Global Orthopedic Devices Market Size, Share, Trends and Growth Forecast Report By Anatomical Location (Knee, Shoulder, Foot, Ankle, Hip, Spine, Elbow and Craniomaxillofacial), Consumable Type (Orthopedic Staples and Orthopedic Suture Anchors) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) - Industry Analysis (2026 to 2034)

Market Size, 2025

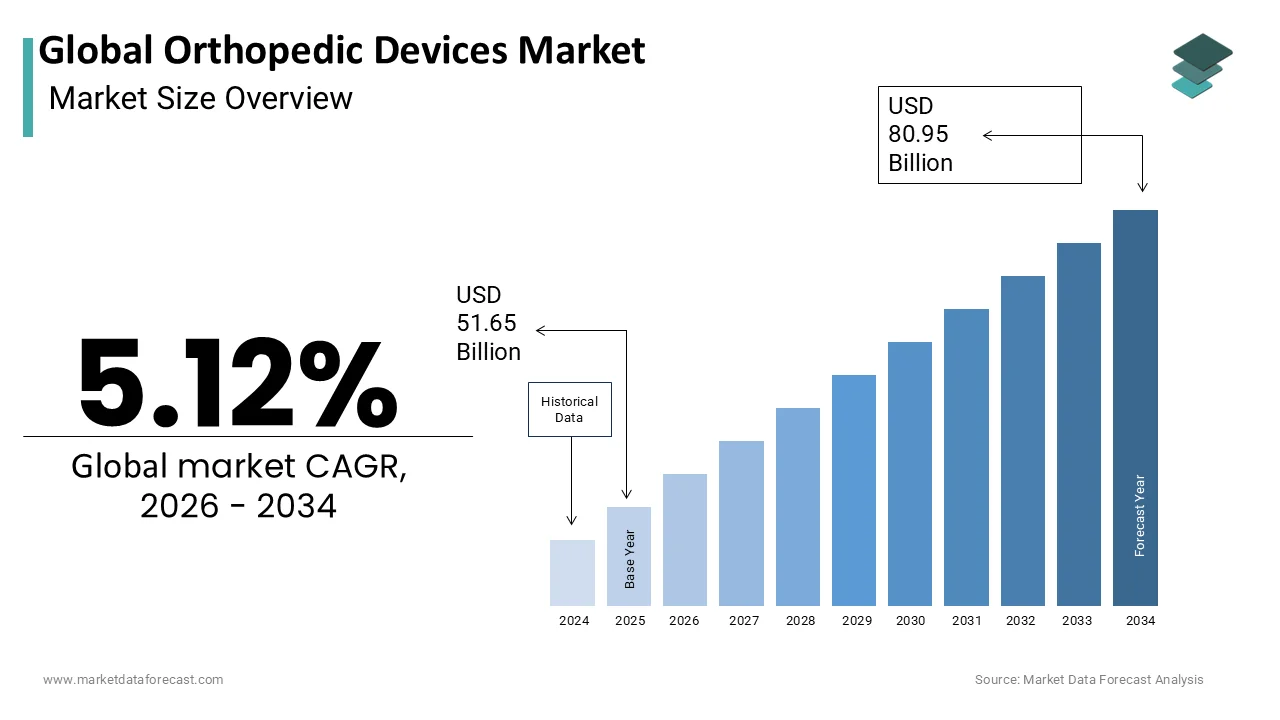

$51.65 BnMarket Estimate, 2026

$54.29 BnMarket Forecast, 2034

$80.95 BnCAGR, 2026–2034

5.12%Global Orthopedic Devices Market Summary

Market Size & Growth

- The global orthopedic devices market was valued at USD 51.65 billion in 2025.

- Expected to reach USD 80.95 billion by 2034, growing at a CAGR of 5.12% from 2026 to 2034.

- Intermediate value projected at USD 54.29 billion in 2026.

- North America leads with a 42.7% share of global market revenue in 2025.

- Asia Pacific is the fastest-growing region, projected to register the highest CAGR through 2034.

Key Market Segments

- By Anatomical Location: Knee, Hip, Shoulder, Spine, Foot, Ankle, Elbow, Craniomaxillofacial — Knee and Hip hold the largest combined share in 2025.

- By Consumable Type: Orthopedic Suture Anchors dominate with 62.7% of consumables revenue in 2025; Orthopedic Staples are the fastest-growing consumable segment at a CAGR of 7.2% from 2025 to 2033.

- By Region: North America leads; Asia Pacific is the fastest growing.

Key Drivers

- Over 528 million people worldwide suffer from osteoarthritis as of the Global Burden of Disease Study 2020, a 113% increase since 1990 — directly driving joint replacement demand.

- Approximately 1.19 million deaths occur annually from road traffic crashes (WHO), with millions more requiring orthopedic trauma intervention.

- Rapid adoption of robotic-assisted surgery platforms (Stryker Mako, Zimmer Biomet ROSA, J&J CMR) is expanding surgical precision and procedure volumes.

Key Players

Medtronic, Stryker, Zimmer Biomet, DePuy Synthes (Johnson & Johnson), Smith & Nephew, Biomed.

Global Orthopedic Devices Market Size

The Global Orthopedic Devices Market is projected to grow from USD 51.65 billion in 2025 to USD 54.29 billion in 2026 and reach USD 80.95 billion by 2034, registering a CAGR of 5.12% during the forecast period from 2026 to 2034.

Orthopedic Devices are medical technologies designed to diagnose, treat, and manage musculoskeletal conditions, including fractures, joint degeneration, spinal deformities, and sports-related injuries. These devices range from joint replacement implants, such as hip and knee prostheses, to spinal fixation systems, trauma fixation devices, and arthroscopic equipment. As populations age and the prevalence of degenerative bone disorders rises, orthopedic interventions have become central to restoring mobility and improving quality of life. The integration of advanced biomaterials, such as titanium alloys and bioceramics, alongside innovations in 3D printing and patient-specific implants, has redefined surgical precision and post-operative outcomes.

According to the World Health Organization, musculoskeletal conditions affect more than 1.7 billion people globally, making them a leading cause of disability. Furthermore, the rise in high-impact injuries due to urbanization and road traffic accidents has amplified demand for trauma care solutions.

MARKET DRIVERS

Increasing Prevalence of Osteoarthritis and Joint Degeneration

The escalating incidence of osteoarthritis (OA) stands as a pivotal demand driver for orthopedic devices, particularly joint replacement systems. OA, the most common form of arthritis, results in progressive cartilage degradation, leading to chronic pain and impaired mobility.

As per the Global Burden of Disease Study 2020, over 528 million people worldwide suffer from osteoarthritis, marking a 113% increase in prevalence since 1990. This surge is largely attributed to aging populations and rising obesity rates, both of which intensify joint stress.

In the United States alone, the Centers for Disease Control and Prevention estimates that 32.5 million adults are affected by OA, with knee involvement being the most prevalent. The economic burden is equally significant. These factors collectively fuel demand for durable, biocompatible implants. Moreover, advancements in minimally invasive joint arthroplasty and the development of gender-specific and anatomically tailored prostheses have enhanced patient acceptance and clinical success rates, further accelerating market expansion.

Rising Trauma Incidence from Accidents and Sports Injuries

Trauma-related musculoskeletal injuries are a critical catalyst for orthopedic device utilization, driven by urbanization, increased vehicular traffic, and growing participation in high-intensity sports. The World Health Organization reports that approximately 1.19 million deaths occur annually due to road traffic crashes, with millions more sustaining non-fatal injuries requiring orthopedic intervention. Notably, fractures of the femur, tibia, and pelvis often necessitate internal fixation devices such as intramedullary nails, plates, and screws. Beyond vehicular accidents, sports-related injuries are on the rise, particularly in developed economies. As per the American Academy of Orthopaedic Surgeons, over 3.5 million children in the U.S. sustain sports injuries annually, with anterior cruciate ligament (ACL) tears requiring arthroscopic reconstruction becoming increasingly common. The demand for arthroscopic devices, trauma plating systems, and external fixators has surged accordingly. Additionally, military conflicts and natural disasters contribute to complex fracture cases, further expanding the need for advanced orthopedic solutions in both civilian and emergency care settings.

MARKET RESTRAINTS

High Cost of Advanced Orthopedic Implants and Procedures

The prohibitive cost associated with advanced implants and surgical interventions, limiting accessibility, particularly in low- and middle-income regions, is one of the most significant restraints in the orthopedic devices market. In developing nations, such costs are often insurmountable. Even in countries with public healthcare systems, long waiting times persist due to budgetary constraints. The high cost stems from the use of premium materials such as cobalt-chrome alloys and polyetheretherketone (PEEK), stringent regulatory compliance, and the need for specialized surgical training. Additionally, the integration of robotic-assisted surgery platforms, improves precision. These financial barriers restrict market penetration and hinder equitable access to life-enhancing orthopedic care.

Stringent Regulatory Pathways and Prolonged Approval Timelines

The orthopedic devices sector faces substantial delays due to rigorous regulatory scrutiny, particularly in mature markets such as the United States and the European Union. The U.S. Food and Drug Administration (FDA) requires extensive clinical data and conformity assessments for Class II and Class III devices, with the average premarket approval (PMA) or (510-k) process taking several months. For novel implant technologies, such as biodegradable fixation devices or smart implants with embedded sensors, the timeline can extend beyond three years due to the need for long-term biocompatibility and performance studies. In the European Union, the transition from the Medical Devices Directive (MDD) to the Medical Devices Regulation (MDR) in 2021 has intensified compliance demands. This scarcity has led to significant delays, with some manufacturers reporting an increase in time-to-market. In Japan, the Pharmaceuticals and Medical Devices Agency (PMDA) encourages local clinical trials for many high-risk devices, even if extensive international data exists, adding both time and cost. These regulatory complexities discourage innovation among small and medium-sized enterprises, which lack the financial resilience to sustain prolonged development cycles. Consequently, patient access to cutting-edge orthopedic technologies is delayed, and market growth is constrained despite strong clinical demand.

MARKET OPPORTUNITIES

Expansion of Minimally Invasive and Patient-Specific Implant Technologies

Advancements in minimally invasive surgical (MIS) techniques and patient-specific implants (PSIs) represent a transformative opportunity in the orthopedic devices market. Unlike traditional open surgeries, MIS procedures reduce tissue damage, shorten hospital stays, and accelerate recovery. The global market for minimally invasive orthopedic devices is expanding rapidly, driven by innovations in arthroscopy, percutaneous fixation, and navigation-guided implantation. Furthermore, the integration of 3D printing and computed tomography (CT)-based modeling has enabled the production of PSIs tailored to individual anatomies. Companies such as Stryker and Zimmer Biomet have launched proprietary PSI platforms. These technologies not only enhance clinical outcomes but also reduce revision rates. As imaging resolution and manufacturing precision improve, the scalability of PSIs is expected to grow, unlocking new avenues for personalized orthopedic care.

Growing Adoption of Robotics and Digital Surgical Navigation in Orthopedics

The integration of robotics and digital navigation systems into orthopedic surgery is revolutionizing procedural accuracy and reproducibility, presenting a major growth opportunity. Robotic-assisted systems, such as the Mako by Stryker, ROSA by Zimmer Biomet, and CMR by Johnson & Johnson, enable real-time intraoperative feedback, ensuring optimal implant positioning and soft tissue balance. Like, robotic-assisted total knee arthroplasty reduces outliers in mechanical alignment compared to conventional techniques. In the U.S., the utilization of robotic systems in joint replacement has grown exponentially. Hospitals report reduced revision rates and shorter recovery times, enhancing cost-effectiveness over the long term. Beyond joint surgery, spinal robotics is gaining traction. Digital navigation, which uses infrared tracking and preoperative imaging, is also expanding in trauma surgery, particularly in complex fracture reductions. With artificial intelligence beginning to integrate into surgical planning platforms, the convergence of digital health and orthopedics is poised to redefine standards of care, driving sustained innovation and market expansion.

MARKET CHALLENGES

Shortage of Skilled Orthopedic Surgeons and Technical Experts

The global shortage of trained orthopedic surgeons and specialized technical personnel capable of deploying advanced technologies is a critical challenge impeding the orthopedic devices market. In sub-Saharan Africa, the World Health Organization reports that countries have a significant shortage of orthopedic surgeons per 100,000 population, severely limiting access to essential musculoskeletal care. Even in middle-income countries like Indonesia, there persists a shortage of orthopedic specialists to meet national demand. The complexity of modern procedures, such as robotic-assisted surgery, spinal instrumentation, and custom implant placement, requires extensive training and continuous upskilling. However, training infrastructure remains inadequate in many regions. This scarcity delays technology adoption, increases surgical complications, and limits the scalability of innovative orthopedic solutions, ultimately constraining market growth despite rising clinical demand.

Post-Operative Infection and Implant Failure Risks

Post-operative infections and implant failures remain persistent challenges in orthopedic surgery, undermining patient outcomes and increasing healthcare costs. Periprosthetic joint infection (PJI) is one of the most severe complications following joint replacement, with incidence rates ranging from 1% to 2% in primary procedures and up to 4% in revisions. Treating such infections often requires prolonged antibiotic therapy, surgical debridement, and two-stage revision surgery, which can be costly for a patient. Biofilm formation on implant surfaces makes eradication particularly difficult, with high recurrence rates. Similarly, aseptic loosening, caused by wear debris and osteolysis, accounts for a notable share of revision hip and knee surgeries. Spinal implants face additional risks, including adjacent segment disease and hardware migration. Also, some of the patients undergoing lumbar fusion required reoperation within five years. These complications not only diminish patient trust but also increase regulatory scrutiny and litigation risks for manufacturers. Consequently, the industry faces mounting pressure to develop antimicrobial coatings, improved bearing surfaces, and smarter implants with remote monitoring capabilities to mitigate long-term failure risks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Analysed | By Anatomical Location, Consumable Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Analysed | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Medtronic, Stryker, Zimmer Inc., DePuy Synthes, Smith & Nephew, and Biomed |

SEGMENTAL ANALYSIS

By Anatomical Location Insights

Based on the anatomical location, the knee and hip segments are the most lucrative segments and accounted for the largest share of the global orthopedic devices market in 2025. Therefore, it is also anticipated that these segments will hold the major share of the worldwide market during the forecast period. The growing prevalence of arthritis and other orthopedic diseases majorly drives the growth of the segments. In addition, factors such as the growing aging population and rapid adoption of technological developments are propelling segmental growth. On the other hand, segments such as spine and craniomaxillofacial are anticipated to witness a promising CAGR during the forecast period. The growing demand for minimally invasive surgical procedures is one of the major factors driving the segment's growth rate.

By Type of Consumables Insights

The orthopedic suture anchors segment remained the prominent part within the orthopedic consumables market by capturing an estimated 62.7% of total revenue in 2025. This dominance is anchored in the widespread application of suture anchors in soft tissue-to-bone fixation, particularly in arthroscopic shoulder and knee procedures. Rotator cuff tears, one of the most common musculoskeletal injuries, affect around 2 million Americans annually. The standard treatment for full-thickness tears involves arthroscopic repair using bioabsorbable or metallic suture anchors, with a significant quantity of such procedures performed in the U.S. each year. The versatility of suture anchors extends beyond the shoulders; they are increasingly used in ankle ligament reconstruction, hip labral repair, and elbow ulnar collateral ligament (UCL) surgeries, especially among athletes. The evolution of knotless anchor systems has further enhanced adoption, reducing surgical time and improving biomechanical stability. Besides, the shift toward outpatient arthroscopy and the growing prevalence of sports-related injuries, particularly in younger demographics, are amplifying demand. With rising participation in high-impact sports and increasing awareness of early intervention, suture anchors remain indispensable in modern orthopedic practice, securing their position as the leading consumable category.

The orthopedic staples segment is experiencing the fastest growth within the consumables segment and is projected to grow at a CAGR of 7.2% from 2025 to 2033. This surge is driven by their expanding role in minimally invasive and trauma surgeries, where rapid, secure closure of fascia and soft tissues is critical. Unlike traditional sutures, orthopedic staples offer faster application, reduced operative time, and lower risk of tissue necrosis, making them ideal for high-tension closures in joint replacement and spinal procedures. The increasing volume of total joint arthroplasties directly correlates with staple usage. In trauma settings, staples are preferred in emergency orthopedic interventions due to their efficiency; as per a study, staple closure reduced skin closure time compared to sutures in tibial fracture surgeries. Moreover, advancements in absorbable and low-profile metallic staples have improved cosmetic outcomes and reduced post-operative complications. As surgical efficiency becomes a key metric in value-based healthcare models, the demand for time-saving, reliable closure devices like orthopedic staples is poised for continued acceleration.

REGIONAL ANALYSIS

North America Orthopedic Devices Market Insights

North America continued at a commanding position in the global orthopedic devices market by securing a 42.7% ofthe total share in 2025. The region’s lead position is underpinned by a robust healthcare infrastructure, high patient awareness, and strong reimbursement mechanisms for orthopedic procedures. The United States, in particular, performs a significant number of joint replacement surgeries annually, with Medicare covering over 80% of these procedures. The prevalence of osteoarthritis and obesity, two key risk factors for joint degeneration, is exceptionally high; a notable portion of U.S. adults are obese, placing immense stress on weight-bearing joints. Additionally, the presence of leading device manufacturers such as Stryker, Zimmer Biomet, and Johnson & Johnson fosters rapid innovation and commercialization. The adoption of robotic-assisted surgery is also most advanced in this region. With rising investments in digital surgery platforms and a growing geriatric population, North America remains the epicenter of orthopedic device innovation and utilization.

Europe Orthopedic Devices Market Insights

Europe maintains a strong market share. The region exhibits a mature but evolving orthopedic landscape, characterized by universal healthcare coverage and a rapidly aging population. Germany, the UK, and France are the primary contributors, with Germany alone performing a significant number of joint replacements annually. However, access to advanced devices is often constrained by budgetary limitations and lengthy approval cycles under the EU Medical Devices Regulation (MDR). Despite these challenges, countries like Sweden and Switzerland lead in the adoption of minimally invasive and robotic-assisted techniques, with robotic knee arthroplasty utilization surging in private hospitals. Millions of Europeans suffer from musculoskeletal disorders, with back pain being the most common cause of work-related disability. The push for outpatient orthopedic care and shorter hospital stays is driving demand for efficient, low-complication devices. Furthermore, public-private partnerships in countries like the Netherlands are accelerating clinical trials and innovation in biodegradable implants, positioning Europe as a hub for next-generation orthopedic solutions despite regulatory headwinds.

Asia-Pacific Orthopedic Devices Market Insights

The Asia-Pacific region is emerging as a pivotal growth engine andis projected to expand at the highest CAGR over the next decade. This growth is fueled by rising healthcare expenditure, expanding medical infrastructure, and a burgeoning middle class with increasing access to elective surgeries. China and India represent the largest markets; in China, orthopedic surgery volumes grew annually between 2018 and 2022, driven by urbanization and rising traffic-related trauma. India, with a large number of individuals affected by osteoarthritis, is witnessing the rapid adoption of joint replacements in private hospitals. Government initiatives such as Ayushman Bharat have improved affordability, covering up to 500,000 rupees per family per year for secondary and tertiary care, including orthopedic procedures. Additionally, local manufacturing and collaborations with global firms, such as Smith & Nephew’s joint venture in Hyderabad, are reducing costs and enhancing supply chain resilience. So, the demand for orthopedic interventions will continue to escalate, solidifying the region’s strategic importance.

Latin America Orthopedic Devices Market Insights

Latin America holds a modest share of the global orthopedic devices market, yet exhibits significant untapped potential. Brazil and Mexico are the dominant markets, with Brazil accounting for a major portion of regional orthopedic procedures. However, rising obesity rates are increasing the prevalence of joint disorders. Private healthcare providers in cities like São Paulo and Mexico City are adopting advanced implants and arthroscopic techniques, catering to medical tourists from North America. The region also faces a high burden of trauma. Despite economic volatility and fragmented reimbursement, increasing investments in healthcare infrastructure and the expansion of private insurance are creating favorable conditions for market growth, particularly in minimally invasive and cost-effective devices.

Middle East and Africa Orthopedic Devices Market Insights

The Middle East and Africa collectively represent a small share of the global orthopedic devices market, with growth concentrated in the Gulf Cooperation Council (GCC) nations. Countries like Saudi Arabia and the United Arab Emirates are modernizing their healthcare systems under national visions such as Saudi Vision 2030, which includes expanding specialized orthopedic centers. Orthopedic surgery volumes increased in Saudi Arabia between 2020 and 2023, supported by government-funded initiatives and medical tourism. In the UAE, a large number of joint replacements were performed, with Dubai and Abu Dhabi emerging as regional hubs for advanced care. However, sub-Saharan Africa faces severe challenges; the majority of orthopedic needs remain unmet due to a lack of surgeons, facilities, and funding. In Nigeria, there are fewer orthopedic surgeons for a population of 220 million. Road traffic accidents, a leading cause of musculoskeletal trauma. While the region lags in market size, strategic investments in training, telemedicine, and affordable implant solutions could unlock substantial growth in the coming decade.

KEY MARKET PLAYERS

Notable companies leading the global orthopedic devices market profiled in the report are Medtronic, Stryker, Zimmer Inc., DePuy Synthes, Smith & Nephew, and Biomed. In addition, the market is categorized by diversified international and national companies, where the global players lead the market and are predicted to grow exponentially by securing regional or local companies.

TOP LEADING PLAYERS IN THE MARKET

Zimmer Biomet

Zimmer Biomet is a global leader in musculoskeletal healthcare, renowned for its comprehensive portfolio spanning joint reconstruction, spine, trauma, and sports medicine. The company has consistently driven innovation through advanced implant design, robotic-assisted surgery platforms, and data-driven care models. Its flagship ROSA Knee System exemplifies its commitment to precision and personalized surgical outcomes. With a strong presence across developed and emerging markets, Zimmer Biomet collaborates extensively with clinicians and research institutions to shape the future of orthopedic interventions. The company’s integrated solutions, which combine implants, instruments, and digital technologies, have redefined standards in surgical efficiency and patient recovery, solidifying its reputation as a pioneer in the field.

Stryker stands

Stryker stands at the forefront of orthopedic technology, known for its disruptive innovations in robotic surgery, navigation, and smart implants. The company’s Mako robotic-arm-assisted system has transformed joint arthroplasty by enabling real-time, patient-specific planning and execution. Stryker emphasizes a solutions-based approach, integrating hardware, software, and services to optimize clinical workflows. Its robust R&D pipeline and strategic focus on minimally invasive techniques have strengthened its foothold in both hospital and ambulatory surgery center settings. With a global footprint and a culture of continuous innovation, Stryker plays a pivotal role in advancing surgical precision and improving long-term implant performance across knee, hip, and spine procedures.

Johnson & Johnson

Johnson & Johnson (DePuy Synthes) operates as a cornerstone in the orthopedic landscape, offering a broad spectrum of products in joint replacement, trauma, craniomaxillofacial, and spinal surgery. The company’s legacy of clinical excellence is supported by deep scientific expertise and a commitment to evidence-based medicine. DePuy Synthes has been instrumental in developing advanced biomaterials, motion-preserving spinal devices, and next-generation bearing surfaces for joint implants. Its global reach, extensive sales network, and collaboration with surgical societies enable widespread adoption of its technologies. By prioritizing education, training, and surgeon engagement, the company fosters trust and consistency in clinical outcomes, maintaining its status as a dominant force in shaping the evolution of orthopedic care.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading companies is the integration of digital surgery platforms, including robotics, AI-driven planning, and intraoperative navigation, to enhance surgical accuracy and reproducibility. By embedding intelligence into surgical workflows, firms are shifting from passive implant providers to active care partners, offering end-to-end procedural ecosystems that improve outcomes and reduce variability. This transformation strengthens brand loyalty and differentiates offerings in a competitive landscape.

Another key approach is strategic collaboration with academic institutions, hospitals, and technology startups to accelerate innovation. These partnerships enable access to early-stage research, real-world clinical insights, and novel engineering concepts, facilitating the development of next-generation devices such as biodegradable implants and smart prostheses with remote monitoring capabilities.

A third critical strategy is geographic expansion into high-growth emerging markets through localized manufacturing, distribution alliances, and tailored product portfolios. By adapting to regional clinical needs, regulatory environments, and cost sensitivities, companies ensure broader accessibility while building sustainable market presence beyond traditional strongholds in North America and Europe.

COMPETITION OVERVIEW

The competitive landscape of the orthopedic devices market is characterized by intense rivalry among established multinational corporations and a growing influx of innovative niche players. Dominant firms leverage extensive R&D capabilities, global distribution networks, and strong brand recognition to maintain leadership, particularly in high-value segments such as robotic-assisted surgery and advanced joint implants. However, the market is undergoing a structural shift as technological convergence spanning digital health, artificial intelligence, and advanced materials redefines competitive advantage. Companies are increasingly competing not just on implant design but on integrated procedural ecosystems that enhance surgical efficiency, predictability, and patient recovery. Differentiation is achieved through proprietary software platforms, surgeon training programs, and data analytics that support value-based care models. At the same time, regulatory complexity and reimbursement pressures necessitate operational agility and strategic foresight. Emerging players are challenging incumbents by introducing cost-effective alternatives and disruptive technologies, particularly in minimally invasive and outpatient-focused solutions. The rise of private-label devices and regional manufacturers in Asia further intensifies competition, compelling global leaders to innovate continuously and expand their service offerings. As healthcare systems prioritize cost containment and clinical outcomes, the competitive edge lies in delivering not only superior devices but comprehensive, evidence-based solutions that align with evolving care delivery paradigms.

RECENT MARKET DEVELOPMENTS

- In March 2025, Stryker acquired Gauss Surgical, a developer of AI-powered blood loss monitoring technology, to enhance real-time surgical decision-making in orthopedic procedures. This integration is expected to improve patient safety and operational efficiency in robotic and complex joint surgeries.

- In January 2025, Zimmer Biomet launched its CMF Planning Studio, a cloud-based digital platform for craniomaxillofacial surgery, enabling 3D surgical planning and patient-specific implant design. This advancement strengthens its digital ecosystem in specialized orthopedic segments.

- In September 2023, Johnson & Johnson’s DePuy Synthes partnered with Verb Surgical to further develop robotic and digital surgery platforms, aiming to integrate advanced visualization and machine learning into orthopedic workflows.

- In July 2023, Smith & Nephew introduced its AI-powered robotics platform, CORI, in new European markets, expanding its footprint in smart surgery and reinforcing its focus on data-driven joint arthroplasty solutions.

- In May 2023, Exactech announced a strategic collaboration with a South Korean distributor to expand its joint replacement portfolio across Southeast Asia, enhancing regional access to its advanced knee and hip implants.

MARKET SEGMENTATION

This research report on the global orthopedic devices market has been segmented and sub-segmented into anatomical location, consumable type, and region.

By Anatomical Location

- Knee

- Shoulder

- Foot

- Ankle

- Hip

- Spine

- Elbow

- Craniomaxillofacial

By Type of Consumables

- Orthopedic Staples

- Orthopedic Suture Anchors

- Resorbable Suture Anchors

- Metallic Suture Anchors

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1.How much is the global orthopedic devices market going to be worth by 2033?

As per our research report, the global orthopedic devices market size is forecasted to grow to USD 77 billion by 2033.

2. Which are the key players operating in the orthopedic devices market?

Medtronic, Stryker, Zimmer Inc., DePuy Synthes, Smith & Nephew, and Biome are some of the noteworthy players in the global orthopedic devices market.

3. What is the growth rate of the global orthopedic devices market?

The global orthopedic devices market is estimated to grow at a CAGR of 5.12% during the forecast period.

4.What are the key drivers of growth in the Orthopedic Devices Market?

Growth is driven by rising musculoskeletal disorders, aging population, technological advances, and increasing sports injuries.

5. How is the aging global population impacting the Orthopedic Devices Market?

An increasing elderly population with osteoarthritis and osteoporosis boosts demand for joint and bone replacement implants globally

6. What geographic regions dominate the Orthopedic Devices Market?

North America leads with over 50% share, followed by Europe and Asia-Pacific showing significant growth prospects.

7. Are technological advancements influencing the Orthopedic Devices Market?

Yes, innovations like 3D printing, AI in surgery planning, and robotic-assisted procedures are positively impacting the market

8. What is the role of knee replacement devices in the Orthopedic Devices Market?

Knee replacement devices hold the largest share due to high incidence of knee osteoarthritis and injury cases across regions.

9. What are orthobiologics and how do they fit in the Orthopedic Devices Market?

Orthobiologics are biologically based treatments like bone grafts and DBM, increasingly used in surgeries to enhance healing.

10. Which end users contribute most to the Orthopedic Devices Market?

Hospitals, ambulatory surgical centers, and orthopedic clinics dominate the demand for these devices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com