Global Medical Aesthetic Devices Market Size, Share, Trends & Growth Forecast Report By Product Type (Energy-Based Devices, Implants and Anti-wrinkle Products), Procedures (Cosmetic Procedures and Reconstruction Procedures), End Users & Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) - Industry Analysis (2025 to 2033)

Global Medical Aesthetic Devices Market Summary

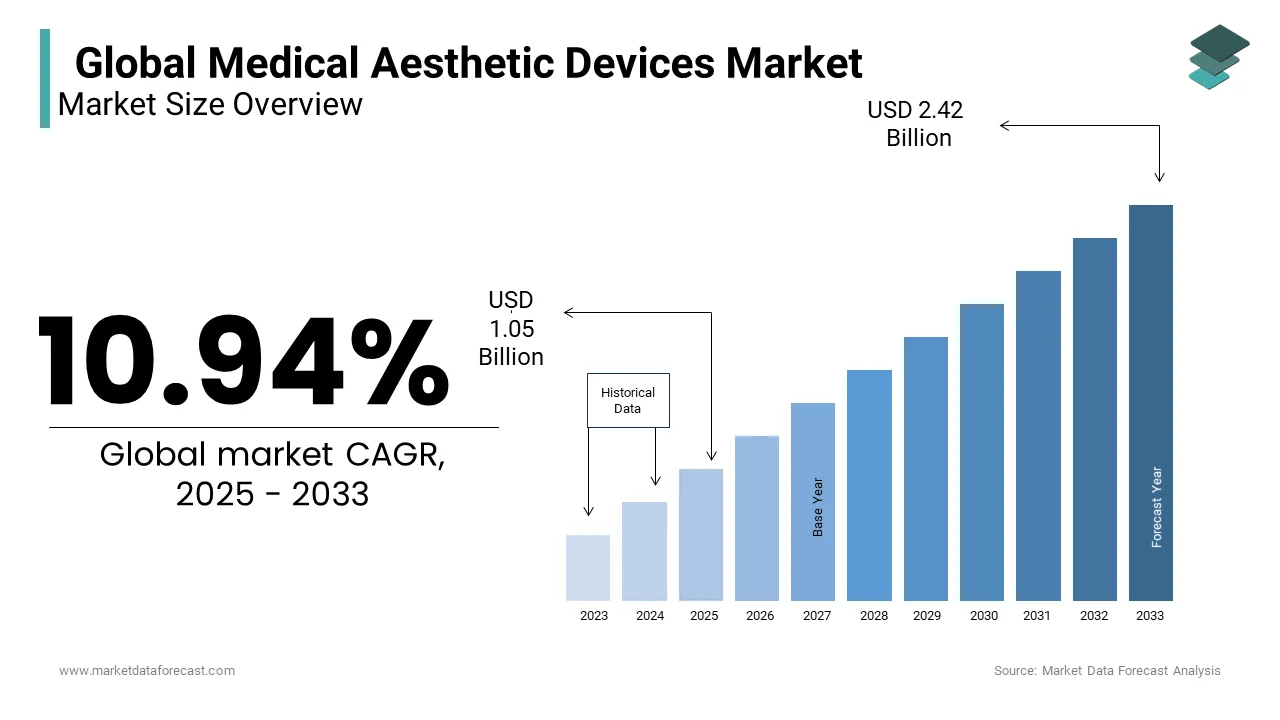

The Global Medical Aesthetic Devices size was valued at USD 0.95 billion in 2024 and is anticipated to reach USD 2.42 billion by 2033, growing at a CAGR of 10.94% from 2024 to 2033. The market is gaining momentum due to the rising demand for remote cardiac care, the growing burden of cardiovascular diseases, and technological advancements in AI-powered diagnostics and wearable cardiac monitoring devices.

Key Market Trends & Insights

- Global dominated the global market with a largest share in 2024.

- Global is projected to grow at the fastest rate between 2024 and 2033.

- Based on technology, the IT services segment is the fastest-growing with a projected CAGR of 10.94%.

- AI and wearable tech adoption are key trends driving innovation in the market.

Market Size & Forecast

- 2024 Market Size: USD 0.95 Billion

- 2033 Projected Market Size: USD 2.42 Billion

- CAGR (2024–2033): 10.94%

- Global: Largest market in 2024

- Global: Fastest-growing region

Global Medical Aesthetic Devices Market Size

The global medical aesthetic devices market size was valued at USD 0.95 billion in 2024. The market size is expected to have a 10.94% CAGR from 2025 to 2033 and be worth USD 2.42 billion by 2033 from USD 1.05 billion in 2025.

Medical Aesthetic Devices refers to a class of technologically advanced, non-invasive or minimally invasive medical instruments designed to enhance physical appearance through dermatological, facial, and body contouring treatments. These devices operate under clinical supervision and include laser and intense pulsed light (IPL) systems, radiofrequency (RF) devices, ultrasound-based body sculpting tools, microneedling platforms, and cryolipolysis equipment. Unlike cosmetic products, medical aesthetic devices are subject to regulatory scrutiny by health authorities such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA), ensuring safety and efficacy. The sector has evolved beyond traditional surgical interventions, with increasing consumer preference for outpatient procedures that offer minimal downtime.

The integration of AI-driven diagnostics and real-time skin analysis in next-generation devices is further enhancing treatment precision. As societal emphasis on appearance intensifies across both genders and age groups, medical aesthetic devices are becoming integral components of preventive and corrective dermatological care, blurring the lines between wellness and cosmetic enhancement.

MARKET DRIVERS

Rising Consumer Demand for Non-Surgical Facial Rejuvenation

The escalating demand for non-surgical facial treatments that address aging signs without prolonged recovery periods is a pivotal force propelling the medical aesthetic devices market. Consumers are increasingly opting for procedures such as laser resurfacing, radiofrequency tightening, and IPL-based photorejuvenation to combat wrinkles, pigmentation, and loss of skin elasticity. This surge is fueled by the growing visibility of dermatological wellness in mainstream media and the normalization of aesthetic care among younger demographics. Furthermore, technological advancements have improved treatment safety and comfort; devices like the Fraxel Dual and Cutera’s Titan utilize fractional laser and bulk heating mechanisms to stimulate collagen with minimal epidermal injury. The integration of real-time thermal monitoring and automated energy calibration has reduced adverse events, enhancing patient confidence. As urban populations face increased exposure to pollution and UV radiation, exacerbating skin aging, the demand for clinically validated, low-downtime facial rejuvenation solutions continues to expand, positioning non-surgical devices at the forefront of aesthetic innovation.

Expanding Access To Aesthetic Treatments In Emerging Economies

The proliferation of medical aesthetic services in developing regions is a critical growth catalyst, driven by rising disposable incomes, urbanization, and the globalization of beauty standards. In countries such as India, Brazil, and Indonesia, a growing middle class is increasingly investing in personal appearance, viewing aesthetic treatments as accessible markers of success and self-care. Also, the number of dermatology and aesthetic clinics in Southeast Asia increased between 2018 and 2023, with Jakarta, Bangkok, and Manila witnessing the most rapid expansion. In India, the number of trained aesthetic physicians has risen in recent years. This expansion is supported by government initiatives to regulate and professionalize the sector, including certification programs for non-physician practitioners. Additionally, device manufacturers are launching cost-optimized models tailored for price-sensitive markets; for instance, Alma Lasers introduced a compact RF platform priced lower than its premium variant to penetrate tier-2 cities in Latin America and South Asia. The rise of medical tourism further amplifies demand. These dynamics are transforming medical aesthetic devices from luxury interventions into increasingly democratized health and wellness services.

MARKET RESTRAINTS

Stringent Regulatory Pathways and Device Approval Delays

The medical aesthetic devices market faces significant constraints due to rigorous regulatory frameworks that govern device safety, efficacy, and marketing claims. In the United States, the FDA requires premarket approval (PMA) or 510(k) clearance for most aesthetic devices, a process that can take several months and incur substantial compliance costs. Similar delays occur in Europe under the Medical Device Regulation (MDR), where the transition from legacy CE marking to stricter conformity assessments has led to a backlog in device approvals. These regulatory hurdles slow market entry, particularly for small and mid-sized innovators lacking extensive compliance infrastructure. Additionally, inconsistent standards across regions complicate global commercialization; for example, China’s National Medical Products Administration mandates local clinical trials for foreign devices, increasing time-to-market by multiple months. The European Commission also enforces strict advertising guidelines, penalizing unsubstantiated claims about skin tightening or fat reduction. As a result, manufacturers must invest heavily in legal and regulatory affairs, diverting resources from R&D and limiting the pace of innovation. These systemic delays hinder the rapid deployment of next-generation aesthetic technologies, constraining market agility.

High Incidence of Adverse Events from Inadequate Practitioner Training

The rising number of complications stemming from improper device usage by inadequately trained personnel is a critical impediment to the sustainable growth of the medical aesthetic devices market. Despite the clinical nature of these technologies, many procedures are administered by non-physicians, including nurses, aestheticians, and technicians, who may lack a comprehensive understanding of skin physiology and laser-tissue interaction. In countries like Turkey and Mexico, where aesthetic tourism is prevalent, unregulated clinics often employ uncertified staff to reduce operational costs, further escalating risks. This regulatory fragmentation undermines patient safety and erodes public trust in non-surgical treatments. Consequently, insurers are increasingly reluctant to cover complications from aesthetic procedures, and malpractice claims are on the rise. Until standardized training and certification become universal, the risk of adverse outcomes will continue to act as a brake on market expansion and consumer confidence.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Skin Diagnostics and Treatment Personalization

The incorporation of artificial intelligence (AI) into medical aesthetic devices presents a transformative opportunity to enhance diagnostic accuracy and deliver personalized treatment protocols. AI-powered imaging systems can analyze skin texture, pigmentation, pore size, and hydration levels with micron-level precision, enabling clinicians to develop data-driven intervention plans. For instance, Canfield Scientific’s VISIA-CR system uses machine learning algorithms to assess up to 14 skin conditions, providing quantifiable baselines for tracking treatment efficacy. Furthermore, AI enables adaptive energy delivery; devices like Lumenis’ LightSheer Duet utilize real-time feedback to modulate laser intensity based on skin response, minimizing the risk of over-treatment. Startups such as Neutrogena (under Kenvue) have launched AI-driven mobile apps that sync with handheld devices for at-home skin analysis, creating a bridge between consumer and clinical ecosystems. As AI becomes more embedded in aesthetic workflows, it will not only improve clinical outcomes but also streamline patient consultations, reduce operator dependency, and support remote monitoring, ushering in a new era of precision aesthetics.

Expansion of At-Home Medical-Grade Aesthetic Devices

The emergence of FDA-cleared, at-home medical aesthetic devices is unlocking a new consumer segment seeking professional-grade results without clinical visits. Enabled by miniaturization, wireless connectivity, and improved safety mechanisms, these devices offer treatments such as microcurrent facial toning, red and blue light therapy, and low-level laser therapy for hair growth. The pandemic accelerated this trend. Moreover, subscription-based models and telehealth integration allow users to receive remote guidance from dermatologists, enhancing safety and adherence. As regulatory bodies adapt to classify certain low-risk devices for consumer use, and as AI and IoT enhance monitoring capabilities, the boundary between clinical and domestic aesthetics is dissolving, creating a scalable, high-margin avenue for device manufacturers.

MARKET CHALLENGES

Escalating Cybersecurity Risks in Connected Aesthetic Devices

As medical aesthetic devices become increasingly connected through IoT and cloud-based platforms, they are exposed to growing cybersecurity vulnerabilities that threaten patient data and device functionality. Modern systems often store sensitive biometric data such as facial scans, skin condition histories, and treatment parameters on networked servers, making them potential targets for cyberattacks. In the USA, medical device-related cyber incidents increased between 2021 and 2023, with aesthetic devices included in the expanding attack surface. The European Agency for Cybersecurity warns that many aesthetic clinics lack robust IT infrastructure, relying on outdated software and unencrypted data transmission. Furthermore, the integration of mobile apps and wearable interfaces amplifies exposure. As device connectivity becomes standard, manufacturers must invest in secure firmware, regular updates, and compliance with standards like IEC 62304. However, balancing usability with security remains a challenge, particularly in decentralized clinical environments where IT support is limited.

Growing Consumer Skepticism Due to Misleading Marketing Claims

The medical aesthetic devices market is increasingly confronting consumer skepticism fueled by exaggerated efficacy claims and ambiguous labeling, particularly in the at-home and direct-to-consumer segments. Many manufacturers market devices with terms like “dermatologist-approved” or “laser clinic results,” which, while not outright false, often lack context or comparative clinical validation. The erosion of trust is compounded by social media influencers promoting devices without disclosing financial ties or clinical limitations. Regulatory bodies are responding with stricter guidelines. However, enforcement remains inconsistent, especially in digital spaces. To regain credibility, manufacturers must adopt transparent communication, publish peer-reviewed outcomes, and align marketing with clinical evidence, a shift that demands cultural and operational change across the industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product Type, Procedure, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Allergan, Cynosure, Johnson & Johnson, LCA Pharmaceutical, Galderma Pharma, Solta Medical, Cutera, Focus Medical, Human Med Ag, Genzyme Corporation, Alcon Inc., and Alma Lasers. |

SEGMENTAL ANALYSIS

By Product Type Insights

The energy-based devices segment dominated the medical aesthetic devices market by capturing 65.4% of global revenue in 2024. This preeminence is anchored in the versatility, non-invasiveness, and clinical efficacy of technologies such as lasers, radiofrequency (RF), intense pulsed light (IPL), and ultrasound systems. A primary driver of this segment’s leadership is the escalating demand for skin resurfacing and pigmentation correction, particularly in aging populations exposed to environmental stressors. Additionally, advancements in fractional and hybrid laser platforms, such as the Fraxel Dual and Halo, have significantly improved safety profiles, reducing downtime and expanding eligibility to diverse skin types. The integration of real-time thermal feedback and automated energy modulation has further enhanced treatment precision, minimizing operator dependency. Moreover, energy-based devices are increasingly used for body contouring, with cryolipolysis and RF-assisted lipolysis gaining traction. These converging clinical, technological, and demographic forces solidify energy-based devices as the cornerstone of modern aesthetic practice.

The anti-wrinkle products segment is emerging as the fastest-growing within the medical aesthetic devices market and is projected to expand at a CAGR of 12.4% from 2025 to 2033. This surge is driven by the rising popularity of neuromodulators such as botulinum toxin (Botox, Dysport) and dermal fillers, which are increasingly administered in outpatient clinics and medspas. A key factor is the shift toward preventive aesthetics, with younger consumers initiating treatments in their mid-20s to delay visible aging. Besides, the normalization of injectables in mainstream culture, amplified by social media and celebrity endorsements, has reduced stigma and increased accessibility. Furthermore, the development of longer-lasting formulations, such as Daxxify, which offers up to six months of efficacy, has improved patient compliance and reduced treatment frequency. The expansion of trained non-physician providers, including nurse practitioners and physician assistants, has also broadened service availability, particularly in North America and Western Europe.

By Procedures Insights

The cosmetic procedures segment accounted for a substantial share of the global medical aesthetic devices market by procedure volume in 2024. This overwhelming dominance is driven by the widespread consumer pursuit of appearance enhancement, particularly in facial aesthetics, skin texture improvement, and body contouring. The demand is especially pronounced among women, who constitute a significant share of all cosmetic interventions globally. A major contributing factor is the growing influence of digital self-presentation, where social media platforms like Instagram and TikTok amplify appearance scrutiny. Additionally, the proliferation of minimally invasive treatments, such as chemical peels, laser hair removal, and dermal fillers, has lowered barriers to entry. The expansion of medspas in urban centers, offering flexible pricing and shorter appointment durations, has further democratized access. These socio-cultural, technological, and infrastructural dynamics collectively sustain the overwhelming dominance of cosmetic procedures in the aesthetic landscape.

The reconstruction procedures segment is registering the highest growth within the medical aesthetic devices market, with a projected CAGR of 9.8% in the coming years. This acceleration is fueled by increasing demand for post-oncological, post-traumatic, and congenital defect repair, particularly in breast reconstruction and facial restoration. A pivotal driver is the rising incidence of mastectomies due to breast cancer, which affects a significant number of women annually worldwide. In the United States, the Women’s Health and Cancer Rights Act mandates insurance coverage for breast reconstruction, contributing to an increase in reconstructive procedures between 2018 and 2023. Additionally, advancements in tissue engineering and fat grafting, supported by energy-based devices for skin tightening and scar remodelling, have enhanced outcomes and patient satisfaction. The integration of 3D imaging and AI-driven surgical planning has further improved precision in facial and craniofacial reconstruction. Moreover, growing psychological recognition of appearance-related trauma has led to greater acceptance of reconstructive interventions as essential healthcare. These medical, legislative, and psychosocial factors are transforming reconstruction from a niche specialty into a rapidly expanding segment of aesthetic medicine.

By End-User Insights

The clinics and beauty centers segment is anticipated to account for a dominating share of the global market during the forecast period and grow at a high pace due to a rise in the number of clinics and medical spas, increasing investments for providing better infrastructure and resources in hospitals, and the availability of skilled professionals. In addition, trained staff to operate aesthetic procedures increased the adoption rate of technologically advanced devices.

However, the home use segment is expected to witness growth during the forecast period due to the increasing interest in home care services, especially after the pandemic. As a result, more people are now opting for the comfort of having services provided to them at home.

REGIONAL ANALYSIS

North America Medical Aesthetic Devices Market Insights

North America led the global medical aesthetic devices market by accounting for 34.3% of total revenue in 2024. The region’s growth is underpinned by a highly developed healthcare infrastructure, widespread insurance coverage for certain reconstructive procedures, and a deeply ingrained culture of aesthetic enhancement. A key driver is the high concentration of FDA-approved devices and certified practitioners, with a large number of dermatologists and plastic surgeons actively offering aesthetic treatments. The proliferation of medspas and the integration of aesthetic care into primary dermatology practices have expanded access beyond urban elites. Additionally, technological innovation is centered in the U.S., with companies like Cutera, Solta Medical, and Cynosure leading in laser and energy-based device development. The rise of tele-aesthetics, where consultations and follow-ups are conducted remotely, has further enhanced convenience. Despite high costs, consumer willingness to pay remains strong. These factors collectively position North America as the most mature and technologically advanced market for medical aesthetic devices.

Europe Medical Aesthetic Devices Market Insights

Europe holds a significant share of the global medical aesthetic devices market. The region’s market is characterized by a blend of medical rigor, regulatory sophistication, and evolving consumer behavior. Countries such as Germany, the UK, and France lead in clinical adoption. A major growth driver is the implementation of the EU Medical Device Regulation (MDR), which has enhanced device safety and traceability, increasing patient confidence. However, the transition has also delayed market entry for some manufacturers, creating a temporary supply gap that is now being resolved. Demand is particularly strong for non-invasive skin rejuvenation and body contouring. Additionally, the rise of medical tourism in Eastern Europe, especially in Hungary and Poland, offers cost-effective treatments without compromising quality. Public healthcare systems in Nordic countries are also beginning to cover reconstructive interventions, expanding access. With a strong emphasis on safety, ethics, and innovation, Europe remains a pivotal market for next-generation aesthetic technologies.

Asia-Pacific Medical Aesthetic Devices Market Insights

Asia-Pacific is the fastest-expanding region in the medical aesthetic devices market. The region’s ascent is driven by rapid urbanization, rising disposable incomes, and shifting beauty ideals influenced by K-beauty and J-beauty trends. South Korea, Japan, and China are at the forefront. A key factor is the cultural emphasis on flawless skin and facial symmetry, reinforced by the entertainment industries and social media. Technological adoption is accelerating, with AI-powered skin analyzers and robotic-assisted laser systems becoming standard in premium clinics. Additionally, government support in countries like Thailand and Malaysia for medical tourism has attracted a significant number of international patients. Local manufacturers such as WonTech and Lasulux are gaining global recognition for cost-effective, high-performance devices. With increasing regulatory harmonization under ASEAN frameworks and rising insurance coverage for reconstructive cases, APAC is transitioning from a price-sensitive market to a hub of innovation and high-volume clinical practice.

Latin America Medical Aesthetic Devices Market Insights

Latin America is reflecting a market defined by cultural enthusiasm and uneven access. Brazil stands as the regional leader, ranking second globally in total aesthetic procedures after the United States. The region’s demand is deeply rooted in sociocultural values that prioritize physical appearance, fitness, and youthfulness. In Brazil, aesthetic surgery is often viewed as a form of self-investment, with public figures and media personalities normalizing procedures from an early age. However, regulatory fragmentation remains a challenge; only a few Latin American countries have national licensing requirements for aesthetic practitioners. This has led to a proliferation of informal clinics, increasing the risk of complications. Despite this, formalization is underway. The rise of mobile clinics and teleconsultations is improving access in remote areas. Besides, medical tourism to Colombia and Costa Rica is growing, with patients from North America seeking lower-cost, high-quality care. These dynamics position Latin America as a high-potential, high-complexity market requiring balanced regulation and innovation.

Middle East and Africa Medical Aesthetic Devices Market Insights

The Middle East and Africa collectively account for a small share of the global medical aesthetic devices market in 2024, with growth concentrated in the Gulf Cooperation Council (GCC) nations. The UAE and Saudi Arabia are driving regional expansion, supported by high disposable incomes, government-backed healthcare modernization, and a youthful population. A key driver is the increasing participation of women in the workforce, leading to greater personal expenditure on appearance and wellness. In Saudi Arabia, Vision 2030 has spurred investments in private healthcare, including aesthetic centers, with the number of licensed clinics increasing between 2020 and 2023. Additionally, cultural shifts are normalizing male aesthetic treatments. In Africa, Nigeria and South Africa are emerging as regional hubs, with Lagos and Johannesburg hosting premium clinics catering to affluent clients. However, limited regulatory oversight and uneven device availability constrain scalability. With increasing digital health adoption and cross-border collaborations, MEA is evolving into a niche but strategically significant market for premium aesthetic technologies.

KEY MARKET PLAYERS

The global medical aesthetic devices market is highly fragmented, with many local players competing with international players. Some of the notable participants dominating the global medical aesthetic devices market are Allergan, Cynosure, Johnson & Johnson, LCA Pharmaceutical, Galderma Pharma, Solta Medical, Cutera, Focus Medical, Human Med Ag, Genzyme Corporation, Alcon Inc., and Alma Lasers.

TOP LEADING PLAYERS IN THE MEDICAL AESTHETIC DEVICES MARKET

Lumenis

Lumenis maintains a prominent position in the Asia Pacific medical aesthetic devices market through its legacy in laser and energy-based technologies. The company has established strong partnerships with dermatology clinics and medspas across South Korea, Japan, and Australia, emphasizing clinical education and hands-on training for practitioners. In 2023, Lumenis launched its next-generation M22™ platform with advanced OPT™ (Optimal Pulse Technology) in India and Southeast Asia, enhancing treatment precision for pigmentation and vascular lesions. It also expanded its regional service network by introducing remote diagnostics and AI-assisted calibration for its devices, improving uptime and performance. Collaborations with local distributors in Thailand and Indonesia have strengthened last-mile access, while participation in APAC-focused aesthetic conferences has reinforced brand authority. By aligning its innovations with regional skin type requirements, particularly Fitzpatrick types III to V, Lumenis has differentiated itself in a competitive landscape, ensuring sustained relevance among clinicians seeking reliable, high-efficacy solutions.

Candela Medical (a Solta Medical company)

Candela Medical has deepened its footprint in the Asia Pacific region by focusing on scientific validation and physician engagement in dermatological aesthetics. The company’s Vbeam pulsed dye laser and Alexandrite platforms are widely adopted in Japan, China, and Singapore for treating vascular and pigmented lesions, supported by extensive clinical data. In 2023, Candela introduced its GentleMax Pro with Dynamic Cooling Device (DCD) technology in tier-1 cities across India, tailored for darker skin tones with reduced risk of post-inflammatory hyperpigmentation. It also initiated a series of clinical training workshops in collaboration with the Japanese Dermatological Association to standardize treatment protocols. The launch of a cloud-based device management system enabled real-time monitoring and predictive maintenance, enhancing operational efficiency for clinics. Additionally, Candela bolstered its digital presence through localized webinars and virtual consultations, increasing accessibility for practitioners in remote areas. By combining technological precision with robust medical education, Candela has solidified its reputation as a trusted partner in evidence-based aesthetic care across diverse APAC markets.

Cutera

Cutera has intensified its presence in the Asia Pacific market by introducing compact, user-friendly aesthetic platforms tailored for high-volume clinical environments. The company’s flagship devices, including Enlighten III for tattoo removal and Excel HR for hair removal, have gained traction in South Korea, Australia, and Malaysia due to their dual-wavelength flexibility and safety on pigmented skin. In 2023, Cutera launched its xeo® platform with an updated Skintel™ Melanin Reader in Singapore and Hong Kong, enabling real-time melanin assessment to optimize laser settings and reduce adverse events. The company also established a regional training hub in Sydney, offering certification programs for dermatologists and aesthetic physicians. Strategic collaborations with local distributors in Indonesia and Vietnam have expanded market reach into emerging urban centers. Furthermore, Cutera integrated IoT-enabled analytics into its devices, allowing clinics to track treatment outcomes and device utilization. By prioritizing safety, adaptability, and data-driven performance, Cutera is positioning itself as a leader in intelligent, clinician-centric aesthetic solutions across the Asia Pacific region.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the medical aesthetic devices market are deploying a range of strategic initiatives to consolidate their positions, including technological innovation, geographic expansion, regulatory compliance enhancement, strategic partnerships, and direct-to-practitioner education. Companies are investing heavily in R&D to develop multi-application platforms that support diverse procedures using interchangeable handpieces, improving cost efficiency for clinics. Expansion into high-growth regions such as the Asia Pacific and Latin America is being accelerated through local distribution networks and regulatory filings tailored to national requirements. Firms are also strengthening compliance with evolving standards like the EU MDR and China’s NMPA regulations to ensure uninterrupted market access. Collaborations with dermatology associations and aesthetic academies are being leveraged to build clinical credibility and standardize treatment protocols. Additionally, manufacturers are enhancing post-sales support through remote monitoring, predictive maintenance, and cloud-based device management systems. The integration of AI for treatment personalization and outcome tracking is emerging as a differentiator. These strategies collectively enable companies to balance innovation, safety, and scalability in a highly regulated and competitive global landscape.

COMPETITION OVERVIEW

Competition in the medical aesthetic devices market is intensifying as global leaders, regional specialists, and technology-driven startups vie for clinical adoption and market influence. Established players such as Lumenis, Cutera, and Candela compete on technological sophistication, regulatory compliance, and clinical support, while newer entrants focus on affordability and ease of use for emerging markets. The battleground spans product versatility, treatment safety across diverse skin types, and integration with digital health ecosystems. Differentiation increasingly hinges on AI-driven diagnostics, real-time monitoring, and interoperability with electronic medical records. Regulatory agility is critical, as delays under frameworks like the EU MDR can cede advantage to faster-compliant rivals. In the Asia Pacific, local manufacturers are challenging multinationals with cost-optimized devices tailored to regional needs. Meanwhile, the rise of medspas and non-physician providers has shifted marketing focus toward training, service support, and workflow integration. Mergers, such as the acquisition of Solta Medical by Bausch Health, reflect consolidation aimed at expanding portfolio breadth. As consumer demand evolves from isolated treatments to holistic aesthetic journeys, competition is shifting from hardware alone to integrated solutions encompassing devices, data, and long-term patient engagement.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Lumenis launched its upgraded M22™ with OPT™ and HALO hybrid fractional technology in South Korea, enhancing treatment efficacy for photodamage and acne scarring while expanding its clinical applications in the premium dermatology segment.

- In April 2023, Candela Medical introduced the GentleMax Pro with Skintel™ Melanin Reader in India, enabling real-time melanin measurement to personalize laser settings and reduce complications in Fitzpatrick skin types IV–VI.

- In August 2023, Cutera established a clinical training and innovation center in Sydney, offering certified programs for dermatologists and aestheticians across the Asia Pacific region to standardize device usage and improve treatment outcomes.

- In November 2023, Solta Medical received CE Mark approval for its new TempSure Envi RF platform with enhanced applicators, facilitating broader adoption in European and Middle Eastern markets for non-invasive skin tightening.

- In April 2024, DynaTouch, a kiosk solutions provider, acquired KioWare, a kiosk management software company. This acquisition is anticipated to allow DynaTouch to offer more comprehensive kiosk solutions and strengthen its market presence.

MARKET SEGMENTATION

This research report on the global medical aesthetic devices market has been segmented and sub-segmented based on the product type, procedure, end-user, and region.

By Product Type

- Energy-Based Devices

- Aesthetic Laser Devices

- Body Contouring Devices

- Microdermabrasion

- Ultrasound

- Implants

- Anti-Wrinkle Products

- Botulinum toxin

- Dermal Fillers

- Chemical Peel

By Procedure

- Cosmetic Procedures

- Minimally Invasive

- Surgical Procedures

- Reconstruction Procedures

By End Users

- Home Use

- Clinics and Beauty Centers

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Which device types dominate the Global Medical Aesthetic Devices Market?

Key device segments in the Global Medical Aesthetic Devices Market include aesthetic laser devices, body contouring systems, facial aesthetic devices, energy-based instruments, and cosmetic implants, reflecting both innovation and patient demand.

2. Which region occupied major share of the global medical aesthetic devices market in 2024?

Geographically, the North American region accounted for the most significant share of the market in 2024.

3. Who are some of the notable players in the medical aesthetic devices market?

Allergan, Cynosure, Johnson & Johnson, LCA Pharmaceutical, Galderma Pharma, Solta Medical, Cutera, Focus Medical, and Human Med Ag, Genzyme Corporation, Alcon Inc., and Alma Lasers are some of the key players in the medical aesthetic devices market.

4. Which segment by product dominated the medical aesthetic devices market in 2024?

Based on the product, the anti-wrinkle product segment accounted for the major share of the market in 2024.

5. What role do body contouring devices play in the Global Medical Aesthetic Devices Market?

Body contouring devices are a large segment in the Global Medical Aesthetic Devices Market, providing non-surgical fat reduction, skin tightening, and cellulite treatment to meet rising demand for body sculpting solutions.

6. What are the main applications of products in the Global Medical Aesthetic Devices Market?

Products in the Global Medical Aesthetic Devices Market are used for facial and skin rejuvenation, body shaping, anti-aging, tattoo removal, scar reduction, and breast enhancement, covering a diverse array of aesthetic demands.

7. Who are the leading end users in the Global Medical Aesthetic Devices Market?

The leading end users of the Global Medical Aesthetic Devices Market are cosmetic centers, hospitals, dermatology clinics, and medical spas, each offering various non-invasive and surgical aesthetic treatments.

8. Which regions are leading in the Global Medical Aesthetic Devices Market?

Regions such as North America and Europe dominate the Global Medical Aesthetic Devices Market due to advanced healthcare infrastructures, high consumer spending, and early adoption of innovative aesthetic technologies.

9. How are minimally invasive devices impacting the Global Medical Aesthetic Devices Market?

Minimally invasive devices in the Global Medical Aesthetic Devices Market are expanding rapidly, offering reduced downtime, safer procedures, and greater patient satisfaction, fueling overall market growth

10. What key drivers are influencing growth in the Global Medical Aesthetic Devices Market?

Growth in the Global Medical Aesthetic Devices Market is driven by aging populations, rising consumer awareness, influence of beauty standards via social media, and the demand for non-surgical cosmetic solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com