Europe Nanotechnology in Medical Devices Market Research Report By Product, Application , End-User & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis (2026 to 2034)

Market Size, 2025

$2,316.06 MnMarket Estimate, 2026

$2,610.06 MnMarket Forecast, 2034

$6,793.07 MnCAGR, 2026–2034

12.7%Europe Nanotechnology in Medical Devices Market Summary

The Europe nanotechnology in medical devices market, valued at USD 2,316.06 million in 2025, is projected to reach USD 6,793.07 million by 2034, expanding at a CAGR of 12.7% driven by precision diagnostics, smart implantables, and nano-enabled therapeutic innovation.

Key Market Highlights

- 2025 Market Size: USD 2,316.06 million

- 2026 Market Size: USD 2,610.06 million

- 2034 Forecast: USD 6,793.07 million

- CAGR (2026–2034): 12.7%

- Base Year: 2025

- Forecast Period: 2026–2034

Quick Growth Drivers

- Accelerated adoption of precision diagnostics and nano-biosensors

- Rising burden of chronic and age-related diseases across Europe

- Growing use of nanostructured coatings in orthopedic and cardiovascular implants

- EU-backed funding under Horizon Europe and EIC for nanomedicine

- Increasing familiarity of regulators with nano-enabled diagnostics and therapeutics

Principal Restraints

- Complex and lengthy regulatory pathways under MDR and EMA overlap

- Lack of harmonized nanomaterial characterization standards

- High compliance costs for SMEs and early-stage innovators

- Persistent public and clinical concerns regarding nanotoxicity

High-Value Opportunities

- Expansion of academic–industry collaborations accelerating clinical translation

- Rising investments in smart, nano-enhanced implantable devices

- Growth of nano-based biochips supporting personalized and genomic medicine

- Integration of AI with nano-diagnostics for real-time molecular sensing

Key Market Challenges

- Limited availability of medical-grade, GMP-certified nanomaterials

- Dependence on complex global supply chains for high-purity nanoparticles

- Absence of nano-specific clinical endpoints for HTA and reimbursement

- Extended trial timelines due to evidence generation complexity

Fastest-Growing Segments

- Biochips: 14.2% CAGR – personalized medicine & multiplex diagnostics

- Diagnostic Applications: 15.1% CAGR – early detection & digital health

- Clinics: 13.7% CAGR – outpatient wound care and nano-textiles

Regional Leadership & Dynamics

- Germany (24.6%) – engineering strength, research hospitals, reimbursement clarity

- France (16.3%) – centralized planning, cancer nanomedicine adoption

- United Kingdom – regulatory agility and academic spin-offs

- Italy – orthopedic & dental nano-implant demand

- Switzerland – precision engineering and biocompatible nano-coatings

What Wins Commercially

- Nano-engineered implant coatings improving osseointegration

- Therapeutic nanocarriers aligned with high-burden diseases

- Strong clinical validation and reimbursement alignment

- Access to EU-funded translational research networks

- Scalable manufacturing with ISO 10993-compliant nanomaterials

Top Strategic Ask for Executives

Invest in nano-enabled implantables and diagnostics with early regulatory engagement, nano-specific evidence frameworks, and secure regional nanomaterial supply chains to accelerate commercialization across Europe.

Leading Players

Some Of The Companies That Are Playing A Dominating Role In The Europe Nanotechnology In Medical Devices Market Include

- B. Braun SE

- Royal Philips

- Medtronic plc

- Smith & Nephew

- PerkinElmer

Europe Nanotechnology in Medical Devices Market Size

The Europe Nanotechnology in Medical Devices Market Size was valued at USD 2316.06 million in 2025, is expected to have 12.7% CAGR from 2026 to 2034, and be worth USD 6793.07 million by 2034 from USD 2610.06 million in 2026.

Nanotechnology in medical devices refers to the integration of engineered nanoscale materials, typically ranging from one to one hundred nanometers, into diagnostic, therapeutic, and monitoring applications to enhance performance, precision, and biocompatibility. Within Europe, this emerging domain has gained traction through innovations such as nanosensors for real-time biomarker detection, nanostructured coatings for implantable devices, and targeted drug delivery systems utilizing nanoparticles. The convergence of nanotechnology with established medical device engineering has enabled the development of smarter, minimally invasive solutions that align with the region’s emphasis on patient-centric care and digital health transformation. European entities are increasingly driving innovation in health-related nanotechnology, resulting in a growing volume of patent applications within the sector, according to findings associated with the European Commission. Additionally, the European Medicines Agency has established increasing familiarity with nano-enabled therapeutics and diagnostics by reviewing a rising number of nanomedicine submissions, enhancing the regulatory path for these products. These indicators reflect a foundational ecosystem that supports the clinical translation of nanotechnology-integrated medical devices, even in the absence of large-scale commercial deployment across all segments.

MARKET DRIVERS

Accelerated Adoption of Precision Diagnostics is Fueling Market Demand

The integration of nanotechnology into diagnostic medical devices is reshaping early disease detection and monitoring paradigms across the region, which drives the growth of the European nanotechnology in medical devices market. Nanomaterials such as quantum dots, gold nanoparticles, and magnetic nanocrystals enable ultrasensitive biosensing platforms capable of detecting biomarkers at concentrations far below conventional thresholds. This capability is particularly critical in oncology and neurodegenerative disorders, where early intervention drastically alters prognosis. A significant portion of new cancer cases in Europe are identified in intermediate to advanced stages, indicating a continued need for improved early detection methods, a gap that nanodiagnostics are being developed to address. The European Union has dedicated substantial funding through Horizon Europe for the development of nanotechnology-enabled diagnostic tools. Pilot studies in certain European countries suggest that nano-biosensors have the potential to speed up the detection of sepsis biomarkers compared to traditional laboratory methods. This diagnostic acceleration not only enhances clinical outcomes but also aligns with national healthcare strategies focused on cost containment through preventive and predictive medicine, thereby intensifying demand for nano-integrated diagnostic devices.

The growing prevalence of Chronic Diseases is Creating Sustained Clinical Need.

Chronic conditions such as cardiovascular diseases, diabetes, and chronic respiratory illnesses continue to exert immense pressure on European healthcare systems, and thereby fuel the development of the European nanotechnology in medical devices market. This creates a fertile ground for advanced therapeutic and monitoring solutions powered by nanotechnology. A substantial proportion of adults across the European Union experience chronic health conditions, with prevalence rising steadily alongside an aging demographic. Nanotechnology enables the development of implantable and wearable devices that offer continuous physiological monitoring and targeted therapy delivery with minimal invasiveness. For example, advanced stent technologies, including nanocoated varieties, have substantially decreased the occurrence of restenosis in patients following angioplasty procedures. Similarly, glucose-sensing nano patches under development in France and Sweden aim to replace traditional finger-prick tests by enabling transdermal monitoring through sweat analysis. These innovations directly address patient adherence challenges and the economic burden associated with long-term disease management. Consequently, the persistent and expanding base of chronically ill patients in Europe acts as a powerful demand catalyst for nanotechnology-infused medical devices that promise improved efficacy, reduced hospitalization, and enhanced quality of life.

MARKET RESTRAINTS

Stringent Regulatory Pathways Impede Timely Commercialization

The European regulatory framework for nanotechnology-based medical devices remains complex and inconsistently applied across member states, which creates significant delays in market entry. Consequently, this restrains the growth of European nanotechnology in the medical devices market. Unlike conventional devices, nano-enabled products often straddle the boundary between medical devices and medicinal products, triggering dual assessments under both the Medical Devices Regulation and the European Medicines Agency guidelines. This ambiguity results in prolonged evaluation timelines and increased compliance costs. In the European Union, the regulatory approval process for advanced nanotechnology-integrated devices typically takes longer than the standard, already rigorous timeline for conventional high-risk Class III medical devices. Moreover, the lack of standardized characterization protocols for nanomaterials, such as size distribution, surface charge, and aggregation behavior, further complicates conformity assessments under the notified body system. Evaluations by European regulatory authorities regarding nanomaterial submissions have indicated that a significant majority of submitted dossiers lack sufficient physicochemical data, highlighting a need for improved, high-quality data generation in safety evaluations. These regulatory gaps not only deter small and medium enterprises lacking regulatory expertise but also discourage cross-border harmonization, ultimately stifling innovation despite strong scientific readiness.

Public Concerns Regarding Nanotoxicity Undermine Market Acceptance

Persistent public skepticism about the long term biological effects of engineered nanomaterials continues to challenge widespread adoption of nano-based medical devices in the region, which hinders the European nanotechnology in medical devices market. Concerns primarily revolve around potential cytotoxicity, biodistribution anomalies, and environmental persistence of nanoparticles following device degradation or disposal. Public perception of medical nanotechnology indicates varying levels of caution among citizens regarding the transparency of safety data. Concerns surrounding these applications appear to influence both prescribing practices and decisions related to reimbursement. Reports have highlighted instances of adverse reactions, such as inflammatory responses, associated with certain nanoparticle-based products, prompting further investigation. Observations suggest that a significant portion of nano-medical waste may not be processed through specialized disposal channels, leading to questions about environmental impact. Such uncertainties impede patient trust and complicate post market surveillance requirements, forcing manufacturers to invest heavily in long term biocompatibility studies. Market adoption of nanotechnology in medicine is constrained more by perceived safety risks than technical hurdles, requiring standardized toxicity assessments to overcome this gap.

MARKET OPPORTUNITIES

Expansion of Academic Industry Collaborations is Unlocking Innovation Pathways

The region’s robust academic infrastructure is increasingly aligning with private sector objectives to accelerate the translation of nanotechnology concepts into clinically viable medical devices, which provides new opportunities for the European nanotechnology in medical devices market. Leading universities in the United Kingdom, Switzerland, and Sweden have established dedicated nanomedicine incubators that provide shared cleanroom facilities, regulatory advisory services, and pilot manufacturing capabilities. The European Innovation Council is actively fostering public-private collaborations to advance nano-medical device technologies under the current EU funding framework, with a stronger emphasis on cross-sectoral, solution-driven partnerships compared to the previous funding cycle. Notably, the NanoMedIC initiative—a consortium spanning nine European countries—has successfully developed a nanoparticle-based intraoperative imaging probe now undergoing multicenter trials for real-time tumor margin delineation. These collaborations not only de risk early stage R and D but also facilitate access to patient cohorts and clinical validation sites, which are critical for regulatory submissions. Moreover, national innovation agencies in Europe, including those in Sweden and France, are providing substantial financial support to assist startups in developing and validating prototype medical devices incorporating nanotechnology. This ecosystem of coordinated support significantly shortens the innovation to commercialization timeline and positions Europe as a global testbed for next-generation nano-enabled healthcare solutions.

Rising Investments in Smart Implantables Present High Growth Potential

The convergence of nanotechnology with smart implantable devices represents a frontier opportunity in the region’s medical device landscape, which creates fresh prospects for the European nanotechnology in medical devices market. This shift is driven by the need for long-term chronic disease management and real-time physiological feedback. Nanomaterials such as graphene and carbon nanotubes are being incorporated into pacemakers, neural interfaces, and orthopedic implants to enhance electrical conductivity, mechanical strength, and biointegration. Public funding initiatives in Europe are actively supporting the development of smart implant technologies. Researchers are developing advanced titanium hip implants with surface modifications designed to trigger beneficial biological responses to local environmental changes. Preliminary trials suggest that these specialized orthopedic implants may lead to a reduction in the need for follow-up revision surgeries. Innovation in the sector includes commercialized cochlear implants featuring nanocoatings that resist biofilm formation, addressing a common cause of device malfunction. These technological advancements are supported by a strong regional manufacturing base and a research focus in biocompatible material science. The clinical trial pipeline for advanced nano-engineered implantables is active and growing. The ability of smart, nano-enhanced implants to deliver durable, low-maintenance, and responsive solutions makes them a key growth driver as healthcare shifts toward value-based care.

MARKET CHALLENGES

Complex Supply Chains for High-Purity Nanomaterials Create Manufacturing Bottlenecks

The production of medical-grade nanomaterials demands extreme precision in particle size control, surface functionalization, and batch-to-batch consistency, which remains a challenge for the European nanotechnology in medical devices market. These requirements are met by only a limited number of specialized suppliers in the region. Unlike bulk chemicals, nanomaterials used in medical devices must comply with stringent ISO 10993 biocompatibility standards and undergo rigorous endotoxin testing, which significantly narrows the vendor pool. The availability of GMP-certified nanomaterials for implantable devices within Europe is limited, resulting in a reliance on suppliers from other regions. Dependence on external sourcing for these materials introduces risks related to supply chain interruptions and trade restrictions. Variations in quality among imported nanomaterials have disrupted production processes for certain medical device manufacturers. Stringent material specifications, particularly regarding size distribution, can challenge the reliability of international supply chains. Additionally, the capital intensity of nanomaterial synthesis, requiring advanced equipment such as microfluidic reactors and plasma synthesis units, deters new entrants. Europe risks delayed device launches and higher production costs without immediate strategic investment in regional nanomaterial manufacturing and harmonized quality standards.

Lack of Standardized Clinical Endpoints for Nano-Enabled Devices Hinders Evidence Generation

The absence of universally accepted clinical endpoints and performance metrics specific to nanotechnology-based medical devices complicates comparative effectiveness research and health technology assessment in the region. This further constrains the expansion of European nanotechnology in the medical devices market. Traditional evaluation frameworks often fail to capture the unique value propositions of nano devices, such as sustained drug release kinetics, localized tissue interaction, or real-time molecular sensing, resulting in inconclusive or unfavorable reimbursement decisions. A notable proportion of nanomaterial-based medical device submissions have often lacked validation for specific nanoscale intervention endpoints, frequently resulting in requests for supplementary clinical evidence. This pattern of missing specialized endpoints is particularly observed in clinical applications related to cancer treatment and tissue regeneration, where traditional measures of efficacy may not fully capture the biological action of nano-formulations. Standard clinical markers, such as those used to track tumor progression, do not consistently align with imaging data that tracks how nanoparticles gather in tumor tissue. Consequently, manufacturers face extended clinical trial durations and higher development costs to generate acceptable evidence bundles. European regulatory and payer bodies must create nano-specific criteria, as the current high evidentiary burden acts as a structural barrier to adoption.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

| Key Market Players | AMAG Pharmaceuticals, Jude Medical, Inc., Smith & Nephew, Inc., and PerkinElmer. |

SEGMENTAL ANALYSIS

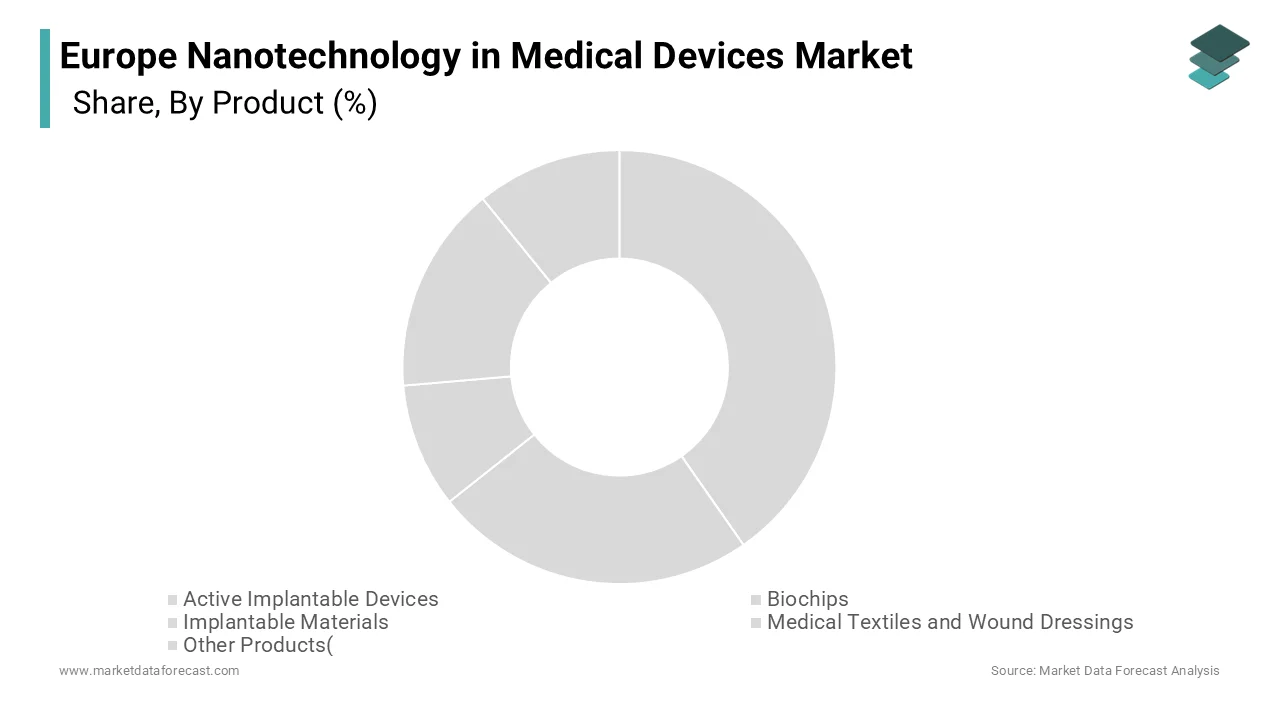

By Product Insights

The implantable materials segment captured the majority share of 38.1% of the European nanotechnology in medical devices market in 2025. The supremacy of the implantable materials is attributed to the widespread adoption of nano-engineered surfaces and coatings in orthopedic, dental, and cardiovascular implants to enhance osseointegration, reduce infection risk, and prolong device lifespan. Europe faces a rapidly aging population, with the share of citizens aged 65 and above reaching a notable share in 2024, according to sources. This demographic shift has intensified demand for joint replacements and dental prosthetics, driving innovation in implant materials. Nano hydroxyapatite and titanium dioxide coatings significantly improve bone bonding. Research indicates that surface modifications on dental implants, such as nanostructures, are associated with an accelerated integration into bone tissue compared to traditional surfaces. Clinical applications for orthopedic implants, specifically in hip replacements, frequently incorporate nanostructured coatings to enhance performance. The use of nanostructured dental implants represents a trend toward improving the speed of healing compared to conventional implant options. The adoption of nanocoatings is a notable pattern in the field of joint replacement surgeries. This clinical reliance onperformance-enhancedd materials underpins the segment’s leadership. European regulatory bodies actively encourage the development of safer and more effective implant materials. The European Commission’s Horizon Europe program has consistently directed substantial funding toward research, development, and application of advanced, nanostructured biomaterials for medical and health applications, including projects focusing on antibiofilm and regenerative materials. Additionally, ISO standards for nanomaterial characterization in medical devices have streamlined product validation. Countries like Switzerland and Sweden host leading biomaterial manufacturers, such as Straumann and Additive Works, that integrate nanotexturing into commercial implant lines. The orthopedic implant industry in Europe is rapidly adopting nanoscale surface modifications as a standard approach to improve biocompatibility, osseointegration, and bacterial resistance.

The biochips segment is estimated to register the fastest CAGR of 14.2% from 2026 to 2034 due to rising investments in personalized medicine, point-of-care diagnostics, and genomic screening. European healthcare systems are increasingly integrating molecular profiling into cancer care pathways. Oncology drug approvals increasingly require paired molecular diagnostic testing to guide treatment, often utilizing nano-based biochip platforms for necessary gene expression and mutation analyses. This trend is supported by national cancer strategies promoting standardized molecular profiling, which boosts the use of biochip technologies capable of high-throughput, multiplexed detection with minimal sample volume, essential for liquid biopsies. Consequently, there is an observed rise in the adoption of nano-biochip technology within genomic testing laboratories in European regions. Biochips are central to Europe’s digital health transformation. European health data initiatives are encouraging the adoption of interoperable diagnostic tools, which highlights the role of nano biochips in facilitating continuous health monitoring. Collaborations between research institutions and semiconductor firms are advancing the development of silicon-based nano biochips that can detect multiple biomarkers from a single blood sample. Pan-European consortia are receiving support to develop AI-integrated nano biochips designed for the early detection of conditions within intensive care environments. Such convergence of nanotechnology, data science, and clinical need is propelling unprecedented adoption and justifying the segment’s leading growth trajectory.

By Application Insights

The therapeutic applications segment led the European nanotechnology in medical devices market by capturing a 45.5% share in 2025. The leading position of the therapeutic applications segment is credited to the clinical deployment of nanotechnology for targeted drug delivery, regenerative medicine, and implant functionalization. Nanoparticle-based therapeutics are now standard in several European treatment protocols. PEGylated liposomal doxorubicin has established a long-term presence in European clinical practice for managing specific solid tumors and AIDS-related Kaposi’s sarcoma. The regulatory environment has expanded to include lipid nanoparticle-based, RNA-interference therapies for genetic diseases. The clinical landscape shows a sustained volume of investigation into nanotherapeutic approaches, particularly targeting solid tumor treatment, while statutory healthcare systems in certain countries have integrated multiple nanotechnology-formulated medications, indicating, in some regions, a systemic acceptance. This therapeutic penetration across high-burden diseases sustains the segment’s dominance. Europe leads global research in tissue engineering, with nanotechnology playing a pivotal role in scaffold design. Nano-fibrous matrices mimicking extracellular structures enhance stem cell adhesion and differentiation. International clinical efforts are exploring the utility of specialized collagen structures for addressing long-term wound recovery and joint tissue restoration. Regional research initiatives have increased support for developing advanced biological materials aimed at repairing heart tissue. Such institutional commitment ensures a steady pipeline of therapeutic applications beyond conventional drug delivery.

The diagnostic applications segment is anticipated to witness the fastest CAGR of 15.1% during the forecast period, owing to the shift toward early detection, decentralized testing, and integration with digital health platforms. National screening programs across Europe are adoptingnano-enabledd diagnostics to improve sensitivity. National health strategies are increasingly incorporating advanced diagnostic technologies, such as liquid biopsies and nano-based biosensors, to improve cancer survival rates through earlier detection and monitoring. Public health initiatives are actively utilizing, or piloting, nanotechnology-based diagnostic tools, such as lateral flow assays, to improve the detection accuracy of cancers in screening programs. Point-of-care, non-invasive, and rapid diagnostics are being prioritized, with significant funding being directed toward nano-based platforms for improved patient monitoring and treatment. There is a clear shift toward integrating molecular diagnostics and nanotechnology, such as gold nanoparticles, to improve the sensitivity and specificity of cancer screenings. Diagnostic innovation is increasingly being supported by, or aligned with, national health funding for improving cancer management and reducing treatment times. Nano diagnostics are increasingly embedded in connected health ecosystems. Developments in graphene-based nano-sensors have enabled the real-time monitoring and transmission of metabolic data directly to mobile devices, offering a potential alternative to traditional clinic-based monitoring for chronic conditions. The integration of nano-diagnostic technology with artificial intelligence is receiving targeted funding to enhance diagnostic capabilities and personalized healthcare solutions. Research suggests that the implementation of advanced, continuous monitoring technologies can alter the frequency of in-person medical consultations for patients managing metabolic conditions. Public sector investment initiatives are actively supporting projects that combine nanotechnology and AI to improve diagnostic efficiency. This fusion of nanoscale sensing with predictive analytics creates scalable, cost-effective surveillance models, especially vital in aging societies, propelling diagnostic applications beyond research into routine care.

By End Users' Insights

The hospitals segment was the largest segment in the European nanotechnology in medical devices market by holding a significant share in 2025. The prominence of the hospitals segment is supported by its role as primary sites for complex interventions, surgical implantation, and advanced diagnostics. Procedures involving nano drug delivery systems, smart implants, or intraoperative nanosensors require specialized infrastructure and multidisciplinary teams found predominantly in large hospitals. Nanotherapeutics administered in Europe are frequently concentrated in university-affiliated hospitals. The delivery of specific advanced cell therapies using nanocarriers in Germany primarily occurs within specialized hematologic oncology centers. These certified hospital-based facilities represent the main sites for the application of these advanced therapies in Germany. The capital intensity of nano imaging systems, like nano MRI contrast agents,s further restricts deployment to well-funded institutions. European healthcare systems typically reimburse high-cost nano devices only within hospital settings under Diagnosis-Related Group frameworks. Reimbursement for specialized nanocoated cardiac implants in some European regions is integrated into comprehensive hospital billing structures rather than separate outpatient schemes. Hospital-based purchasing groups frequently negotiate contracts for a majority of nanotechnology-enabled medical devices, leveraging high-volume procurement to facilitate access to advanced medical technology. This institutional procurement dominance ensures hospitals remain the primary commercial channel.

The clinics segment is likely to experience the fastest CAGR of 13.7% from 2026 to 2034. The rapid expansion of the clinics segment is fueled by the decentralization of chronic care and the rise of specialized outpatient centers. Outpatient management of chronic wounds and skin conditions has surged, with clinics adopting silver and chitosan nanoparticle dressings for antimicrobial efficacy. Specialized wound clinics across Europe widely utilize nano dressings in their standard procedures. Private dermatology clinics in Spain have increased the use of nano topical products, influenced by patient demand for scar reduction and anti-aging applications. These high-margin and low-risk applications are economically viable in clinic settings. Class I and IIa nano devices, such as nano-infused bandages or diagnostic patches, face streamlined CE marking routes, enabling rapid clinic adoption. Approved nano medical textiles are increasingly being cleared for outpatient use. Healthcare systems are incorporating nano-enabled monitoring devices into primary care protocols, which may contribute to a decrease in reliance on traditional laboratory services. National health initiatives are beginning to include nanomedical technologies for managing chronic conditions. This regulatory and operational alignment positions clinics as agile adopters of next-generation nano devices, accelerating their market share growth.

COUNTRY LEVEL ANALYSIS

Germany Nanotechnology In Medical Devices Market Analysis

Germany dominated the European nanotechnology in medical devices market by accounting for a 24.6% share in 2025. The dominance of the German market is driven by its world-class engineering base, dense network of research hospitals, and strong public investment in medtech innovation. The national medical device sector features a high density of manufacturers, including major international firms, that are increasingly incorporating nanomaterials into cardiovascular and orthopedic products. Significant funding has been directed toward nanomedicine initiatives, driving projects focused on translating advanced materials into clinical applications. The regulatory environment has adopted a structured approach to approving reimbursement for nanotech-based therapeutic and diagnostic devices, providing a clearer commercial pathway. Leading academic and research institutions are advancing the clinical translation of nano-based technologies, particularly regarding implants and biosensors. The concentration of active clinical trials and research initiatives highlights a strong, growing focus on nanotechnology within the national health technology landscape.

France Nanotechnology In Medical Devices Market Analysis

France was the next prominent country in the European nanotechnology in medical devices market by capturing a share of 16.3% in 2025. The growth of the French market is propelled by centralized healthcare planning and strategic national health programs. Public investment initiatives in France have directed substantial funding toward the development of health technologies, with a specific focus on the intersection of nanotechnology and personalized medical approaches. The nation has developed a significant capability in utilizing nanotechnology for cancer treatments, resulting in a high volume of patients receiving these specialized formulations. The adoption and coverage of nanodrugs within the healthcare system have experienced a notable upward trend over recent years. Moreover, France’s strong biotech corridor in Lyon and Paris fosters startups like Cytimmune Sciences Europe, which develops gold nanoparticle platforms for tumor targeting. The integration of nano diagnostics into the national cancer screening program further cements France’s high adoption rate and market scale.

United Kingdom Nanotechnology In Medical Devices Market Analysis

United Kingdom holds a noteworthy position in the European nanotechnology in medical devices market due to a robust academic-industrial nexus and post Brexit regulatory agility. Regulatory bodies in the UK have implemented specialized evaluation units for nanotechnology, leading to faster review processes than certain regional averages. Academic institutions in the UK are actively producing new startups focused on areas such as biochips and neural interfaces. Healthcare systems in the UK are increasingly incorporating advanced nanotechnology-based products, such as specialized dressings, into community care settings. National research funding initiatives are providing dedicated investment to support the ongoing development and commercialization of nanomedicine technologies.

Italy Nanotechnology In Medical Devices Market Analysis

Italy experienced a consistent growth in the European market, with strength in implantable materials and regenerative medicine. Its high volume of orthopedic and dental procedures, a large number of joint and dental implants annually, creates natural demand for nnano-enhancedsurfaces. Italian firms like SintX Technologies and Bio-Gate produce nanoceramic and antimicrobial coatings widely adopted across Southern Europe. Regulatory bodies are increasingly facilitating faster reviews for medical products that incorporate advanced materials designed to enhance implant durability. The approval of various nano-enabled medical devices has continued over the past few years. Collaborative efforts between public research institutions and healthcare facilities are exploring the use of nano-scaffolds to aid in bone regeneration. Initial pilot studies evaluating these regenerative materials have demonstrated positive outcomes in patients. This clinical validation, combined with aging demographics, solidifies Italy’s niche leadership.

Switzerland Nanotechnology In Medical Devices Market Analysis

Switzerland is anticipated to expand in the European nanotechnology in medical devices market from 2026 to 2034, owing to its population weight through precision engineering and regulatory excellence. Home to global medtech giants like Roche Diagnostics and Sonova, Switzerland leverages nanotechnology in high-value diagnostic and auditory implant segments. Research funding for nanotechnology in medicine has focused heavily on biocompatibility and microfabrication techniques. Advancements in anti-biofilm coatings are being applied to devices designed for implantation, such as those used for hearing restoration. The application of these nano-coatings is associated with a decrease in the need for revision surgeries related to infections. Data from clinical environments indicates that a high proportion of certain implants produced in the region now incorporate these advanced coatings. Switzerland’s mutual recognition agreements with the EU facilitate swift market access, while its ISO 13485-certified nanomaterial suppliers serve as critical enablers for the broader European ecosystem. This combination of innovation quality and regulatory efficiency sustains Switzerland’s outsized influence.

COMPETITIVE LANDSCAPE

The Europe Nanotechnology In Medical Devices Market features a moderately consolidated competitive landscape characterized by a mix of global medtech giants and specialized European innovators. Established players leverage extensive R and D infrastructure and regulatory expertise to dominate high complexity segments such as active implantables and nano therapeutics. Meanwhile, agile startups and spin-offs from leading universities focus on niche applications like biochips and nano-wound dressings, often supported by Horizon Europe grants. Intense competition is evident in the race to achieve first-mover advantage in AI-integrated nano diagnostics and regenerative implants. Strategic differentiation hinges on clinical validation, depthof manufacturing, scalability, and alignment with national reimbursement frameworks. Cross-border partnerships and participation in EU-level standardization initiatives further intensify rivalry as companies vie for influence in shaping the future of nano-enabled healthcare delivery across the region.

KEY MARKET PLAYERS

Companies playing a leading role in the europe nanotechnology in medical devices market profiled in the report are

- AMAG Pharmaceuticals,

- Jude Medical, Inc.,

- Smith & Nephew, Inc.,

- PerkinElmer, Inc.,

- Acusphere, Inc.,

- 3M Company,

- Affymetrix, Inc.,

- Starkey Hearing Technologies,

- Stryker Corporation.

TOP LEADING PLAYERS IN THE MARKET

- B Braun SE is a leading German medical technology company deeply engaged in integrating nanotechnology into drug delivery systems and implantable devices. The company has pioneered nano-coated catheters and infusion systems that reduce infection risks through antimicrobial nanoparticle integration. In recent years, B. Braun has intensified collaboration with European research institutes to develop smart implants featuring nano sensors for real-time physiological monitoring. Its initiatives underscore its commitment to advancing patient safety and clinical efficacy through nanoscale innovation in Europe and globally.

- Royal Philips leverages nanotechnology to enhance diagnostic imaging and wearable health monitoring solutions across Europe. The company has embedded quantum dot nanomaterials into its advanced imaging platforms to improve resolution and reduce radiation doses in CT and MRI systems. Philips has also introduced nano-engineered biosensors in its wearable ECG patches, enabling continuous cardiac monitoring with greater accuracy. Its strategic alignment with academic and clinical leaders reinforces its global footprint innano-enabledd precision diagnostics and remote patient care.

- Medtronic plc actively incorporates nanotechnology into its cardiovascular and neurological implant portfolios in Europe. The company utilizes nano-textured surfaces on pacemakers and neurostimulators to enhance tissue integration and reduce fibrosis. Medtronic has invested significantly in nano drug-eluting stents that provide localized anti-inflammatory effects with improved pharmacokinetics. Medtronic also participates in EU-funded consortia such as NanoReg2 to shape regulatory frameworks for nanomedical devices, strengthening its influence in both European and global markets.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in theEuropeane Nanotechnology in Medical Devices Market predominantly employ strategic collaborations with academic and clinical institutions to co-develop validated nano solutions. They invest heavily in dedicated research facilities to enhance in-house nanomaterial characterization and biocompatibility testing capabilities. Companies also pursue regulatory alignment by participating in EU advisory groups to shape safety and standardization protocols. Product portfolio expansion through integration of nanosensors into existing diagnostic and therapeutic platforms remains a core tactic. Additionally, firms prioritize geographic consolidation by establishing regional nano innovation hubs to accelerate market responsiveness and clinical adoption across diverse European healthcare systems.

MARKET SEGMENTATION

This research report on the europe nanotechnology in medical devices market has been segmented and sub-segmented into the following categories.

By Product

- Active Implantable Devices

- cardiac pacemakers

- Neurostimulators

- Implantable Drug Delivery Systems

- Biochips

- Lab-On-A-Chip Devices

- DNA Microarrays

- Protein Microarrays

- Implantable Materials

- Nanocomposite Materials

- Biodegradable Polymers

- Coatings For Implants

- Medical Textiles and Wound Dressings

- Nanofiber Dressings

- Antimicrobial Textiles

- Smart Textiles For Monitoring

- Other Products(Nanoparticles For Imaging, Diagnostic Devices Incorporating Nanotechnology)

By Application

- Therapeutic Applications

- Diagnostic Applications

- Research Applications

By End-Users

- Hospitals

- Clinics

- Other End-Users

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What drives growth in the Europe Nanotechnology in Medical Devices Market?

Growth in the Europe Nanotechnology in Medical Devices Market stems from high chronic disease prevalence, aging populations, and EU funding like Horizon Europe for nanotech R&D. Technological integrations such as AI with nanosensors and favorable MDR regulations further accelerate adoption in countries like Germany and the UK

2. Which countries lead the Europe Nanotechnology in Medical Devices Market?

Germany holds the largest share in the Europe Nanotechnology in Medical Devices Market due to high healthcare spending and tech advancements, followed by the UK with strong R&D collaborations. France, Italy, and Spain also contribute significantly through chronic disease management innovations.

3. What are key applications in the Europe Nanotechnology in Medical Devices Market?

Key applications in the Europe Nanotechnology in Medical Devices Market include drug delivery systems, implantable materials, biochips, and active implants for targeted therapies. Nanoparticles enhance imaging and diagnostics, particularly for oncology, improving precision medicine outcomes.

4. Who are major players in the Europe Nanotechnology in Medical Devices Market?

Major players in the Europe Nanotechnology in Medical Devices Market include companies focusing on nanomaterials and nanosensors, supported by mergers and R&D hubs in Germany and the UK. Innovations in eco-friendly nanoparticles and IoMT integrations define competitive strategies.

5. How does EU MDR impact the Europe Nanotechnology in Medical Devices Market?

EU MDR (2017/745) imposes stricter safety and performance requirements on the Europe Nanotechnology in Medical Devices Market, affecting nanomaterial classifications and Notified Body certifications. This ensures biocompatibility but challenges SMEs, boosting demand for compliance expertise.

6. What role do nanoparticles play in Europe Nanotechnology in Medical Devices Market?

Nanoparticles in the Europe Nanotechnology in Medical Devices Market enable targeted drug delivery, enhanced imaging, and biosensors for real-time monitoring. Gold NPs act as radiosensitizers, while carbon nanotubes improve implant stability, reducing immune responses.

7. What are emerging trends in Europe Nanotechnology in Medical Devices Market?

Emerging trends in the Europe Nanotechnology in Medical Devices Market include AI-IoMT nanosensors, nanorobots for therapy, and sustainable nanomaterials. Personalized medicine and wearable nanodevices address aging demographics and chronic conditions.

8. What challenges face the Europe Nanotechnology in Medical Devices Market?

Challenges in the Europe Nanotechnology in Medical Devices Market involve regulatory hurdles under MDR, nanomaterial toxicity concerns, and scaling production. Immune responses to debris and high R&D costs limit widespread adoption despite growth potential.

9. How does nanotechnology improve medical implants in Europe market?

Nanotechnology improves medical implants in the Europe market by enhancing biocompatibility and longevity using carbon nanotubes mimicking bone collagen. This boosts integration, reduces rejection, and supports applications in orthopedics and cardiology.

10. What is the role of nanotechnology in diagnostics for Europe market?

Nanotechnology in diagnostics for the Europe Nanotechnology in Medical Devices Market uses nanosensors and biochips for high-resolution imaging and early detection. It improves MRI contrast and ultrasound reflectivity, aiding cancer and chronic disease screening.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com