote monitoring software.

Segmental Insights

- Based on payload, the less than 5 kg segment accounted for 48.2% of the market in 2024, driven by precision applications in electronics assembly, laboratory automation, and small-part handling, where lightweight robots align with ISO/TS 15066 safety requirements.

- Based on component, the hardware segment held the dominant share in 2024, reflecting the capital-intensive purchase of robotic arms, tooling, and sensors.

- Based on end-user industry, the automotive segment led the market with 32.2% share in 2024, supported by high automation needs and electrification-driven production changes.

Regional Insights

The Europe collaborative robots market is witnessing strong adoption across major economies, supported by industrial modernization efforts, workforce shortages, and regulatory incentives.

- Germany led the market with a 28.5% share in 2024, driven by strong SME adoption, Industry 4.0 funding programs, and local robot manufacturing expertise.

- Italy ranked second with a 12.3% share, supported by automation needs in machinery, food processing, and furniture manufacturing clusters.

- France showed strong growth due to national reindustrialization strategies and investments under “France 2030,” supporting deployment across aerospace and battery manufacturing.

- United Kingdom continues to expand collaborative robot adoption, particularly in life sciences, pharmaceuticals, and advanced engineering, supported by strong R&D ecosystems.

Competitive Landscape

The Europe collaborative robots market is highly competitive, shaped by established industrial automation leaders and agile innovators offering safe, flexible robotic systems. Companies focus on intuitive programming, compliant design, sector-specific solutions, and strong alignment with EU safety and cybersecurity regulations. Strategic priorities include workforce upskilling, training partnerships, simulation-based deployment tools, and development of modular ecosystems for faster integration across SMEs and high-tech industries. Prominent companies in the Europe collaborative robots market include: Universal Robots AS, Fanuc Corp., TechMan Robot Inc., AUBO Robotics USA, ABB Ltd., and KUKA AG.

Europe Collaborative Robots Market Size

The Europe collaborative robots market was valued at USD 0.36 billion in 2025, is estimated to reach USD 0.43 billion in 2026, and is projected to reach USD 1.83 billion by 2034, growing at a CAGR of 19.83% from 2026 to 2034.

Collaborative robots, or robots, in Europe represent a distinct class of industrial automation systems engineered to operate in direct physical proximity with human workers without the need for safety cages or physical barriers. As of 2025, the adoption of robots in Europe is increasingly shaped by labor market constraints, regulatory frameworks promoting human-centric automation, and cross-sectoral digitization mandates. According to some reports, the European Union faced a shortage of 2.1 million skilled manufacturing workers in 2024, with a structural gap that has accelerated interest in assistive robotic solutions. Furthermore, as per the European Commission’s updated Machinery Regulation, effective January 2024, new conformity assessment pathways were introduced specifically for human-robot collaboration, streamlining certification for ISO/TS 15066-compliant systems. These institutional and demographic dynamics position collaborative robotics not merely as a productivity tool but as a socio-technical response to Europe’s evolving labor ecosystem and industrial sustainability goals.

MARKET DRIVERS

Persistent Labor Shortages in Skilled Manufacturing Drive Robot Adoption

Europe’s manufacturing sector faces an acute and worsening shortage of skilled labor, creating urgent demand for collaborative robots as force multipliers in production environments. This factor is eventually to elevate the growth of the Europe collaborative robots market. This gap is exacerbated by demographic aging, where the European Commission projects that by 2030, nearly 30% of the EU’s current industrial workforce will reach retirement age. In response, small and medium enterprises, which constitute 99.8% of all EU businesses, are turning to robots due to their ease of deployment and low integration cost. The Italian National Institute for Industrial Technology confirmed in 2024 that 42% of surveyed SMEs in Lombardy and Emilia Romagna had piloted robots for machine tending and assembly tasks previously left unstaffed.

Stringent Workplace Safety Regulations Favor Human Centric Automation Solutions

Europe’s regulatory environment actively incentivizes collaborative robots through safety standards that prioritize human-machine coexistence over isolation. The stringent workplace safety regulations favor human-centric automation solutions is additionally propelling the growth of the Europe collaborative robots market. The European Union’s Machinery Regulation 2023/1230, which came into full effect in January 2024, establishes specific conformity pathways for collaborative systems that comply with ISO/TS 15066, the technical specification governing force and pressure limits in shared workspaces. According to the reports, traditional industrial robots were linked to 112 serious workplace incidents across the EU in 2023, which is prompting regulators to accelerate approvals for inherently safe alternatives. Robot designs by featuring torque sensors, soft exteriors, and emergency stop responsiveness that align with the EU’s “precautionary by design” safety philosophy. In France, the Labour Inspectorate mandated in 2024 that all new automation projects in facilities with fewer than 250 employees undergo a human-centric risk assessment, effectively favoring robots over caged robots. This regulatory tailwind, combined with proactive safety culture initiatives funded under the EU’s Horizon Europe program, creates a structural preference for collaborative robotics across member states, particularly in labor-intensive sectors such as food processing and precision assembly.

MARKET RESTRAINTS

High Initial Integration Costs Limit Accessibility for Small Enterprises

The hidden integration expenses that constrain adoption among Europe’s vast small and medium enterprise base are restraining the growth of Europe's collaborative robots market. While a basic robot arm may cost between 25000 and 50000 euros, the total cost of ownership frequently doubles when including end-of-arm tooling, safety validation, software licensing, and workforce training. According to a 2024 study by the German Federation of Industrial Research Associations, many surveyed SMEs cited unexpected integration costs as the primary reason for abandoning or delaying robot projects. Moreover, EU automation grants in 2024 specifically covered robot integration support, with most funding directed toward large-scale Industry 4.0 infrastructure. This financing gap disproportionately affects regions like Greece and Portugal, where access to specialized system integrators remains limited. The promise of plug-and-play automation remains unrealized for many, turning robots into aspirational rather than accessible tools for Europe’s entrepreneurial industrial backbone.

Lack of Standardized Interoperability Across Platforms Hinders Scalability

The fragmented software ecosystems and proprietary communication protocols that impede seamless integration across machines and enterprise systems are solely restraining the growth of the Europe collaborative robots market. Unlike traditional industrial robots that often adhere to established fieldbus standards, robots from different manufacturers rarely support plug-and-play interoperability, forcing users into vendor lock-in or costly middleware solutions. According to the European Robotics Forum, robot deployments in 2024 achieved full integration with existing manufacturing execution systems without custom API development. The lack of a unified programming language further exacerbates the issue, while ROS 2 is gaining traction in research, commercial robots still rely on brand-specific interfaces, such as URScript or KUKA Sunrise. The European Commission acknowledged this challenge in its 2024 Digital Europe Programme by allocating 45 million euros to develop an open architecture framework for collaborative robotics, but widespread adoption remains years away.

MARKET OPPORTUNITIES

Expansion into Non-Traditional Sectors Opens New Application Frontiers

The collaborative robots are rapidly transcending their manufacturing origins to penetrate sectors, such as healthcare, agriculture, and laboratory automation, which is creating new opportunities for the growth of the Europe collaborative robots market. In healthcare, robots are being deployed for repetitive yet precision-sensitive tasks like lab sample handling and pharmacy dispensing. According to the studies, over 120 hospitals in Germany, France, and the Netherlands integrated robots into clinical laboratories in 2024 to address chronic staffing shortages and reduce diagnostic errors. In agriculture, the European Union’s Common Agricultural Policy now includes subsidies for robotic assistance in labor-intensive activities 2, such as fruit harvesting and livestock monitoring. Similarly, in research, the Max Planck Society in Germany deployed 30 robots across its institutes for high-throughput experimentation in materials science. These cross-sectoral forays are enabled by modular grippers, vision AI, and ISO 13482-compliant safety certification for service environments.

EU Green Deal Alignment Creates Sustainability-Driven Demand

The European Union’s Green Deal and associated industrial decarbonization mandates are fostering demand for collaborative robots as enablers of energy-efficient and resource-optimized production, which is greatly influencing the growth of Europe's collaborative robots market. Robot deployments typically consume 80 to 90% less energy than traditional industrial robots due to their lighter mass, absence of high-torque motors, and on-demand operation. This efficiency aligns with the EU’s Energy Efficiency Directive, which requires member states to achieve annual energy savings of 1.9% in industry through 2030. In Sweden, the Environmental Protection Agency certified robot-assisted battery assembly lines at Northvolt’s Skellefteå plant as “low-impact automation,” qualifying them for carbon credit incentives. These policy linkages transform robots from mere productivity tools into instruments of regulatory compliance and environmental stewardship, embedding them within Europe’s broader industrial sustainability transformation.

MARKET CHALLENGES

Skill Gaps in Robotics Maintenance and Programming Impede Operational Continuity

The collaborative robots require a baseline of technical literacy that many European workforces lack, leading to underutilization and operational issues. This factor is one of the factors challenging the growth of the Europe collaborative robots market. According to the European Centre for the Development of Vocational Training, EU technical education programs included robot programming or troubleshooting modules as of 2024 by leaving a significant competency gap. In Eastern Europe, the problem is acute, where the robot installations in Moravian manufacturing clusters operated below utilization due to operator unfamiliarity with teach pendants and logic scripting. The shortage is compounded by the rapid evolution of robot software with new features, such as AI-based path planning requires continuous upskilling that many firms cannot support.

Cybersecurity Vulnerabilities in Connected Robot Systems Raise Operational Risks

They introduce new cybersecurity exposure points that challenge Europe’s industrial risk management frameworks as collaborative robots increasingly integrate with enterprise IT networks and cloud-based monitoring platforms. The cybersecurity vulnerabilities in connected robot systems raise operational risks is additionally degrade the growth of the Europe collaborative robots market. Unlike isolated legacy robots, modern robots often feature Wi Fi connectivity, remote software updates, and data logging capabilities by making them potential entry vectors for ransomware or data exfiltration attacks. The risk is heightened by inconsistent security standards, while the EU’s Cyber Resilience Act covers general machinery, it lacks specific protocols for real-time robotic control systems. A German automotive supplier experienced a production halt in early 2024 when malware infiltrated its network via an unpatched robot firmware update channel.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Payload, Component, Application, End-User Industry, Programming Method, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Universal Robots AS, Fanuc Corp., TechMan Robot Inc., AUBO Robotics USA, ABB Ltd., KUKA AG, and Others. |

SEGMENTAL ANALYSIS

By Payload Insights

The less than 5 kg payload segment accounted in holding 48.2% of the Europe collaborative robots market share in 2024, with its suitability for high precision, low force applications prevalent across electronics assembly, laboratory automation, and small parts handling. This payload class aligns with the ergonomic and safety requirements of human-robot collaboration, as defined under ISO/TS 15066, which limits permissible contact forces by making lighter robots inherently compliant. The robot deployments in European electronics manufacturing in 2024 involved sub-5 kg units for tasks, such as printed circuit board insertion and micro component placement. In the pharmaceutical sector, 92 hospitals and private laboratories in Germany, France, and the Netherlands adopted 3 to 4 kg robots for repetitive pipetting and vial labeling to reduce human error and contamination risk.

The 10–20 kg payload segment is projected to grow at a CAGR of 24.6% throughout the forecast period, with its expanding role in mid-weight industrial tasks that demand both human collaboration and material handling capacity. This range bridges the gap between lightweight precision robots and traditional industrial robots by enabling applications such as gearbox assembly, battery module handling, and machine tending for medium-sized CNC equipment. According to the research, automotive tier two suppliers increased their deployment of 15 kg robots by 41% in 2024 to automate transmission subassembly lines without full line retooling. In renewable energy manufacturing, the European Solar Manufacturing Council noted that 12-gigawatt-scale photovoltaic module plants in Spain and Poland integrated 12 to 18 kg robots for frame insertion and junction box mounting tasks requiring >10 kg payload but benefiting from human oversight for quality control. Furthermore, the European Commission’s updated Machinery Regulation now includes specific safety validation pathways for robots up to 20 Kg by reducing certification timelines by up to 30%, as per some sources. These technical, regulatory, and industrial shifts position the 10–20 kg segment as the dynamic growth engine for collaborative automation beyond micro assembly.

By Component Insights

The hardware segment was the largest by holding a dominant share of the Europe collaborative robots market in 2025, with the capital-intensive nature of initial robot deployment, where robotic arms, end-of-arm tooling, and safety sensors represent the primary investment. The hardware forms the physical core of every installation, with even the most basic deployment requiring a controller, joint modules, and mounting infrastructure. As per the study, the average hardware cost per robot system in 2024 was 38000 euros by accounting for nearly 70% of total project expenditure. The prevalence of standalone automation among small and medium enterprises often delays investment in advanced software layers. The French Ministry of Economy reported that robot buyers in the Auvergne-Rhône-Alpes region purchased only base hardware in their first acquisition. Additionally, national subsidy programs across Europe, including Germany’s “Digital Now” initiative, primarily reimburse hardware costs, skewing procurement behavior. The Czech Ministry of Industry confirmed that 94% of its 2024 robot grants were allocated to mechanical and electrical components rather than software licenses.

The software segment is deemed to register the fastest CAGR of 28.3% throughout the forecast period, from the rising demand for intelligent, adaptive, and remotely manageable robot systems that go beyond basic motion control. European manufacturers increasingly adopt simulation platforms, AI-based path planning, and cloud-based monitoring tools to maximize uptime and operational flexibility. According to the European Institute of Innovation and Technology, Horizon Europe funding was awarded in 2024 to projects developing cognitive robot software for dynamic human-robot teamwork. Companies like BMW Group now use digital twin software to validate robot workflows before physical deployment by reducing integration time by 35%, as stated by its Munich innovation unit. Similarly, robot users in food processing adopted vision-guided software in 2024 to handle variable product geometries. Moreover, the European Cyber Resilience Act mandates secure over-the-air update capabilities for all connected machinery from 2025 by forcing vendors to embed robust software architectures.

By End User Industry Insights

The automotive industry was the largest by occupying 32.2% of the Europe collaborative robots market share in 2024 by owing to its deep integration of automation, high labor cost pressures, and stringent quality requirements. European automakers and their supply chains use robots for tasks such as interior component installation, battery pack assembly, and quality inspection, where human dexterity combined with robotic repeatability enhances throughput without compromising safety. The shift toward electrification has intensified this trend, where battery module assembly requires precise torque control and contamination-free handling tasks, where 5 to 10-kg robots excel. Additionally, labor shortages in skilled mechanical trades have pushed tier one suppliers like Bosch and Valeo to automate final assembly stations using collaborative systems.

The electronics industry segment is expected to grow at the fastest CAGR of 26.8% throughout the forecast period, with the miniaturization of components, rising demand for consumer and industrial electronics, and the need for contamination-free, high-precision handling in cleanroom environments. The European electronics manufacturing output grew by 9.3% in 2024, with robots increasingly deployed for printed circuit board population, micro soldering, and camera module calibration. Similarly, in the Netherlands, ASML’s supplier ecosystem adopted sub-5 kg robots with electrostatic discharge safe grippers to handle sensitive photolithography subassemblies. The European Commission’s Chips Act further amplifies this trajectory, where its 2024 implementation guidelines explicitly encourage robot use in semiconductor packaging to reduce human-induced defects.

COUNTRY-LEVEL ANALYSIS

Germany Collaborative Robots Market Analysis

Germany was the top performer of the Europe collaborative robots market by holding 28.5% of the share in 2024 with its world-class manufacturing base, engineering expertise, and proactive industrial policy. The country’s Mittelstand comprises over 350000 small and medium enterprises that have embraced robots as a strategic response to chronic skilled labor shortages and rising wage pressures. The “Digital Now” funding program, which reimburses up to 50% of automation investments for SMEs, directly contributed to this adoption, with over 4300 approved robot projects in 2024 alone. Additionally, Germany hosts major robot manufacturers such as KUKA and Franka Emika, whose R&D centers in Augsburg and Munich continuously advance force sensing and human intent recognition. This ecosystem of policy support, industrial density, and technological leadership ensures Germany’s continued dominance in Europe’s collaborative robotics landscape.

Italy Collaborative Robots Market Analysis

Italy collaborative robots market was ranked second by holding 12.3% of share in 2024, with a dense network of specialized manufacturing clusters in machinery, furniture, and food processing. According to some studies, over 3800 robots were deployed in 2024, with 52% used in packaging, assembly, and surface finishing within the Emilia Romagna and Veneto regions. The furniture industry is increasingly employing 5 to 10 kg robots for sanding and varnish application tasks historically linked to high rates of respiratory illness. Moreover, Italian technical schools have integrated robot programming into vocational curricula, with over 120 institutes certified by ABB and Universal Robots.

France Collaborative Robots Market Analysis

France collaborative robots market growth is propelled by national strategies linking automation to reindustrialization and green manufacturing. The French government’s “France 2030” investment plan allocated 1.2 billion euros in 2024 specifically to support smart factory adoption, including robots in aerospace, pharmaceuticals, and battery production. As per the research, over 2800 robots were installed in 2024, with a 37% year-on-year increase in the New Aquitaine and Occitanie regions, hubs for renewable energy and medtech innovation. In aerospace, Safran and Thales use 10–20 kg robots for composite layup and turbine blade inspection by reducing cycle times by 22%, as confirmed by their Toulouse engineering teams. Additionally, France hosts the European Robotics Week secretariat, fostering cross-border knowledge exchange. This strategic alignment of industrial policy, high-value manufacturing, and workplace health ensures France’s sustained influence in shaping Europe’s collaborative automation agenda.

United Kingdom Collaborative Robots Market Analysis

The United Kingdom collaborative robots market growth is driven by the strong adoption in life sciences, automotive, and advanced engineering, despite its post-Brexit regulatory divergence. The UK’s concentration of global pharmaceutical and medical device companies has made it a leader in laboratory and cleanroom robot integration. According to the research, 1400 robots were deployed in 2024, with 45% in the life sciences sector in Cambridge, Oxford, and Scotland’s “Silicon Glen.” AstraZeneca’s Cambridge R&D center uses robots for high-throughput drug screening, handling over 50000 microplates monthly with 99.98% accuracy.

COMPETITIVE LANDSCAPE

The Europe collaborative robots market features a dynamic interplay between European engineering heritage and agile innovation, with competition defined less by price and more by integration ease, safety certification, and sector-specific adaptability. Established players like KUKA and ABB leverage their deep roots in industrial automation to offer robots that seamlessly interface with legacy systems, while pioneers like Universal Robots dominate the SME segment through simplicity and rapid deployment. The market is further enriched by specialized vendors focusing on healthcare, laboratory, and food-grade applications, creating a multi-tiered competitive landscape. National policies and EU funding schemes amplify local advantages, with companies aligning closely with regional industrial strategies such as Germany’s Industry 4.0 or France’s reindustrialization plans. Unlike commoditized markets, success here hinges on trust, compliance, workforce enablement, and the ability to deliver demonstrable return on investment within months. This environment fosters collaboration as much as competition, with vendors, integrators, and educators forming regional automation clusters that reinforce Europe’s leadership in human-centric robotics.

KEY MARKET PLAYERS

The leading companies operating in the Europe collaborative robots market include:

- Universal Robots AS

- Fanuc Corp.

- TechMan Robot Inc.

- AUBO Robotics USA

- ABB Ltd.

- KUKA AG

TOP PLAYERS IN THE MARKET

- Universal Robots is a Danish pioneer in collaborative robotics and a central force in shaping global robot standards. The company’s lightweight, user-programmable arms have become synonymous with accessible automation across European small and medium enterprises. It actively contributes to international safety frameworks, including ISO/TS 15066, and maintains a robust ecosystem of certified integrators and end-of-arm tooling partners. In 2024, Universal Robots launched its next-generation UR20e model with enhanced force sensing and AI-ready software architecture, enabling dynamic path adjustment in unstructured environments. The company also expanded its training academies in Germany, Italy, and Poland to address the European skills gap, certifying over 5000 technicians in robot programming during the year, thereby deepening its integration into the continent’s industrial fabric.

- ABB Robotics, headquartered in Sweden and operating globally, leverages its industrial automation heritage to deliver high-performance collaborative robots tailored for demanding European manufacturing sectors. Its YuMi and CRB series serve automotive, electronics, and pharmaceutical clients requiring precision, speed, and seamless integration with existing ABB control systems. In 2024, ABB introduced the CRB 1300 robot with a 20 kg payload and an IP67 rating, specifically designed for wet and dusty environments in food and battery production. The company also partnered with the European Institute of Innovation and Technology to develop robot applications for circular economy processes, including e-waste disassembly. These initiatives reinforce ABB’s strategy of combining industrial robustness with collaborative flexibility to meet Europe’s evolving sustainability and productivity demands.

- KUKA AG, a German engineering leader, plays a pivotal role in advancing collaborative robotics through its iiQKA ecosystem and LBR series of sensitive, torque-controlled arms. Deeply embedded in Europe’s automotive and machinery sectors, KUKA integrates robots with digital twin technology and cloud-based monitoring to enable predictive maintenance and remote operation. In 2024, KUKA unveiled the LBR Med robot certified for direct integration into medical devices, opening new avenues in clinical automation across EU hospitals. It also collaborated with the German Federal Ministry for Economic Affairs to launch a nationwide “Robot Readiness” program for SMEs, providing subsidized feasibility studies and integration support.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe collaborative robots market prioritize ecosystem development by certifying integrators and tooling partners to accelerate deployment. They invest heavily in intuitive software and simulation platforms to reduce programming barriers for non-technical users. Companies align product roadmaps with European regulatory standards such as the Machinery Regulation and Cyber Resilience Act to ensure compliance and trust. Strategic partnerships with vocational schools and government agencies address the skills gap through certified training programs. They also tailor robots for sector-specific needs, including cleanroom compatibility for electronics and washdown resistance for food processing. Additionally, firms emphasize sustainability by designing energy-efficient models and supporting circular economy applications such as remanufacturing and recycling. These multifaceted strategies enhance accessibility, safety, and long-term value across diverse European industrial contexts.

MARKET SEGMENTATION

This research report on the Europe collaborative robots market has been segmented and sub-segmented into the following categories.

By Payload

- Less than 5 kg

- 5–9 kg

- 10–20 kg

- More than 20 kg

By Component

- Hardware

- Software

- Services

- Consulting and Integration

- Maintenance and Training

By Application

- Material Handling

- Pick and Place

- Assembly

- Palletizing and De-palletizing

- Welding and Soldering

- Quality Testing and Inspection

- Packaging

- Other Applications

By End-User Industry

- Automotive

- Electronics and Semiconductors

- General Manufacturing

- Food and Beverage

- Chemicals and Pharmaceuticals

- Logistics and E-commerce

- Healthcare and Life Sciences

- Metals and Machining

- Other Industries

By Programming Method (Qualitative Only)

- Hand-Guiding / Direct Teaching

- Lead-through Teaching

- Offline Programming and Simulation

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What is the size of the Europe collaborative robots market?

The Europe collaborative robots market reached USD 0.43 billion in 2025 and is projected to reach USD 1.83 billion by 2034 amid automation surges.

2. What drives the Europe collaborative robots market?

Labor shortages, easy programming, and Industry 4.0 initiatives propel the Europe collaborative robots market in manufacturing.

3. What trends shape the Europe collaborative robots market?

AI, IoT integration, and SME adoption define trends in the Europe collaborative robots market for flexible operations

4. Which industries dominate the Europe collaborative robots market?

Automotive, electronics, and logistics lead the Europe collaborative robots market with precision task demands.

5. What payload rules the Europe collaborative robots market?

Up to 5kg payloads hold a major share in the Europe collaborative robots market for assembly and inspection.

6. How does hardware impact the Europe collaborative robots market?

Hardware like sensors and grippers takes 61.9% in the Europe collaborative robots market via safety enhancements.

7. Why is Germany key in the Europe collaborative robots market?

Germany's Industry 4.0 and automotive focus drive 43% of the Europe collaborative robots market revenue.

8. What challenges hinder the Europe collaborative robots market?

Integration costs and supply chains challenge the Europe collaborative robots market despite high adoption.

.

9. How do cobots aid SMEs in the Europe collaborative robots market?

Affordable, deployable cobots enhance SME productivity in the Europe collaborative robots market

10. What innovations drive the Europe collaborative robots market?

Digital twins, higher payloads, and AI advance the Europe collaborative robots market safety and versatility.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com