Europe Soil Treatment Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Technology, End User, and Country – Industry Forecast From 2026 to 2034

Europe Soil Treatment Market Report Summary

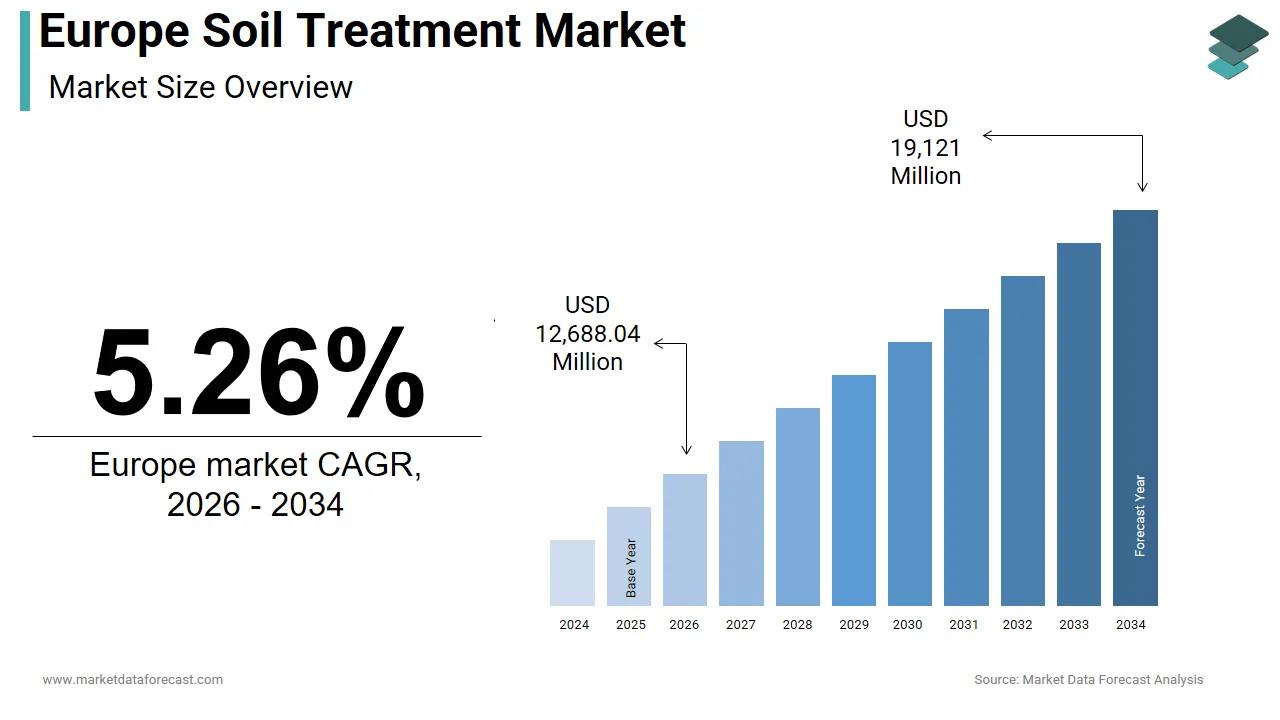

The Europe soil treatment market was valued at USD 12,054 million in 2025 and is projected to grow from USD 12,688.04 million in 2026 to USD 19,121 million by 2034, registering a CAGR of 5.26% from 2026 to 2034. Market growth is driven by increasing emphasis on sustainable agriculture, growing concerns over soil degradation, and stringent environmental regulations promoting soil restoration and conservation. Rising adoption of biological soil treatment technologies, organic soil amendments, and regenerative farming practices, along with increasing investments in contaminated land remediation, are further supporting market expansion.

Key Market Trends

- Increasing adoption of organic soil amendments and biological treatment solutions.

- Rising focus on soil health restoration and sustainable agricultural practices.

- Growing implementation of bioremediation and environmentally friendly soil treatment technologies.

- Expansion of precision agriculture and regenerative farming initiatives.

- Strengthening environmental regulations for soil contamination management and land remediation.

Segmental Insights

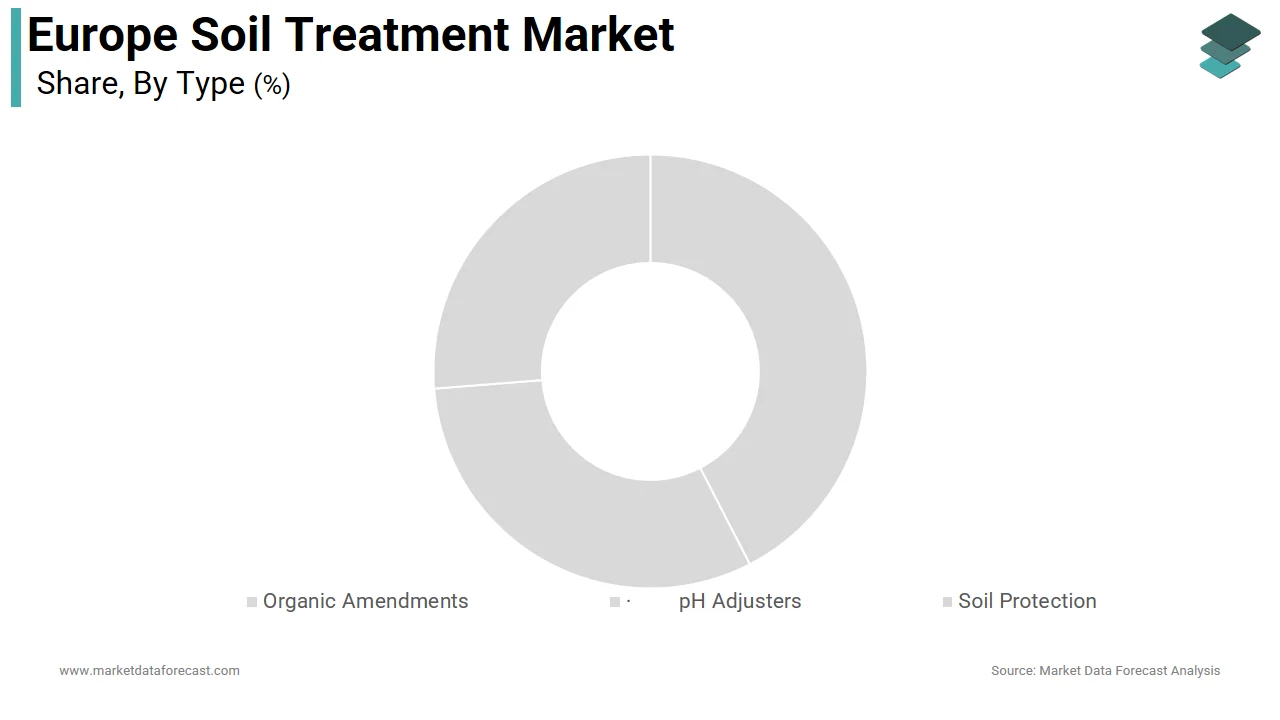

- Based on type, the organic amendments segment dominated the Europe soil treatment market by accounting for 40.3% market share in 2025, driven by increasing demand for sustainable soil enhancement products that improve fertility, organic matter content, and crop productivity.

- Based on technology, the biological treatment segment held the largest market share with 45.1% in 2025, supported by growing adoption of microbial treatments, bioremediation techniques, and environmentally sustainable soil restoration solutions.

- Based on end user, the agricultural segment accounted for 55.7% of the Europe soil treatment market in 2025, owing to the extensive area of arable land requiring continuous soil management, fertility improvement, and compliance with sustainable farming standards.

Regional Insights

The Europe soil treatment market continues to expand across major agricultural economies, supported by increasing environmental awareness, sustainable farming initiatives, and investments in soil restoration technologies.

- Germany dominated the European market by accounting for 22.2% share in 2025, driven by advanced agricultural practices, strong environmental regulations, and increasing adoption of sustainable soil management technologies.

- France held the second-largest position with 18.5% share in 2025, supported by its extensive agricultural sector, growing implementation of regenerative farming practices, and increasing investments in biological soil treatment solutions.

- Italy remains a significant contributor to the Europe soil treatment market, driven by the need to restore historically contaminated land, improve soil quality in intensive farming regions, and promote sustainable agricultural production.

Competitive Landscape

The Europe soil treatment market is highly competitive, with leading agricultural and environmental solution providers focusing on biological treatments, soil remediation technologies, and sustainable crop management products. Companies are investing in research and development, strategic partnerships, and innovative soil treatment formulations to strengthen their market presence. Continuous advancements in biological remediation, soil conditioners, and regenerative agriculture technologies continue to shape the competitive landscape.

Prominent companies operating in the Europe soil treatment market include AMVAC Chemical Corporation (American Vanguard Corporation), Arkema S.A., BASF SE, Veolia Environnement, Bayer AG, Compagnie de Saint-Gobain S.A., Corteva Inc., Novozymes A/S, Solvay S.A., Swaroop Agrochemical Industries, Syngenta Group (China National Chemical Corporation), Tata Chemicals Ltd., and UPL Limited.

Europe Soil Treatment Market Size

The Europe soil treatment market reached USD 12,054 million in 2025, is expected to grow to USD 12,688.04 million in 2026, and is anticipated to touch USD 19,121 million by 2034, at a CAGR of 5.26% from 2026 to 2034.

Soil treatment is the process of altering soil's physical, chemical, or biological properties to make it safe and productive. This market includes physical, chemical, and biological methods such as bioremediation, soil washing, thermal desorption, and the application of organic amendments or microbial inoculants. The market is driven by the urgent need to address legacy pollution from industrial activities and to combat soil degradation caused by intensive farming practices. According to the European Environment Agency (EEA), there are an estimated 2.8 million potentially contaminated sites in the EU, while health and environmental tracking via the World Health Organization (WHO) Europe confirms that roughly 300,000 of those sites are validated as contaminated and still require clean-up. Furthermore, as per the EU Soil Observatory dashboard published by the Joint Research Centre (JRC), a precise 61% of EU soils are recorded in an unhealthy state due to compounding degradation footprints like carbon reduction, erosion, and organic decline. The regulatory framework is anchored by the proposed Soil Monitoring Law, which aims to achieve healthy soils across the EU by 2050. This legislative push transforms soil treatment from an optional environmental service into a mandatory compliance requirement for landowners and industries. The market serves diverse end users, including real estate developers, municipal authorities, agricultural enterprises and industrial manufacturers who seek to unlock land value and ensure sustainable land use. Technological advancements are shifting focus toward nature-based solutions and circular economy principles where treated soil materials are reused rather than disposed of. This holistic approach integrates environmental protection with economic viability, ensuring long-term land productivity and ecosystem resilience.

MARKET DRIVERS

Stringent Regulatory Frameworks and the EU Soil Strategy For 2030

The implementation of stringent regulatory frameworks, particularly the EU Soil Strategy for 2030, drives the growth of the Europe soil treatment market. This strategy mandates that all member states identify and assess contaminated sites, establish national registers, and implement remediation measures for high-risk areas. According to the European Commission Soil Monitoring Law, the directive sets a long-term framework to achieve healthy EU soils by 2050 by establishing a strict monitoring structure for member states to track and assess soil health parameters. The proposed Soil Monitoring Law requires regular testing of soil health indicators, forcing agricultural and industrial entities to adopt proactive treatment measures. Non-compliance results in substantial fines and restrictions on land use, which drives demand for professional remediation services. National governments are transposing these EU directives into local laws, with countries like Germany and France introducing stricter limits on heavy metals and pesticide residues in soil. The definition of healthy soil now includes specific thresholds for biodiversity and organic matter content, which necessitates active management and treatment. Public procurement policies increasingly favor projects that demonstrate soil restoration credentials, further stimulating market activity. The clarity provided by these regulations reduces uncertainty for investors and encourages long-term planning for soil health initiatives. This regulatory pressure transforms soil treatment from a reactive cost centre into a strategic compliance necessity for businesses operating in Europe.

Urban Redevelopment and Brownfield Regeneration Projects

The acceleration of urban redevelopment and brownfield regeneration projects significantly fuels the demand for advanced soil treatment technologies in the region, which in turn propels the expansion of the European market. As cities expand and infrastructure projects require new land availability, greenfield sites diminish, forcing developers to utilize previously industrial or contaminated lands. As per the European spatial network CABERNET via ResearchGate, brownfield land accumulation poses significant urban redevelopment challenges across Europe, varying heavily from roughly 11,000 hectares in the Netherlands to upwards of 900,000 hectares in countries like Romania. Urban planning policies in major metropolitan areas such as London, Paris and Berlin prioritize the reuse of inner-city land to prevent urban sprawl and preserve natural habitats. Soil treatment enables the safe conversion of these contaminated sites into residential, commercial or recreational spaces by removing or neutralising pollutants like hydrocarbons, heavy metals and asbestos. The economic value of regenerated land often exceeds the cost of remediation, making it a financially viable option for developers. Government incentives and grants for brownfield redevelopment further encourage investment in soil cleaning technologies. The integration of soil treatment into early-stage project planning ensures timely delivery and compliance with safety standards. This trend is particularly strong in Western Europe, where land scarcity is acute and environmental standards are high. The ability to treat soil in situ reduces transportation costs and carbon emissions, aligning with sustainable construction goals. This urban transformation dynamic sustains robust demand for efficient and effective soil remediation solutions.

MARKET RESTRAINTS

High Operational Costs and Financial Burden on Stakeholders

The high operational costs associated with advanced soil treatment technologies are a significant restraint to the growth of the European market. This trend is particularly true for small- and medium-sized enterprises. Remediation processes such as thermal desorption, chemical oxidation and extensive bioremediation require specialised equipment, skilled labour and prolonged monitoring periods, which drive up expenses. According to ScienceDirect, the total expenditures required to completely clean up heavily compromised industrial properties routinely scale past 1 million euros due to site complexity, chemical depths, and specialized technology requirements. These costs are often borne by private landowners or developers who may lack the financial resources to undertake such investments without external support. The complexity of contamination involving multiple pollutants requires customised treatment plans, which are more expensive than standardized solutions. Budget constraints in public sector projects also limit the scope and speed of remediation efforts, leading to delays in land redevelopment. Economic uncertainty and rising energy prices further exacerbate operational costs, making some treatment methods less viable. Small farmers facing soil degradation often cannot afford premium biological treatments or precision amendments despite their long-term benefits. The lack of affordable financing options for soil health improvements restricts widespread adoption among smaller stakeholders. This financial barrier slows down the pace of remediation and limits the market potential for cost-effective but still expensive technologies. Many sites remain untreated without substantial subsidies or cost reductions. Consequently, they pose ongoing environmental risks.

Technical Complexity and Site-Specific Variability

The technical complexity of soil treatment and the high variability of site conditions are significant barriers to standardisation and efficiency, which slows down the expansion of the Europe soil treatment market. Each contaminated site presents unique characteristics regarding soil type, pollutant concentration, depth of contamination, and hydrogeological conditions, which require tailored treatment approaches. According to the Joint Research Centre of the European Commission, there is no one-size-fits-all solution for soil remediation, necessitating extensive site characterisation and pilot testing before full-scale implementation. This customisation increases the time and expertise required for each project, limiting the scalability of treatment providers. The presence of mixed contaminants such as heavy metals combined with organic compounds complicates the selection of effective treatment methods, as some techniques may address one pollutant while exacerbating another. Inconsistent regulatory interpretations across different member states add layers of administrative complexity, requiring separate approvals and compliance strategies for cross-border projects. The lack of standardized protocols for certain emerging contaminants like microplastics and pharmaceutical residues creates uncertainty in treatment efficacy. Skilled professionals capable of designing and managing complex remediation projects are in short supply, leading to bottlenecks in service delivery. The unpredictability of subsurface conditions can lead to unexpected complications during treatment, increasing costs and timelines. These technical hurdles discourage entry of new players and limit the rapid deployment of innovative solutions across diverse European landscapes.

MARKET OPPORTUNITIES

Adoption Of Bioremediation And Nature-Based Solutions

The growing adoption of bioremediation and nature-based solutions offers a significant opportunity for innovation and expansion in the Europe soil treatment market. Bioremediation utilises micro-organisms, plants and enzymes to degrade or immobilise contaminants, offering an eco-friendly and cost-effective alternative to traditional physical and chemical methods. According to the Bio-based Industries Consortium, the European landscape for environmental biotechnology is projected to grow annually, driven by demand for sustainable remediation techniques. Plants such as willows and poplars are used in phytoremediation to extract heavy metals from soil while specific bacteria break down hydrocarbons and pesticides. These methods minimise soil disturbance, preserve soil structure and enhance biodiversity, aligning with the EU Biodiversity Strategy. Government funding for green technologies supports research and development of enhanced microbial consortia and genetically modified organisms for targeted cleanup. The application of biochar and compost as soil amendments not only treats contamination but also improves soil fertility and carbon sequestration. Farmers and landowners increasingly prefer these gentle methods that allow continued land use during treatment. The integration of bioremediation into landscape design and urban green spaces creates multifunctional benefits. This shift toward biological processes transforms soil treatment from an industrial intervention into a regenerative ecological practice, opening new revenue streams for specialized providers.

Integration of Digital Technologies and Precision Soil Management

The integration of digital technologies and precision soil management tools paves the way for enhancing the efficiency and accuracy of soil treatment operations, which is likely to promote the expansion of the European market. Advanced sensors, drones, and satellite imagery enable real-time mapping of soil contamination levels, moisture content, and nutrient status, allowing for targeted application of treatment agents. According to CEMA European Agricultural Machinery, the integration of digital data management, sensor tools, and precision mapping serves as a structural pillar for smart, sustainable European land and soil management. Artificial intelligence algorithms analyse data from soil samples to predict contamination spread and recommend optimal treatment strategies, reducing trial and error. Blockchain technology facilitates transparent tracking of soil quality improvements and compliance with regulatory standards, providing verifiable data for stakeholders. Digital platforms connect landowners with remediation experts and suppliers, streamlining the procurement and management process. Precision application equipment ensures that treatments are delivered exactly where needed, minimising waste and environmental impact. The data generated supports long-term soil health monitoring, enabling proactive management rather than reactive cleanup. This technological convergence appeals to tech-savvy investors and regulators who value transparency and efficiency. It creates opportunities for software developers and data analysts to enter the soil treatment market alongside traditional engineering firms.

MARKET CHALLENGES

Long Duration Of Remediation Processes And Project Delays

The extended duration of many soil remediation processes is a significant challenge to project timelines and financial viability in the Europe soil treatment market. Biological and natural attenuation methods can take years or even decades to achieve desired cleanup levels, delaying land redevelopment and generating ongoing maintenance costs. As per the European Environment Agency (EEA), the administrative, diagnostic, and technical lifecycle needed to safely manage and clear heavily contaminated real estate stretches across multiple years, impacting local investment timelines. Prolonged timelines increase exposure to regulatory changes, liability risks, and fluctuating market conditions, which can render projects economically unviable. Stakeholders often face pressure to deliver results quickly, leading to conflicts between speed and thoroughness in treatment execution. Weather dependencies further complicate outdoor remediation activities, causing seasonal interruptions and schedule slippage. The lack of rapid testing methods for certain contaminants means that verification of cleanup success is slow and cumbersome. Delays in obtaining permits and approvals from multiple regulatory bodies add to the overall project duration. Community opposition to long-term construction or treatment activities can also cause stoppages and legal challenges. These temporal challenges require robust project management and contingency planning, which increase operational overheads. The inability to guarantee quick results discourages some landowners from initiating necessary treatment, leading to prolonged environmental hazards.

Public Perception And Community Opposition To Treatment Methods

Public perception and community opposition to certain soil treatment methods are persistent hurdles for operators in the Europe soil treatment market. Residents living near contaminated sites often express concerns about health risks associated with excavation, transport and treatment of polluted soil, particularly when chemical or thermal methods are used. According to the World Health Organization (WHO) Europe, the presence of unmitigated industrially contaminated sites poses severe public health anxieties, prompting local communities to closely scrutinise remediation safety profiles and long-term local impacts. Protests and legal actions can halt projects indefinitely, forcing companies to engage in costly public consultation and mitigation efforts. The stigma associated with contaminated land affects property values and community morale, creating social resistance to redevelopment plans. Misinformation about the effectiveness and safety of treatment technologies fuels fear and skepticism among the public. Noise, dust and traffic generated during remediation works disrupt daily life, leading to complaints and regulatory scrutiny. Companies must invest heavily in community engagement and transparent communication to build trust and secure social licence to operate. The requirement for extensive environmental impact assessments adds time and cost to project initiation. Failure to address community concerns adequately can result in reputational damage and loss of future business opportunities. This social dimension adds a layer of complexity beyond technical and regulatory challenges, requiring soft skills and strategic diplomacy.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Technology, End User, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | AMVAC Chemical Corporation (American Vanguard Corporation), Arkema S.A., BASF SE, Veolia Environnement, Bayer AG, Compagnie de Saint-Gobain S.A., Corteva Inc., Novozymes A/S, Solvay S.A., Swaroop Agrochemical Industries, Syngenta Group (China National Chemical Corporation), Tata Chemicals Ltd., UPL Limited, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The organic amendments segment dominated the Europe soil treatment market and accounted for a 40.3% share in 2025. This dominance of the segment was driven by the widespread depletion of soil organic carbon across European agricultural lands, which necessitates regular replenishment to maintain fertility and structure. As per the Joint Research Centre (JRC), over 60% of all EU soils are classified as structurally unhealthy due to compounding issues like organic carbon depletion, erosion, and biodiversity loss. Organic amendments such as compost manure and biochar improve water retention, nutrient availability, and microbial activity, which are critical for sustainable crop production. The EU Farm to Fork Strategy mandates a significant increase in organic farming area, which directly boosts demand for certified organic inputs that enhance soil biology without synthetic chemicals. Farmers increasingly recognize the long-term economic benefits of healthy soils, including reduced fertilizer dependency and improved resilience to climate stress. Government subsidies under the Common Agricultural Policy specifically support practices that increase soil organic carbon, providing financial incentives for amendment application. The circular economy model encourages the recycling of urban and agricultural waste into valuable soil treatments, reducing disposal costs and environmental impact. This alignment with regulatory agronomic and environmental goals secures the dominant market share of organic amendments.

On the other hand, the soil protection segment is expected to exhibit a noteworthy CAGR of 8.2% from 2026 to 2034 due to increasing awareness of soil erosion risks and stringent regulations mandating protective measures in vulnerable areas. According to Eurostat, soil erosion by water is a major driver of land degradation that affects more than 12% of European agricultural land, generating massive annual economic strains in lost productivity. Climate change-induced extreme weather events such as heavy rainfall and droughts exacerbate erosion risks, prompting farmers and land managers to invest in protective treatments. These include mulch films, cover crops and geotextiles that stabilise the soil surface and reduce runoff. The EU Soil Strategy for 2030 sets specific targets for reducing erosion rates, which drives adoption of preventive technologies. Construction projects also require extensive soil protection measures to comply with environmental permits and prevent sediment pollution in water bodies. Innovations in biodegradable erosion control mats and hydroseeding techniques offer effective and eco-friendly solutions. The integration of soil protection into landscape planning and infrastructure development creates new revenue streams. This regulatory and climatic pressure fuels the robust growth of the soil protection segment.

By Technology Insights

The biological treatment segment led the Europe soil treatment market and captured a 45.1% share in 2025. This leading position of the segment was attributed to its cost-effectiveness and environmental compatibility compared to traditional physical or chemical methods. Biological treatments utilise micro-organisms, plants or enzymes to degrade contaminants such as hydrocarbons, pesticides and heavy metals into harmless substances. According to ResearchGate, biological remediation offers a low-impact, clean technology pathway that significantly undercuts the intensive financial infrastructure required by standard civil excavation or thermal destruction methods. The technology aligns with the EU Green Deal objectives by minimising energy consumption and carbon emissions during the remediation process. It preserves soil structure and biodiversity, allowing for immediate reuse of treated land for agriculture or recreation. Advances in microbial engineering have enhanced the efficacy and speed of biological processes, addressing previous limitations regarding treatment duration. Public acceptance of nature-based solutions is high, reducing community opposition and regulatory hurdles. Government funding for green technologies supports research and deployment of advanced biological systems. The versatility of biological treatment across various contaminant types and soil conditions ensures broad applicability. This combination of economic and ecological advantages secures the dominant position of biological treatment.

However, the thermal treatment segment is predicted to witness the highest CAGR of 7.5% during the forecast period owing to the urgent need for rapid remediation of heavily contaminated industrial sites where time is a critical factor for redevelopment. Thermal technologies such as incineration and thermal desorption effectively destroy persistent organic pollutants and volatilise heavy metals, achieving high cleanup standards in short durations. As per the Joint Research Centre (JRC) Bureau, properly deployed thermal infrastructure provides rapid, highly effective destruction of toxic chemical chains, ensuring it is a preferred path for high-risk waste volumes. The increasing value of inner-city land drives developers to choose faster, albeit more expensive, methods to accelerate project timelines. Technological advancements have improved energy efficiency and emission control systems, addressing previous environmental concerns associated with thermal processes. Strict regulations on hazardous waste disposal limit landfill options, forcing greater reliance on destruction technologies. The ability to treat soil in situ or ex situ provides flexibility for complex site conditions. Investment in mobile thermal units enhances accessibility for remote or constrained sites. This demand for speed and thoroughness drives the rapid expansion of the thermal treatment segment.

By End User Insights

In 2025, the agricultural segment held the majority share of 55.7% of the Europe soil treatment market because of the vast area of arable land requiring continuous management to maintain productivity and comply with sustainability standards. Farmers extensively use organic amendments, pH adjusters, and biological treatments to combat soil degradation and enhance crop yields. According to the Food and Agriculture Organization of the United Nations, sustainable soil management is critical for food security, driving adoption of treatment practices across the continent. The transition toward precision agriculture enables targeted application of treatments, optimising resource use and minimising environmental impact. Government policies under the Common Agricultural Policy link subsidies to soil health indicators, encouraging widespread adoption of treatment technologies. The rise of organic farming, which prohibits synthetic inputs, increases demand for natural soil treatments such as compost and bio-fertilisers. Climate change adaptation strategies require resilient soils capable of retaining water and nutrients, further boosting treatment usage. The economic imperative to protect long-term land value ensures consistent investment in soil health. This foundational role of agriculture in the European economy sustains its leadership in the soil treatment market.

But the construction segment is estimated to register the fastest CAGR of 9.1% between 2026 and 2034. This rapid growth of the segment is fuelled by extensive urban redevelopment and brownfield regeneration projects that require remediation of contaminated land before building. As greenfield sites become scarce, cities increasingly rely on previously industrial lands for housing and infrastructure development. According to ResearchGate's CABERNET profile, the sheer scale of legacy industrial brownfields varies wildly between member states, creating a structural need for remediation before municipal redevelopment can occur. Construction companies must comply with strict environmental regulations regarding soil quality and contamination levels, driving demand for professional remediation services. The integration of soil treatment into early-stage project planning ensures timely delivery and cost control. Green building certifications such as BREEAM and LEED incentivize sustainable land management practices, including soil restoration. The high economic value of regenerated urban land justifies investment in advanced treatment technologies. Public-private partnerships for infrastructure projects often include soil remediation components, creating steady demand. This urban transformation dynamic drives the robust expansion of the construction end-user segment.

COUNTRY-LEVEL ANALYSIS

Germany Soil Treatment Market Analysis

Germany was the top performer in the Europe soil treatment market and accounted for a 22.2% share in 2025. The country benefits from a legacy of industrial activity requiring extensive remediation of contaminated sites, particularly in former East Germany. According to the German Federal Ministry for the Environment (BMUV), the country’s Federal Soil Protection Act establishes legal mandates for site investigation, risk evaluation, and decontamination parameters, explicitly driving commercial market reliance on advanced bioremediation and physical treatment technologies. German engineering firms are global leaders in developing innovative thermal and biological remediation systems. The strong focus on renewable energy and circular economy principles promotes the use of bio-based soil treatments in agriculture. Government funding supports research into sustainable soil management practices, enhancing technological capabilities. High public awareness of environmental issues ensures strict enforcement of regulations and community engagement in remediation projects. The presence of major chemical and industrial companies creates a steady pipeline of contaminated sites requiring professional treatment. Germany's central location facilitates the export of expertise and technology to neighbouring countries. This combination of regulatory rigour, technical innovation and industrial demand sustains its leadership position.

France Soil Treatment Market Analysis

France was the next prominent country in the Europe soil treatment market and captured an 18.5% share in 2025. The diverse agricultural sector drives demand for organic amendments and biological treatments to maintain soil health and comply with agro-Environmental standards. France has launched ambitious brownfield regeneration programs to revitalise industrial zones and expand urban housing stock. As per the United Nations Environment Programme (UNEP), France's National Biodiversity Strategy and Action Plan structures public spending and local conservation priorities around halting soil artificialisation and financing the active restoration of natural ecosystems. French companies specialise in phytoremediation and biological solutions, leveraging the country's strong research base in ecology. Government subsidies for organic farming boost adoption of natural soil treatments among growers. The prevalence of vineyards and speciality crops requires precise soil management to ensure quality and authenticity. Local authorities actively promote soil sealing reduction and permeable surface restoration in urban planning. Collaborative platforms connect stakeholders to share best practices and innovations in soil treatment. This balanced approach between agricultural sustainability and urban redevelopment ensures steady market growth.

Italy Soil Treatment Market Analysis

Italy plays a major role in the European soil treatment market, which is driven by urgent restoration needs related to historical contamination and intensive farming. The country faces challenges from industrial pollution in northern regions and soil erosion in southern agricultural areas. Italian farmers increasingly adopt organic amendments to restore fertility in degraded soils, supporting the renowned food and wine sectors. According to the Organisation for Economic Co-operation and Development (OECD), Italy's National Recovery and Resilience Plan (PNRR) targets a multi-billion euro budget toward supporting the ecological transition, specifically allocating dedicated investments for soil protection, green infrastructure, and sustainable agricultural remediation. The presence of numerous small- and medium-sized farms favours cost-effective and accessible treatment solutions. Research institutions focus on developing region-specific remedies for local soil types and contaminants. The tourism industry drives demand for landscape restoration and soil stabilisation in coastal and rural areas. Strict EU compliance requirements push industries to invest in advanced remediation technologies. The cultural emphasis on land stewardship encourages adoption of sustainable practices. This unique mix of agricultural heritage and industrial legacy creates a dynamic market for diverse soil treatment solutions.

Spain Soil Treatment Market Analysis

Spain grew steadily in the Europe soil treatment market due to its urgent need for erosion control and water management. Severe soil erosion affects large parts of the country, driven by climate change and intensive agriculture. Farmers and land managers invest heavily in soil protection technologies such as cover crops and mulching to retain moisture and prevent loss. The arid climate necessitates treatments that improve the water infiltration and retention capacity of soils. Government programs support sustainable land management practices to combat desertification risks. The expansion of organic farming in regions like Andalusia drives demand for certified organic soil amendments. Urban development in coastal areas requires remediation of contaminated lands for tourism infrastructure. Spanish companies innovate in dryland agriculture techniques and biological treatments suited for hot climates. EU funding for climate adaptation projects boosts investment in resilient soil solutions. This environmental urgency drives steady growth in the soil treatment market.

COMPETITIVE LANDSCAPE

The competition in the Europe soil treatment market is characterized by intense rivalry among multinational environmental service providers, specialized chemical manufacturers, and regional remediation firms who vie for dominance in a regulated sector. Major players leverage their technological expertise and financial resources to offer comprehensive solutions ranging from assessment to final restoration. The market sees significant activity in sustainability innovation, with companies striving to develop low-carbon and nature-based treatment methods. Price competition is moderate, but value-added services such as digital monitoring and regulatory compliance support play a crucial role in customer retention. Regulatory pressures regarding soil health and contamination drive continuous improvement in treatment efficacy and environmental safety. Local firms compete by offering customized solutions tailored to specific regional soil conditions and regulatory nuances. The shift toward circular economy principles creates opportunities for niche players to challenge incumbents with recycling and reuse technologies. Collaboration with research institutions fosters technological advancements that shape competitive dynamics. Supply chain reliability becomes a key competitive factor as disruptions impact material availability. This dynamic environment requires continuous adaptation and strategic investment to maintain leadership and profitability in the sector.

KEY MARKET PLAYERS

The leading companies operating in the Europe soil treatment market include:

- AMVAC Chemical Corporation (American Vanguard Corporation)

- Arkema S.A.

- BASF SE

- Veolia Environnement

- Bayer AG

- Compagnie de Saint-Gobain S.A.

- Corteva Inc.

- Novozymes A/S

- Solvay S.A.

- Swaroop Agrochemical Industries

- Syngenta Group (China National Chemical Corporation)

- Tata Chemicals Ltd.

- UPL Limited

TOP PLAYERS IN THE MARKET

- Veolia Environnement is a global leader in environmental services with a significant presence in the European soil treatment market through its advanced remediation technologies. The company specializes in biological and physicochemical treatments for contaminated industrial and urban sites, ensuring compliance with strict EU regulations. Recent actions include the expansion of its mobile thermal desorption units to address urgent brownfield regeneration projects across France and Germany. Veolia strengthens its market position by integrating digital monitoring tools that provide real-time data on soil quality and treatment progress. The company collaborates with municipal authorities to develop sustainable land management strategies that align with circular economy principles. Its commitment to innovation drives the development of low-carbon remediation solutions. These initiatives enhance operational efficiency and build trust among stakeholders seeking reliable and eco-friendly soil restoration services.

- Solvay SA contributes significantly to the Europe soil treatment market by providing specialized chemical solutions and additives for soil stabilization and remediation. The company offers a range of products including pH adjusters and organic amendments that improve soil structure and fertility for agricultural and construction applications. Recent initiatives involve the launch of bio-based soil conditioners derived from renewable resources to support sustainable farming practices. Solvay strengthens its position through strategic partnerships with agricultural cooperatives to promote precision soil management techniques. The company invests in research facilities dedicated to developing innovative materials that enhance nutrient retention and water efficiency. Its focus on sustainability aligns with the EU Green Deal objectives, driving adoption among environmentally conscious farmers. These efforts establish Solvay as a trusted provider of high-performance soil treatment solutions.

- BASF SE plays a pivotal role in the Europe soil treatment market by offering comprehensive agricultural solutions including biological treatments and soil health enhancers. The company leverages its extensive chemical expertise to develop effective microbial inoculants and organic amendments that restore soil biodiversity. Recent actions include the acquisition of a biotechnology firm specializing in soil microbiome analysis to enhance product efficacy. BASF strengthens its market position by launching digital platforms that provide farmers with customized soil treatment recommendations based on field data. The company actively engages in educational programs to raise awareness about the importance of soil health and sustainable practices. Its commitment to innovation ensures the development of safe and effective products that meet regulatory standards. This holistic approach supports long-term agricultural productivity and environmental stewardship across Europe.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe soil treatment market employ innovation strategies to develop sustainable and efficient remediation technologies that comply with stringent environmental regulations. Companies invest heavily in research and development to create bio-based solutions and digital tools that enhance treatment precision and reduce ecological impact. Strategic partnerships with governmental bodies and agricultural organizations facilitate the adoption of best practices and secure funding for large-scale projects. Expansion of service portfolios to include consulting and monitoring services adds value for clients seeking comprehensive soil management solutions. Compliance with EU directives drives continuous improvement in safety standards and operational transparency. Mergers and acquisitions allow companies to consolidate expertise and expand their geographic reach competitively. Customer-centric approaches focusing on education and technical support strengthen brand loyalty and market presence. These strategies collectively drive growth and competitiveness in the evolving European environmental sector.

MARKET SEGMENTATION

This Europe soil treatment market research report is segmented and sub-segmented into the following categories.

By Type

- Organic Amendments

- pH Adjusters

- Soil Protection

By Technology

- Biological Treatment

- Thermal Treatment

- Physiochemical Treatment

By End User

- Agricultural

- Construction

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe soil treatment market?

The Europe soil treatment market includes products and methods used to improve soil quality, fertility, and overall soil health across farms and other land uses.

How does the Europe soil treatment market work?

The Europe soil treatment market works by using amendments and treatments that restore soil balance, structure, and productivity for better land use.

What drives growth in the Europe soil treatment market?

The Europe soil treatment market grows from rising soil degradation concerns, sustainable farming demand, and stricter environmental rules.

Which treatment type leads the Europe soil treatment market?

Biological treatment leads the Europe soil treatment market, while physiochemical and thermal methods also support soil improvement.

Why are organic amendments important in the Europe soil treatment market?

Organic amendments are important in the Europe soil treatment market because they improve soil structure, nutrients, and microbial activity.

What role do pH adjusters play in the Europe soil treatment market?

pH adjusters support the Europe soil treatment market by correcting soil acidity or alkalinity for healthier crop growth.

How does soil remediation relate to the Europe soil treatment market?

Soil remediation relates closely to the Europe soil treatment market because both focus on cleaning, restoring, and protecting land.

What is the role of bioremediation in the Europe soil treatment market?

Bioremediation supports the Europe soil treatment market by using natural biological processes to improve soil quality and safety.

Which end use drives the Europe soil treatment market?

Agriculture drives the Europe soil treatment market most, with added demand from construction, land reclamation, and contaminated site use.

What trends shape the Europe soil treatment market?

The Europe soil treatment market is shaped by precision agriculture, smart farming, and innovative soil amendment products.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com