Europe Gaming Console Market Size, Share, Trends And Growth Forecasts Research Report, Segmented By Type, Interface, Application and Country – Industry Analysis (2026 to 2034)

Europe Gaming Console Market Report Summary

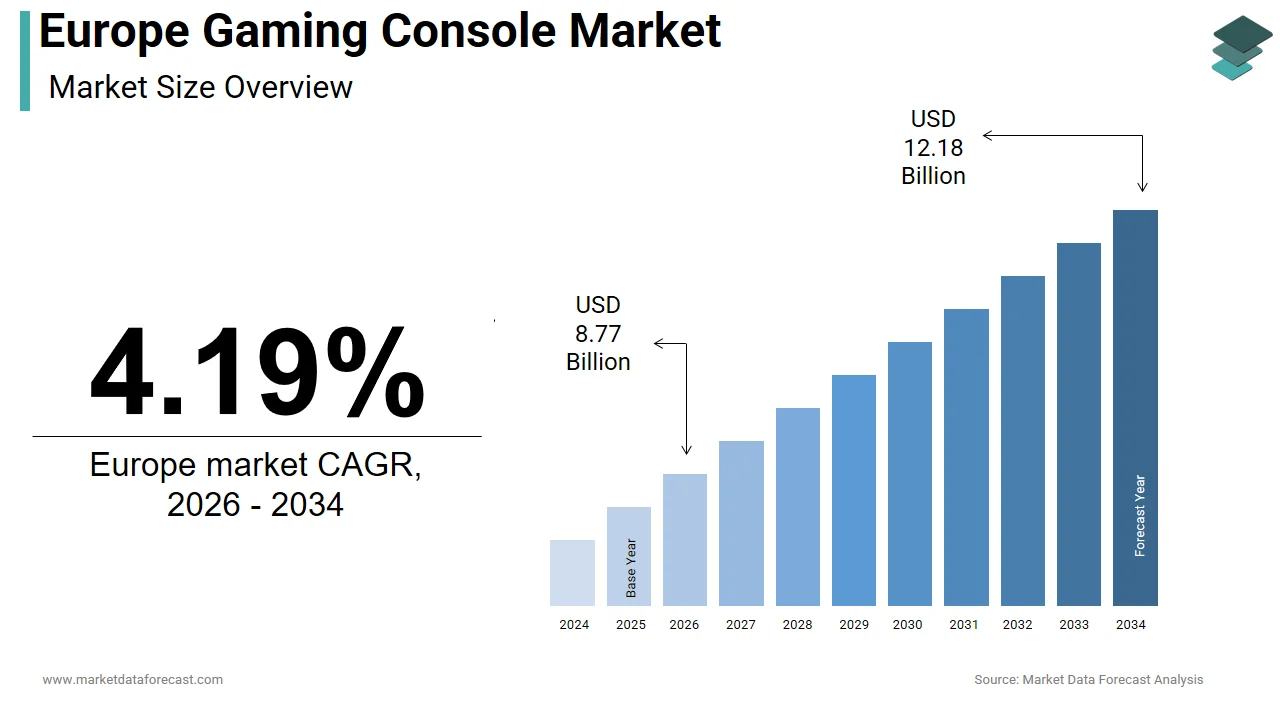

The Europe gaming console market was valued at USD 8.42 billion in 2025, is estimated to reach USD 8.77 billion in 2026, and is projected to reach USD 12.18 billion by 2034, growing at a steady CAGR of 4.19% from 2026 to 2034. The market growth is fueled by a rising gaming population, strong adoption of next-generation consoles, and increasing integration of immersive technologies such as 4K graphics, VR/AR compatibility, and cloud gaming. Additionally, the expansion of digital game libraries, subscription-based gaming services, and enhanced online multiplayer ecosystems continues to strengthen console demand across Europe.

Key Market Trends

- Growing adoption of next-generation consoles supporting high-performance graphics and advanced processing capabilities.

- Rise of cloud gaming and digital game subscriptions, boosting content accessibility and recurring revenue models.

- Increasing importance of online multiplayer and eSports ecosystems, driving demand for high-performance consoles.

- Continuous upgrades in gaming accessories, including controllers, VR headsets, and audio systems.

- Growing involvement of youth and young adults, supported by digital engagement, streaming culture, and social gaming.

Segmental Insights

- Based on type, the home consoles segment dominated the Europe gaming console market in 2024, capturing 58.3% share. This dominance is attributed to strong consumer preference for high-performance systems, advanced hardware capabilities, and access to exclusive game titles offered by leading console manufacturers.

- Based on application, the gaming segment remained the primary application in 2025, representing nearly 94% of total market activity. The segment’s overwhelming dominance is driven by Europe’s vibrant gaming culture, expanding digital game ecosystems, and increasing adoption of online and multiplayer gaming experiences.

- Based on interface, the residential interface segment held the dominant share of the Europe gaming console market in 2025. The segment’s leadership is supported by strong household adoption of gaming consoles, rising entertainment spending, and the growth of family-oriented gaming environments.

Regional Insights

The Europe gaming console market is experiencing robust growth across major economies, driven by strong consumer demand, rapid expansion of the digital entertainment sector, and rising investments in gaming infrastructure.

- The United Kingdom was the largest contributor, accounting for 19.8% of the Europe gaming console market share in 2024, supported by a mature gaming ecosystem, strong eSports presence, and high adoption of premium consoles.

- Germany followed with a 15.4% share in 2024, driven by its large gaming community, strong purchasing power, and increasing preference for high-end hardware.

- France is witnessing steady growth, fueled by a vibrant youth population, government-supported digital culture initiatives, and rising digital content consumption.

Competitive Landscape

The Europe gaming console market is dominated by globally recognized console manufacturers and technology companies with strong brand equity, extensive game libraries, and advanced hardware offerings. Companies are focusing on enhancing cloud gaming capabilities, expanding exclusive content portfolios, and integrating immersive technologies such as VR and haptic feedback. Strategic collaborations, digital service expansions, and competitive pricing strategies are further intensifying market competition across Europe.

Prominent companies in the Europe gaming console market include Sony Interactive Entertainment, Microsoft Corporation, Nintendo Co. Ltd., Valve, Sega, Atari, Razer, Corsair, and Logitech.

Europe Gaming Console Market Size

The Europe gaming console market was valued at USD 8.42 billion in 2025, is estimated to reach USD 8.77 billion in 2026, and is projected to reach USD 12.18 billion by 2034, growing at a CAGR of 4.19% from 2026 to 2034.

Gaming consoles are dedicated hardware platforms designed for interactive digital entertainment, primarily centered around video game play, multimedia streaming, and online social engagement. While consumer spending on hardware is influenced by macroeconomic conditions, the underlying engagement with console-based gaming remains resilient due to strong community dynamics and exclusive software titles. According to Eurostat, over 68% of households in the European Union with individuals aged 16 to 34 owned a dedicated gaming console in 2023, reflecting deep cultural integration beyond mere hardware ownership. This behavioral shift underscores consoles’ evolution from gaming devices to multimedia and social hubs.

MARKET DRIVERS

Rise of Exclusive First-Party Game Titles Drives Hardware Demand

The strategic release of high-quality exclusive titles by platform holders for console adoption is primarily driving the growth of the Europe gaming console market. Unlike multi-platform games, exclusives such as “The Legend of Zelda” on Nintendo or “God of War” on PlayStation offer unique experiences that cannot be replicated on competing systems, which is compelling consumers to purchase specific hardware. Sony’s “Spider-Man 2” sold more than 5 million physical and digital copies in Europe within its first six weeks of release in 2023, which directly correlates with a spike in PlayStation 5 sales across Germany, France, and the UK. Similarly, Microsoft’s acquisition of Activision Blizzard has heightened anticipation for future exclusives like “Call of Duty” iterations, which historically sell over 3 million units annually in Europe alone, as per data from the Entertainment Retailers Association. These titles not only drive initial hardware uptake but also sustain long-term engagement through downloadable content and seasonal updates, creating a self-reinforcing cycle of ecosystem loyalty.

Strong Cultural Integration of Console Gaming in Youth and Family Segments

Gaming consoles have become deeply embedded in the social and familial fabric of European households, particularly among younger demographics and multi-generational families. The strong cultural integration of console gaming in the youth and family segment is boosting the growth of the Europe gaming console market. Unlike PC or mobile gaming, consoles offer a shared, living room-centric experience that encourages co-play and spectator engagement. In countries like Sweden and the Netherlands, school holiday periods see a 35% average increase in console usage. Furthermore, local multiplayer games such as “Mario Kart” or “FIFA” are routinely used in social gatherings with consoles as tools for real-world interaction rather than solitary entertainment. This cultural normalization reduces purchase resistance and extends product lifecycles, as consoles transition from individual to household assets.

MARKET RESTRAINTS

Persistent Semiconductor Supply Constraints Limit Hardware Availability

The periodic shortages due to ongoing semiconductor allocation challenges are hindering the growth of the Europe gaming console market. Consoles rely on advanced system-on-chip designs that compete for foundry capacity with automotive and data center sectors. This imbalance caused extended lead times for PlayStation 5 and Xbox Series X units in several European markets during the first half of 2023, with retailers in Italy and Spain reporting stockouts lasting over eight weeks. Although production has stabilized, the concentration of chip manufacturing in Asia introduces vulnerability to geopolitical disruptions, as seen during the 2024 Taiwan Strait tensions, which temporarily delayed component shipments to European distribution hubs.

High Cost of Living and Consumer Spending Pressure Curtail Discretionary Purchases

Elevated inflation and rising household expenses have significantly dampened discretionary spending on premium entertainment hardware, which is also degrading the growth of the Europe gaming console market. The gaming consoles are priced between 300 and 600 euros which face scrutiny as non-essential purchases. This trend is particularly pronounced in Southern and Eastern Europe, where real wage growth has lagged behind inflation. While digital game sales remain resilient due to lower price points, the upfront hardware investment acts as a barrier to entry for new users and slows generational transitions.

MARKET OPPORTUNITIES

Expansion of Cloud-Enabled Hybrid Gaming Models Creates New Entry Points

The integration of cloud streaming with traditional console ecosystems is lowering the barrier to high fidelity gaming, which is prompting new opportunities for the growth of the Europe gaming console market. Services such as Xbox Cloud Gaming and PlayStation Plus Premium now allow users to stream AAA titles to smartphones, tablets, and low-end PCs without owning dedicated hardware. This infrastructure maturity enables hybrid adoption, where consumers initially engage via cloud before investing in physical consoles. Microsoft reported in early 2024 that many new Xbox Game Pass subscribers in France and the Netherlands began with cloud access and later purchased an Xbox Series S within six months. Similarly, Sony’s partnership with European telecom providers like Deutsche Telekom and Orange bundles console trials with broadband contracts, converting casual streamers into hardware owners. This funnel strategy expands the total addressable audience beyond traditional gamers to include mobile-centric and budget-constrained users, particularly in regions with high mobile penetration, such as Spain and Sweden.

Growing Emphasis on Accessibility and Inclusive Design Attracts Broader Demographics

The console manufacturers are increasingly embedding accessibility features into hardware and software to serve aging populations and users with disabilities, which is also expected to enhance the growth of the Europe gaming console market. Microsoft’s Xbox Adaptive Controller is now integrated into retail bundles across Europe, which supports over 40 external assistive devices and is certified under the EU Accessibility Act’s consumer electronics guidelines. As per a study, more than 87 million people in the EU live with some form of disability by representing a historically underserved segment. Nintendo’s “Switch Lite” and PlayStation’s customizable button mapping have further lowered physical and cognitive barriers to play. Game developers are also responding with Ubisoft’s “Assassin’s Creed Mirage,” which includes 30 accessibility options at launch, developed in consultation with European advocacy groups.

MARKET CHALLENGES

Intensifying Competition from Mobile and PC Gaming Fragmented Attention and Spending

The rapid advancement of mobile and PC gaming ecosystems that offer comparable experiences at lower or no upfront cost is solely hampering the growth of the Europe gaming console market. High-end smartphones now support console-quality graphics through cloud streaming and native Unreal Engine 5 titles, with over 78% of Europeans aged 18 to 34 owning a device capable of 60 frames per second gameplay as per the European Mobile Observatory 2024. Free-to-play mobile games such as “Genshin Impact” and “Honkai Star Rail” generate substantial engagement, with European players spending an average of 7.2 hours per week on mobile titles according to data from the Interactive Software Federation of Europe. PC gaming benefits from hardware flexibility and digital storefronts like Steam, which offer deep discounts and modding communities. In 2023, the average European gamer allocated only 38% of their total gaming budget to console hardware and software, down from 52% in 2019.

Regulatory Scrutiny on In-Game Purchases and Data Privacy Compliance

The European regulators are imposing increasingly stringent rules on digital transactions and user data handling within gaming ecosystems by creating operational and design challenges for console manufacturers. This regulatory scrutiny on gaming purchases will hamper the growth of the Europe gaming console market. The EU Digital Services Act mandates transparent disclosure of loot box odds and restricts targeted advertising to minors, provisions that directly impact monetization strategies for live service games. Additionally, the General Data Protection Regulation requires granular user consent for telemetry data collection, which consoles rely on for performance optimization and personalized content. These regulatory layers increase compliance costs and delay feature rollouts, as engineers must redesign store interfaces and data pipelines to meet country-specific interpretations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Interface, Application, Country. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Sony Interactive Entertainment, Microsoft Corporation, Nintendo Co., Ltd, Valve, Sega, Atari, Razer, Corsair, Logitech, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The home consoles segment was the largest by accounting for 58.3% of the Europe gaming console market share in 2024, like the PlayStation 5 and Xbox Series X. The cultural preference for premium, big screen gaming experiences in Western and Northern Europe is additionally fuelling the growth of the Europe gaming console market. As per the European Audiovisual Observatory, over 70% of European households own a television larger than 55 inches by creating an ideal environment for high-fidelity home console play. Exclusive AAA titles such as “Horizon Forbidden West” and “Forza Motorsport” are engineered to leverage this hardware advantage, which is driving repeat purchases and ecosystem loyalty. Consoles now function as entertainment hubs offering access to Netflix Disney+ Plus and YouTube.

The hybrid console segment is anticipated to register the fastest CAGR of 11.2% during the forecast period, owing to the shifting consumer preferences toward flexible, multi-context gaming. The rising demand for on-the-go entertainment among younger demographics and families is also driving up the growth of the segment. The Switch bridges this gap by delivering console-quality gameplay in a portable format. The device’s appeal to non-traditional gamers. In Sweden and the Netherlands, schools and senior centers have integrated Switch into social and cognitive therapy programs.

By Application Insights

The gaming segment held a prominent share of the Europe gaming console market remains the overwhelming primary application for consoles in Europe, representing roughly 94% of total market activity in 2024, as confirmed by the European Interactive Digital Entertainment Association. This near-total dominance reflects the foundational design purpose of consoles as dedicated platforms for interactive entertainment. The unmatched optimization between hardware and software in console ecosystems. Unlike PCs or mobile devices, consoles offer locked specifications that allow developers to extract maximum performance by enabling cinematic experiences with consistent frame rates and load times. The deep integration of online multiplayer and social features. Services like PlayStation Network and Xbox Live host over 65 million active European users who spend an average of 9.3 hours weekly in social gaming environments, as per the European Telecommunications Standards Institute.

The non-gaming application segment is expected to register the fastest CAGR of 13.8% from 2025 to 2033, owing to the strategic transformation of consoles into multifunctional digital entertainment and wellness platforms. The integration of fitness and health applications is also expected to fuel the growth of the segment. Titles like “Ring Fit Adventure” have turned consoles into home gym alternatives. Another driver is the adoption of consoles in educational and therapeutic contexts.

By Interface Insights

The residential interface segment was the largest by occupying a dominant share of the Europe gaming console market in 2024. The integration of consoles into home entertainment ecosystems is also fuelling the growth of the segment. In Germany and the UK, consoles rank as the second most used device for video streaming after smart TVs, with average weekly usage exceeding 6 hours per household. Games like “Mario Party” and “Just Dance” are routinely used during gatherings, turning consoles into social facilitators.

The commercial interface segment is projected to grow at a CAGR of 15.2% throughout the forecast period. The integration of consoles into hotel and resort amenities is also expected to fuel the growth of the segment. The use of consoles in educational and rehabilitation settings is additionally to enhance the growth of the segment. Similarly, universities in Sweden and Switzerland deploy consoles for simulation-based learning in engineering and psychology courses. These institutional applications, though currently niche, are scaling rapidly due to low hardware cost and high engagement, positioning commercial interfaces as a high-potential growth frontier.

COUNTRY LEVEL ANALYSIS

United Kingdom Gaming Console Market Analysis

The United Kingdom was the largest contributor to the Europe gaming console market by holding 19.8% of share in 2024, with its mature digital infrastructure and strong gaming culture. The country boasts one of the highest console penetration rates in Europe, with over 65% of households owning at least one device as per the UK’s Office for Communications. The Entertainment Retailers Association reported that UK consumers spent 2.1 billion pounds on console hardware in 2023, with the PlayStation 5 leading sales for the third consecutive year. Additionally, the UK’s robust broadband network, where 89% of households have access to full fiber that enables seamless online multiplayer and cloud integration. Government initiatives like the Cultural Development Fund have also supported esports tournaments and gaming festivals, further embedding consoles into mainstream entertainment.

Germany Gaming Console Market Analysis

Germany was positioned second in the European gaming console market by holding 15.4% of share in 2024, with its high purchasing power and technically discerning consumer base. According to the German Federal Statistical Office, over 58% of households with individuals under 35 own a dedicated gaming console, with a strong preference for high-performance home systems like the Xbox Series X. Germany’s strict data privacy laws have also shaped platform design, with Microsoft and Sony localizing cloud data storage within Frankfurt to comply with GDPR. Furthermore, the federal government’s Digital Culture Initiative funds public gaming labs in over 200 municipalities by promoting digital literacy through interactive media.

France Gaming Console Market Analysis

France gaming console market growth is fueled by its vibrant youth population and state-supported digital culture policies. The country is also home to major publishers like Ubisoft, whose locally developed franchises, such as “Assassin’s Creed,” drive hardware sales during launch windows. In 2023, the French Ministry of Culture allocated 45 million euros to the “Creative Gaming” program, which funds indie developers and public console installations in libraries and community centers. Paris, Lyon, and Marseille host annual gaming expos that attract over 200000 visitors, combined with consoles as cultural artifacts beyond mere technology.

Italy Gaming Console Market Analysis

Italy gaming console market growth is driven by the strong regional variation and rising digital adoption among younger demographics. This infrastructure upgrade enables online play and digital purchases, previously concentrated in the industrial north. Retailers like Unieuro report that Nintendo Switch dominates sales due to its suitability for multi-generational households, a cultural norm in Italy.

Spain Gaming Console Market Analysis

Spain gaming console market growth is likely to be driven by high youth engagement and tourism-linked commercial adoption. The country’s warm climate and social culture favor outdoor activities, yet consoles thrive as indoor entertainment during summer evenings and siesta hours. In 2023, Spain imported over 2.1 million units, with the PlayStation 5 leading due to its strong football game portfolio, including “FIFA” and “eFootball,” which align with national sports passion. Coastal resorts in the Costa del Sol and Balearic Islands increasingly offer consoles in vacation rentals and hotel suites to attract digital native tourists.

COMPETITIVE LANDSCAPE

Competition in the Europe gaming console market is dominated by three global players, like Sony, Microsoft, and Nintendo, each pursuing distinct yet overlapping strategies. Sony emphasizes cinematic exclusives and premium hardware performance, appealing to core gamers. Microsoft leverages its cloud and subscription ecosystem to offer flexibility and value through Game Pass while accelerating content acquisition. Nintendo differentiates through a hybrid design and family-friendly experiences that attract non-traditional audiences. The market features high brand loyalty due to ecosystem lock-in from digital libraries and multiplayer networks. Regulatory compliance, particularly around data privacy in game purchases and online safety, shapes product development and service delivery. While hardware margins are tight, the real competition centers on software engagement services and long-term user retention. New entrants face near insurmountable barriers due to scale content and infrastructure demands, making this a stable yet intensely innovative triopoly across European territories.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe gaming console market include

- Sony Interactive Entertainment

- Microsoft Corporation

- Nintendo Co Ltd

- Valve

- Sega

- Atari

- Razer

- Corsair

- Logitech

TOP PLAYERS IN THE MARKET

- Sony Interactive Entertainment is a global leader in the gaming console market with its PlayStation brand serving as a cornerstone of digital entertainment in Europe. The company’s PlayStation 5 has become a cultural phenomenon through exclusive titles like “Spider-Man” and “God of War” that drive hardware adoption and ecosystem loyalty. Sony actively tailors its content and services to European audiences with localized language support, regional pricing, and partnerships with European telecom providers for bundled internet and gaming subscriptions. In recent years, the company has expanded cloud streaming access across the EU and strengthened data compliance under GDPR by localizing server infrastructure in Germany and Ireland. These initiatives reinforce Sony’s commitment to both technological innovation and regulatory alignment in one of its most strategic global regions.

- Microsoft Corporation plays a pivotal role in the Europe gaming console market through its Xbox ecosystem, which integrates hardware, cloud services, and subscription offerings. The company has deepened its European footprint by expanding Xbox Game Pass availability and launching region-specific payment options to accommodate diverse consumer preferences. Microsoft’s acquisition of Activision Blizzard significantly bolsters its content pipeline with franchises like “Call of Duty” and “Diablo” that resonate strongly with European gamers.

- Nintendo Co Ltd maintains a distinctive position in the Europe gaming console market through its innovative hybrid console, the Nintendo Switch, which bridges home and portable gaming. The company’s family-oriented and universally accessible titles, such as “Animal Crossing” and “The Legend of Zelda,” have cultivated a broad user base spanning children, seniors, and casual players across the continent. Nintendo actively localizes its software with full audio and text support in major European languages and partners with retailers for seasonal promotions tied to local holidays. Recently, the company enhanced its online services for European users and introduced region-specific bundles featuring popular local franchises.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe gaming console market focus on strengthening exclusive content libraries to drive hardware loyalty and ecosystem retention. They invest in cloud infrastructure and streaming capabilities to expand access beyond traditional ownership models. Companies localize user interfaces, payment methods, and customer support to align with regional preferences and regulatory requirements. Strategic partnerships with telecom and retail partners enable bundled offerings and wider distribution. Additionally, they enhance accessibility features and comply with EU digital regulations such as the Digital Services Act and GDPR to build consumer trust and ensure long-term market sustainability.

MARKET SEGMENTATION

This research report on the Europe gaming console market has been segmented and sub-segmented into the following categories.

By Type

- Home Console

- Handheld Console

- Hybrid Console

By Interface

- Residential

- Commercial

By Application

- Gaming

- Non-Gaming

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What is the europe gaming console market?

The europe gaming console market involves the sales and usage of devices like PlayStation, Xbox, and Nintendo Switch within Europe, driven by gaming and entertainment trends.

2. Which consoles dominate the europe gaming console market?

PlayStation, Xbox, and Nintendo Switch are the main consoles in the europe gaming console market, with each offering unique game libraries and features supporting regional preferences

3. What are the latest trends in the europe gaming console market?

Trends include cloud gaming, VR integration, 3D technology, subscription services, and portable consoles, all transforming the europe gaming console market landscape

4. How is cloud gaming influencing the europe gaming console market?

Cloud gaming reduces hardware costs and enhances accessibility, boosting sales of cloud-optimized consoles like Xbox Series X/S and PlayStation 5 in the europe gaming console market

5. What role does esports play in the europe gaming console market?

Esports growth in Europe increases demand for gaming consoles with high-performance capabilities, fostering a competitive gaming ecosystem within the europe gaming console market

6. Which factors drive demand in the europe gaming console market?

Factors include rising disposable income, gaming culture, technological advancements, e-sports, popular franchises, and the availability of next-gen consoles in Europe

7. How are subscription platforms impacting the europe gaming console market?

Subscription platforms like Xbox Game Pass and PlayStation Now create steady revenue streams, encouraging gamers to stay engaged and expanding the europe gaming console market

8. What is the impact of VR on the europe gaming console market?

VR's rise enhances immersive gaming, with consoles increasingly integrating VR features, thus expanding the europe gaming console market’s offerings and consumer engagement

9. How does the europe gaming console market promote family and social gaming?

Consoles support multiplayer, online gaming, and social features, promoting family entertainment and social interaction in the europe gaming console market

10. What are the primary challenges in the europe gaming console market?

Challenges include high hardware costs, piracy concerns, rapid technological obsolescence, and regional regulatory differences affecting market growth

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com