North America Probiotics Market Research Report Segmented By Application (Food & Beverages, Dairy Products, Non-Dairy Beverages, Infant Formula, Cereals, Dietary Supplements, Feed), Ingredient (Bacteria, Yeast), Form (Dry, Liquid), End-User (Human And Animal), And Country (Us, Canada And Rest Of North America) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

North America Probiotics Market Size

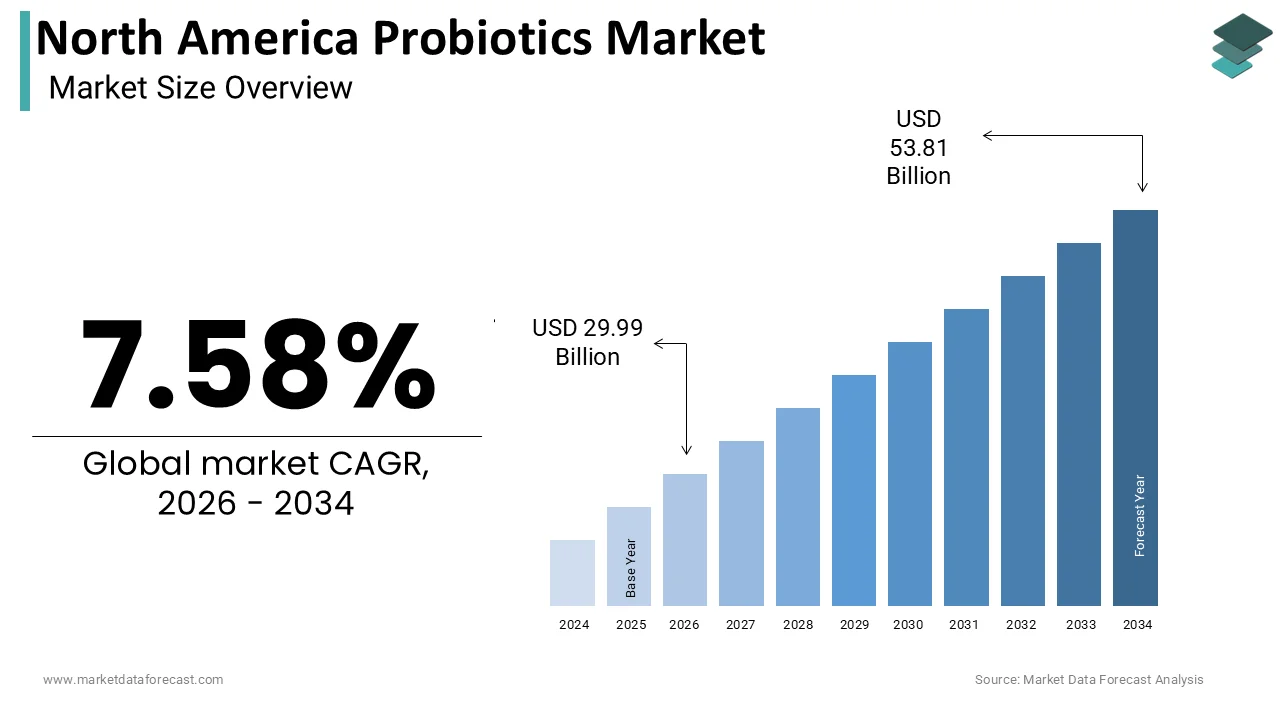

The size of the North American probiotics market was expected to be worth USD 27.88 billion in 2025 and is anticipated to be worth USD 53.81 billion by 2034, from USD 29.99 billion in 2026, growing at a CAGR of 7.58% during the forecast period.

The North American probiotics market includes a wide range of live microorganisms, primarily bacteria and yeasts, that confer health benefits when consumed in adequate amounts. These beneficial microbes are widely incorporated into dietary supplements, functional foods, and beverages to support gut health, immune function, and overall wellness. The market spans various product categories, including yogurts, fermented dairy products, plant-based alternatives, infant formulas, and encapsulated supplements.

As awareness about preventive healthcare grows, consumers in the U.S., Canada, and Mexico are increasingly integrating probiotic-rich products into their daily diets. According to the Centers for Disease Control and Prevention (CDC), digestive disorders affect a significant number of Americans annually, reinforcing the need for microbiome-supporting interventions.

MARKET DRIVERS

Rising Incidence of Digestive and Immune-Related Disorders

A significant driver fueling the growth of the North American probiotics market is the increasing prevalence of gastrointestinal (GI) and immune-related conditions among the general population. According to the American College of Gastroenterology, a significant portion of people in the U.S. suffer from digestive ailments such as irritable bowel syndrome (IBS), inflammatory bowel disease (IBD), and antibiotic-associated diarrhea. These conditions have prompted both medical professionals and consumers to explore probiotics as a natural intervention for maintaining gut flora balance and alleviating symptoms. In addition, research published by the National Institutes of Health (NIH) highlights a strong link between gut microbiota and immune system functionality, reinforcing the role of probiotics in strengthening immunity. With a notable share of the immune system residing in the gut, consumption of probiotic strains like Lactobacillus and Bifidobacterium has gained traction. Like, nearly half of all U.S. adults take dietary supplements regularly, with probiotics witnessing one of the fastest adoption rates due to their perceived efficacy in supporting digestive and immune health. Moreover, hospitals and integrative medicine clinics are increasingly recommending probiotics to patients undergoing antibiotic treatments, further validating their clinical relevance.

Expansion of Functional Food and Beverage Segment

The rapid expansion of the functional food and beverage industry is another key factor propelling the North American probiotics market forward. Consumers are increasingly seeking food products that offer added health benefits beyond basic nutrition, leading manufacturers to incorporate probiotics into a diverse array of items, including yogurt, kefir, kombucha, plant-based milks, and even snack bars. According to the International Food Information Council (IFIC), a notable share of U.S. consumers actively seek out foods and beverages with functional health benefits, making probiotic-enriched products highly attractive. Companies like KeVita, GT’s Living Foods, and Danone have capitalized on this trend by introducing innovative probiotic beverages that appeal to health-conscious demographics. Similarly, major dairy producers such as Chobani and Horizon Organic have expanded their lines of probiotic yogurts and fermented milk products. Retailers and e-commerce platforms have also played a pivotal role in enhancing accessibility. Amazon Fresh and Instacart now feature dedicated probiotic sections, while Whole Foods and Kroger promote gut-health-focused promotions.

MARKET RESTRAINTS

Regulatory Complexity and Labeling Challenges

One of the primary restraints affecting the North American probiotics market is the complex regulatory landscape governing health claims, strain specificity, and product labeling. According to the FDA, unless a probiotic product undergoes rigorous drug approval processes, it cannot claim to treat or cure diseases, creating ambiguity for marketers and consumers alike. Similarly, Health Canada imposes stringent guidelines on probiotic labeling, requiring manufacturers to specify exact bacterial strains and viable counts at the point of sale. This level of detail increases production costs and necessitates advanced quality control measures. Additionally, inconsistencies in international regulations complicate cross-border trade and formulation strategies for multinational companies.

Limited Consumer Awareness and Misconceptions

Despite rising interest in gut health, a notable restraint in the North American probiotics market is the persistent lack of comprehensive consumer understanding regarding probiotic efficacy, strain differentiation, and appropriate usage. This knowledge gap leads to misconceptions such as equating all fermented foods with effective probiotic content or assuming that higher colony-forming units (CFUs) always equate to better results. Many consumers also remain unaware of storage requirements and shelf-life considerations, which can impact the viability of live cultures. Furthermore, misinformation spread on social media platforms often exaggerates probiotic benefits without scientific backing, leading to skepticism among cautious consumers.

MARKET OPPORTUNITIES

Personalized Probiotics and Microbiome Testing Services

An emerging opportunity in the North American probiotics market lies in the development of personalized probiotic formulations based on individual microbiome profiles. Advances in genetic sequencing and digital health technologies have enabled companies to offer customized probiotic blends tailored to a person's unique gut composition, lifestyle, and health goals. Companies such as Viome, Thryve, and Atlas Biomed have introduced at-home gut microbiome testing kits that analyze microbial diversity and recommend targeted probiotic regimens. These services cater to health-conscious consumers seeking data-driven wellness solutions, particularly in urban centers where preventive healthcare trends are strongest. The American Gut Project, led by researchers at the University of California San Diego, has further validated the link between microbiome composition and chronic conditions, reinforcing scientific credibility. Moreover, partnerships between probiotic manufacturers and telehealth platforms are streamlining access to personalized recommendations.

Expansion into Non-Dietary Applications

Beyond traditional dietary supplements and food products, the North American probiotics market is witnessing significant growth opportunities in non-dietary applications, particularly in skincare, pharmaceuticals, and animal health. According to the Personal Care Products Council, probiotic-infused skincare products accounted for over 15% of new beauty launches in 2023, driven by the recognition of the skin microbiome’s role in dermatological health. Leading personal care brands such as L’Oréal, Johnson & Johnson, and Aveeno have introduced probiotic-based moisturizers, cleansers, and serums designed to restore skin barrier integrity and reduce inflammation. Clinical studies cited by the American Academy of Dermatology indicate that topical probiotics can help manage conditions like eczema, rosacea, and acne by modulating skin flora. Simultaneously, the pharmaceutical sector is exploring probiotics as adjunct therapies for conditions ranging from Clostridioides difficile infections to mental health disorders via the gut-brain axis. In veterinary medicine, probiotics are increasingly used in pet food and livestock feed to enhance digestion and reduce antibiotic reliance.

MARKET CHALLENGES

Strain-Specific Efficacy and Scientific Validation

One of the most pressing challenges facing the North American probiotics market is the inconsistency in strain-specific efficacy and the need for rigorous scientific validation. Unlike pharmaceuticals, where active ingredients are standardized and tested for specific outcomes, many probiotic products on the market contain undefined or poorly characterized bacterial strains, making it difficult to determine their actual health benefits. According to a review published by the National Institutes of Health (NIH), only a fraction of commercially available probiotic strains have undergone controlled clinical trials to substantiate their claimed effects. This lack of standardization raises concerns among healthcare professionals and regulatory bodies regarding the reliability and reproducibility of health outcomes associated with different probiotic formulations. Moreover, the American Gastroenterological Association (AGA) issued clinical guidelines in 2023 stating that few probiotic strains have sufficient evidence to support their use in treating specific gastrointestinal conditions. This disparity between consumer perception and scientific consensus poses a challenge for manufacturers attempting to position their products as credible health solutions.

Supply Chain and Shelf-Life Stability Issues

Maintaining the viability of live microbial cultures throughout the supply chain presents a significant challenge for the North American probiotics market. Unlike conventional food or supplement ingredients, probiotics require strict temperature controls and specialized packaging to ensure microbial survival until consumption. Cold chain logistics play a crucial role in preserving probiotic potency, especially for perishable products such as refrigerated yogurts, kefirs, and liquid supplements. However, disruptions in transportation, fluctuating warehouse temperatures, and improper consumer storage can compromise product effectiveness. Also, extended shelf life remains a technical hurdle for manufacturers aiming to produce ambient-stable probiotic formulations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.58% |

| Segments Covered | By Application, Ingredient, Form, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Us, Canada, and the rest of North America |

| Market Leaders Profiled | Yakult Honsha Co. Ltd, Nestle S.A., Groupe Danone, PepsiCo Inc. (Kevita), Lifeway Foods Inc., Actimel, Activia, Bright Dairy, BioGaiad CHR Hansen. |

SEGMENTAL ANALYSIS

By Application Insights

Dietary supplements represented the largest application segment in the North American probiotics market i.e. 35.4% of total consumption in 2025. This dominance is primarily driven by the growing consumer preference for preventive healthcare and the ease of incorporating probiotic capsules or powders into daily routines without altering dietary habits. One of the key drivers is the increasing awareness of gut health benefits among U.S. consumers. According to the Council for Responsible Nutrition (CRN), over 75% of U.S. adults take dietary supplements regularly, with probiotics ranking among the fastest-growing categories. The convenience, high CFU counts, and availability of strain-specific formulations have made supplements a preferred choice for individuals seeking targeted digestive or immune support. Moreover, regulatory clarity around supplement labeling and health claims has fostered market growth. The FDA’s oversight under DSHEA (Dietary Supplement Health and Education Act) provides a structured framework that supports product innovation while ensuring quality standards.

The non-dairy beverages segment is experiencing the highest growth rate in the North American probiotics market, expanding at a CAGR of 11.6%. This rapid expansion is fueled by shifting consumer preferences toward plant-based nutrition and functional hydration. One of the primary growth catalysts is the surge in popularity of plant-based diets, particularly among millennials and Gen Z consumers. Brands like Kevita, GoodBelly, and Danone North America are capitalizing on this trend by introducing probiotic-infused alternatives that offer digestive benefits alongside lactose-free options. Moreover, rising concerns about lactose intolerance and dairy allergies have accelerated the shift away from traditional dairy products. According to the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK), an estimated 65% of the global population has a reduced ability to digest lactose after infancy making non-dairy beverages an attractive alternative.

By Ingredient Insights

Bacteria-based probiotics dominated the NorAmericanica market by capturing a substantial share of ingredient-type consumption in 2025. This overwhelming influence is due to the long-standing scientific validation and commercial adoption of bacterial strains such as Lactobacillus, Bifidobacterium, and Streptococcus thermophilus in promoting gut and immune health. A primary driver of this segment’s leadership is the extensive research backing bacterial probiotics for digestive wellness. According to the National Institutes of Health (NIH), a considerable share of clinical studies conducted on probiotics globally focus on bacterial strains, providing robust evidence for their efficacy in managing conditions like irritable bowel syndrome (IBS) and antibiotic-associated diarrhea. Furthermore, bacterial probiotics are widely used across food, dietary supplements, and animal feed industries due to their adaptability and compatibility with various delivery formats.

Yeast-based probiotics are developing as the highest-growing ingredient segment in the North American probiotics market, registering a CAGR of 14.3%. This rapid growth is attributed to the unique advantages offered by yeast strains such as Saccharomyces boulardii, including acid resistance, broad-spectrum antimicrobial activity, and compatibility with antibiotic therapy. A key growth driver is the increasing demand for probiotics that can survive harsh gastrointestinal conditions and exert beneficial effects without requiring refrigeration. According to a review published in the journal Frontiers in Microbiology, Saccharomyces boulardii has demonstrated efficacy in preventing Clostridioides difficile infections and reducing symptoms of traveler’s diarrhea—conditions that are increasingly managed through probiotic supplementation. Moreover, yeast-based probiotics are gaining traction in pharmaceutical applications due to their stability and safety profile.

By Form, Insights

Dry-form probiotics had the maximum share in the North American market representing 78.2% of total consumption in 2025. This control is largely due to the superior shelf life, ease of formulation, and cost-effectiveness associated with dry forms such as capsules, tablets, and powders. The main reason for this segment’s leadership is the enhanced microbial stability provided by freeze-drying and microencapsulation technologies. This makes dry forms more suitable for mass distribution through retail and e-commerce channels. Another key factor is consumer preference for convenience and portability. The Council for Responsible Nutrition (CRN) noted that over 70% of U.S. adults prefer taking probiotics in capsule or tablet format due to ease of dosing and minimal handling requirements. Apart from these, dry probiotics are extensively used in dietary supplements and fortified foods, allowing manufacturers to integrate them seamlessly into various product lines.

Liquid-form probiotics are witnessing the strongest development in the North American market, rising at a CAGR of 12.1%. This growth is primarily driven by the rising popularity of ready-to-consume functional beverages and fermented drinks that incorporate live cultures for digestive and immune benefits. A key growth catalyst is the increasing integration of probiotics into non-dairy beverages such as kombucha, kefir, and plant-based milk These products appeal to health-conscious consumers who prefer palatable, convenient, and refreshing ways to consume probiotics. Additionally, advancements in biopreservation techniques have improved the viability of live cultures in liquid environments. Research published by the International Dairy Journal indicates that cold-chain logistics and protective packaging solutions have significantly enhanced the survival rates of probiotic strains in liquid matrices.

REGIONAL ANALYSIS

The United States had the maximum share in the North American probiotics market by contributing 72.3% of regional revenue in 2025. This top position is supported by high consumer awareness of gut health, the strong presence of key industry players, and a well-developed regulatory framework for dietary supplements and functional foods. A major driver is the widespread integration of probiotics into everyday nutrition, with a growing number of Americans incorporating them into their diets through supplements, yogurts, and fermented beverages. This has led to strong demand across multiple product categories, including refrigerated and ambient-stable probiotics. Additionally, the U.S. Food and Drug Administration (FDA) has established clear guidelines for probiotic labeling and manufacturing practices under the Dietary Supplement Health and Education Act (DSHEA), fostering innovation and consumer confidence. Major companies such as General Mills, PepsiCo, and Nestlé have expanded their probiotic offerings, further embedding these ingredients into mainstream food and beverage products.

Canada is maintaining a steady growth trajectory driven by increasing health consciousness and regulatory support for functional foods. Consumers in Canada are showing a growing inclination towards natural health products, with probiotics playing a central role in digestive wellness and immunity enhancement. A key factor supporting this growth is the proactive approach taken by Health Canada in evaluating and approving probiotic strains for specific health claims. Additionally, the Canadian dairy industry has been instrumental in integrating probiotics into yogurt and fermented milk products, aligning with national dietary guidelines that promote gut-friendly nutrition. These developments underscore Canada’s expanding role in the broader North American probiotics landscape.

Mexico is emerging as a promising player due to rising urbanization, changing dietary habits, and increasing investment in functional food production. While traditionally less developed than the U.S. and Canada in terms of probiotic adoption, Mexico is witnessing a gradual shift toward health-focused consumption patterns. One of the key drivers is the growing presence of multinational food and beverage companies establishing operations in Mexico to serve both domestic and export markets. Also, the Mexican government has shown interest in promoting nutritional education programs, particularly in schools and public health initiatives.

LEADING PLAYERS IN THE NORTH AMERICAN PROBIOTICS MARKET

Danone North America

Danone is a global leader in probiotics, particularly through its portfolio of dairy and plant-based products fortified with live cultures. In North America, the company plays a dominant role via brands like Activia and DanActive, which are widely recognized for their digestive health benefits. The company integrates scientific research with product development to ensure efficacy and consumer trust. Danone’s commitment to sustainability and gut health education has strengthened its position as a trusted name in the probiotic food and beverage space.

Chr. Hansen Holding A/S

A key player in microbial solutions, Chr. Hansen supplies high-quality probiotic strains to food, dietary supplements, and pharmaceutical companies across North America. Known for its science-driven approach, the company develops strain-specific probiotics backed by clinical research, catering to both human and animal health applications. Its strategic collaborations with major food manufacturers and investment in microbiome innovation have solidified its presence in the region's probiotics supply chain.

DuPont Nutrition & Biosciences (Now Part of IFF)

DuPont has been instrumental in advancing probiotic research and commercialization in North America. The company offers a broad range of probiotic strains used in supplements, dairy, and functional foods. With a strong focus on clinical validation and partnerships with healthcare professionals, DuPont has helped shape regulatory standards and consumer confidence in probiotic products globally.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One of the primary strategies employed by leading players in the North America probiotics market is product innovation and differentiation, focusing on developing targeted, strain-specific formulations that address health concerns such as digestive wellness, immunity, and mental health. Companies are investing heavily in clinical research to validate the efficacy of their probiotic strains, enhancing credibility and consumer trust.

Another crucial strategy is strategic acquisitions and partnerships, allowing firms to expand their portfolios, access new markets, and integrate into adjacent sectors such as personalized nutrition and biopharmaceuticals. By acquiring smaller biotech startups or forming alliances with digital health platforms, companies can accelerate innovation and enhance market reach.

Lastly, consumer education and brand positioning play a central role in strengthening market presence. Leading firms engage in awareness campaigns, collaborate with healthcare professionals, and leverage digital marketing to highlight the benefits of probiotics, fostering long-term loyalty and differentiating themselves in a competitive landscape.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the North American probiotics market include Yakult Honsha Co. Ltd, Nestle S.A., Groupe Danone, PepsiCo Inc. (Kevita), Lifeway Foods Inc., Actimel, Activia, Bright Dairy, BioGaiad CHR Hansen.

The competition in the North American probiotics market is highly dynamic, characterized by the presence of established multinational corporations, emerging biotech firms, and regional specialty brands vying for consumer attention and shelf space. While global players dominate due to their extensive R&D capabilities, brand recognition, and distribution networks, niche companies are gaining traction by offering differentiated, science-backed formulations tailored to specific health needs. The market is increasingly fragmented, with players competing not only on product quality and efficacy but also on formulation innovation, delivery formats, and branding strategies.

A significant battleground lies in the differentiation of probiotic strains and their scientifically validated benefits, as consumers become more discerning about what they consume. Additionally, the rise of private-label brands and direct-to-consumer models is reshaping retail dynamics, pressuring traditional manufacturers to enhance value propositions. As demand for transparency, traceability, and personalization grows, companies must continuously evolve their offerings and strengthen partnerships across the supply chain to maintain relevance and competitiveness in this rapidly expanding sector.

RECENT HAPPENINGS IN THE MARKET

- In January 2025, Danone North America launched a new line of plant-based probiotic yogurts under the Activia brand, targeting lactose-intolerant consumers and aligning with the growing trend of alternative protein sources.

- In March 2025, Chr. Hansen announced a collaborative research initiative with a leading U.S. university to explore next-generation probiotics for metabolic health, reinforcing its commitment to scientific advancement in microbiome-based therapies.

- In June 2025, IFF (formerly DuPont Nutrition & Biosciences) introduced a suite of spore-forming probiotic strains designed for enhanced stability and resilience, catering to the dietary supplement and functional food industries.

- In August 2025, Nestlé Health Science acquired a U.S.-based personalized probiotics startup to expand its footprint in precision nutrition and develop customized microbiome solutions for individual consumers.

- In October 2025, General Mills expanded its partnership with a Canadian probiotic ingredient supplier to enhance the live culture content in its yogurt products, aiming to strengthen its position in the premium probiotic dairy segment.

MARKET SEGMENTATION

This research report on the North America Probiotics Market has been segmented and sub-segmented based on application, ingredient, form, and region.

By Application

- Dietary Supplements

- Non-Dairy Beverages

By Ingredient

- Bacteria-Based Probiotics

- Yeast-Based Probiotics

By Form

- Dry Form Probiotics

- Liquid Form Probiotics

By Region

- Us

- Canada

- Rest of North America

Frequently Asked Questions

1. What are the key drivers of the market?

Rising awareness of gut health, increasing demand for functional foods, and growing use of dietary supplements drive the market

2. Why are probiotics popular in North America?

Consumers are highly focused on digestive health, immunity, and overall wellness

3. What are the main product types?

Functional foods and beverages, dietary supplements, infant nutrition, and animal feed

4. Which segment dominates the market?

Probiotic food and beverages dominate due to high consumption of yogurt and fermented products

5. Which segment is growing fastest?

Dietary supplements are the fastest-growing segment due to convenience and increasing health awareness

6. What are the major applications?

Digestive health, immune support, gut health management, and preventive healthcare

7. What trends are shaping the market?

Growth of personalized nutrition, clean-label products, and probiotic-enriched foods

8. What challenges does the market face?

High product costs, regulatory complexities, and stability issues of probiotic strains

9. What opportunities exist in the market?

Expansion in functional foods, e-commerce growth, and innovation in probiotic formulations

10. Who are the key players in the market?

Danone, Yakult, Nestlé, Procter & Gamble, and BioGaia are major players

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com