Europe Geospatial Solutions Market Size, Share, Trends, and Growth Analysis Report, Segmented by Solution Type, Application, Technology, End User, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

$166.49 BnMarket Estimate, 2026

$190.98 BnMarket Forecast, 2034

$572.53 BnCAGR, 2026–2034

14.71%Europe Geospatial Solutions Market Report Summary

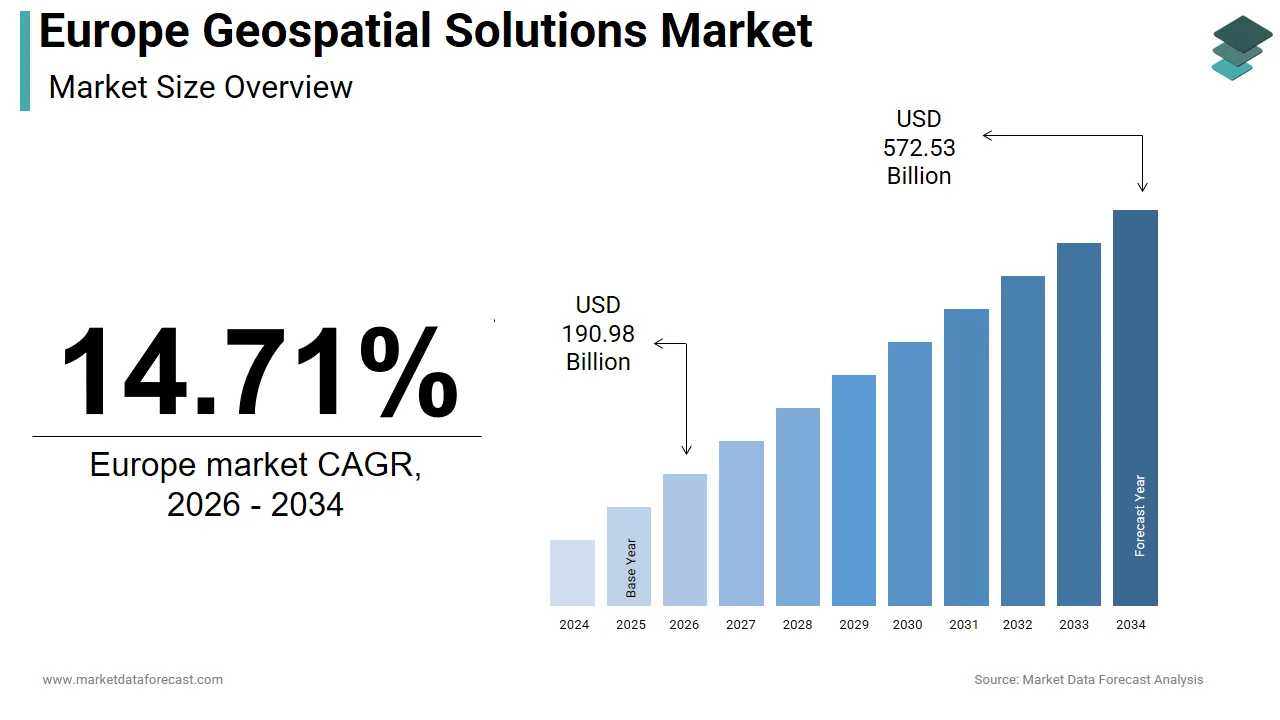

The Europe geospatial solutions market was valued at USD 166.49 billion in 2025, is anticipated to reach USD 190.98 billion in 2026, and is projected to reach USD 572.53 billion by 2034, registering a strong CAGR of 14.71% from 2026 to 2034. The market growth is driven by increasing adoption of location-based intelligence, rising investments in smart city infrastructure, and the integration of geospatial analytics into climate monitoring, transportation planning, and urban development initiatives. Governments and enterprises across Europe are leveraging geospatial technologies to improve decision-making, optimize resource utilization, and enhance infrastructure resilience. The growing use of satellite imagery, GIS platforms, AI-powered mapping tools, and cloud-based spatial analytics is further accelerating market expansion.

Key Market Trends

- Rising adoption of AI- and cloud-enabled geospatial platforms for real-time mapping, spatial modeling, and predictive analytics.

- Increasing integration of geospatial data into climate action plans, disaster management, and environmental monitoring systems.

- Strong growth in smart city and intelligent transportation projects, boosting demand for spatial data solutions.

- Expanding use of satellite imagery and remote sensing technologies for urban planning, agriculture, and defense applications.

- Growing emphasis on digital twins and 3D geospatial modeling to support infrastructure development and asset management.

Segmental Insights

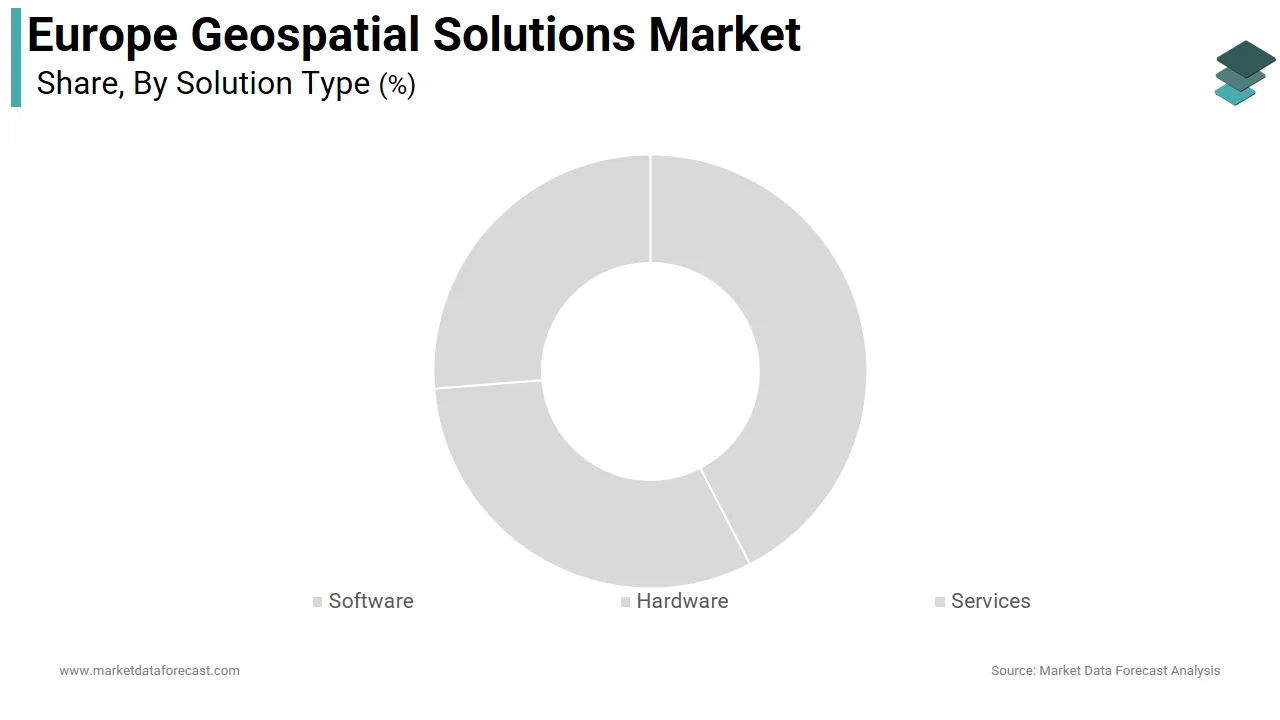

- Based on solution type, the software segment dominated the Europe geospatial solutions market in 2025, commanding 53.5% market share. This dominance is attributed to the widespread adoption of GIS software, cloud-based mapping platforms, and advanced spatial analytics tools across public and private sectors.

- Based on application, the planning and analysis segment led the market by accounting for 36.6% share in 2025, driven by the increasing integration of geospatial analytics into national climate strategies, urban development programs, and environmental risk assessment frameworks.

- Based on end user, the infrastructural development segment dominated the market by capturing 36.5% share in 2025. The segment’s strong position is supported by rising investments in transportation networks, utilities, smart cities, and large-scale construction projects requiring precise spatial intelligence.

Regional Insights

The Europe geospatial solutions market is witnessing robust growth across major economies, supported by rising government investments, expanding digital mapping initiatives, and increasing reliance on location intelligence for infrastructure and environmental planning.

- Germany held the leading position, accounting for 20.6% of the regional market share in 2025, driven by strong industrial digitization, smart manufacturing initiatives, and advanced spatial data infrastructure.

- France captured 16.3% of the European market share in 2025, supported by government-led urban planning projects and climate-focused geospatial applications.

- The United Kingdom is anticipated to register a promising CAGR during the forecast period, driven by its National Geospatial Framework, open data policies, and strong private-sector innovation ecosystem.

Competitive Landscape

The Europe geospatial solutions market is characterized by the presence of global technology leaders, specialized geospatial providers, and engineering service companies with strong capabilities in mapping, satellite imaging, and spatial analytics. Market players are focusing on AI-powered geospatial platforms, cloud-based GIS solutions, and integrated digital twin technologies to enhance service offerings. Strategic partnerships, acquisitions, and investments in satellite infrastructure and data platforms are strengthening competitive positioning across the region.

Prominent companies operating in the Europe geospatial solutions market include Apple, Inc., Hexagon AB, Oracle Corporation, Microsoft Corporation, Trimble Inc., Maxar Technologies, Inc. (DigitalGlobe, Inc.), Amazon.com, Inc., IBM Corporation, SNC-Lavalin Group, Inc. (Atkins PLC), Pitney Bowes, Inc., Esri, Inc., TomTom N.V., China Geo-Engineering Corporation (CGC), and L3Harris Technologies, Inc.

Europe Geospatial Solutions Market Size

The Europe geospatial solutions market size was USD 166.49 billion in 2025, is anticipated to be USD 190.98 billion in 2026, and is projected to reach USD 572.53 billion by 2034, registering a CAGR of 14.71% from 2026 to 2034.

The geospatial solutions market comprises technologies and services that collect, analyse, manage, and visualize spatial or geographic data through Geographic Information Systems (GIS), remote sensing, Global Navigation Satellite Systems (GNSS), and location-based platforms. These solutions underpin decision-making across public administration, urban development, agriculture, logistics, defense, and environmental monitoring. According to EuroGeographics, more than 90% of public sector data in Europe contains a spatial component, which indicates the centrality of geospatial intelligence in governance. According to the European Environment Agency, over 380 official spatial data infrastructures operate across European countries, reflecting deep institutional embedding. The EU’s INSPIRE Directive mandates cross‑border compatibility of geospatial datasets, while the Copernicus programme delivers more than 20 terabytes of Earth observation data daily, freely accessible and widely used for environmental monitoring and emergency management. Together, these policy and technological foundations position geospatial systems as critical infrastructure in Europe’s digital transformation.

MARKET DRIVERS

Expansion of Smart City Initiatives Drives Adoption of Geospatial Platforms

Urbanization has reached 78% across Europe according to Eurostat, which is compelling cities to adopt integrated digital management frameworks and propelling the growth of the European geospatial solutions market. As per the European Commission, over 300 cities participate in the Urban Agenda for the EU, committing to data-driven sustainability strategies. Geospatial platforms serve as the operational core of these smart city ecosystems, enabling real-time coordination of transport, utilities, and emergency services. For example, Vienna’s integrated GIS platform has reduced municipal response times according to the Vienna Smart City Agency. Barcelona employs a city-scale digital twin powered by high-resolution geospatial data, improving flood prediction accuracy according to its Urban Ecology Department. As per the European Commission, the Horizon Europe programme has allocated significant funding from 2021 to 2027 for digital urban infrastructure, much of it directed toward spatial data integration. As urban governance shifts toward predictive and participatory models, geospatial intelligence transitions from auxiliary tool to foundational layer.

Integration of Geospatial Data in Precision Agriculture Fuels Market Growth

Agriculture contributes 1.3% to the EU’s GDP according to the European Commission, and policy frameworks like the Common Agricultural Policy increasingly tie subsidies to sustainable practices enabled by geospatial analytics, which is another major factor fuelling the expansion of the European geospatial solutions market. As per the Joint Research Centre, millions of hectares of EU farmland are managed using satellite-guided machinery, allowing variable input application that reduces nitrogen runoff in countries such as Denmark and the Netherlands. According to the FranceAgriMer data, a significant share of large cereal farms in France use GIS-based decision support systems to achieve measurable yield gains. The European Space Agency’s Farm Sustainability Tool for Nutrients, powered by geospatial datasets, is utilized by thousands of farms to meet EU environmental compliance. With climate resilience and resource efficiency now central to EU agri policy, geospatial technologies are evolving into non-negotiable components of modern farm management across the continent.

MARKET RESTRAINTS

Stringent Data Privacy Regulations Impede Cross-Border Geospatial Data Flows

The General Data Protection Regulation imposes strict controls on the processing of location data that can identify individuals, even when anonymized, which is a significant restraint on the growth of the European geospatial solutions market. As per the European Data Protection Board, many geospatial analytics firms cite compliance complexity as a major operational constraint. As per a 2023 survey by the European GNSS Agency, a considerable share of transport and logistics operators scaled back geofencing initiatives due to legal uncertainty. The 2022 European Court of Justice ruling that invalidated certain international data transfer mechanisms further disrupted cloud-based geospatial services relying on non-EU data centers. National divergence exacerbates the issue; Germany’s Federal Data Protection Act enforces tighter geolocation rules than the EU baseline, which is creating a fragmented compliance landscape. These regulatory barriers not only raise costs but also deter innovation in real-time mobility analytics, limiting the scalability of consumer and enterprise location services.

Fragmented National Geospatial Infrastructures Limit System Interoperability

Despite the INSPIRE Directive’s harmonization goals, implementation remains uneven. This factor is also hindering the European geospatial solutions market growth. According to a 2023 European Environment Agency assessment, only a portion of EU countries fully comply with INSPIRE’s technical standards for spatial data exchange. This results in mismatches in coordinate systems, metadata schemas, and update cycles. For instance, the Netherlands refreshes its national topographic database frequently, whereas Bulgaria’s equivalent dataset is updated annually according to its respective mapping authorities. The European Commission’s Digital Compass initiative identifies this fragmentation as a key obstacle to the digital single market, noting that firms operating in multiple EU countries incur higher data harmonization costs. Such inconsistencies degrade analytical reliability in cross-border applications from disaster response to freight logistics and inflate integration expenses, slowing market maturation.

MARKET OPPORTUNITIES

Emergence of Digital Twins for National Infrastructure Unlocks New Geospatial Applications

European nations are investing in national digital twins that rely on high-fidelity geospatial data to replicate physical environments virtually, which is a promising opportunity in the European geospatial solutions market. As per Finland’s National Land Survey, 3D city models have been developed to cover most of its urban population, which is enabling energy and emissions simulations with high spatial accuracy. According to the European Investment Bank, billions of euros in public infrastructure funding from 2024 to 2027 will require digital twin readiness, directly stimulating demand for dynamic geospatial capture. In the Netherlands, the Digital Delta platform uses geospatial twins to manage its extensive dike network, reducing maintenance costs according to Rijkswaterstaat. As these systems evolve from static visualization to predictive simulation engines, they create sustained demand for continuously updated, high-resolution spatial data, repositioning geospatial providers as essential infrastructure enablers.

Growth in Defense and Border Security Applications Accelerates Geospatial Investment

Geopolitical instability and migration pressures have intensified reliance on geospatial intelligence for security, which is another major opportunity in the European geospatial solutions market. According to the European Defence Agency, a majority of EU member states now integrate commercial satellite imagery into defense planning. Frontex processes millions of location records monthly from drones and vessel tracking systems to monitor the EU external borders. As per the European External Action Service, geospatial monitoring has improved illegal crossing detection latency in the Eastern Mediterranean between 2022 and 2024. The European Commission’s Military Mobility Action Plan allocates hundreds of millions of euros for geospatial infrastructure to support rapid cross-border troop movement. France’s Military Programming Law dedicates significant funding to space-based ISR capabilities, including all-weather radar satellites. These defense and security imperatives are driving sustained procurement of advanced geospatial solutions and fostering public-private innovation partnerships.

MARKET CHALLENGES

Shortage of Skilled Geospatial Professionals Constrains Market Scalability

Europe faces a growing talent gap in geospatial expertise, which is a significant challenge to the growth of the European geospatial solutions market. According to the European Commission’s Digital Skills and Jobs Coalition, many geospatial employers struggle to hire professionals skilled in spatial analytics, machine learning, and cloud GIS. As per Eurostat, the number of geoinformatics graduates annually across the EU is far below the estimated need. As per the European Space Agency’s workforce review, a large share of Earth observation data goes underutilized due to insufficient analytical capacity. In Central and Eastern Europe, vacancy rates for spatial data scientists remain high according to national mapping agencies. Fewer than 20 European universities offer courses in real-time geospatial processing, creating a curriculum lag. This deficit delays deployments and increases reliance on costly consultants, inflating project expenses as per the European Umbrella Organisation for Geographic Information. Without targeted education investment, market growth will remain constrained by human capital shortages.

Inconsistent Access to High-Quality Base Mapping Data Across Regions

Foundational geospatial layers such as cadastral maps, elevation models, and road networks vary widely in quality and recency across Europe, which further challenges the expansion of the European geospatial solutions market. According to the European Environment Agency, only a portion of EU member states provide nationwide sub-meter orthophotography updated within the last three years. In parts of Romania and Greece, topographic data remains outdated according to national statistical offices. During the 2023 Slovenia floods, the European Civil Protection Mechanism reported rescue delays due to misaligned hydrological and road datasets. Commercial providers often compensate by commissioning primary data collection, raising costs in underserved areas, according to the European Association of Remote Sensing Companies. Even in France, rural cadastral boundaries are not fully digitized according to the National Institute of Geographic and Forest Information. Without uniform, current base maps, the accuracy of applications from autonomous navigation to land management is fundamentally compromised across large parts of Europe.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Solution Type, Application, Technology, End User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Apple, Inc., Hexagon AB, Oracle Corporation, Microsoft Corporation, Trimble Inc, Maxar Technologies, Inc. (DigitalGlobe, Inc.), Amazon.com, Inc., IBM Corporation, SNC-Lavalin Group, Inc. (Atkins PLC), Pitney Bowes, Inc., Esri, Inc., TomTom N.V., China Geo-Engineering Corporation (CGC)( China Energy Conservation and Environmental Protection Group) and L3Harris Technologies, Inc. |

SEGMENTAL ANALYSIS

By Solution Type Insights

The software segment dominated the market by commanding 53.5% of the regional market share in 2025. The dominance of the software segment in the European market is attributed to the region’s strong emphasis on digital transformation, data integration, and cloud-based analytics across public and private sectors. European institutions increasingly rely on scalable geospatial software platforms to manage environmental monitoring, urban planning, and infrastructure modeling. One key driver is the widespread adoption of Geographic Information Systems in public administration. As per EuroGeographics, most national mapping agencies in the EU use enterprise-grade GIS software for land registry, cadastral management, and spatial policy design. Another factor is the integration of artificial intelligence with geospatial software. According to the European Commission’s Digital Europe Programme, hundreds of millions of euros have been allocated toward AI-enabled spatial analytics between 2021 and 2027. Additionally, the Copernicus programme’s open data policy has spurred the development of downstream software applications, with tens of thousands of active users of its data processing platforms, as confirmed by the European Space Agency.

The services segment is projected to grow at the highest CAGR of 15.5% over the forecast period in the European geospatial solutions market, owing to the rise of geospatial consulting for sustainability compliance. As per the European Environment Agency, many large corporations now engage third-party geospatial service providers to conduct environmental impact assessments under the EU Taxonomy Regulation. The proliferation of public-private partnerships in smart infrastructure is also contributing to the growth of the services segment in this regional market. For example, Germany’s Federal Ministry of Transport commissioned geospatial service firms to support the digitalization of its federal roads according to official tender documents. Furthermore, the European Investment Bank notes that a majority of Horizon Europe-funded urban resilience projects require outsourced geospatial analytics for simulation and monitoring.

By Application Insights

The planning and analysis segment led the market by accounting for 36.6% of the Europe geospatial solutions market share in 2025 due to the integration of geospatial analytics into national climate strategies. According to the European Environment Agency, all EU member states use geospatial planning tools to model carbon sequestration potential and heat island effects in urban areas. The expansion of spatial epidemiology is also fuelling the growth of the planning and analysis segment in the regional market. During the COVID-19 pandemic, the European Centre for Disease Prevention and Control deployed geospatial planning models across multiple countries to allocate testing resources. Additionally, the EU’s Biodiversity Strategy for 2030 mandates spatial gap analysis for protected areas, requiring member states to conduct geospatial assessments covering significant portions of terrestrial land.

The asset management segment is the fastest-growing application segment and is estimated to register a CAGR of 14.4% over the forecast period owing to the EU’s commitment to modernizing water and energy grids. According to the European Commission, a large share of Europe’s water pipelines are over 50 years old, which is prompting utilities to adopt geospatial asset management systems. In the Netherlands, Vitens uses geospatial asset platforms to monitor its pipelines according to its sustainability report. Another driver is the Rail Baltica project, which employs geospatial asset tracking across new high-speed rail linking the Baltic states to the European network, with real-time condition monitoring mandated by the Connecting Europe Facility.

By End User Insights

The infrastructural development segment dominated the market by capturing 36.5% of the regional market share in 2025. The dominance of the infrastructural development segment in the regional market is attributed to the EU’s mandate for digital twins in major infrastructure projects. The European Commission requires large projects exceeding specific funding thresholds to incorporate geospatial digital modeling. Another factor is urban densification pressures. According to Eurostat, 78% of Europeans live in cities, compelling municipalities to optimize land use through 3D geospatial planning. For example, Paris’s Greater Urban Plan uses geospatial analysis to identify underutilized land for housing according to the Paris Urban Planning Agency. Additionally, the Connecting Europe Facility has allocated billions of euros to transport and energy infrastructure through 2027, much of which relies on geospatial site selection and environmental impact modeling.

The business segment is the fastest-growing end-user category and is anticipated to grow at a CAGR of 15.5% over the forecast period owing to the growing adoption of retail and logistics firms. As per the European Retail Round Table, many large European retailers now use geospatial analytics for site selection and supply chain optimization. In insurance, the European Insurance and Occupational Pensions Authority reports that most property insurers integrate flood and fire risk maps derived from geospatial data into underwriting. Real estate platforms like France’s SeLoger and Germany’s ImmobilienScout24 embed interactive geovisualization to enhance buyer engagement according to internal performance metrics.

COUNTRY-LEVEL ANALYSIS

Germany Geospatial Solutions Market Analysis

Germany had the leading share of 20.6% of the regional market in 2025. The dominance of Germany in the European market is driven by its advanced digital public administration, robust engineering sector, and commitment to Industry 4.0 integration. Germany’s Federal Agency for Cartography and Geodesy maintains one of the world’s most detailed national spatial data infrastructures, with extensive high resolution geodata updated regularly. The Energiewende policy drives geospatial demand in grid planning, with thousands of kilometres of new power lines mapped using LiDAR and GIS for renewable integration as per the Federal Network Agency. Additionally, Germany’s automotive industry relies on centimetre-accurate geospatial data for autonomous vehicle testing, contributing to significant annual private sector geospatial spending according to the VDA.

France Geospatial Solutions Market Analysis

France captured 16.3% of the European market share in 2025. Its position is anchored in strong state-led spatial governance and defense applications. IGN operates the Géoplateforme, a national cloud-based geospatial infrastructure used by thousands of public agencies and private entities. The French Ministry of Armed Forces allocated substantial funding in 2024 for geospatial intelligence satellites under its CSO programme. Civil applications are equally robust as the Grand Paris Express metro expansion uses geospatial digital twins across its extensive network to coordinate workers and prevent subsidence risks. Moreover, France’s agricultural sector leverages geospatial tools on millions of hectares of farmland to comply with the Ecophyto II+ pesticide reduction plan, as confirmed by FranceAgriMer.

United Kingdom Geospatial Solutions Market Analysis

The United Kingdom is anticipated to register a promising CAGR in the European geospatial market during the forecast period, owing to its National Geospatial Framework and strong private sector innovation. The Ordnance Survey’s OS MasterMap remains one of the world’s most detailed topographic databases, updated frequently and widely used by major companies. The UK’s National Digital Twin programme has catalysed billions of pounds in infrastructure digitization since 2020. In finance, London-based firms use geospatial risk platforms to model climate exposure across global portfolios. The government’s Levelling Up agenda has further expanded geospatial use in regional development, with hundreds of millions of pounds allocated in 2025 for spatial analytics in housing and transport planning as per HM Treasury documentation.

Italy Geospatial Solutions Market Analysis

Italy is projected to hold a notable share of the European geospatial solutions market over the forecast period. The country’s demand is driven by seismic risk management, cultural heritage preservation, and agricultural modernization. Italy sits on one of Europe’s most active fault lines, prompting the Civil Protection Department to deploy real-time geospatial monitoring across high-risk regions. The Ministry of Cultural Heritage uses drone-based photogrammetry and GIS to manage thousands of UNESCO sites, including predictive erosion modeling for Venice’s historic center. In agriculture, Italy’s farms increasingly adopt geospatial precision tools, with vineyards in Tuscany and Piedmont using satellite-based canopy analysis to optimize harvest timing according to the National Research Council. The National Recovery and Resilience Plan allocates billions of euros through 2026 for geospatial digitalization in public works.

Netherlands Geospatial Solutions Market Analysis

The Netherlands is estimated to grow at a healthy CAGR in the European geospatial solutions market during the forecast period. The Netherlands is remarkable for its small size but exceptional data maturity. The country’s low-lying geography makes geospatial intelligence critical for water management. Rijkswaterstaat uses geospatial platforms to monitor thousands of kilometers of dikes and pumping stations, preventing significant annual flood damage. The Dutch Cadastre maintains a real-time land registry integrated with 3D building models for millions of structures, enabling instant property valuation and urban planning. The Port of Rotterdam employs AI-driven geospatial logistics systems to manage container flows, reducing idle time as per port authority reports. Additionally, the Netherlands hosts the European GNSS Agency and numerous geospatial startups, supported by the Dutch Ministry of Economic Affairs’ Geodata Innovation Fund, launched in 2023.

COMPETITIVE LANDSCAPE

The Europe geospatial solutions market features intense competition among global technology providers, European public mapping agencies, and agile startups. Established players like Hexagon Trimble and Esri dominate through comprehensive end-to-end platforms while national entities such as Ordnance Survey and IGN leverage sovereign data access and policy influence. The competitive landscape is shaped by rapid technological convergence, where geospatial tools integrate with AI, IoT, and cloud infrastructure. Differentiation arises from domain expertise, regulatory compliance, and localized data accuracy. Startups are gaining ground in specialized niches like real-time mobility analytics and climate risk modeling, often supported by EU innovation grants. With public sector procurement favoring interoperability and open standards, collaboration and ecosystem building are as critical as product innovation driving a dynamic and multi layered competitive environment across the region.

KEY MARKET PLAYERS

The leading companies operating in the Europe geospatial solutions market include:

- Apple, Inc.

- Hexagon AB

- Oracle Corporation

- Microsoft Corporation

- Trimble Inc.

- Maxar Technologies, Inc

- Amazon.com, Inc.

- IBM Corporation

- SNC-Lavalin Group, Inc

- Pitney Bowes, Inc.

- Esri, Inc.

- TomTom N.V.

- China Geo-Engineering Corporation (CGC

- L3Harris Technologies, Inc.

TOP PLAYERS IN THE MARKET

- Hexagon AB is a Swedish technology leader deeply embedded in the Europe geospatial solutions market through its Geosystems division. The company delivers high-precision sensors, reality capture systems, and geospatial software used in surveying, infrastructure, and urban planning across the continent. In recent years, Hexagon has intensified its focus on cloud enabled spatial analytics and digital twin integration. It launched HxDR, a global cloud based digital reality platform that combines satelliteaerial, and ground-based geospatial data to support infrastructure resilience projects in Germany, France, and the Netherlands. The company also expanded partnerships with EU research bodies under Horizon Europe to advance AI-driven geospatial modeling for climate adaptation.

- Trimble Inc maintains a strong footprint in Europe by providing integrated hardware and software solutions for construction agriculture and transportation sectors. Its geospatial offerings include GNSS receivers, laser scanners, and cloud-based data management platforms widely adopted by European engineering firms and public agencies. Trimble recently strengthened its position by enhancing its Trimble Connect collaboration platform with real time geospatial BIM integration enabling cross border infrastructure teams to coordinate seamlessly. The company also deepened its collaboration with European rail operators to deploy geospatial asset tracking for predictive maintenance, aligning with the EU’s Rail Freight Corridors initiative and supporting digital transformation in critical transport networks.

- Esri is a foundational player in Europe’s geospatial ecosystem through its ArcGIS platform, which powers spatial analysis in over 90% of European national mapping agencies and numerous city governments. The company supports EU policy implementation by enabling INSPIRE-compliant data infrastructures and climate risk dashboards. Recently, Esri launched the ArcGIS GeoAI Toolkit in partnership with European academic institutions to accelerate machine learning applications in land use and biodiversity monitoring. It also expanded its cloud operations in Germany and France to ensure GDPR compliant data processing. These actions reinforce Esri’s role not only as a software provider but as an enabler of Europe’s digital sovereignty in spatial intelligence.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe geospatial solutions market prioritize strategic partnerships with public institutions to align with EU regulatory frameworks such as INSPIRE and the Green Deal. They invest heavily in cloud native and AI powered platforms to enable real time spatial analytics and digital twin capabilities. Geographic expansion through localized data centers ensures compliance with stringent European data privacy laws. Companies also focus on vertical-specific solutions targeting sectors like smart infrastructure precision agriculture and defense. Continuous innovation through the acquisition of niche geospatial AI and remote sensing startups allows them to integrate cutting edge capabilities and maintain technological leadership in a rapidly evolving market landscape.

MARKET SEGMENTATION

This research report on the Europe geospatial solutions market has been segmented and sub-segmented into the following categories.

By Solution Type

- Software

- Hardware

- Services

By Application

- Surveying & Mapping

- Geovisualization

- Planning & Analysis

- Asset Management

- Others

By Technology

- Earth Observation

- Gnss & Positioning

- Geospatial Analytics

- Scanning

By End User

- Utility

- Defense & Intelligence

- Infrastructural Development

- Transportation

- Business

- Natural Resource

- Others

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

What is the Europe geospatial solutions market?

The Europe geospatial solutions market provides GIS, remote sensing, and analytics for location-based insights. It supports urban planning, utilities, and transportation across the continent.

What drives the Europe geospatial solutions market?

Smart city initiatives and digital transformation propel the Europe geospatial solutions market. Governments invest in infrastructure monitoring and environmental analytics.

How is the Europe geospatial solutions market segmented?

The Europe geospatial solutions market segments by technology into GIS, GNSS, remote sensing, 3D scanning, plus applications like surveying and asset management.

Which countries lead the Europe geospatial solutions market?

France registers highest growth in the Europe geospatial solutions market, with Germany and UK dominating through advanced GIS adoption in infrastructure.

What role does GIS play in the Europe geospatial solutions market?

GIS/spatial analytics generates largest revenue in the Europe geospatial solutions market powering planning, analysis, and decision-making applications.

Why 3D scanning grows in the Europe geospatial solutions market?

3D scanning registers fastest growth in the Europe geospatial solutions market enabling precise digital twins for construction and heritage preservation.

What applications define the Europe geospatial solutions market?

Surveying, geovisualization, planning, and asset management characterize the Europe geospatial solutions market across utilities and transportation sectors.

What industries use the Europe geospatial solutions market?

Utilities, defense, infrastructure, transportation lead adoption in the Europe geospatial solutions market for operational optimization and monitoring.

How does regulation impact the Europe geospatial solutions market?

EU digital single market rules standardize the Europe geospatial solutions market promoting cross-border data sharing and open geospatial platforms.

What is remote sensing's role in the Europe geospatial solutions market?

Remote sensing provides earth observation data in the Europe geospatial solutions market, supporting agriculture monitoring and environmental protection.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com