Global Knee Reconstruction Devices Market Size, Share, Trends & Growth Forecast Report By Product Type (Primary Cemented, Primary Cementless, Partial and Revision Implants) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

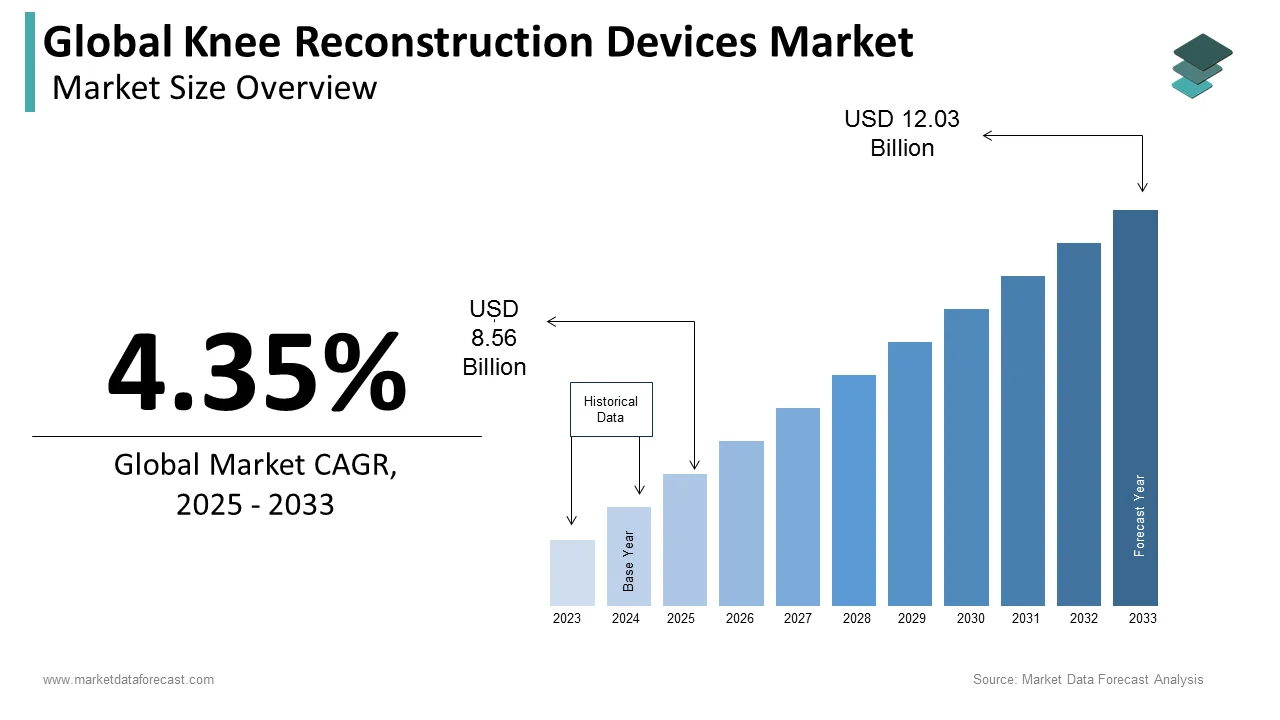

$8.56 BnMarket Estimate, 2026

$8.93 BnMarket Forecast, 2034

$12.56 BnCAGR, 2026–2034

4.35%Global Knee Reconstruction Devices Market Size

The size of the global knee reconstruction devices market was valued at USD 8.56 billion in 2025. This market is expected to grow at a CAGR of 4.35% from 2026 to 2034 and be worth USD 12.56 billion by 2034 from USD 8.93 billion in 2026.

The knee reconstruction devices market encompasses a range of orthopedic implants and surgical tools designed to restore joint functionality in patients suffering from knee injuries, osteoarthritis, or post-traumatic damage. These devices include anterior cruciate ligament (ACL) reconstruction systems, meniscus repair implants, patellar stabilization components, and custom graft fixation solutions. With advancements in biomaterials, minimally invasive surgical techniques, and patient-specific implant designs, knee reconstruction has become an integral part of musculoskeletal care.

According to the World Health Organization (WHO), musculoskeletal disorders affect over 1.7 billion people globally, with knee-related conditions accounting for a significant portion of orthopedic consultations and surgical interventions. As population’s age and physical activity levels rise, the demand for durable, biocompatible, and long-lasting knee reconstruction devices is increasing across both developed and emerging markets.

In parallel, sports medicine has evolved into a specialized field, particularly in North America and Europe, where professional athletes and active individuals frequently require reconstructive procedures following ligament tears or cartilage damage.

Besides, rising awareness about regenerative therapies and faster rehabilitation protocols has led to improved patient outcomes and shorter hospital stays. As per the American Academy of Orthopaedic Surgeons, approximately 400,000 ACL reconstructions are performed annually in the United States alone. This trend highlights the critical role of knee reconstruction devices in modern orthopedics, positioning the market as a key segment within the broader medical device industry.

MARKET DRIVERS

Rising Incidence of Sports-Related Knee Injuries

A primary driver of the knee reconstruction devices market is the growing prevalence of sports-related knee injuries, especially among younger and physically active populations. According to the National Institutes of Health (NIH), knee injuries account for more than 35% of all sports medicine consultations, with ACL tears being among the most common. Participation in high-impact sports such as soccer, basketball, skiing, and American football significantly increases the risk of ligament damage requiring surgical reconstruction.

As per the American Orthopaedic Society for Sports Medicine (AOSSM), approximately 200,000 ACL injuries occur annually in the U.S., with around 100,000 of these cases undergoing reconstructive surgery. This trend is not limited to the U.S.; countries like Germany, Brazil, and Japan have also reported rising numbers of sports-induced knee trauma, largely due to increased participation in competitive athletics and fitness culture.

Moreover, youth sports participation has surged globally, contributing to higher injury rates. As per the Journal of Athletic Training, the incidence of ACL injuries among adolescents aged 14–18 has increased by nearly 2.3% annually over the past decade. To address this demand, manufacturers are developing gender-specific and pediatric-sized implants tailored for younger patients.

Also, professional leagues and sports organizations are investing heavily in preventive training and early intervention programs, which indirectly boost the market by raising awareness and encouraging timely treatment. As athletic participation continues to grow worldwide, so does the demand for reliable and durable knee reconstruction devices.

Advancements in Minimally Invasive Surgical Techniques

A major factor driving the Knee Reconstruction Devices Market is the rapid adoption of minimally invasive surgical (MIS) techniques, which offer reduced recovery times, lower complication rates, and improved post-operative mobility compared to traditional open surgeries. These advancements are supported by improvements in imaging technology, robotic-assisted surgery, and bioengineered graft materials that enhance precision and integration with natural tissue. For instance, the use of autografts, allografts, and synthetic scaffolds has expanded, enabling surgeons to tailor reconstruction strategies based on patient anatomy and lifestyle requirements.

In addition, the U.S. Food and Drug Administration (FDA) has approved several next-generation devices in recent years, including absorbable fixation implants and smart grafts embedded with biosensors to monitor healing progress. Hospitals and ambulatory surgical centers are increasingly adopting these technologies to reduce hospitalization periods and improve patient satisfaction.

Furthermore, healthcare providers are incentivized to adopt MIS due to lower procedural costs and reduced burden on hospital resources. This evolution is directly fueling demand for compatible surgical instruments and implantable devices.

MARKET RESTRAINTS

High Cost of Advanced Knee Reconstruction Devices

A significant restraint affecting the Knee Reconstruction Devices Market is the high cost associated with advanced implants and surgical equipment, which limits accessibility for a large portion of the global population.

Even in developed regions, out-of-pocket expenses for knee reconstruction can be substantial. While insurance coverage helps mitigate some costs, co-payments and deductibles still pose barriers for many patients.

In emerging economies, where public healthcare systems often lack funding and private medical facilities remain unaffordable for most, the situation is even more challenging. As per the Indian Council of Medical Research, only 22% of Indians have access to comprehensive health insurance, restricting widespread adoption of premium knee reconstruction devices.

Also, regulatory hurdles and import duties in certain countries further inflate pricing. These financial constraints continue to hinder market expansion despite growing clinical demand.

Limited Reimbursement Policies in Developing Economies

An additional major constraint impacting the knee reconstruction devices market is the inconsistent or inadequate reimbursement policies in many developing countries, which discourage elective and non-emergency knee surgeries.

According to a 2024 report by the International Federation of Health Plans (IFHP), public health insurance schemes in Sub-Saharan Africa and South Asia typically cover less than 30% of orthopedic surgical procedures, leaving patients to bear the majority of the cost.

In Latin America, while countries like Brazil and Argentina offer partial reimbursement for knee reconstruction under their public health systems, bureaucratic delays and eligibility restrictions often prevent timely access to treatment.

Similarly, in parts of Eastern Europe and Southeast Asia, reimbursement frameworks do not fully recognize newer implant technologies, limiting their adoption. This lack of robust reimbursement infrastructure discourages both patients and healthcare providers from opting for advanced knee reconstruction procedures. As a result, despite rising awareness and demand, market penetration remains constrained in key growth regions.

MARKET OPPORTUNITIES

Expansion of Regenerative Medicine and Tissue Engineering

A promising opportunity for the Knee Reconstruction Devices Market lies in the expanding field of regenerative medicine and tissue engineering, which aims to restore knee function through biological rather than purely mechanical means. According to the International Society for Cellular Therapy (ISCT), regenerative treatments such as stem cell therapy, platelet-rich plasma (PRP) injections, and scaffold-based tissue regeneration are gaining traction as complementary or alternative options to conventional implants.

Biological scaffolds, in particular, are attracting significant investment from major orthopedic device manufacturers. Companies like Smith & Nephew and Zimmer Biomet have introduced bioengineered matrices designed to support cartilage and ligament regeneration, reducing the need for permanent metal or polymer implants. These innovations align with the growing preference for biocompatible, long-term solutions that integrate seamlessly with the body.

Also, academic institutions and research labs are advancing the development of 3D-printed biodegradable implants that degrade once native tissue regeneration is complete. As per the journal Nature Biomedical Engineering, preclinical trials have demonstrated promising results in terms of cellular integration and functional restoration.

With increasing regulatory approvals and patient interest in non-invasive alternatives, the integration of regenerative therapies into mainstream knee reconstruction is expected to drive new revenue streams and expand market reach beyond traditional implant-based solutions.

Growth of Telehealth and Remote Post-Operative Monitoring

An emerging opportunity in the Knee Reconstruction Devices Market is the integration of telehealth platforms and remote monitoring technologies into post-surgical care, enhancing patient recovery and improving long-term outcomes.

Remote monitoring devices, including wearable sensors and mobile applications, allow clinicians to track a patient's rehabilitation progress in real time. Smart implants equipped with embedded sensors such as those developed by OrthoSensor and Stryker, are capable of transmitting data on load distribution, joint movement, and implant wear, offering insights that help personalize rehabilitation plans.

In response to this trend, major players in the orthopedic space are partnering with digital health startups to develop integrated care ecosystems. For example, Johnson & Johnson launched a cloud-based platform in 2023 that connects knee replacement patients with physiotherapists and physicians via AI-driven analytics.

As healthcare systems seek to reduce readmission rates and optimize resource allocation, the convergence of knee reconstruction with digital health presents a compelling growth avenue, fostering innovation and improving patient engagement throughout the recovery process.

MARKET CHALLENGES

Regulatory Complexity and Lengthy Approval Processes

A major challenge facing the Knee Reconstruction Devices Market is the complex and time-consuming regulatory approval process required for new implant technologies. These prolonged approval cycles delay market entry for innovative products and increase R&D expenditures for manufacturers. According to the Advanced Medical Technology Association (AdvaMed), compliance costs for medium-sized orthopedic firms have risen by nearly 40% since 2020 due to stricter documentation, clinical evidence requirements, and post-market surveillance mandates.

In emerging markets, regulatory landscapes are often fragmented and inconsistently enforced. Countries such as India, Brazil, and Indonesia have implemented evolving standards for orthopedic implants, creating uncertainty for multinational companies seeking to expand regionally.

Furthermore, the requirement for extensive clinical validation of newer materials, such as bioresorbable implants and 3D-printed constructs, adds another layer of complexity. As regulatory scrutiny intensifies globally, device manufacturers must navigate a more intricate path to commercialization, slowing down the pace of innovation diffusion.

Risk of Implant Failure and Revision Surgeries

Another significant challenge in the Knee Reconstruction Devices Market is the persistent risk of implant failure and the subsequent need for revision surgeries, which impact both patient outcomes and healthcare expenditure. According to a study published in The Journal of Bone and Joint Surgery, revision rates for ACL reconstruction range between 5% and 10%, with factors such as graft choice, surgical technique, and patient compliance playing crucial roles.

Revision surgeries are not only more complex but also more costly, with average expenses exceeding those of primary procedures by up to 50%, as reported by the Blue Cross Blue Shield Association. Additionally, repeat operations expose patients to higher risks of infection, stiffness, and long-term joint instability.

Device-related complications, such as loosening, wear debris, and improper integration with surrounding tissue, contribute significantly to revision rates. Manufacturers are addressing these concerns through material innovation and design enhancements, yet challenges persist in ensuring long-term durability across diverse patient demographics.

Moreover, legal liabilities and recalls associated with faulty implants add pressure on manufacturers. As per the FDA’s MAUDE database, several knee reconstruction devices were recalled between 2021 and 2023 due to issues related to fixation strength and biocompatibility.

These factors underscore the ongoing need for rigorous quality control, continuous improvement in implant design, and enhanced patient education to mitigate the burden of revision surgeries on both healthcare systems and individual well-being.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered

| United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | Zimmer, Inc., Stryker, DePuy Synthes, Smith & Nephew plc, Arthrex, Exactech, Inc., Corin, DJO Global, Japan Medical Dynamic Marketing, Inc., and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The primary cemented implant segment commandedthe knee reconstruction devices market at 38.2% in 2024. This dominance is primarily attributed to the widespread adoption of cemented fixation techniques in total knee arthroplasty (TKA), especially among elderly patients suffering from osteoarthritis and rheumatoid arthritis.

One key driver of this segment’s leadership is the high success rate and long-term stability associated with cemented implants, particularly in older adults with lower bone density. Also, cemented implants remain the gold standard in revision surgeries where biological fixation may not be viable, further reinforcing their clinical relevance. With an aging global population and rising prevalence of degenerative joint diseases, primary cemented implants continue to maintain their stronghold in the knee reconstruction market.

The revision implant segment is growing at the fastest pace, recording a CAGR of 7.1%. This rapid growth is driven by the increasing number of failed primary knee replacements requiring corrective surgical interventions, particularly in mature markets with high historical implantation rates.

One major contributing factor is the rising incidence of implant wear, loosening, infection, and instability following primary knee arthroplasty, necessitating complex revision procedures. As per data from the National Joint Registry (NJR) of the UK, approximately 10% of all knee replacements require revision within ten years, highlighting the growing demand for advanced revision implants.

Moreover, technological advancements in modular revision systems and biocompatible materials have improved surgical outcomes and reduced complication risks. Companies like Zimmer Biomet, Stryker, and Smith & Nephew have introduced customizable revision components that accommodate diverse anatomical defects and restore joint functionality effectively.

Also, the expansion of orthopedic centers specializing in complex revision surgeries has enhanced access to treatment, particularly in North America and Europe. With the aging of previously implanted patient cohorts and the rise in obesity-related knee complications, the revision implant segment is expected to sustain its accelerated growth trajectory.

REGIONAL ANALYSIS

North America Knee Reconstruction Devices Market Analysis

North America maintained the largest regional market share at 39% in 2024, driven primarily by the United States’ robust healthcare infrastructure, high prevalence of knee disorders, and early adoption of advanced orthopedic technologies.

A key factor behind this dominance is the increasing incidence of osteoarthritis and sports-related knee injuries, which has led to a surge in both primary and revision knee surgeries. The Centers for Disease Control and Prevention (CDC) estimates that over 32 million Americans suffer from osteoarthritis, making knee replacement one of the most common elective procedures in the country.

Another significant influence is the presence of leading orthopedic device manufacturers and continuous innovation in implant design and surgical techniques. Major players such as Johnson & Johnson, Zimmer Biomet, and Stryker invest heavily in R&D, regulatory approvals, and strategic acquisitions to maintain competitive advantage.

Furthermore, favorable reimbursement policies under Medicare and private insurance schemes ensure broad accessibility to knee reconstruction procedures. These combined factors solidify North America’s position as the global leader in the knee reconstruction devices market.

Europe Knee Reconstruction Devices Market Analysis

Europe commands a notable regional market share, supported by well-established healthcare systems, high patient awareness, and favorable regulatory frameworks that facilitate the rapid integration of new orthopedic technologies.

Germany leads the European market due to its high volume of knee replacement surgeries and strong emphasis on medical device innovation. France and the UK also play pivotal roles, benefiting from advanced hospital networks and specialized orthopedic clinics. The National Health Service (NHS) in the UK continues to expand access to knee reconstruction procedures despite financial constraints, while France's mandatory health insurance system ensures broad coverage for implant-based treatments.

Also, the implementation of the Medical Device Regulation (MDR) across the EU has standardized product approval processes, enhancing trust in implant safety and efficacy.

Asia-Pacific Knee Reconstruction Devices Market Analysis

Asia-Pacific is one of the fastest-growing regions due to increasing healthcare expenditure, rising disposable incomes, and expanding medical tourism sectors in countries like India, China, and South Korea. Japan remains the largest contributor in the region, driven by its aging population and high prevalence of osteoarthritis. China is witnessing rapid modernization of orthopedic care, with government initiatives aimed at improving access to joint replacement surgery. India, meanwhile, is leveraging its medical tourism potential, offering cost-effective knee reconstruction solutions to international patients. Hospitals in cities like Mumbai, Delhi, and Chennai perform thousands of knee implants annually at a fraction of the cost compared to Western nations. With continued investment in healthcare infrastructure and technology transfer, APAC is poised for substantial market expansion.

Latin America Knee Reconstruction Devices Market Analysis

Latin America is an emerging region in the knee reconstruction devices market, with Brazil and Mexico leading the way due to improving healthcare access and rising awareness about orthopedic treatments.

Brazil accounts for the majority of knee implant procedures in the region, supported by public health programs under the Unified Health System (SUS). However, wait times for publicly funded surgeries remain long, prompting a growing number of patients to seek private alternatives.

Mexico, on the other hand, benefits from proximity to North American markets and participation in trade agreements that facilitate medical device imports. Despite economic fluctuations and inconsistent reimbursement policies, growing urbanization and rising middle-class affluence are driving gradual market growth. Local distributors and multinational firms are increasingly targeting LATAM for expansion, recognizing its untapped potential in the orthopedic space.

Middle East and Africa Knee Reconstruction Devices Market Analysis

The Middle East and Africa collectively account for a descent of the knee reconstruction devices market, with Saudi Arabia, UAE, and South Africa being the primary contributors.

In the Gulf region, rising healthcare investments and government-backed medical tourism initiatives are boosting orthopedic procedure volumes.

South Africa, the most developed healthcare market in Africa, sees moderate use of knee implants, though affordability and limited insurance coverage constrain broader adoption. Public hospitals often lack resources for complex knee reconstructions, leaving private clinics as the main providers.

Efforts by international orthopedic companies to establish distribution partnerships and conduct training workshops are gradually improving market access. While still in its early stages, the MEA region presents long-term growth opportunities as governments prioritize musculoskeletal health and expand medical infrastructure.

COMPETITIVE LANDSCAPE

The competition in the knee reconstruction devices market is intense, characterized by a mix of established multinational corporations and emerging regional players striving to capture market share through technological differentiation and strategic expansion. The presence of well-entrenched global leaders ensures a high degree of innovation and product diversification, while local manufacturers in emerging markets seek to offer cost-effective alternatives tailored to regional healthcare needs.

Product differentiation remains a core competitive factor, with companies focusing on advanced implant materials, minimally invasive surgical compatibility, and integration with digital health technologies such as robotics and data analytics. Brand reputation, surgeon preference, and long-term clinical performance play a decisive role in hospital procurement decisions and physician adoption.

Strategic moves such as mergers, acquisitions, and joint ventures are frequently used to strengthen market positions and expand into new geographies. Additionally, regulatory compliance and reimbursement policies significantly influence competitive dynamics, particularly in regions where healthcare budgets are constrained. As demand for knee reconstruction continues to rise globally, competition is expected to intensify further, driving ongoing advancements in implant technology and surgical methodologies.

KEY MARKET PLAYERS

Companies dominating the Global Knee Reconstruction Devices Market profiled in this report are

- Zimmer, Inc.

- Stryker

- DePuy Synthes

- Smith & Nephew plc

- Arthrex

- Exactech, Inc.

- Corin

- DJO Global

- Japan Medical Dynamic Marketing, Inc.

TOP LEADING PLAYERS IN THE MARKET

One of the leading companies in the knee reconstruction devices market is Johnson & Johnson, through its subsidiary DePuy Synthes, which has a strong global footprint in orthopedic implants and surgical solutions. The company offers a comprehensive range of knee reconstruction products, including advanced primary and revision implants, supported by robust research and development initiatives. Its commitment to innovation and strategic partnerships has solidified its leadership position.

Another key player is Zimmer Biomet, known for its extensive portfolio of knee arthroplasty systems that cater to both cemented and cementless fixation techniques. Zimmer Biomet emphasizes patient-specific implant technologies and digital surgery integration, enhancing clinical outcomes and surgeon adoption worldwide. The company’s continuous investment in next-generation implant materials and surface technologies reinforces its competitive edge.

Stryker Corporation also holds a dominant position in the market with a focus on advanced knee reconstruction solutions, including modular implants and minimally invasive surgical instruments. Stryker's emphasis on robotic-assisted knee surgery platforms, such as Mako, has transformed precision in implant placement. The company consistently expands its product offerings through acquisitions and R&D, ensuring sustained growth and market relevance across diverse healthcare settings.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

A major strategy employed by leading players in the knee reconstruction devices market is continuous innovation in implant design and biocompatible materials. Companies are investing heavily in developing patient-specific implants, bioresorbable fixation devices, and surface technologies that enhance osseointegration and reduce wear debris.

Another crucial approach is strategic acquisitions and partnerships to expand product portfolios and geographic reach. Major firms are acquiring smaller orthopedic startups and forming collaborations with digital health companies to integrate smart implants and remote monitoring capabilities into their offerings.

Lastly, enhancing digital integration in surgical planning and post-operative care is gaining traction. Manufacturers are incorporating AI-driven analytics, robotic-assisted surgery, and cloud-based rehabilitation tracking to improve surgical precision and patient recovery, thereby strengthening their market positioning and customer loyalty.

GLOBAL KNEE RECONSTRUCTION DEVICES MARKET NEWS

- In February 2024, Zimmer Biomet launched a next-generation cementless knee implant system designed for enhanced bone integration and longevity, targeting younger and more active patients seeking durable solutions without the need for future revisions.

- In May 2024, Stryker Corporation announced a strategic partnership with a European medical robotics firm to incorporate AI-powered preoperative planning tools into its Mako robotic platform, aiming to improve precision and reduce variability in knee implant procedures.

- In July 2024, Johnson & Johnson (DePuy Synthes) introduced a new line of personalized knee implants based on 3D imaging and patient-specific anatomical modeling, enhancing surgical accuracy and reducing intraoperative decision-making complexity.

- In September 2024, a leading South Korean orthopedic device manufacturer entered into a distribution agreement with a U.S.-based knee implant supplier to expand access to advanced reconstruction products in Asia-Pacific markets, leveraging localized supply chain efficiencies.

- In November 2024, Smith & Nephew unveiled a cloud-connected knee implant embedded with sensor technology capable of transmitting real-time load and movement data to clinicians, supporting improved post-operative rehabilitation and long-term patient monitoring.

MARKET SEGMENTATION

This research report on the global knee reconstruction devices market has been segmented and sub-segmented based on the product type and region.

By Product Type

- Primary Cemented

- Primary Cementless

- Partial

- Revision Implants

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the global knee reconstruction devices market?

The global knee reconstruction devices market includes implants, instruments, and technologies used for knee repair and replacement surgeries worldwide

2. What factors drive growth in the global knee reconstruction devices market?

Growth is driven by rising osteoarthritis, aging population, obesity, technological advances, and increasing adoption of minimally invasive procedures

3. What are key product types in the global knee reconstruction devices market?

Key types include total knee replacements, partial implants, revision implants, orthobiologics, and surgical instruments in the global knee reconstruction devices market

4. How does technology impact the global knee reconstruction devices market?

Robotics, patient-specific implants, and smart sensors are improving surgical precision and outcomes, boosting the global knee reconstruction devices market

5. Which regions lead the global knee reconstruction devices market?

North America dominates the global knee reconstruction devices market, followed by growing adoption in Asia-Pacific and Europe

6. What challenges face the global knee reconstruction devices market?

Challenges include high implant costs, reimbursement variability, and limited access in low-income areas in the global knee reconstruction devices market

7. How do minimally invasive surgeries affect the global knee reconstruction devices market?

They increase demand for advanced devices by offering faster recovery and less complication risks in the global knee reconstruction devices market

8. What role do revision implants play in the global knee reconstruction devices market?

Revision implants are critical for replacement surgeries after implant failure, holding growing share in the global knee reconstruction devices market

9. How is patient demand evolving in the global knee reconstruction devices market?

Younger, active patients seek durable, high-performance implants, shaping product innovation in the global knee reconstruction devices market

10. How does obesity influence the global knee reconstruction devices market?

Obesity increases knee disease prevalence, driving higher demand for reconstruction devices in the global knee reconstruction devices market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com