Europe Simulation Software Market Size, Share, Trends and Growth Forecasts Research Report, Segmented By Deployment, Application, Industry and Country – Industry Analysis (2026 to 2034)

Europe Simulation Software Market Report Summary

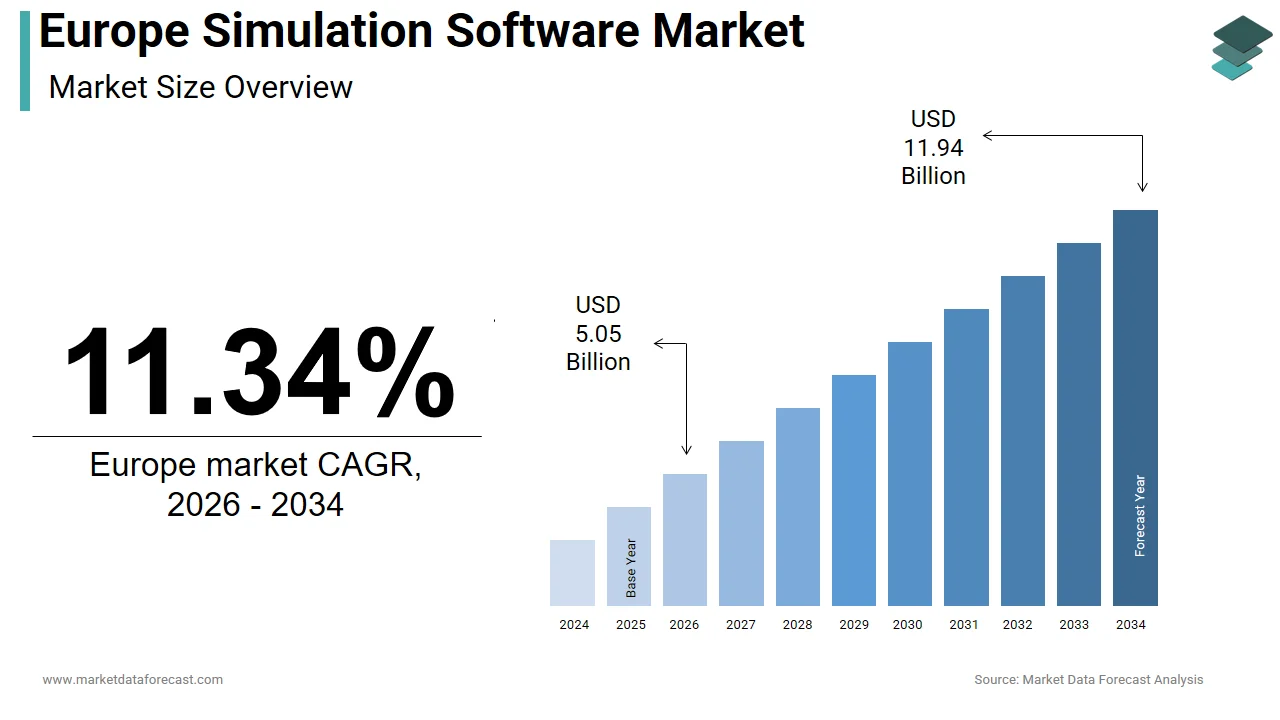

The Europe simulation software market was valued at USD 4.54 billion in 2025 and is projected to grow from USD 5.05 billion in 2026 to USD 11.94 billion by 2034, registering a CAGR of 11.34% from 2026 to 2034. Market growth is driven by increasing adoption of digital twins, rising demand for virtual prototyping, and the need to reduce product development time and costs across industries. Strong uptake across automotive, aerospace, manufacturing, and industrial automation sectors, along with advancements in high-performance computing and AI-assisted simulation, is accelerating market expansion across Europe.

Key Market Trends

- Growing adoption of digital twin and virtual prototyping technologies.

- Rising demand for simulation-driven product engineering and validation.

- Increased use of advanced modeling and multiphysics simulation tools.

- Continued preference for on-premises deployment in data-intensive engineering environments.

- Strong integration of simulation software with AI, IoT, and automation platforms.

Segmental Insights

- Based on deployment, the on-premises segment held a prominent share of the Europe simulation software market in 2025, driven by the need for high computational performance, data security, and integration with legacy engineering systems.

- Based on application, the product engineering segment led the market in 2025, supported by extensive use of simulation tools in design optimization, testing, and performance validation.

- Based on industry, the automotive segment accounted for the largest market share in 2025, driven by increasing use of simulation in vehicle design, electrification, safety testing, and autonomous systems development.

Regional Insights

The Europe simulation software market is witnessing strong growth across major industrial economies, supported by advanced engineering capabilities and high R&D investment.

- Germany was the top-performing market in 2025, driven by its strong automotive manufacturing base and leadership in industrial engineering and automation.

- France ranked second, supported by its aerospace, defense, and nuclear engineering sectors, which rely heavily on advanced simulation and modeling tools.

Competitive Landscape

The Europe simulation software market is characterized by strong competition among global software vendors and specialized engineering simulation providers. Leading companies are focusing on expanding multiphysics capabilities, enhancing AI-driven simulation, and integrating cloud-enabled workflows alongside traditional on-premises systems. Strategic partnerships with industrial enterprises and continuous product innovation remain key competitive strategies.

Prominent companies operating in the Europe simulation software market include Autodesk Inc., ANSYS, Inc., Dassault Systemes, Altair Engineering Inc., The AnyLogic Company, Siemens Digital Industries Software, Flex Ltd., Rockwell Automation, Inc., Bentley Systems, Inc., Simulations Plus, and MathWorks, Inc.

Europe Simulation Software Market Size

The Europe simulation software market was valued at USD 4.54 billion in 2025. The regional market is projected to grow from USD 5.05 billion in 2026 to reach USD 11.94 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 11.34% from 2026 to 2034.

The simulation software is the digital tools that model real-world physical processes ranging from fluid dynamics and structural mechanics to electromagnetic fields and thermal behavior to enable virtual prototyping, testing, and optimization across engineering, design, manufacturing, and scientific research. These solutions reduce reliance on physical testing, lower development costs, and accelerate time to market while supporting compliance with stringent EU regulatory standards. Europe’s leadership in high-value engineering sectors, including aerospace, automotive, and medical devices, creates a fertile environment for advanced simulation adoption.

MARKET DRIVERS

Regulatory Acceptance of Simulation for Product Certification and Compliance

The regulatory bodies increasingly recognize simulation as a valid substitute for physical testing in high-risk industries, dramatically increasing software adoption, which is a major factor accelerating the growth of the Europe simulation software market. According to the European Medicines Agency, in silico clinical trials are now accepted for Class III medical devices when validated under ISO 13485 and ISO 25000 standards by reducing approval timelines by up to 40%. In automotive, the EU General Safety Regulation mandates advanced driver assistance system validation through virtual scenarios requiring over 100000 simulated driving hours per vehicle type. These regulatory shifts de risk in digital engineering and compel companies to invest in certified simulation platforms. Siemens Healthineers and Dassault Systèmes have responded by embedding regulatory templates directly into their software by ensuring compliance by design and accelerating market entry across Europe’s heavily regulated sectors.

Industrial Demand for Digital Twins in Smart Manufacturing

The integration of simulation into digital twin frameworks by enabling real-time process optimization and predictive maintenance is another attribute prompting the growth of the Europe simulation software market. Airbus uses ANSYS-based digital twins to simulate wing assembly stress in real time, reducing rework by 22% at its Hamburg facility, as documented by the German Aerospace Center. Similarly, BMW’s Regensburg plant runs live simulations of paint shop airflow and thermal dynamics to maintain quality under variable conditions. The EU’s Important Project of Common European Interest on Next Generation Cloud Infrastructure has allocated 400 million euros to support digital twin interoperability standards.

MARKET RESTRAINTS

High Licensing Costs and Total Cost of Ownership for Advanced Solvers

The advanced solvers are expensive for small and medium enterprises that form the backbone of Europe’s industrial ecosystem, which is one of the factors hampering the growth of the Europe simulation software market. The average annual license for a high-fidelity multiphysics suite exceeds 75000 euros, with high-performance computing add-ons increasing costs by 40 to 60%. Only 24% of EU manufacturing SMEs use advanced simulation due to budget constraints, relying instead on simplified tools or outsourcing. Although cloud-based pay-per-use models are emerging, most vendors still rely on perpetual licenses with costly annual maintenance fees.

Shortage of Skilled Personnel Proficient in Advanced Simulation Techniques

The effective deployment of simulation software requires engineers trained in computational modeling, numerical methods, and domain-specific physics, with a skill set in critically short supply, across Europe. The shortage of skilled personnel proficient in advanced simulation techniques is additionally to further degrade the growth of the Europe simulation software market. Germany’s Federal Institute for Vocational Education noted that fewer than 15% of technical universities offer dedicated simulation engineering curricula despite industry demand. This gap forces companies to rely on expensive external consultants or vendor support teams, increasing dependency and slowing innovation cycles.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Simulation Acceleration and Surrogate Modeling

The fusion of artificial intelligence with simulation software is unlocking unprecedented speed and scalability by replacing computationally intensive solvers with AI-trained surrogate models. The integration of artificial intelligence for simulation and surrogate modelling is expected to bolster the growth of the Europe simulation software market. According to the Technical University of Munich, AI-enhanced simulation reduced computational time for crash test modeling by 90% while maintaining 98% accuracy in 2023 trials. In aerospace, Thales uses neural networks to predict electromagnetic interference in satellite systems, cutting simulation cycles from weeks to hours. The European High Performance Computing Joint Undertaking has allocated 120 million euros through 2027 to develop AI simulation co-design platforms under its EuroHPC LEMUR project. Additionally, the EU AI Act provides a clear regulatory framework for trustworthy AI in engineering applications by encouraging adoption in safety-critical domains.

Expansion into Sustainable Product Design and Lifecycle Assessment

Simulation software is emerging as a key enabler of the European Green Deal by allowing engineers to virtually assess environmental impact across a product’s lifecycle. The EU’s Ecodesign for Sustainable Products Regulation mandates digital product passports from 2027, requiring granular environmental data simulation to provide the most accurate method to generate this information pre-production. Companies like Volvo and Siemens now require all new products to undergo virtual sustainability validation. This regulatory and strategic alignment positions simulation as indispensable for compliant and competitive sustainable innovation in Europe.

MARKET CHALLENGES

Interoperability Deficits Between Simulation Tools and Legacy PLM/ERP Systems

The operations in silos disconnected from product lifecycle management and enterprise resource planning systems that govern real-world production, which is a significant factor that is challenging the growth of the Europe simulation software market. According to some reports, only 35% of European manufacturers achieved full data integration between simulation outputs and manufacturing execution systems in 2023. When design changes occur in CAD platforms, simulation models frequently require manual rebuilds due to a lack of associative linking, a process that adds 5 to 10 days per iteration, as documented by Airbus.

Cybersecurity and Intellectual Property Risks in Cloud-Based Simulation Platforms

As simulation migrates to cloud environments, concerns over data security and proprietary model protection intensify in defense, aerospace, and automotive sectors, where designs are highly sensitive. The cybersecurity and intellectual property risks in cloud-based simulation platforms are another attribute hindering the growth of the Europe simulation software market. According to the European Union Agency for Cybersecurity, 42% of surveyed engineering firms in 2023 delayed cloud simulation adoption due to fears of IP leakage or unauthorized access. In 2023, a ransomware incident at a French automotive supplier compromised unencrypted simulation files, leading to design theft. The EU’s NIS2 Directive mandates enhanced cybersecurity for critical infrastructure but does not yet specify protections for engineering simulation data.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Deployment, Application, Industry, and County. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Autodesk Inc., ANSYS, Inc., Dassault Systèmes, Altair Engineering Inc., The AnyLogic Company, Siemens Digital Industries Software, Flex Ltd., Rockwell Automation, Inc., Bentley Systems, Inc., Simulations Plus, MathWorks, Inc., and Others. |

SEGMENTAL ANALYSIS

By Deployment Insights

The on-premises segment held a prominent share of the Europe simulation software market in 2025. Industries, such as aerospace defense and automotive, require absolute control over simulation data containing proprietary designs and trade secrets. According to the European Union Agency for Cybersecurity, defense and aerospace firms in the EU mandated on-premises simulation deployment in 2023 due to concerns over cloud data residency and third-party access. In Germany, the Federal Office for Information Security requires that all simulation models for critical infrastructure components be stored on sovereign infrastructure. Similarly, Airbus and Dassault Aviation maintain private high-performance computing clusters in Toulouse and Hamburg to safeguard aircraft design simulations. Many European engineering organizations have invested heavily in on-premises high-performance computing systems that are deeply integrated with existing CAD, PLM, and testing workflows.

The Cloud segment is projected to expand at a CAGR of 21.4% from 2025 to 2033. Cloud-based simulation removes the barrier of high upfront hardware investment, enabling small and medium enterprises to access enterprise-grade tools on a pay-per-use basis. According to the research survey, 53% of EU engineering SMEs adopted cloud simulation platforms in 2023, up from 29% in 2021, primarily through offerings from Ansys Cloud and SimScale. The European Innovation Council’s SME Fund now includes cloud simulation credits as eligible expenses, further lowering adoption barriers. Cloud platforms provide on-demand access to thousands of CPU and GPU cores essential for large-scale simulations such as full vehicle crash tests or climate modeling. According to the Technical University of Munich, researchers reduced simulation time for wind farm aerodynamics from 14 days to 8 hours by leveraging AWS ParallelCluster in 2023. The integration of AI training workloads with simulation data further drives cloud adoption as AI models require massive computational resources, only economically viable in cloud environments.

By Application Insights

The product engineering segment led the Europe simulation software market by occupying 58.3% of share in 2024. Regulatory bodies across Europe require extensive simulation validation before physical testing. Similarly, the European Aviation Safety Agency accepts simulation for up to 70% of structural certification under CS 25 Appendix O. These regulatory mandates transform simulation from optional to essential, creating consistent high-value demand across Europe’s engineering-intensive industries. Product engineering simulation is embedded in the digital thread connecting design, simulation, manufacturing, and service. The large EU manufacturers use simulation outputs to generate machine tool paths and inspection protocols directly.

The Research & Development segment is projected to expand at a CAGR of 19.8% from 2025 to 2033. The European Commission allocated 2.1 billion euros in 2023 to digital modeling and simulation under Horizon Europe’s Cluster 4, focusing on climate health and advanced materials. Projects like EuroHPC LEMUR develop exascale simulation platforms for fusion energy and drug discovery. Similarly, Germany’s DFG supported 120 university simulation initiatives ranging from biomechanics to sustainable concrete. These grants provide sustained demand for advanced simulation software in academic and public research institutions, driving segment growth beyond industrial applications.

By Industry Insights

The automotive segment was the largest by holding 32.3% of the Europe simulation software market share in 2024. EU vehicle homologation mandates extensive simulation for crash safety emissions and advanced driver assistance systems. New cars must pass 18 virtual crash scenarios before physical testing. Additionally, electric vehicles require thermal simulation of battery packs. Stellantis runs 5000+ thermal cycles virtually per model to ensure safety. These regulatory and technical demands make automotive the most intensive simulation user in Europe. Automakers compress development timelines to compete in the EV and autonomy race. Renault’s digital wind tunnel cuts aerodynamics validation from weeks to days. This speed imperative ensures continuous and expanding simulation investment across Europe’s automotive ecosystem.

The healthcare segment is likely to grow at an anticipated CAGR of 24.3% from 2025 to 2033. The European Medicines Agency now accepts simulation-based evidence for Class IIb and III medical devices under specific validation frameworks. According to the Medical Devices Coordination Group, 37 in silico trials were approved in 2023 for cardiovascular implants and orthopedic devices. Companies like Medtronic use ANSYS to simulate stent deployment in virtual arteries, reducing animal testing by 60%. Hospitals increasingly use simulation to plan complex surgeries based on individual patient anatomy.

COUNTRY LEVEL ANALYSIS

Germany Simulation Software Market Analysis

Germany was the top performer of the Europe simulation software market by occupying 25.3% of share in 2024, with its position as Europe’s engineering and manufacturing powerhouse. According to Research, over 200 million euros were allocated in 2023 to digital twin and simulation projects under the High Tech Strategy 2025. Companies like BMW, Siemens, and Bosch operate some of Europe’s most advanced simulation centers with private high-performance computing clusters. Germany’s dual education system also produces a steady stream of simulation-literate engineers, over 8000 graduates annually in computational mechanics, as per the German Academic Exchange Service.

France Simulation Software Market Analysis

France held second position by holding 18.3% of the Europe simulation software market share in 2024, with its strong aerospace defense and nuclear engineering sectors. According to the French Ministry of Higher Education, over 120 million euros were committed in 2023 to the national simulation initiative “Calcul Intensif” supporting both public research and industrial deployment. The CEA’s Military Applications Division operates Europe’s most powerful simulation supercomputer, Tera 1000, for defense applications. Additionally, France’s “France 2030” investment plan includes 500 million euros for digital twins in energy and transport.

United Kingdom Simulation Software Market Analysis

The United Kingdom simulation software market is likely to grow with excellence in automotive motorsport and life sciences simulation. According to the UK’s Engineering and Physical Sciences Research Council, 95 million pounds were awarded in 2023 to simulation-based projects in sustainable aviation and biomedical engineering. Universities like Imperial College and the University of Cambridge lead in computational fluid dynamics and multiscale modeling. Additionally, the NHS is piloting patient-specific simulation for surgical planning in partnership with Siemens Healthineers.

Italy Simulation Software Market Analysis

Italy simulation software market growth is likely to grow with its specialized manufacturing base in automotive, fashion machinery, and industrial design. Italian companies like Ferrari, Lamborghini, and Pirelli use simulation for aerodynamics, tire dynamics, and material stress testing. The Italian government’s National Recovery and Resilience Plan allocated 400 million euros to digital twin initiatives in manufacturing and cultural heritage using simulation to restore historical structures. Additionally, fashion houses like Prada employ simulation for sustainable material testing, reducing physical sampling.

COMPETITIVE LANDSCAPE

The Europe simulation software market features intense competition among global technology leaders, European industrial champions, and specialized engineering software firms vying for dominance in a highly regulated and innovation-driven environment. Competition is defined by technical accuracy, regulatory compliance, interoperability with existing PLM systems, and alignment with EU industrial policy rather than price alone. Incumbents like Dassault Systèmes, Siemens, and Ansys leverage deep domain expertise long long-standing customer relationships, and comprehensive platform integration to maintain leadership. Niche players differentiate through specialized solvers or open source frameworks, but face challenges in scaling. The market is further shaped by public funding through Horizon Europe and national recovery plans, which de-risk adoption and foster ecosystem collaboration.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe simulation software market include

- Autodesk Inc.

- ANSYS, Inc.

- Dassault Systemes

- Altair Engineering Inc.

- The AnyLogic Company

- Siemens Digital Industries Software

- Flex Ltd.

- Rockwell Automation, Inc.

- Bentley Systems, Inc.

- Simulations Plus

- MathWorks, Inc.

TOP PLAYERS IN THE MARKET

- Dassault Systèmes is a French multinational and a global leader in 3D design and simulation software with deep integration across the European automotive, aerospace, and healthcare sectors. The company’s 3DEXPERIENCE platform enables end-to-end virtual prototyping, digital twin deployment, and in silico clinical trials aligned with EU regulatory frameworks. In Europe, Dassault serves major clients including Airbus, BMW, and Siemens Healthineers with industry-specific simulation solutions. In 2023, the company expanded its cloud-based simulation offerings through partnerships with Microsoft Azure, enhancing accessibility for small and medium enterprises. This strategic alignment with EU policy priorities and industrial digitization sustains its technological leadership in the region.

- Siemens Digital Industries Software is a Germany-headquartered provider of integrated simulation and product lifecycle management solutions widely adopted across Europe’s advanced manufacturing base. Its NX and Simcenter portfolios are used by companies like Bosch, Volkswagen, and Siemens Energy for multiphysics simulation, digital twin implementation, and AI-enhanced predictive engineering. The company actively participates in EU-funded initiatives, including the Important Project of Common European Interest on digital twins, ensuring interoperability with European industrial standards.

- Ansys is a global simulation leader with a strong European presence serving high-performance engineering sectors, including automotive, defense electronics, and healthcare. The company’s physics-based solvers are embedded in the workflows of Airbus, Volvo, and ASML for applications ranging from electromagnetic compatibility to structural integrity. In Europe, Ansys has deepened its cloud strategy through the Ansys Cloud Direct platform, enabling scalable high-performance computing on Microsoft Azure and AWS. Ansys also collaborates with European universities and research institutions under Horizon Europe to advance exascale computing and digital twin validation.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe simulation software market focus on embedding simulation into end-to-end digital twin ecosystems that span design, manufacturing, and operational phases. They invest heavily in cloud and AI integration to enhance accessibility, scalability, and speed for both large enterprises and SMEs. Strategic alignment with EU regulatory frameworks such as the Medical Device Regulation and General Safety Regulation ensures software compliance by design. Companies actively participate in Horizon Europe and national innovation programs to co-develop next-generation simulation capabilities with public research institutions. Additionally, they offer industry-specific solution templates and sustainability modules to address sectoral challenges like lightweighting, electrification, and circular design. Partnerships with hyperscalers and system integrators further strengthen deployment support and market reach across diverse European industrial landscapes.

MARKET SEGMENTATION

This research report on the Europe simulation software market has been segmented and sub-segmented into the following categories.

By Deployment

- Cloud

- On-premises

By Application

- Product Engineering

- Research & Development

- Gamification

By Industry

- Automotive

- Manufacturing

- Electronics & Semiconductor

- Aerospace & Defense

- Healthcare

- Others (Education, Media & Entertainment)

By Country

- United Kingdom

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Rest of Europe

Frequently Asked Questions

1. What is the size of the Europe simulation software market?

The Europe simulation software market is valued at USD 5.05 billion in 2026, growing from USD 4.54 billion in 2025 due to industrial digitalization

2. What is the growth rate of the Europe simulation software market?

The Europe simulation software market grows at 11.34% CAGR from 2026 to 2036, reaching USD 11.94 billion by 2034.

3. Which countries lead the Europe simulation software market?

Germany and UK dominate Europe simulation software market with advanced manufacturing and R&D investments

4. What drives the Europe simulation software market?

The Europe simulation software market grows via Industry 4.0, AI adoption, and demand for virtual testing

5. What industries use the Europe simulation software market?

Automotive, aerospace, manufacturing lead Europe simulation software market applications

6. How does cloud affect the Europe simulation software market?

Cloud deployment boosts scalability in Europe simulation software market for SMEs and enterprises

7. Who are key players in Europe simulation software market?

Ansys, Dassault, Altair, and Autodesk lead Europe simulation software market innovations

8. How does manufacturing impact Europe simulation software market?

Process optimization drives the Europe simulation software market in manufacturing hubs like Germany

9. What role does AI play in Europe simulation software market?

AI integration enhances predictive modeling in Europe simulation software market

10. What challenges face Europe simulation software market?

High costs and skill gaps challenge adoption in Europe simulation software market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com