Middle East And Africa Non-Alcoholic Beverage Market Research Report Segmented By Product Type (Soft Drinks, Bottled Water, Tea & Coffee, Juice, Dairy Drinks), Distribution Channel (Specialty Stores, Online Store , Super Markets/ Hyper Markets, Convenience Stores, Departmental Stores And Others), And Country (KSA, UAE, Israel, Rest Of GCC Countries) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Middle East and Africa Non-Alcoholic Beverage Market Size

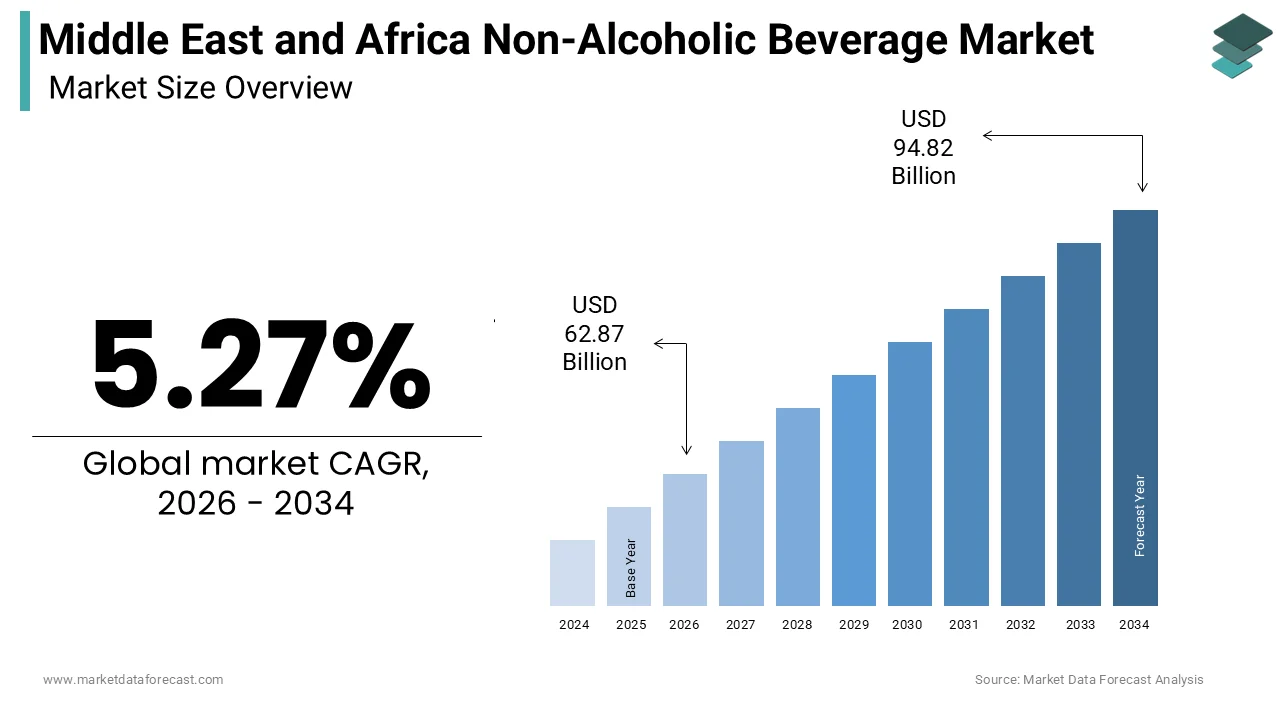

The size of the Middle East and Africa non-alcoholic beverage market was calculated to be USD 59.72 billion in 2025 and is anticipated to be worth USD 94.82 billion by 2034 from USD 62.87 billion in 2026, growing at a CAGR of 5.27% during the forecast period.

A non-alcoholic beverage is any drink that contains no alcohol or has an alcohol level below 0.5% alcohol by volume (ABV). This market is deeply intertwined with the social fabric and climatic realities of the region, where hydration and social hospitality are paramount cultural values. In many Middle Eastern countries, religious prohibitions against alcohol consumption further cement the dominance of non alcoholic alternatives in social and commercial settings. The market operates within a diverse economic landscape ranging from high-income Gulf Cooperation Council nations to emerging economies in Sub-Saharan Africa. According to the World Health Organization, individual water requirements rise significantly in hot climates, where a minimum of 7.5 liters per person per day is recommended to meet basic hydration, survival, and hygiene needs. The Food and Agriculture Organization regional reports emphasize that North Africa remains a critical zone for high-value crop cultivation, though agricultural expansion faces severe constraints due to rising groundwater depletion and climate-driven water scarcity. Furthermore, according to tracking data from the International Coffee Organization, coffee consumption in the Middle East is projected to grow by approximately 4% annually, fueled by an expanding demographic of younger consumers and a strong preference for premium coffee experiences. The market is characterized by a mix of multinational corporations and local producers who cater to distinct regional tastes, such as date-based drinks and hibiscus infusions. Urbanization and rising disposable incomes are reshaping consumption patterns, moving consumers from traditional homemade beverages to branded, packaged options. This transition highlights the market's evolution from a basic necessity to a lifestyle-oriented industry focused on health, convenience, and variety.

MARKET DRIVERS

Rapid Urbanization and Changing Lifestyles Fuel Convenience Demand

Rapid urbanization is propelling the growth of the Middle East and Africa non alcoholic beverage market. This shift fundamentally alters consumer lifestyles and purchasing behaviors. As populations migrate from rural areas to cities, there is a marked shift away from traditional home-prepared beverages towards convenient, ready-to-drink options. According to projections from the United Nations Department of Economic and Social Affairs, roughly 60% of Africa's population will live in urban areas by 2050, building an increasingly dense market for consumer packaged goods. In the Middle East, urbanization rates are exceptionally high, reaching approximately 85% in Saudi Arabia and 88% in the United Arab Emirates, which heavily supports a lifestyle centered on on-the-go consumption. The fast-paced nature of urban life increases the demand for portable hydration solutions such as bottled water, energy drinks, and single-serve juices. World Bank economic analyses indicate that urbanization and long-term demographic shifts in Sub-Saharan Africa are gradually expanding consumer markets, driving diverse growth in spending on commercial beverages. The proliferation of modern retail formats such as supermarkets and convenience stores in urban centers enhances product accessibility. Additionally, the rise of office culture and corporate environments in cities like Lagos, Cairo, and Dubai drives the consumption of coffee and tea during work hours. This demographic shift necessitates efficient distribution networks that can deliver fresh beverages to dense urban populations. Thus, beverage manufacturers are focusing their marketing and logistics efforts on metropolitan hubs to capture this growing segment of convenience-oriented consumers.

Health Consciousness and Demand for Functional Beverages

Increasing health consciousness among consumers further contributes to the expansion of the Middle East and Africa non alcoholic beverages market. This is significantly driving the demand for functional and healthier non alcoholic beverages. There is a growing awareness of the adverse effects of high sugar intake, leading to a preference for low-calorie, natural, and fortified drinks. According to data from the International Diabetes Federation, the Middle East and North Africa region records the highest adult diabetes prevalence globally, affecting approximately 16.2% of the adult population. This health crisis has prompted governments and healthcare providers to advocate for reduced sugar consumption, influencing consumer choices. Data from the Global Nutrition Report reveals a major public health challenge in South Africa, where over 41% of adult women live with obesity, helping accelerate a consumer shift toward low-sugar and healthier food and beverage alternatives. Consumers are increasingly seeking drinks enriched with vitamins, minerals, and probiotics that offer additional health benefits beyond hydration. The demand for natural fruit juices without added sugars has surged. Furthermore, the popularity of herbal and traditional remedies such as ginger and turmeric-infused drinks is rising due to their perceived immune-boosting properties. Retailers are responding by expanding their shelves with organic and clean-label products. This trend is supported by aggressive marketing campaigns that highlight nutritional benefits and natural ingredients. The convergence of health awareness and product innovation creates a robust environment for the growth of functional beverages in the region.

MARKET RESTRAINTS

High Sugar Taxation and Regulatory Pressures

The implementation of high sugar taxes and stringent regulatory frameworks is hampering the growth of the Middle East and Africa non alcoholic beverage market. This trend is particularly visible in the carbonated soft drinks and high sugar juices segments. Governments in the region are increasingly adopting fiscal policies to combat rising rates of obesity and diabetes, which directly impact the pricing and profitability of sugary beverages. Under multilateral agreements signed by member states of the Gulf Cooperation Council, a 50% selective tax was enacted on carbonated beverages and 100% on energy drinks, notably shifting retail prices to discourage high-sugar intake. Published economic research indicates that after Saudi Arabia applied its initial 50% excise tax alongside VAT, per capita volume sales of carbonated soda fell by roughly 35% to 41%. Similar measures are being considered or implemented in other African nations, such as South Africa, which introduced a health promotion levy on sugary beverages. These regulatory pressures force manufacturers to reformulate their products to reduce sugar content, which involves substantial research and development costs. Additionally, strict labeling requirements mandate clear disclosure of nutritional information, which can deter health-conscious consumers from purchasing high-sugar items. The compliance burden associated with these regulations increases operational complexity for beverage companies. These policies aim to improve public health. However, they create short-term financial challenges for industry players who must navigate price sensitivity and changing consumer preferences in a highly regulated environment.

Supply Chain Infrastructure Deficiencies in Sub-Saharan Africa

Inadequate supply chain infrastructure in many Sub-Saharan African countries is a major barrier to the efficient distribution and availability of these beverages, and thereby negatively impacts the expansion of the Middle East and Africa non-alcoholic beverages market. The region faces significant challenges related to poor road networks, unreliable electricity supply, and limited cold chain facilities, which hinder the transportation and storage of perishable beverage products. Historical studies tracked by the African Development Bank have highlighted that limited rural access to all-season roads presents long-standing challenges for regional last-mile product distribution. The lack of consistent refrigeration infrastructure leads to high spoilage rates for fresh juices and dairy-based drinks, limiting their market reach to urban centers with better facilities. Data from the World Logistics Performance Index indicates that several African countries rank low in logistics efficiency, resulting in higher transportation costs and longer delivery times. Power outages are frequent in nations like Nigeria and Kenya, disrupting production schedules and compromising product quality in retail outlets. These infrastructural deficits increase the overall cost of doing business, forcing companies to invest heavily in private logistics solutions such as generator-powered cold storage and proprietary fleet management. The high capital expenditure required to overcome these barriers limits the ability of smaller players to enter the market and restricts the expansion of larger firms into rural areas. Thus, the potential market size remains underutilized due to logistical bottlenecks that prevent consistent product availability and affordability in remote regions.

MARKET OPPORTUNITIES

Expansion of Local Fruit Processing and Indigenous Flavors

The vast availability of diverse tropical fruits in the region unlocks potential for the development of locally sourced and indigenous flavored beverages, which is likely to promote the growth of the Middle East and Africa non alcoholic beverages market. The region is rich in unique fruits such as dates, baobab, hibiscus, tamarind, and moringa, which are increasingly being utilized to create distinctive beverage products that appeal to both local and international consumers. According to FAO statistical databases, Africa produces over 100 million tons of fruit annually, though substantial volumes are lost post-harvest due to limited industrial agro-processing and cold-storage capacity. Investing in local processing facilities allows companies to reduce reliance on imported concentrates and lower production costs. Strategic frameworks from the African Union emphasize that expanding the continent's agro-processing sector can add over 100 billion dollars in economic value by accelerating local manufacturing and lowering dependency on food imports. Consumers are showing a growing preference for authentic, traditional flavors that reflect their cultural heritage, driving demand for beverages made from native ingredients. Traditional hibiscus tea, widely known as Karkade in Egypt and Sudan, remains a culturally dominant, antioxidant-rich beverage deeply integrated into regional daily diets. Companies that innovate with these indigenous ingredients can differentiate their brands in a crowded market. Furthermore, exporting these unique flavors to global markets offers an additional revenue stream. Beverage manufacturers can support rural farmers and enhance their sustainability credentials by leveraging local agricultural resources. Doing so creates a competitive advantage through product uniqueness and cultural relevance.

Growth of E-Commerce and Digital Retail Channels

The rapid growth of e-commerce and digital retail channels offers a significant opportunity for beverage companies to expand their reach and engage directly with consumers in the region, which paves the way for the expansion of the Middle East and Africa non alcoholic beverage market. The increasing penetration of smartphones and internet connectivity is transforming how consumers discover and purchase beverages, bypassing traditional retail limitations. Moreover, the International Telecommunication Union indicates that internet penetration in Africa has expanded toward 47%, while mobile financial networks independently streamline digital consumer transactions. Beverage brands are leveraging online platforms to offer subscription services, bulk purchases, and exclusive product launches, enhancing customer loyalty and convenience. Digital marketing allows for targeted advertising based on consumer preferences and behavior, improving conversion rates. The rise of quick commerce apps that deliver groceries within minutes is particularly beneficial for impulse purchases of cold beverages. Consumer data shows that digital grocery channels in the Middle East continue to scale up rapidly, driven by urban consumer preferences for quick commerce and delivery apps. By integrating with these digital ecosystems, beverage companies can gather valuable consumer data to inform product development and inventory management. Additionally, e-commerce enables smaller niche brands to reach a wider audience without the need for extensive physical distribution networks. This digital transformation opens new avenues for growth and customer engagement in the non alcoholic beverage sector.

MARKET CHALLENGES

Water Scarcity and Environmental Sustainability Concerns

Water scarcity and increasing environmental sustainability concerns are critical challenges to the Middle East and Africa non-alcoholic beverage market. Water resources in the region are already under severe stress. The production of beverages, particularly bottled water and soft drinks, is water-intensive, requiring significant volumes for both ingredients and cleaning processes. According to the World Resources Institute, the Middle East is the most water-stressed region globally, holding 14 of the 33 countries projected to face the highest risk of surface water scarcity. This scarcity drives up the cost of water procurement and imposes strict regulatory limits on industrial water usage. Climate change exacerbates the situation, with prolonged droughts affecting agricultural output and water availability. Reports from the United Nations Environment Programme indicate that major urban centers and agricultural zones across Africa face severe groundwater depletion and contamination risks due to unregulated extraction and poor waste management. Beverage companies face mounting pressure from consumers and regulators to adopt sustainable water management practices such as water recycling and efficiency improvements. Failure to address these issues can lead to reputational damage and operational disruptions. Additionally, the disposal of plastic bottles contributes to environmental pollution, prompting calls for circular economy solutions. Governments are implementing stricter waste management regulations, requiring companies to invest in recycling infrastructure and biodegradable packaging. Balancing production needs with environmental stewardship is a complex challenge that requires significant capital investment and technological innovation. Companies must proactively address water security and sustainability to ensure long-term viability in this resource-constrained region.

Currency Volatility and Economic Instability

Currency volatility and economic instability in several Eastern countries in the region also hold back the expansion of the Middle East and Africa non alcoholic beverage market. This affects both production costs and consumer purchasing power. Many countries in the region rely on imported raw materials such as flavorings, packaging materials, and machinery, which are priced in foreign currencies. The International Monetary Fund and global currency tracking show that nations like Nigeria, Egypt, and Turkey have experienced severe currency devaluations well exceeding 40% in recent years, heavily inflating the local cost of imported raw materials. This inflationary pressure forces beverage manufacturers to raise prices, which can suppress demand in price-sensitive markets. According to the World Bank, over a dozen countries in Sub-Saharan Africa experienced persistent double-digit inflation in 2024, eroding overall household purchasing power and intensifying regional food insecurity. Economic uncertainty also discourages foreign direct investment, limiting the expansion capabilities of multinational beverage corporations. Local producers face similar challenges as the cost of local inputs rises in tandem with inflation. The fluctuating exchange rates make financial planning and profit forecasting difficult for businesses operating across multiple currencies. Additionally, economic instability can lead to supply chain disruptions due to foreign exchange shortages that hinder the ability to pay for imports. Companies must employ sophisticated hedging strategies and localize sourcing where possible to mitigate these risks. However, the persistent economic volatility remains a significant hurdle to stable growth and profitability in the region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.27% |

| Segments Covered | By Product Type, Distribution Channel, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, the rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, and the rest of MEA |

| Market Leaders Profiled | A.G. Barr, Dr. Pepper Snapple Group, Dydo Drinco, Attitude Drinks, Co, Livewire Energy, Calcol, Inc, Danone, Nestle S.A, PepsiCo, Inc, and Coca-Cola Company. |

SEGMENTAL ANALYSIS

By Product Type Insights

The bottled water segment dominated the Middle East and Africa Non Alcoholic Beverage Market and accounted for a 31.8% share in 2025. This dominance of the segment was driven by the critical necessity for safe and accessible hydration in regions characterized by arid climates and limited potable tap water infrastructure. In many parts of the Middle East and Sub-Saharan Africa, municipal water supplies are either unreliable or require extensive treatment before consumption, making bottled water a daily essential rather than a discretionary purchase. Joint monitoring reports from the World Health Organization and UNICEF indicate that more than 60% of the population in Sub-Saharan Africa lacks access to safely managed drinking water, creating a strong alternative market for packaged and treated water solutions. The extreme heat prevalent in Gulf Cooperation Council countries further amplifies daily water consumption requirements. Data from the Saudi Ministry of Environment, Water, and Agriculture reveals that residential water consumption averages nearly 300 liters per capita daily, while a robust retail bottled water market fulfills consumer demands for convenience. In urban centers across Egypt and Nigeria, bottled water is the primary source of drinking water for middle and upper-income households. The perception of bottled water as a safer and healthier option compared to tap water reinforces its dominant market share. Additionally, the widespread availability of affordable small-format packs ensures accessibility across various socioeconomic groups. This fundamental need for safe hydration creates a consistent and inelastic demand base that sustains the leadership of the bottled water segment over other beverage categories.

The robust expansion of the tourism and hospitality sector in the region significantly boosts the dominance of the bottled water segment. The region has emerged as a global tourism hub, with countries like the United Arab Emirates, Saudi Arabia, and Egypt attracting millions of international visitors annually who rely heavily on bottled beverages for hydration and safety. According to data from UN Tourism, international tourist arrivals in the Middle East reached approximately 95 million, solidifying its position as a leading region for post-pandemic tourism recovery. Hotels, resorts, and restaurants predominantly serve bottled water to guests due to hygiene standards and consumer expectations. The rise of religious tourism in Saudi Arabia, particularly during the Hajj and Umrah seasons, generates massive temporary spikes in demand. Furthermore, the development of large-scale entertainment venues and sports events across the region increases institutional consumption. The hospitality industry's strict health and safety regulations mandate the use of sealed bottled water, ensuring a steady and high volume demand. This institutional backing solidifies the segment's market leadership.

On the other hand, the tea and coffee segment is likely to experience the fastest CAGR of 6.8% between 2026 and 2034 due to the deep-rooted cultural heritage and evolving social cafe culture in the Middle East and Africa. Beverages such as Arabic coffee, Turkish tea, and Ethiopian coffee are integral to social interactions, business meetings, and family gatherings. The emergence of modern cafe chains in cities like Riyadh, Dubai, and Cairo has transformed coffee consumption from a home-based ritual to a lifestyle experience. Moreover, tea remains a staple in North and West Africa, with countries like Morocco and Kenya having high per capita consumption rates. The younger demographic is increasingly adopting western-style coffee habits while maintaining traditional preferences, creating a dual demand stream. Social media influence and the status associated with visiting premium cafes further drive the frequency of consumption. This cultural embeddedness, combined with modernization ensures that tea and coffee continue to grow at the fastest rate in the non alcoholic beverage market.

The premiumization of tea and coffee products, along with innovation in ready-to-drink formats, accelerates the growth of this segment. Consumers are increasingly willing to pay higher prices for high-quality single-origin coffees, organic tea,s and artisanal blends. Manufacturers are responding by introducing convenient, ready-to-drink canned and bottled coffee and tea products that cater to on-the-go consumers. These products offer the convenience of instant consumption without compromising on quality. The introduction of functional ingredients such as collagen, vitamins, and adaptogens in tea and coffee beverages appeals to health-conscious consumers. Local roasters and tea blenders are gaining popularity by offering unique flavor profiles that resonate with regional tastes. The expansion of e-commerce platforms allows niche brands to reach wider audiences and educate consumers about product origins and brewing methods. Subscription models for coffee and tea delivery are also gaining traction among urban professionals. This combination of premium quality, convenience, and functional benefits drives the rapid expansion of the tea and coffee segment in the regional market.

By Distribution Channel Insights

The supermarkets and hypermarkets segment led the Middle East and Africa non alcoholic beverage market and captured a 44.8% share in 2025. This leading position of the segment was attributed to the convenience of one-stop shopping and the ability to purchase bulk quantities. These retail formats offer a wide variety of beverage options under one roof, allowing consumers to compare brands, prices, and promotions efficiently. In the Gulf Cooperation Council countries, supermarkets are the primary source of grocery shopping for most households. The ability to store large volumes of beverages such as bottled water and soft drinks aligns with the consumption patterns of large families prevalent in the region. Promotional activities such as buy one get one free offers and seasonal discounts attract price-sensitive consumers. The presence of private label brands in these stores also provides affordable alternatives to national brands. The consistent availability of stock and controlled storage conditions ensure product quality and freshness. This reliability and convenience make supermarkets and hypermarkets the preferred choice for regular beverage procurement, sustaining their dominant market share.

The strategic location of supermarkets and hypermarkets in residential and commercial hubs, along with extended operating hours, enhances their accessibility and dominance in the beverage market. Retailers are increasingly placing stores in high-traffic areas and shopping malls to maximize visibility and footfall. These locations allow consumers to purchase beverages alongside other household needs during leisure outings. Extended operating hours, including 24-hour service in some locations, cater to the diverse schedules of urban populations. The integration of loyalty programs and digital payment systems further enhances the shopping experience and encourages repeat visits. Supermarkets also serve as key launch pads for new beverage products, allowing manufacturers to reach a broad audience quickly. The trust associated with established retail chains ensures consumer confidence in product authenticity and safety. This combination of accessibility, convenience, and trust solidifies the leading position of supermarkets and hypermarkets in the distribution landscape.

The online stores segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 14.5%, owing to increasing digital penetration and smartphone adoption across the Middle East and Africa. The widespread use of mobile devices has enabled consumers to shop for beverages from the comfort of their homes, offering unparalleled convenience. The ability to browse a wide range of products, read reviews, and compare prices online empowers consumers to make informed choices. E-commerce platforms often offer exclusive deals and bundles that attract price-conscious shoppers. The integration of social media marketing influences purchasing decisions, particularly among younger demographics. The ease of reordering staple items such as bottled water and soft drinks through subscription services enhances customer retention. This digital shift is transforming the retail landscape and enabling online stores to capture a growing share of the beverage market.

The improvement in last-mile delivery infrastructure and cold chain logistics is a critical factor accelerating the growth of online stores in the beverage market. Efficient delivery services ensure that perishable and temperature-sensitive beverages such as fresh juices and dairy drinks reach consumers in optimal condition. Companies are investing in advanced warehousing and fleet management systems to reduce delivery times and costs. The use of insulated packaging and refrigerated vehicles maintains product quality during transit. In Africa, startups are leveraging motorcycle fleets to navigate traffic-congested urban areas, ensuring timely deliveries. The reliability of these services builds consumer trust in online shopping for beverages. Additionally, the ability to track orders in real time provides transparency and convenience. These logistical advancements remove previous barriers to online beverage purchases, enabling the segment to grow at the fastest rate in the distribution channel landscape.

REGIONAL ANALYSIS

Kingdom of Saudi Arabia Non Alcoholic Beverage Market Analysis

The Kingdom of Saudi Arabia outperformed other regions in the Middle East and Africa Non Alcoholic Beverage Market and occupied a 25.5% share in 2025. Its large population and high per capita consumption have contributed to its supremacy. The country's hot climate and cultural preferences for hydration and social beverages create a robust demand base. According to the official General Authority for Statistics (GASTAT), the population of Saudi Arabia reached 35.3 million in 2024, up from 33.7 million in 2023. The market is heavily influenced by a large, young demographic under 35 years old that strongly drives the consumption of carbonated soft drinks, energy beverages, and healthy alternatives. The Vision 2030 initiative has spurred the development of the entertainment and tourism sectors, increasing out-of-home consumption. The government's focus on health and wellness has led to a rise in demand for low-sugar and functional beverages. The expansion of retail infrastructure and e-commerce platforms enhances product accessibility across the kingdom. Major international and local beverage companies are investing heavily in production facilities to capitalize on this growth. The strict regulatory framework ensures high-quality standards, fostering consumer trust. The combination of demographic trends, economic diversification, and regulatory support positions Saudi Arabia as the dominant market in the region.

United Arab Emirates Non Alcoholic Beverage Market Analysis

The United Arab Emirates is another major country in the regional market due to high disposable incomes and a cosmopolitan consumer base. The country serves as a hub for beverage innovation and premium product launches in the Middle East. According to the official annual report by the Dubai Department of Economy and Tourism (DET), Dubai actually hosted a record-breaking 18.72 million international overnight visitors in 2024, which was a 9% increase compared to the previous year. This massive surge directly drove record-high occupancy levels in the hospitality and retail sectors. The diverse expatriate population introduces varied taste preferences, leading to a wide array of beverage offerings. The government's sustainability initiatives encourage the adoption of eco-friendly packaging and local production. The well-developed retail landscape, including luxury supermarkets and online platforms, ensures broad product availability. Consumers in the UAE are highly receptive to health and wellness trends, driving sales of organic and functional beverages. The country's strategic location facilitates re-exports to neighboring markets, enhancing its market influence. The focus on quality and innovation keeps the UAE at the forefront of the regional beverage industry.

Israel Non Alcoholic Beverage Market Analysis

Israel holds a noteworthy position in the Middle East and Africa Non Alcoholic Beverage Market owing to a technologically advanced agricultural sector and high health consciousness. The country is a leader in water technology and efficient irrigation, which supports the production of high-quality fruits for juice manufacturing. The strong focus on research and development leads to innovative beverage formulations, including functional and fortified drinks. The domestic market is characterized by a preference for natural and organic products driven by educated consumers. The retail sector is highly competitive with a strong presence of private label brands. The integration of digital technologies in supply chain management ensures efficiency and product freshness. Israel's emphasis on sustainability and health positions it as a niche but influential player in the regional market.

COMPETITION OVERVIEW

The competition in the Middle East and Africa Non Alcoholic Beverage Market is intense and characterized by the presence of global multinational corporations alongside strong regional and local players. Multinational giants leverage their extensive resources and brand equity to dominate mainstream segments while local companies compete through niche offerings and a deep understanding of regional preferences. The market features high barriers to entry due to significant capital requirements for production facilities and distribution networks. Competitive dynamics are influenced by fluctuating raw material costs and currency volatility, which impact profitability and pricing strategies. Companies differentiate themselves through innovation in product formulations, packaging, and marketing campaigns that resonate with local cultures. The rise of health consciousness has intensified competition in the healthy beverage segment, with brands vying for shelf space with low sugar and organic options. Retailers play a pivotal role in shaping competition by promoting private label brands that offer lower prices. Strategic alliances and mergers are common tactics used to consolidate market position and expand geographic reach. The fragmented nature of the African market presents unique challenges and opportunities for competitors who can navigate logistical complexities. Overall, the competitive landscape requires agility, innovation, and strong local partnerships to sustain growth and maintain relevance in this diverse and evolving market.

KEY MARKET PLAYERS

A few major players of the Middle East and Africa non-alcoholic beverage market include

- A.G. Barr

- Dr. Pepper Snapple Group

- Dydo Drinco

- Attitude Drinks, Co

- Livewire Energy

- Calcol, Inc

- Danone

- Nestle S.A

- PepsiCo, Inc

- Coca-Cola Company

Top Strategies Used by Key Market Participants

Key players in the Middle East and Africa Non Alcoholic Beverage Market primarily focus on product localization and diversification to cater to distinct regional tastes and cultural preferences. Companies increasingly invest in research and development to create healthy and functional beverages such as low-sugar drinks and fortified juices that address rising health concerns. Sustainability initiatives are central to corporate strategies, with firms adopting eco-friendly packaging and water conservation practices to comply with environmental regulations. Expansion of distribution networks into rural and underserved areas enables broader market reach and increased sales volume. Strategic partnerships with local bottlers and distributors enhance operational efficiency and reduce logistics costs. Digital transformation through e-commerce platforms and social media marketing strengthens consumer engagement and brand loyalty. Price competitiveness remains crucial in price-sensitive markets, prompting companies to optimize production costs and offer affordable pack sizes. These multifaceted strategies help participants navigate regulatory challenges and capitalize on growth opportunities in the diverse MEA region.

Leading Players in the MEA Non-Alcoholic Beverage Market

- The Coca-Cola Company maintains a robust presence across the Middle East and Africa through its extensive bottling partnerships and diverse product portfolio. The company actively invests in local manufacturing facilities to enhance supply chain efficiency and reduce logistical costs. Recent initiatives include the introduction of low-sugar and zero-calorie variants to align with regional health regulations and consumer preferences. Coca-Cola has strengthened its market position by launching innovative flavors tailored to local tastes, such as date and pomegranate-infused beverages. The corporation also focuses on sustainability by implementing water replenishment projects and recycling programs in key markets like South Africa and Egypt. Digital marketing campaigns targeting younger demographics have enhanced brand engagement and loyalty. By leveraging its vast distribution network, the company ensures widespread availability of its products in both urban and rural areas. These strategic efforts enable Coca-Cola to maintain its leadership while adapting to evolving regulatory and consumer landscapes in the region.

- PepsiCo Inc operates as a major competitor in the Middle East and Africa non alcoholic beverage sector with a strong focus on innovation and localization. The company has expanded its portfolio to include healthier options such as bottled water, juice,s and functional drinks to meet changing consumer demands. Recent actions involve significant investments in production capabilities in countries like Saudi Arabia and Nigeria to support local economies and ensure product freshness. PepsiCo has introduced new ready-to-drink tea and coffee products to capitalize on the growing cafe culture in the region. The organization emphasizes sustainable packaging solutions by increasing the use of recycled materials in its bottles. Strategic partnerships with local distributors have improved market penetration in remote areas. PepsiCo also engages in community development programs that enhance its brand reputation and social license to operate. These comprehensive strategies allow PepsiCo to compete effectively and drive growth in the dynamic MEA beverage market.

- Almarai Company is a leading integrated dairy and beverage producer in the Middle East with a dominant position in the Gulf Cooperation Council markets. The company offers a wide range of non alcoholic beverages, including juice,s laban, and flavored milk products that are staples in regional diets. Almarai has strengthened its market position by expanding its production capacity and investing in advanced processing technologies to ensure high-quality standards. Recent initiatives include the launch of organic juice lines and fortified beverages to cater to health-conscious consumers. The company utilizes its vertically integrated supply chain to control costs and maintain consistent product availability. Almarai also focuses on sustainability by adopting renewable energy sources in its facilities. Its strong brand recognition and trust among consumers provide a competitive advantage. Almarai continuously innovates its product offerings and optimizes its distribution networks. This approach reinforces its status as a key player in the regional non-alcoholic beverage market.

MARKET SEGMENTATION

This research report on the Middle East and Africa non-alcoholic beverage market has been segmented and sub-segmented based on product type, distribution channel, and region.

By Product Type

- Soft drinks

- Dairy drinks

- Tea & coffee

- Bottled water

- Juice

- Others

By Distribution Channel

- Specialty Stores

- Online Stores

- Super Markets/ Hyper Markets

- Convenience Stores

- Departmental Stores

- Others

By Region

- KSA

- UAE

- Israel

- Rest Of GCC Countries

Frequently Asked Questions

1. What factors are driving the growth of the MEA non-alcoholic beverage market?

The market growth is driven by rapid urbanization, increasing population, rising disposable incomes, and growing consumer demand for convenient, ready-to-drink beverages. The expanding youth demographic across the region is also boosting the demand for soft drinks, bottled water, and functional beverages.

2. How is health awareness influencing the market?

Health awareness is encouraging consumers to shift from high-sugar carbonated drinks toward healthier alternatives such as fruit juices, bottled water, plant-based drinks, and low-calorie functional beverages. This trend has prompted manufacturers to introduce reformulated products with reduced sugar content.

3. Which product segments dominate the MEA non-alcoholic beverage market?

Carbonated soft drinks and bottled water account for a significant share of the market due to widespread consumption across urban and rural areas. However, energy drinks, flavored water, and functional beverages are gaining traction due to changing lifestyle preferences.

4. Which countries contribute significantly to the MEA non-alcoholic beverage market?

Key contributing countries include Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Nigeria. These countries are experiencing increased demand due to population growth and expanding retail infrastructure.

5. How does cultural preference impact beverage consumption in the region?

Cultural and religious restrictions on alcohol consumption in several Middle Eastern countries encourage higher demand for non-alcoholic beverages. As a result, soft drinks, juices, and flavored beverages are widely consumed across the region.

6. How is the demand for functional beverages evolving?

Functional beverages containing vitamins, minerals, or herbal extracts are gaining popularity as consumers seek drinks that offer additional health benefits beyond hydration.

7. What are the key challenges in the MEA non-alcoholic beverage market?

The market faces challenges such as fluctuating raw material costs, regulatory policies on sugar content, and competition from alternative beverages like herbal teas and plant-based drinks.

8. How does packaging influence the non-alcoholic beverage market?

Packaging innovations such as recyclable bottles, lightweight materials, and resealable containers enhance product shelf life and consumer convenience while supporting sustainability goals.

9. Which distribution channels dominate the MEA market?

Supermarkets and hypermarkets dominate beverage distribution, followed by convenience stores and online retail platforms. Foodservice outlets such as restaurants and cafes also play a key role.

10. What is the future outlook of the MEA non-alcoholic beverage market?

The MEA non-alcoholic beverage market is expected to witness steady growth driven by increasing urbanization, expanding retail infrastructure, rising health awareness, and growing demand for functional and premium beverages.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com