- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

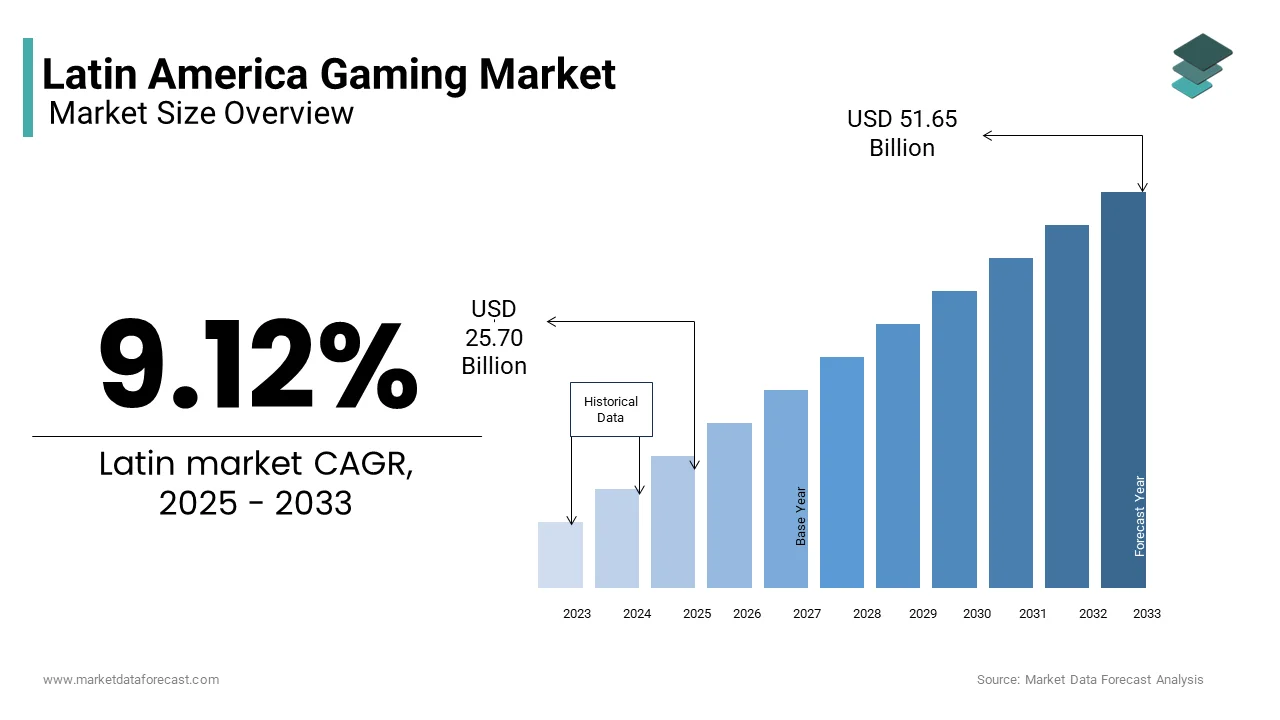

Market Size, 2025

$25.70 BnMarket Estimate, 2026

$28.04 BnMarket Forecast, 2034

$56.37 BnCAGR, 2026–2034

9.12%Latin America Gaming Market Size

The Latin American gaming market was valued at USD 25.70 billion in 2025 and is anticipated to reach USD 28.04 billion in 2026, from USD 56.37 billion by 2034, growing at a CAGR of 9.12% during the forecast period from 2026 to 2034.

The Latin American gaming market involves a diverse ecosystem that includes console, PC, mobile, and online gaming segments. It reflects the growing integration of digital entertainment into everyday life across countries such as Brazil, Mexico, Argentina, Colombia, and Chile. With rising disposable incomes, increasing internet penetration, and a youthful population, the region has emerged as a key growth area in the global gaming landscape.

Moreover, the rise of e-sports and live streaming has further fueled interest in gaming culture. Platforms like Twitch and YouTube Gaming have seen exponential growth in Latin American audiences, with millions tuning in daily to watch competitive matches and streamer content.

MARKET DRIVERS

Rapid Growth of Mobile Internet and Smartphone Penetration

One of the primary drivers of the Latin American gaming market is the rapid proliferation of mobile internet and smartphone adoption, which has significantly expanded the reach of gaming content. According to GSMA Intelligence, mobile internet penetration in Latin America reached 72% in 2023, with over 400 million unique mobile subscribers across the region. This widespread connectivity enables consumers to access games anytime and anywhere, fostering a shift toward mobile-first gaming experiences.

In Brazil, smartphone ownership exceeded 80% among the adult population in 2023, as reported by the Brazilian Institute of Geography and Statistics (IBGE). This high level of device penetration has made mobile gaming the most accessible and widely adopted form of interactive entertainment. Games like Free Fire, developed by Sea Limited, have capitalized on this trend, achieving over 100 million downloads in Latin America, according to Sensor Tower data.

Mexico has also experienced a surge in mobile gaming, particularly among younger demographics. As mobile networks continue to evolve with 5G deployment and app store ecosystems mature, the accessibility and affordability of mobile gaming will remain a major catalyst for sustained market growth across Latin America.

Increasing Youth Demographics and Digital Engagement

Another critical driver fueling the Latin America gaming market is the region’s large and digitally engaged youth population. This young demographic is highly receptive to digital entertainment, making gaming a central part of their lifestyle.

In Argentina, where youth unemployment remains a persistent challenge, gaming has emerged as a significant pastime and even a potential career path.

Schools and universities have started incorporating gamified learning methods, further embedding digital interaction into early education.

This generational shift toward digital engagement is not only boosting consumer demand but also encouraging local talent development and entrepreneurship in game development studios.

MARKET RESTRAINTS

Economic Instability and Currency Volatility

Economic instability and currency volatility represent major restraints on the Latin American gaming market, limiting consumer purchasing power and discouraging long-term investment. Several countries in the region, including Argentina, Venezuela, and Ecuador, have faced persistent inflationary pressures that erode real income levels and reduce discretionary spending.

According to the International Monetary Fund, Argentina recorded an annual inflation rate of over 211% in 2023, making it difficult for consumers to justify expenditures on premium games, subscriptions, or hardware.

In Brazil, despite a relatively stable macroeconomic environment compared to its neighbors. As reported by the Brazilian Institute of Economics at FGV, this price sensitivity led to a noticeable decline in premium game purchases among mid-income households.

These economic challenges create uncertainty for both global publishers and local developers, who must navigate fluctuating exchange rates while trying to maintain competitive pricing strategies.

Regulatory Complexity and Taxation Barriers

Regulatory complexity and taxation barriers pose another significant restraint on the Latin American gaming market, creating operational hurdles for international developers and local businesses alike. Each country in the region maintains distinct tax regimes, import duties, and content regulations, complicating market entry and distribution strategies.

In Brazil, for instance, the federal government imposes a high import tax on physical gaming consoles and software. These tariffs make imported gaming products prohibitively expensive for many consumers and incentivize informal or gray-market transactions instead of legal retail channels.

Similarly, in Mexico, value-added tax (VAT) policies apply to digital content purchases, including downloadable games and in-game microtransactions.

Argentina has taken a more restrictive approach, requiring all locally distributed games to undergo mandatory classification by the National Directorate of Audiovisual Classification before release. Until regulatory frameworks become more harmonized and business-friendly, compliance costs and administrative burdens will continue to hinder the Latin American gaming market’s full commercial potential.

MARKET OPPORTUNITY

Expansion of Cloud Gaming and Subscription-Based Services

A major opportunity shaping the Latin American gaming market is the expansion of cloud gaming and subscription-based services, which offer cost-effective and flexible alternatives to traditional game ownership models. As internet infrastructure improves and broadband speeds increase, more consumers are shifting away from purchasing individual titles toward accessing vast libraries via monthly subscriptions.

In Brazil, Google Stadia and Xbox Cloud Gaming have gained traction among budget-conscious gamers who cannot afford high-end PCs or next-generation consoles.

Xbox Game Pass has been particularly successful in Latin America. The service’s affordable pricing and inclusion of localized language support have helped attract a broad audience beyond traditional gaming demographics.

With continued investment in network infrastructure and strategic partnerships with local ISPs, cloud gaming is positioned to unlock a new wave of growth across Latin America.

Rise of Local Game Development and Indie Studios

The emergence of local game development and independent studios presents a compelling opportunity for the Latin American gaming market. A growing number of regional creators are leveraging digital distribution platforms like Steam, Itch.io, and the Epic Games Store to launch original titles that resonate with both domestic and international audiences.

Brazil has also seen a surge in homegrown talent, with studios like Aquiris Game Studio (developers of NASCAR Heat Mobile ) securing publishing deals with major companies like Electronic Arts. According to the Brazilian Game Developers Association (BIG Festival organizers), the number of registered game studios in Brazil increased in 2023, supported by government grants and incubator programs.

Colombia and Chile are following suit, with government-backed initiatives aimed at fostering creative industries. As funding options grow and international visibility increases, Latin America’s indigenous gaming scene is well-positioned to contribute significantly to the region’s digital economy.

MARKET CHALLENGES

Piracy and Unauthorized Distribution of Games

Piracy and unauthorized distribution of games remain a persistent challenge for the Latin American gaming market, undermining legitimate sales and deterring investment from international publishers. Despite improvements in digital payment systems and content licensing, illegal downloads and cracked versions of games continue to circulate widely across the region.

According to a 2023 report by the Global Innovation Policy Center, Latin America consistently ranks among the top regions for game piracy, with Brazil and Mexico being major hotspots. Torrent sites, unofficial app stores, and social media links serve as common distribution channels, often offering pirated copies of premium titles within days of their official release.

In Argentina, enforcement of intellectual property laws remains inconsistent, allowing rogue websites to operate without significant consequences. As per the National Institute of Industrial Property (INPI), authorities shut down over 500 illegal game distribution sites in 2023, yet new ones quickly replaced them, highlighting the scale of the issue.

This rampant piracy affects not only global publishers but also local developers, who struggle to monetize their work in an environment where free alternatives are readily available. Without stronger legal deterrents and public awareness campaigns, piracy will continue to stifle market growth and discourage innovation in the Latin American gaming sector.

Infrastructure Limitations and Uneven Broadband Access

Infrastructure limitations and uneven broadband access pose a significant challenge to the Latin American gaming market, particularly in rural and semi-urban areas. While major metropolitan centers enjoy relatively fast and stable internet connections, many regions still suffer from inadequate network coverage and slow download speeds, hindering participation in online and cloud-based gaming.

According to the Inter-American Development Bank, a significant portion of rural roads in Latin America lack reliable internet infrastructure, limiting the ability of residents to engage with digital entertainment.

In Brazil, despite national broadband expansion efforts, upload and download speeds in smaller towns remain below the threshold required for seamless multiplayer gaming.

These infrastructural gaps prevent a substantial portion of the population from fully participating in the digital gaming revolution. Addressing these limitations requires coordinated public-private investments in fiber-optic networks, satellite internet, and mobile broadband upgrades to ensure equitable access across the region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.12% |

| Segments Covered | By Device, Type, and Region. |

|

Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | Brazil, Chile, Argentina, Mexico, and Colombia, etc |

| Market Leaders Profiled | Activision Blizzard, Inc., Apple, Inc., The Walt Disney Company, Electronic Arts, Inc., Microsoft Corporation, Nintendo Co., Ltd, Rovio Entertainment Corporation, Sega Enterprises, Inc., Sony Corporation, Tencent Holdings Ltd. |

SEGMENTAL ANALYSIS

By Device Insights

Mobile gaming is the largest segment in the Latin American gaming market, capturing 58.2%th % of the total revenue share in 2024. This dominance stems from the widespread adoption of smartphones and the affordability of mobile games compared to console or PC-based alternatives.

According to GSMA Intelligence, mobile penetration in Latin America reached over 72% in 2023, with more than 400 million unique subscribers, making it the most accessible platform for digital entertainment.

In Mexico, mobile gaming has become the preferred format among younger demographics, particularly due to the popularity of free-to-play titles with in-app purchases.

Moreover, local developers are increasingly targeting mobile platforms due to lower development costs and easier distribution via app stores. In Argentina, indie studios have leveraged this trend to launch successful regional titles that also gain international traction.

With continued improvements in mobile internet infrastructure and smartphone affordability, the mobile gaming segment remains the cornerstone of the Latin American gaming industry.

The console gaming segment is emerging as the fastest-growing device category in the Latin American gaming market, projected to expand at a CAGR of 9.4%. This growth is fueled by increased availability of next-generation consoles, expanding digital storefronts, and rising disposable incomes among middle-class consumers. The expansion of localized pricing strategies and installment-based purchasing options has made consoles more accessible to a broader demographic.

In Mexico, Sony and Microsoft have strengthened their presence through strategic partnerships with retailers and telecom providers, offering bundled deals. Additionally, the rise of e-sports tournaments and live streaming on platforms like Twitch has elevated interest in high-performance gaming experiences. As global publishers continue to localize content and offer flexible payment methods, console gaming is set to outpace other segments in terms of growth momentum across Latin America.

By Type Insights

Online gaming constituted the strongest segment in the Latin American gaming market, holding an estimated 63.2% of total revenue in 2024. This dominance is attributed to the increasing popularity of multiplayer and cloud-based games that facilitate social interaction and real-time competition.

Games such as Free Fire, Valorant, and League of Legends have cultivated large player bases, supported by regional e-sports leagues and live-streaming culture.

The proliferation of digital payment systems and improved broadband access has enabled seamless transactions and uninterrupted gameplay, encouraging sustained participation.

Argentina has also witnessed a surge in online gaming activity, particularly among teenagers and young adults. With ongoing investments in cloud infrastructure, mobile data plans, and competitive gaming events, online gaming remains the most dynamic and lucrative segment of the Latin American gaming landscape.

Offline gaming is experiencing steady growth within the Latin American gaming market, projected to expand at a CAGR of 6.8% in the coming years, despite the development of online formats. This growth is driven by persistent limitations in internet access across rural areas and the enduring appeal of single-player narrative-driven experiences. As a result, offline-capable games remain highly relevant, especially among budget-conscious consumers who prefer locally stored content.

Mexico has also seen a resurgence in interest in retro-style and story-focused games that do not require constant internet access. While online gaming continues to dominate, offline formats provide essential accessibility and flexibility, ensuring their relevance and growth in underserved markets across Latin America.

COUNTRY-LEVEL ANALYSIS

Brazil Gaming Market Analysis

Brazil prevailed in the American gaming market, accounting for 38.4% in 2024. As the region’s most populous country and economic powerhouse, Brazil drives significant demand across mobile, console, and online gaming segments.

The country’s digital payment ecosystem has matured rapidly, facilitating microtransactions and subscriptions. Also, electronic payments in the gaming industry have grown in recent years, supporting both domestic and international game developers. Furthermore, Brazil has become a hub for e-sports and game development. With robust consumer engagement and evolving digital infrastructure, Brazil remains the dominant force in the Latin American gaming landscape.

Mexico Gaming Market Analysis

Mexico is another key contributor to the Latin American gaming market. The country benefits from a large, tech-savvy youth population and a well-developed digital economy that supports diverse gaming formats. Also, the popularity of battle royale and role-playing games has surged, particularly among teens and young adults.

The Mexican government has taken steps to promote digital literacy and internet access, which has benefited online gaming adoption. Additionally, Mexico has emerged as a key market for international game publishers. Companies like Electronic Arts and Ubisoft have localized marketing campaigns and introduced installment-based payment options to cater to Mexican consumers, as noted by Newzoo. With a growing middle class and increasing investment in gaming infrastructure, Mexico is poised to maintain its strong position in the Latin American gaming sector.

Argentina Gaming Market Analysis

Argentina is emerging as a strategically important player due to its high internet penetration rate and a youthful, digitally engaged population.

Despite economic instability, gaming remains a popular form of entertainment, particularly among teenagers and young adults. Mobile gaming dominates the Argentine market, aided by the widespread use of smartphones. Local game development is also gaining traction. Although currency fluctuations and import restrictions pose challenges, Argentina’s strong digital culture positions it as a growing force in the regional gaming industry.

Chile Gaming Market Analysis

Chile is serving as a strategic growth hub due to its stable economy, advanced digital infrastructure, and early adoption of new technologies. This digital readiness has attracted international publishers looking to test new business models.

The country has also invested in supporting local game developers. E-sports is gaining institutional support, with universities incorporating competitive gaming into extracurricular programs. With a favorable regulatory environment and strong consumer interest, Chile is positioned to play a pivotal role in the evolution of the Latin American gaming ecosystem.

Rest of Latin America

The Rest of Latin America markets exhibit varied growth patterns influenced by economic conditions, internet access, and cultural preferences.

In Colombia, the government has actively promoted digital entrepreneurship, leading to a rise in local game development studios. Peru is focusing on expanding its mobile gaming base, with telecom operators offering data plans tailored for digital entertainment. Meanwhile, Central American nations like Costa Rica and Panama are leveraging bilingual education and outsourcing opportunities to attract international game development talent and outsourcing contracts. Collectively, these countries present significant untapped potential for future expansion in the Latin American gaming sector, particularly in mobile-first and indie game development.

COMPETITIVE LANDSCAPE

The Latin American gaming market is highly dynamic and increasingly competitive, shaped by a mix of global giants, regional developers, and emerging digital-native studios. International companies such as Electronic Arts, Microsoft, and Sea Limited have established strong footholds by leveraging their global resources, while simultaneously adapting to local conditions to gain consumer trust and loyalty. At the same time, local developers are gaining traction by creating culturally relevant content that resonates with domestic audiences and often finds success internationally.

Competition extends beyond product offerings to include platform accessibility, pricing models, and digital infrastructure integration. Companies must navigate diverse regulatory environments, economic disparities, and uneven internet penetration to maintain growth. E-sports and live streaming are also intensifying competition, as brands seek to engage younger demographics through influencer partnerships and event sponsorships. As mobile and cloud gaming continue to evolve, the race to innovate and capture market share is pushing companies toward deeper localization, strategic alliances, and investments in digital ecosystems tailored specifically to Latin American consumers.

KEY MARKET PLAYERS

These are the market players that are dominating the Latin American gaming market.

- Activision Blizzard, Inc.

- Apple, Inc

- Sea Limited (Garena/Free Fire)

- The Walt Disney Company

- Electronic Arts, Inc.

- Microsoft Corporation

- Nintendo Co., Ltd

- Rovio Entertainment Corporation

- Sega Enterprises, Inc.

- Sony Corporation

- Tencent Holdings Ltd

Top Players In The Market

- Electronic Arts has established a strong presence in the Latin American gaming market by tailoring its global franchises to regional preferences and expanding digital distribution channels. The company focuses on engaging local communities through localized content, language support, and mobile-first adaptations of popular titles such as FIFA Mobile. EA also collaborates with telecom providers to offer game bundles and promotions that increase accessibility for cost-conscious consumers. Its investment in regional marketing campaigns and partnerships with e-sports leagues has strengthened its brand recognition and user base across countries like Brazil and Mexico.

- Sea Limited is a dominant force in the Latin American gaming landscape, primarily through its battle royale title Free Fire, which has achieved massive popularity among mobile gamers. The company leverages aggressive localization strategies, including in-game events tied to regional festivals and collaborations with local influencers. Sea has also invested in community-driven initiatives and competitive e-sports circuits to sustain player engagement. By offering low-spec compatibility and microtransaction models suited to emerging markets, the company has secured a loyal user base across Latin America, making it one of the most influential international players in the region.

- Microsoft plays a critical role in shaping the console and cloud gaming segments in Latin America through its Xbox ecosystem and subscription-based services like Xbox Game Pass. Despite relatively high hardware costs, Microsoft has focused on making gaming more accessible via cloud streaming and flexible payment plans. The company partners with local retailers and internet service providers to bundle subscriptions and promote digital adoption. Microsoft’s commitment to expanding cloud infrastructure and supporting indie developers from the region has helped it build a growing consumer base, particularly in urban centers where broadband access is improving.

Top Strategies Used by Key Market Participants

- One of the primary strategies employed by key players in the Latin American gaming market is localized content development and marketing, where companies tailor games, promotional campaigns, and in-app purchases to reflect regional languages, cultural themes, and consumer behavior. This approach enhances relatability and engagement, especially among younger audiences who value representation and relevance.

- Another crucial strategy is strategic pricing and flexible payment models, which allow companies to cater to a diverse economic landscape. Given the varying purchasing power across Latin American countries, publishers offer tiered pricing, installment-based purchases, and carrier billing options to ensure affordability and reduce barriers to entry for new users.

- Lastly, expanding digital distribution and cloud-based platforms has become central to maintaining a competitive advantage. Companies are investing in cloud gaming, app store optimization, and partnerships with telecom operators to improve accessibility and reach broader audiences, especially in regions where physical retail and high-end hardware remain limited.

RECENT MARKET NEWS

- In March 2024, Electronic Arts launched a localized version of FIFA Mobile tailored specifically for Latin American audiences, featuring regional football leagues, teams, and in-game promotions aligned with local tournaments.

- In June 2024, Sea Limited expanded its esports initiative in Brazil by sponsoring the Free Fire Continental Cup, aiming to deepen its engagement with the region’s competitive gaming community and boost viewership on streaming platforms.

- In August 2024, Microsoft partnered with a major Brazilian telecom provider to offer bundled Xbox Game Pass subscriptions with mobile data plans, enhancing accessibility for cloud gaming in areas with limited fixed broadband infrastructure.

- In October 2024, Ubisoft announced the opening of a new regional customer support and localization center in Mexico City, aimed at improving player experience and accelerating game translations and updates for Spanish-speaking users.

- In December 2024, Google collaborated with Chilean indie developers to launch a dedicated "Made in Latin America" showcase on the Play Store, promoting homegrown talent and increasing visibility for local game studios on a global scale.

MARKET SEGMENTATION

This research report on the Latin American gaming market is segmented and sub-segmented into the following categories.

By Device

- Console

- Mobile

- Computer

By Type

- Online

- Offline

By Country

- Brazil

- Mexico

- Argentina

- Colombia

- Chile

- Others