Europe Sugar Substitutes Market Research Report Segmented By Origin (Natural and Synthetic), Composition (Stevia, Aspartame, Cyclamate, Sucrose, ACEK, Saccharin, D-Tagarose, Sorbitol, Maltitol, Xylitol), Application (Beverages, Food, Health & Personal Care, Pharmaceuticals, and Others), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Europe Sugar Substitutes Market Size

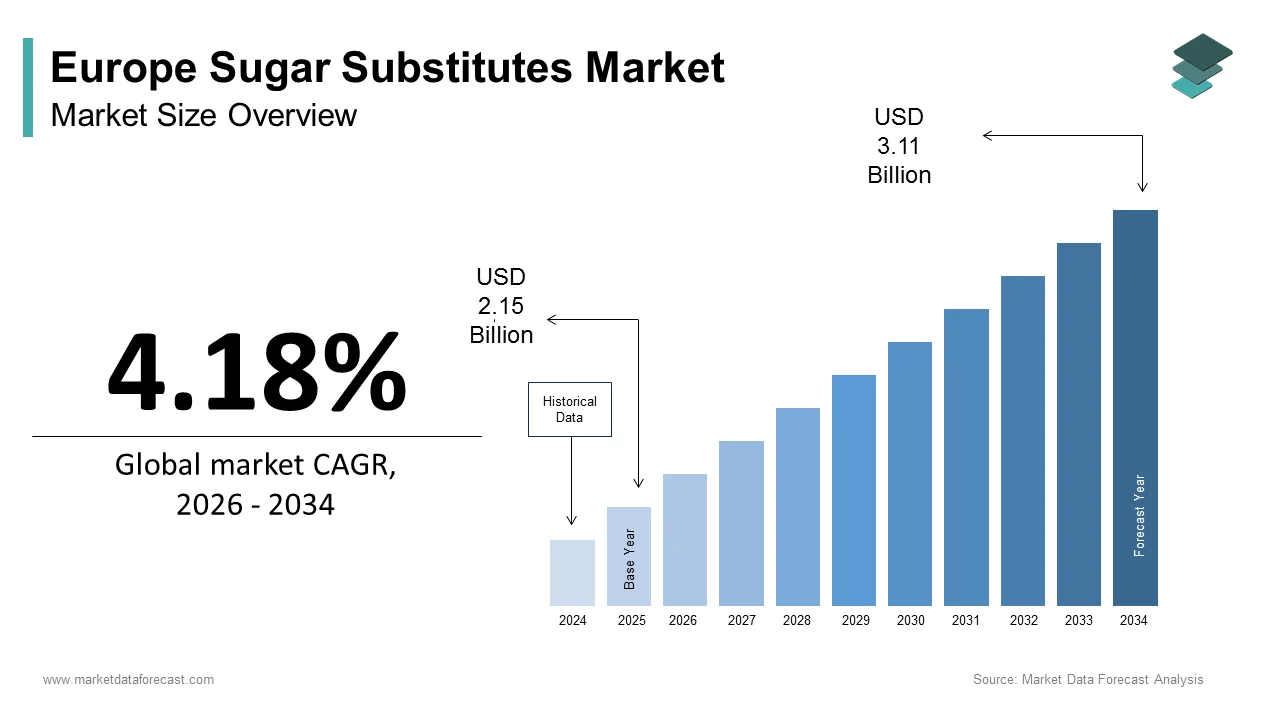

The size of the European sugar substitutes market was expected to be worth USD 2.15 billion in 2025 and is anticipated to be worth USD 3.11 billion by 2034, from USD 2.24 billion in 2026, growing at a CAGR of 4.18% during the forecast period.

Sugar substitutes encompass a diverse array of non-nutritive and low-calorie sweetening agents designed to replicate the sensory profile of sucrose without the associated metabolic burden. This sector includes high-intensity sweeteners like stevia and sucralose alongside bulk replacers such as erythritol and xylitol, which serve critical roles in reducing caloric density across food and beverage formulations. The strategic shift toward these alternatives stems from an urgent public health imperative to combat the rising prevalence of obesity and type 2 diabetes across the continent. As per the World Health Organization, adults in the European Region face significant challenges with overweight and obesity, which has created a demographic requiring dietary intervention. The European Food Safety Authority has rigorously evaluated numerous sweetening compounds to ensure their safety for human consumption, thereby establishing a robust regulatory foundation for their use. As per national health authorities in countries such as France and the United Kingdom, sugar taxes on soft drinks have been implemented, which incentivize manufacturers to reformulate products using these substitutes. The growing consumer awareness regarding the link between excessive sugar intake and chronic diseases further amplifies demand for cleaner label options. As the culinary industry seeks to maintain palatability while adhering to stricter nutritional guidelines, the integration of advanced sweetening blends becomes essential for product viability in modern retail environments.

MARKET DRIVERS

Escalating Prevalence of Diabetes and Obesity Drives Reformulation

The surging incidence of metabolic disorders serves as the primary catalyst for the widespread adoption of sugar substitutes across the European food and beverage landscape, which is majorly driving the growth of the European sugar substitutes market. Healthcare systems are under immense pressure to mitigate the long-term costs associated with treating type 2 diabetes and cardiovascular diseases linked to excessive sugar consumption. As per the International Diabetes Federation, diabetes prevalence in the European region is a growing concern, with projections indicating a significant rise without effective preventive measures. Governments have responded by implementing fiscal policies such as the Soft Drinks Industry Levy in the United Kingdom, which charges producers based on sugar content, thereby forcing a rapid shift toward alternative sweeteners. Major confectionery and beverage manufacturers have reformulated thousands of stock-keeping units to reduce sugar levels while maintaining taste profiles that satisfy consumer expectations. The medical community actively promotes the use of non-glycemic sweeteners for patients managing blood glucose levels, which validates their utility in therapeutic diets. Public health campaigns across Germany and Spain emphasize reading nutrition labels and choosing low-sugar options, which educates consumers and drives market pull. This dual pressure from regulatory bodies and health advocates creates an inelastic demand for sugar substitutes as they become indispensable tools for public health management and product compliance.

Stringent Government Regulations and Sugar Reduction Targets

The implementation of rigorous government mandates and voluntary reduction targets is further boosting the expansion of the European sugar substitutes market. The European Union has established comprehensive frameworks that encourage member states to adopt measures to reduce sugar intake among populations, particularly children. As per the European Commission, the EU Action Plan on Childhood Obesity calls for reformulation of processed foods to lower sugar content, which has led many nations to set specific reduction goals for various food categories. Countries like Portugal and Ireland have introduced levies on sugary beverages that make traditional sugar economically less viable compared to high-intensity sweeteners. These fiscal measures directly impact profit margins, prompting companies to switch to cost-effective and tax-exempt alternatives to remain competitive. The mandatory front-of-pack labeling schemes, such as NutriScore in France and Belgium, penalize high sugar products with poor ratings, which influences consumer purchasing behavior significantly. Manufacturers strive to achieve higher scores by replacing sugar with approved substitutes to maintain shelf visibility and brand reputation. The regulatory environment also ensures that only safe and thoroughly tested sweeteners enter the market, which builds consumer trust in these ingredients. This legislative landscape transforms sugar substitution from a marketing choice into a strategic necessity for market access and commercial survival.

MARKET RESTRAINTS

Persistent Consumer Skepticism Regarding Artificial Ingredients

The growing consumer preference for natural and clean-label products presents a significant restraint on the growth of synthetic sugar substitutes within the European market. Shoppers are increasingly scrutinizing ingredient lists and avoiding additives perceived as artificial or chemically derived, despite their regulatory approval and safety profiles. As per the European Consumer Organisation, consumers in Western Europe express hesitation toward consuming products containing aspartame or sucralose due to concerns about potential long term health effects. This skepticism forces manufacturers to limit the use of established high-intensity sweeteners in favor of more expensive natural alternatives, which can constrain market expansion for synthetic variants. The negative media coverage surrounding certain artificial sweeteners exacerbates public fear and leads to brand switching toward unsweetened or naturally sweetened options. Retailers respond to this sentiment by dedicating shelf space to products free from artificial additives, thereby marginalizing items that rely on synthetic sweeteners. The complexity of explaining the safety and origin of these ingredients to a wary public requires substantial marketing investment, which smaller brands often cannot afford. Until the perception of artificiality shifts or until natural alternatives become universally cost-effective, the resistance from health-conscious consumers will continue to dampen the uptake of specific sugar substitute categories.

Regulatory Hurdles and Lengthy Approval Processes for Novel Sweeteners

The complex and time-consuming regulatory approval process for novel sweetening ingredients is further hindering the sugar substitutes market growth in Europe. The European Food Safety Authority conducts exhaustive safety assessments for new substances, which can take several years before authorization for use in food and beverages is granted. As per the European Commission, the approval timeline for new food additives is lengthy, often exceeding several years, during which competitors in other regions may already be commercializing the ingredient. This delay discourages investment in research and development for next-generation sweeteners, as companies face uncertainty regarding return on investment. The stringent data requirements for toxicological studies and exposure assessments impose high financial burdens on applicants, particularly small and medium-sized enterprises. Once approved, the specific conditions of use and maximum permitted levels vary across different food categories, which complicates formulation strategies for manufacturers. The lack of harmonization in labeling requirements for certain natural sweeteners like steviol glycosides across member states further fragments the market and increases compliance costs. These regulatory bottlenecks slow the introduction of innovative tastes and functional benefits that could drive market growth. Consequently, the European market often lags behind North America and Asia in adopting new sweetening technologies, limiting the diversity of options available to formulators and consumers.

MARKET OPPORTUNITIES

Expansion of Plant-Based and Natural Sweetener Portfolios

The burgeoning demand for plant-derived and natural sweetening solutions offers a transformative opportunity for market players to capture the growing segment of clean-label conscious consumers. Ingredients such as stevia, monk fruit, and allulose are gaining traction as they align with the consumer desire for transparency and minimal processing in food products. As per the European Plant-Based Foods Association, sales of plant-based products have shown strong growth in recent years, reflecting a broader trend toward natural ingredients that extends to the sweetener category. Manufacturers are investing heavily in extraction and purification technologies to improve the taste profile of stevia by removing bitter notes and enhancing sweetness intensity. The development of enzymatic bioconversion processes allows for the production of rare sugars that offer unique functional properties and lower caloric content. Brands that successfully launch products sweetened exclusively with natural ingredients can command premium pricing and foster strong loyalty among health-oriented demographics. The versatility of these natural substitutes enables their application in a wide range of categories, from bakery goods to dairy alternatives, expanding the addressable market. Collaborative efforts between agricultural suppliers and food technologists are driving the scalability of crop cultivation for these sweeteners, ensuring stable supply chains. This shift toward nature-identical solutions positions companies at the forefront of the clean label movement and mitigates the reputational risks associated with artificial additives.

Innovation in Blending Technologies for Taste Optimization

The advancement of blending technologies presents a significant opportunity for the European sugar substitutes market. Single sweeteners often fail to replicate the full sensory experience of sugar, including mouthfeel, bulk, and caramelization, which limits their use in certain products. As per International Flavors and Fragrances Inc., research indicates that strategic combinations of high-intensity sweeteners with bulking agents and flavor modulators can achieve a sugar-like taste profile that satisfies discerning palates. Companies are developing proprietary blends that mask off notes such as metallic aftertastes commonly associated with stevia or saccharin. These customized solutions enable manufacturers to reduce sugar content in beverages and confectionery without compromising consumer acceptance. The ability to tailor blends for specific applications, such as acidic drinks or baked goods, allows for broader adoption across the food industry. Investment in sensory science and consumer testing drives the refinement of these formulations, ensuring they meet regional taste preferences across Europe. The emergence of smart sweetening systems that release sweetness at different stages of consumption further enhances the eating experience. By solving the taste challenge through innovation, providers can unlock new revenue streams and accelerate the displacement of traditional sugar in mainstream products.

MARKET CHALLENGES

Volatility in Raw Material Supply and Pricing

The instability of raw material supply chains and fluctuating pricing for key ingredients poses a critical challenge for the expansion of the Europe sugar substitutes market. Many natural sweeteners rely on crops such as stevia leaves or corn for erythritol, which are susceptible to weather conditions, pests, and geopolitical disruptions. As per the European Commission, agricultural producer prices have experienced volatility in recent years due to climate change impacts and energy cost increases affecting farming operations. Dependence on imports from non-European countries for certain raw materials exposes manufacturers to currency fluctuations and trade barriers that can abruptly raise production costs. The limited number of suppliers for high-purity extracts creates a concentrated market where supply shortages can lead to dramatic price spikes. Manufacturers struggle to pass these increased costs onto consumers in a highly competitive retail environment, leading to margin compression. The logistical challenges of transporting perishable botanical materials further complicate inventory management and quality control. Diversifying sourcing strategies requires long-term contracts and investment in local cultivation, which takes time to yield results. Until supply chains become more resilient and localized, the industry remains vulnerable to external shocks that threaten product availability and price stability.

Technical Limitations in Functional Performance

The inherent technical limitations of sugar substitutes in replicating the multifunctional roles of sucrose present a persistent challenge for the European sugar substitutes market. Sugar provides more than just sweetness; it contributes to texture, volume, browning, and preservation in many food applications, which substitutes often fail to mimic effectively. As per Campden BRI, replacing sugar in baked goods can result in products with poor crumb structure, reduced moisture retention, and inadequate shelf life. The lack of bulk in high-intensity sweeteners necessitates the addition of fillers, which can alter the nutritional profile and increase formulation complexity. In frozen desserts, sugar lowers the freezing point to ensure a smooth texture, whereas substitutes may lead to icy crystallization if not properly balanced. The Maillard reaction, responsible for browning in cookies and breads, does not occur with most non-nutritive sweeteners, affecting the visual appeal of finished products. Overcoming these functional gaps requires extensive research and the use of multiple ingredients, which increases development time and cost. The inability to achieve a perfect one-to-one replacement in all categories restricts the penetration of sugar substitutes in certain traditional food segments. Continuous innovation in ingredient technology is essential to bridge these performance gaps and enable wider adoption across diverse food categories.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.18% |

| Segments Covered | By Origin, Composition, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Cargill, Tate and Lyle, Ingredion Incorporated, Archer Daniels Midland Company, Ajinomoto Co., Inc., Roquette, PureCircle, NutraSweet Company, JK SucraloseInc. , and E. I. DuPont De Nemours |

SEGMENTAL ANALYSIS

By Origin Insights

The synthetic segment dominated the market by commanding the major share of the European sugar substitutes market by origin in 2025. The dominance of the synthetic segment in the European market is driven by its established presence, cost effectiveness, and high stability in various food processing conditions, and the extensive use of artificial sweeteners like aspartame and sucralose in the mass market beverage and confectionery industries, where low production costs are critical. As per the European Food Safety Authority, synthetic sweeteners have been rigorously tested and approved for decades, creating a high level of regulatory certainty that encourages widespread adoption by large-scale manufacturers. The intense sweetness potency of these compounds allows producers to achieve desired sweetness levels with minute quantities, significantly reducing formulation costs compared to bulkier natural alternatives. Major soft drink producers across Germany and the United Kingdom continue to rely heavily on synthetic blends to reformulate their flagship products to meet sugar tax requirements without compromising profit margins. The thermal stability of many synthetic agents makes them indispensable for baked goods and processed foods that undergo high-temperature treatments, where natural options might degrade. Furthermore, the long shelf life and consistent flavor profile of synthetic sweeteners ensure product uniformity across global supply chains, a factor highly valued by multinational food corporations. As long as price sensitivity remains a key driver for consumer goods, the economic advantages of synthetic origins will sustain their market leadership despite growing interest in natural alternatives.

The natural segment is a promising segment and is estimated to witness a CAGR of 10.5% over the forecast period in the European market. The growth of the natural segment in the European market is likely to be driven by the profound shift in consumer preference toward clean-label ingredients and plant-based solutions that are perceived as safer and healthier. The growing avoidance of artificial additives among health-conscious demographics is further boosting the expansion of the natural segment in the European market. As per the European Consumer Organisation, surveys highlight that European shoppers actively seek products with recognizable natural ingredients, prompting retailers to prioritize natural sweetener formulations. Innovations in extraction technologies have significantly improved the taste profile of stevia and monk fruit, removing bitter aftertastes that previously hindered their acceptance in premium applications. The rise of the free-from movement has led to a surge in demand for naturally derived sweeteners in the organic food sector. Government initiatives promoting sustainable agriculture also support the cultivation of crops like stevia within the EU, enhancing supply security and reducing reliance on imports. As major food brands launch new product lines marketed explicitly as naturally sweetened, the momentum for natural origin substitutes accelerates beyond traditional niche markets into mainstream consumption.

By Composition Insights

The aspartame segment held the dominant position in the Europe sugar substitutes market by holding the major share of the European sugar substitutes market in 2025. The growth of the spartame segment in this regional market is primarily due to its unparalleled ability to mimic the taste of sugar without the metallic aftertaste common in other high-intensity sweeteners. This leadership is sustained by its widespread integration into the diet soda and low-calorie beverage sectors. As per the International Council on Beverages Associations, aspartame remains the most widely used low-calorie sweetener globally. Its cost efficiency allows manufacturers to produce affordable diet products that remain accessible to a broad consumer base. The extensive regulatory history and repeated safety confirmations by the European Food Safety Authority provide a stable foundation for its continued use. Aspartame's synergy with other sweeteners enables formulators to create blends that optimize sweetness intensity and duration. The established supply chain and large-scale production capabilities ensure consistent availability and competitive pricing. While facing competition from natural options, its functional properties in acidic environments like carbonated drinks keep it as the preferred choice for many leading beverage brands.

The stevia segment is emerging as the fastest growing composition segment in the Europe sugar substitutes market and is estimated to witness a CAGR of 13.3% over the forecast period, owing to its plant-based origin and zero calorie profile, and its alignment with the clean label trend. As per the Global Stevia Institute, adoption of stevia in new product launches across Europe has increased significantly as brands respond to demand for transparency. Regulatory approvals for a wider range of steviol glycosides in the European Union have opened new avenues for innovation. The sustainability narrative surrounding stevia cultivation resonates strongly with environmentally conscious European buyers. Major confectionery companies are increasingly incorporating stevia into their flagship chocolate and gum lines. As research continues to unlock new flavor profiles and functional benefits, stevia is poised to displace traditional artificial sweeteners in an expanding array of food and beverage applications.

By Application Insights

The beverages segment led the market by capturing the largest share of the European sugar substitutes market in 2025. The urgent need for the soft drink industry to reduce sugar content in response to fiscal policies and health mandates, and the implementation of sugar taxes in countries like the United Kingdom, France, and Portugal, are driving the dominance of the beverages segment in the European market. As per the British Soft Drinks Association, reductions in sugar content have been achieved primarily through substitution with high-intensity sweeteners. The sheer volume of beverage consumption across Europe ensures that even small shifts in formulation result in massive demand for sweetening agents. Carbonated soft drinks, juices, and ready-to-drink teas rely heavily on sweeteners to maintain palatability while achieving zero or low-calorie claims. The competitive landscape of the beverage sector drives continuous innovation in sweetener blends. As hydration trends shift toward functional and enhanced waters, reliance on versatile sweeteners grows. The beverage industry's commitment to portfolio transformation ensures that this application segment remains the primary engine of consumption for sugar substitutes in the region.

The health and personal care segment is expected to experience the fastest CAGR of 11.6% over the forecast period, owing to the rising prevalence of oral care awareness and diabetic friendly personal products and the increasing incorporation of non-cariogenic sweeteners like xylitol and erythritol in toothpaste, mouthwashes, and chewing gums. As per the European Academy of Paediatric Dentistry, recommendations to use sugar-free oral care products have gained traction among parents and healthcare providers. The expansion of the nutraceutical sector has also contributed to this growth. The trend toward natural and organic personal care products aligns perfectly with the availability of plant-based sweeteners. Innovation in delivery systems, such as dissolvable strips and lozenges, further diversifies the application scope. As consumers become more educated about the link between sugar intake and skin or dental issues, the formulation of personal care items without sugar becomes a standard expectation, driving robust adoption of specialized sweeteners in this high-value category.

REGIONAL ANALYSIS

Germany Sugar Substitutes Market Analysis

Germany stood as the preeminent leader in the Europe sugar substitutes market by commanding 23.6% of the European market share in 2025 due to its robust food processing industry and stringent health regulations. The country’s position is reinforced by a highly developed manufacturing base that produces a vast array of low-calorie beverages, confectionery, and baked goods for domestic and export markets. As per the German Federal Ministry of Food and Agriculture, the nation has one of the highest levels of health consciousness in Europe, driving consumers to actively seek reduced sugar options in their daily diets. The strong presence of major sweetener producers and ingredient suppliers within Germany facilitates rapid innovation and efficient distribution of advanced sweetening solutions. German regulatory bodies strictly enforce labeling laws and nutritional standards, compelling manufacturers to adopt high-quality sweeteners to maintain compliance and consumer trust. The thriving organic food sector in Germany further amplifies the demand for natural sweeteners like stevia and erythritol, setting trends that influence neighbouring markets. Research institutions and universities in the country are at the forefront of studying the metabolic effects of different sweeteners, providing scientific backing for those that shape industry practices. This combination of industrial capacity, regulatory rigor, and informed consumerism ensures Germany remains the central hub for sugar substitute consumption and development in the region.

United Kingdom Sugar Substitutes Market Analysis

The United Kingdom had the second-largest share of the European sugar substitutes market in 2025. The promising position of the UK in the European market is attributed to its pioneering implementation of sugar taxation policies. The market status in the UK is characterized by a dramatic shift in product formulations following the introduction of the Soft Drinks Industry Levy, which served as a catalyst for widespread sweetener adoption across the beverage landscape. As per Public Health England, the levy successfully prompted many manufacturers to reduce the sugar content in their drinks, predominantly by switching to artificial and natural sweeteners. The high level of public awareness regarding obesity and diabetes in the UK creates a receptive environment for low-calorie alternatives, with retailers actively promoting sugar-free ranges. The vibrant startup ecosystem fosters innovation in natural sweetener technologies, with numerous companies developing novel extraction methods and blending strategies. Consumer advocacy groups play a significant role in holding brands accountable for sugar content, further accelerating the transition away from sucrose. The post Brexit regulatory environment allows the UK to potentially diverge from EU standards, offering opportunities for faster approval of new sweetening ingredients. These factors combine to make the UK a dynamic and influential market where policy and consumer behavior drive rapid evolution in sweetener usage.

France Sugar Substitutes Market Analysis

France is anticipated to showcase a promising CAGR in the European sugar substitutes market over the forecast period, owing to a blend of culinary tradition and growing health imperatives and a gradual but steady transition toward reduced sugar products as consumers reconcile their love for gastronomy with increasing awareness of metabolic health risks. As per Santé Publique France, national programs aimed at combating obesity have led to voluntary reformulation charters where major food companies commit to lowering sugar levels in processed foods. The French government supports the use of approved sweeteners to help achieve these public health goals while maintaining the sensory quality expected by discerning consumers. The popularity of tabletop sweeteners remains high in France, reflecting a cultural habit of adjusting sweetness in coffee and desserts without adding calories. The strong agricultural sector is exploring the cultivation of stevia and other natural sweeteners to reduce import dependency and support local farmers. Retailers in France are increasingly adopting NutriScore labeling, which incentivizes manufacturers to use sweeteners to improve the nutritional rating of their products. This balanced approach allows France to maintain its culinary identity while embracing necessary shifts toward healthier eating patterns through the strategic use of sugar substitutes.

Italy Sugar Substitutes Market Analysis

Italy represents a crucial and rapidly growing market within the Europe sugar substitutes market. The rising wellness trends, an aging population, and the high prevalence of diabetes and cardiovascular diseases in Italy, which drive medical recommendations for sugar reduction among a significant portion of the population, are contributing to the Italian market growth. As per the Italian National Institute of Statistics, the demand for dietetic and special medical purpose foods has surged, creating fertile ground for the adoption of various sweetening agents. The Italian confectionery and beverage industries, renowned globally, are increasingly integrating sweeteners to offer lighter versions of traditional products without compromising their iconic flavors. The Mediterranean diet evolution now includes a greater emphasis on limiting added sugars, encouraging households to switch to alternative sweeteners for home cooking and baking. Government initiatives promoting healthy lifestyles in schools and communities are raising awareness about the benefits of sugar-free options among younger generations. The growth of the organic and natural food sector in Italy also boosts demand for plant-based sweeteners that align with clean label preferences. As Italian consumers become more proactive about managing their health, the penetration of sugar substitutes in everyday food items is expected to accelerate significantly.

Spain Sugar Substitutes Market Analysis

Spain is projected to witness a healthy CAGR in the European sugar substitutes market over the forecast period due to the dynamic changes in consumer habits, aggressive marketing by food manufacturers, and a young and increasingly health-conscious demographic that is quick to adopt new food trends, including low sugar and keto-friendly products. As per the Spanish Agency for Food Safety and Nutrition, national surveys indicate a declining tolerance for high sugar content in snacks and beverages, prompting brands to reformulate extensively. The tourism industry in Spain exposes the market to international tastes and preferences, accelerating the introduction of global sugar-free brands and innovations. Local manufacturers are investing heavily in research to develop sweetener blends that suit the specific flavor profiles preferred by Spanish consumers, particularly in dairy and baked goods. The implementation of front-of-pack labeling and public health campaigns has heightened scrutiny on sugar content, pushing retailers to expand their sugar-free assortments. The warm climate in Spain also drives high consumption of cold beverages and ice creams, categories where sweeteners play a vital role in reducing caloric load. These converging factors position Spain as a vibrant market with substantial potential for future growth as the transition toward healthier diets gains momentum across the country.

COMPETITION OVERVIEW

The competition in the Europe sugar substitutes market is intense and characterized by a dynamic mix of global chemical giants and specialized natural ingredient providers vying for dominance. Major corporations leverage their vast resources to offer comprehensive portfolios that span both artificial and natural sweeteners, ensuring they can meet diverse customer needs. Smaller niche players differentiate themselves by focusing on organic certifications, unique extraction methods, or specific health benefits associated with their products. The landscape is rapidly evolving as consumer preferences shift decisively toward clean-label and plant-based options, forcing all participants to innovate continuously. Price competition remains fierce, particularly in the commodity sweetener segment, prompting vendors to emphasize value-added services like technical support and custom formulation. Regulatory compliance serves as a key battleground where providers compete to navigate complex approval processes and bring new ingredients to market faster. Strategic alliances between sweetener producers and end users are becoming essential to co-develop solutions that balance taste, cost, and health attributes. This highly competitive environment fosters relentless innovation and consolidation as firms strive to capture market share in a health-conscious region.

KEY MARKET PLAYERS

A few major players of the Europe sugar substitutes market include

- Cargill

- Tate and Lyle

- Ingredion Incorporated

- Archer Daniels Midland Company

- Ajinomoto Co., Inc

- Roquette

- PureCircle

- NutraSweet Company

- JK SucraloseInc

- E. I. DuPont De Nemours

Top Strategies Used by Key Market Participants

Key players in the Europe sugar substitutes market primarily focus on product innovation to develop natural sweeteners with improved taste profiles and functional properties. Companies frequently pursue strategic acquisitions of specialized ingredient firms to expand their portfolios and secure access to unique technologies. Investment in sustainable sourcing and regenerative agriculture helps firms meet growing consumer demand for eco-friendly products. Expanding production capacities within Europe ensures reliable supply chains and reduces dependency on imports. Collaborations with food and beverage manufacturers drive the creation of customized blending solutions that address specific application challenges. Marketing efforts emphasize health benefits and clean label credentials to differentiate products in a competitive landscape. These strategies collectively enable market participants to capture growth opportunities and maintain leadership positions in the evolving sweetener industry.

Leading Players in the Market

- Cargill Incorporated stands as a pivotal leader in the Europe sugar substitutes market by offering a comprehensive portfolio of natural and synthetic sweetening solutions. The company contributes significantly to the global market through its extensive supply chain and commitment to sustainable sourcing practices for ingredients like stevia and erythritol. Recent actions include the expansion of its stevia production capabilities to meet the surging demand for clean-label sweeteners across the European food and beverage sectors. Cargill actively collaborates with major manufacturers to develop customized blending solutions that optimize taste and functionality while reducing sugar content. The firm invests heavily in research and development to innovate next-generation sweeteners that address specific consumer health concerns. By focusing on vertical integration and strategic partnerships, Cargill strengthens its position as a reliable supplier capable of delivering high-quality ingredients at scale to diverse industries worldwide.

- Ingredion Incorporated plays a crucial role in the Europe sugar substitutes market by providing innovative plant-based sweetening ingredients and texturizing systems. The company leverages its global expertise to help formulators create delicious low-sugar products that appeal to health-conscious consumers. Recent initiatives involve the launch of new stevia varieties with improved taste profiles and reduced bitterness to facilitate broader adoption in premium applications. Ingredion has expanded its manufacturing footprint in Europe to ensure a consistent supply and reduce logistics costs for local clients. The firm prioritizes sustainability by working directly with farmers to implement regenerative agriculture practices for raw material sourcing. Collaborative efforts with customers drive the development of tailored solutions for beverages, confectionery, and dairy products. Through continuous innovation and a focus on customer success, Ingredion solidifies its reputation as a forward-thinking partner dedicated to advancing the future of sweetening.

- DuPont de Nemours Inc maintains a significant presence in the Europe sugar substitutes market through its advanced bioscience division, offering high-purity stevia and monk fruit extracts. The company contributes to the global market by utilizing proprietary fermentation technologies to produce rare steviol glycosides with superior sensory attributes. Recent actions include the introduction of novel enzyme-modified stevia products that deliver a sugar-like taste without off notes. DuPont actively engages in educational programs to inform manufacturers about the benefits and applications of natural high-intensity sweeteners. The firm has strengthened its distribution networks across Europe to ensure rapid delivery and technical support for clients. Investment in state-of-the-art research facilities enables the discovery of new sweetening compounds and functional blends. By combining scientific excellence with market insight, DuPont reinforces its status as a key innovator driving the transition toward healthier and more sustainable sweetening options globally.

MARKET SEGMENTATION

This research report on the Europe Sugar substitutes market has been segmented and sub-segmented based on origin, composition, application, & region.

By Origin

- Natural

- Synthetic

By Composition

- Stevia

- Aspartame

- Cyclamate

- Sucrose

- AceK

- Saccharin

- D-Tagarose

- Sorbitol

- Maltitol

- Xylitol

By Application

- Food

- Beverages

- Pharmaceutical

- Health And Personal Care

- Others

By Region

- United Kingdom

- Germany

- Spain

- France

- Denmark

- Italy

- Switzerland

- the Netherlands

- Russia

- Poland

- Belgium

- Turkey

- Sweden

- Others

Frequently Asked Questions

1. What factors are driving the growth of the Europe sugar substitutes market?

Growth is driven by increasing health consciousness, rising diabetes and obesity prevalence, government sugar reduction initiatives, and strong demand for low-calorie and low-glycemic food products.

2. What are the major types of sugar substitutes used in Europe?

The market includes artificial sweeteners (aspartame, sucralose, saccharin), natural sweeteners (stevia, monk fruit), and sugar alcohols (xylitol, sorbitol, erythritol).

3. What industries use sugar substitutes in Europe?

Key end-use industries include food & beverages (bakery, dairy, beverages), pharmaceuticals, nutraceuticals, and personal care products.

4. How is the rising diabetic population influencing the market?

The growing number of diabetic consumers is significantly increasing demand for low-calorie and sugar-free food and beverage products across Europe.

5. What role do government regulations play in the market?

European Union regulations promote sugar reduction strategies and strict labeling requirements, encouraging manufacturers to reformulate products using sugar substitutes.

6. What are the key challenges in the Europe sugar substitutes market?

Challenges include consumer concerns about artificial sweetener safety, taste differences compared to sugar, regulatory approvals, and price volatility of natural sweeteners.

7. What is the difference between artificial and natural sugar substitutes?

Artificial sweeteners are synthetically produced and offer high sweetness intensity with low calories, while natural substitutes are plant-derived and often perceived as healthier alternatives.

8. How is clean-label demand influencing the market?

Consumers prefer natural, plant-based sweeteners with minimal processing, leading to increased demand for stevia and other naturally derived sweeteners.

9. What distribution channels dominate the market?

Supermarkets and hypermarkets hold the largest share, followed by specialty health stores and rapidly expanding online retail platforms.

10. What are the future trends in the Europe sugar substitutes market?

Future trends include increasing adoption of plant-based sweeteners, expansion of functional foods, clean-label product launches, and growing demand for low-calorie beverages.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com