Global TAVR Market Size, Share, Trends & Growth Analysis Report – Segmented By Surgery Method (Transfemoral Implantation, Transapical Implantation, Transaortic Implantation and Transcaval Implantation), Valve Frame Material, Valve Size, Valve Leaflets Material, End Users & Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 to 2033

Global TAVR Market Size

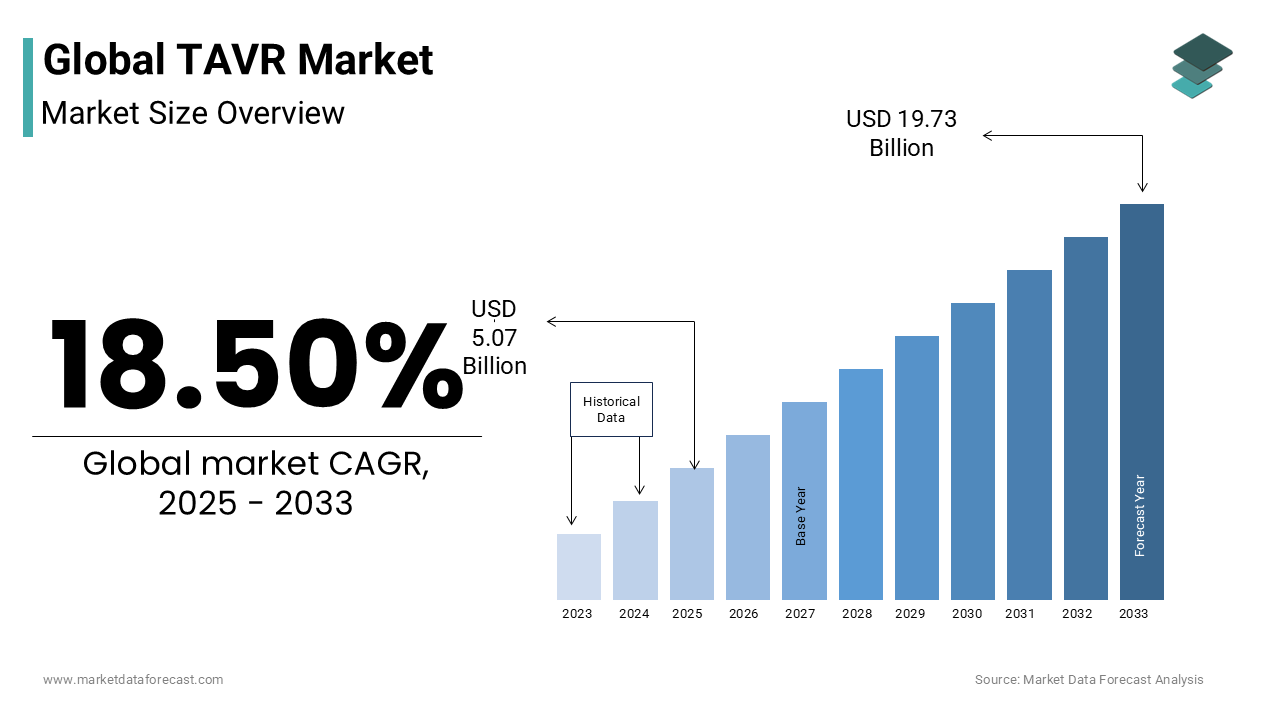

The global TAVR is estimated to grow from USD 5.07 billion in 2025 to USD 19.73 billion in 2033, representing a CAGR of 18.50%.

The Transcatheter Aortic Valve Replacement (TAVR) is a minimally invasive cardiovascular intervention designed to replace a diseased aortic valve without open-heart surgery. TAVR is primarily indicated for patients with severe aortic stenosis who are at intermediate, high, or prohibitive surgical risk, offering a life-extending alternative with reduced recovery time and lower perioperative complications. The procedure involves delivering a bioprosthetic valve via a catheter, typically through the femoral artery (transfemoral approach), and expanding it within the native valve annulus. As per the American Heart Association, aortic stenosis affects approximately 1.5 million people in the United States alone, with prevalence increasing sharply in individuals over 75 years of age.

MARKET DRIVERS

Rising Prevalence of Aortic Stenosis in Aging Populations

The global increase in life expectancy has led to a parallel surge in age-related cardiovascular conditions, with aortic stenosis emerging as a leading cause of morbidity and mortality among the elderly. According to the World Health Organization, the number of people aged 60 and over is expected to double from 1 billion in 2020 to 2.1 billion by 2050 by creating a rapidly expanding pool of individuals at risk for degenerative valve disease. According to the U.S. Centers for Disease Control and Prevention, aortic stenosis is responsible for 73,000 hospitalizations annually, with untreated severe cases carrying a two-year mortality rate exceeding 50%.

Expansion of TAVR Indications to Lower-Risk Patient Populations

The progressive expansion of its clinical indications beyond high-risk patients to include those classified as intermediate and low surgical risk is propelling the growth of the Transcatheter Aortic Valve Replacement (TAVR) market. Similarly, in Canada, the Canadian Cardiovascular Society updated its guidelines in 2022 to recommend TAVR as a first-line option for select low-risk individuals

MARKET RESTRAINTS

High Cost of TAVR Procedures and Limited Reimbursement in Emerging Economies

The financial burden associated with TAVR remains a barrier to widespread adoption in low- and middle-income countries where healthcare budgets are constrained and reimbursement mechanisms are underdeveloped. Even in countries with universal healthcare, coverage is inconsistent. Brazil’s Unified Health System (SUS) reimburses only 1,200 TAVR procedures annually, despite an estimated 15,000 potential candidates, as per the Brazilian Society of Cardiovascular Surgery.

Limited Availability of Specialized Infrastructure and Trained Interventional Teams

The successful execution of TAVR requires a multidisciplinary heart team, advanced imaging systems, hybrid operating rooms, and rigorous post-procedural care resources that are concentrated in tertiary care centers and largely absent in rural and underserved regions. This attribute is also hampering the growth of the Transcatheter Aortic Valve Replacement (TAVR) market. Canada faces a 30% deficit in interventional cardiologists, delaying patient access, according to the Canadian Cardiovascular Society. Additionally, logistical challenges such as valve transportation, storage, and inventory management hinder scalability. The U.S. Food and Drug Administration mandates strict handling protocols for transcatheter valves, which require temperature-controlled supply chains that are difficult to maintain in remote areas.

MARKET OPPORTUNITIES

Technological Advancements in Next-Generation TAVR Devices

Innovation in transcatheter valve design and delivery systems is unlocking new clinical possibilities by enhancing procedural safety and expanding patient eligibility. The multicenter SURTAVI trial demonstrated that these advanced devices reduced the incidence of moderate-to-severe paravalvular regurgitation to less than 2%, a 70% improvement over first-generation systems. Additionally, the development of mechanically expandable valves like the JenaValve EnVeo S enables precise placement in complex anatomies, including bicuspid aortic valves, which were historically considered high-risk for TAVR. Furthermore, integration with intraprocedural imaging and AI-based planning tools such as Siemens Healthineers’ syngo-valve has improved accuracy in valve sizing and positioning.

Increasing Adoption of TAVR in Ambulatory and Outpatient Settings

TAVR transitions from an inpatient hospital procedure to a same-day or 23-hour observation model is driven by improved procedural efficiency that enhances patient selection and streamlined care pathways. According to the American College of Cardiology, over 40% of TAVR procedures in the United States were performed with a length of stay of 48 hours or less in 2023, up from 12% in 2018. The EVOLVT RCT study demonstrated that transfemoral TAVR in low-risk patients could be safely conducted with discharge within 48 hours in 85% of cases, without increasing 30-day mortality or readmission rates. This trend is accelerating the development of dedicated outpatient TAVR centers; the Cleveland Clinic opened the first ambulatory TAVR suite in 2022 by reducing average costs by 28% and increasing procedural throughput.

MARKET CHALLENGES

Long-Term Durability and Structural Valve Deterioration in Younger Patients

The long-term durability of transcatheter heart valves as TAVR expands into younger, lower-risk populations with longer life expectancies is acting as a barrier for the growth of the Transcatheter Aortic Valve Replacement (TAVR) market.

Risk of Conduction Abnormalities and Permanent Pacemaker Implantation

The development of conduction disturbances, often necessitating permanent pacemaker (PPM) implantation, which increases morbidity, cost, and long-term device management, is likely to degrade the growth of the Transcatheter Aortic Valve Replacement (TAVR) market. As per the CoreValve US Pivotal Trial, the rate of PPM implantation following self-expanding valve deployment ranges from 15% to 30%, with higher incidences in patients with pre-existing right bundle branch block or greater valve oversizing. While newer valves with adaptive sealing and lower implantation depths have reduced PPM rates to 7–10%, as seen with the Lotus Edge, the risk remains a key consideration in patient counseling and procedural planning.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Surgery Method, Valve Frame Material, Valve Size, Valve Leaflets Material, End Users, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Edwards Lifesciences Corporation (U.S.), Medtronic, Inc. (Ireland), Boston Scientific Corporation (U.S.), Abbott Laboratories (U.S.), St. Jude Medical Inc. (U.S.), JenaValve Technology, Inc. (Germany), Symetis SA (Switzerland), Direct Flow Medical, Inc. (U.S.), |

SEGMENTAL ANALYSIS

By Surgery Method Insights

The transfemoral implantation segment was accounted for in holding a prominent share of the Transcatheter Aortic Valve Replacement (TAVR) market in 2024 with its minimally invasive nature, superior safety profile, and compatibility with the majority of patient anatomies. The transfemoral route, which accesses the aortic valve via the femoral artery, is associated with significantly lower rates of complications compared to alternative surgical pathways. According to the PARTNER 3 trial, patients undergoing transfemoral TAVR had a 39% lower risk of major vascular complications and a 54% reduction in life-threatening bleeding compared to transapical or transaortic approaches.

The transcaval implantation method segment is likely to grow with an expected CAGR of 26.8% in the coming years, with its role as a viable alternative for patients with no other percutaneous access options due to severe iliofemoral calcification or aortic occlusive disease. Transcaval access involves puncturing the inferior vena cava and deploying a closure device to seal the access site post-procedure, enabling valve delivery through the venous system. The U.S. Food and Drug Administration has cleared dedicated closure systems such as the Manta Vascular device, enhancing safety and reproducibility.

By Valve Frame Material Insights

The Nitinol segment was the largest by holding a significant share of the Transcatheter Aortic Valve Replacement (TAVR) market in 2024, which is attributable to Nitinol’s unique superelasticity, shape memory, and biocompatibility, which enable precise valve deployment and adaptive sealing within the native aortic annulus. Unlike rigid materials, Nitinol allows for controlled, gradual expansion of self-expanding valves such as Medtronic’s Evolut series, reducing the risk of annular rupture and conduction disturbances. Additionally, Nitinol’s fatigue resistance ensures long-term structural integrity under continuous cardiac pulsation for patient safety over time. In Japan, the Pharmaceuticals and Medical Devices Agency reports that all approved self-expanding TAVR devices utilize Nitinol frames with their regulatory and clinical acceptance. Furthermore, Nitinol’s compatibility with magnetic resonance imaging (MRI) post-implantation enhances long-term patient management.

The cobalt-chromium segment is swiftly emerging with a CAGR of 14.6% from 2025 to 2033, with its use in balloon-expandable valves such as Edwards Lifesciences’ Sapien series, which are increasingly favored for their precision, durability, and lower rates of permanent pacemaker implantation. Cobalt-chromium offers superior radial strength and fatigue resistance compared to stainless steel by allowing for thinner struts and a reduced valve profile for navigating tortuous anatomy. The PARTNER II trial found that cobalt-chromium valves had a 10.2% rate of new PPM implantation, significantly lower than the 18.7% observed with self-expanding Nitinol valves.

By Valve Size Insights

The 22mm to 29mm valve size segment was accounted in holding a prominent share of the Transcatheter Aortic Valve Replacement (TAVR) market in 2024. Edwards Lifesciences and Medtronic have optimized their commercial valve portfolios around this spectrum, with the Sapien 3 and Evolut PRO+ offering sizes from 23mm to 29mm to accommodate anatomical variability. The European Association of Cardio-Thoracic Surgery emphasizes that accurate sizing via pre-procedural CT angiography is necessary to prevent paravalvular leak or annular rupture, both of which are more likely with undersized or oversized implants. Additionally, newer-generation valves in this range feature adaptive sealing skirts and external tissue cuffs that enhance conformity and reduce leakage.

The 18mm to 22mm valve size segment is expected to witness a CAGR of 17.3% in the coming years with the expansion of TAVR into younger, lower-risk patients who often have smaller annular dimensions and are increasingly being treated with transcatheter valves. Additionally, women constitute nearly 60% of TAVR patients in Europe, as per EuroHeart IV, and typically have smaller annular sizes, increasing demand for this range. The U.S. Food and Drug Administration cleared the first 19mm TAVR valve in 2021, marking a shift toward personalized valve selection.

By End-User Insights

The hospitals segment was the accounted in holding a significant share of the Transcatheter Aortic Valve Replacement (TAVR) market in 2024 due to the complex, multidisciplinary nature of TAVR, which requires a dedicated heart team, hybrid operating rooms, advanced imaging systems, and intensive post-procedural monitoring resources concentrated in large academic and tertiary care centers. The Society of Thoracic Surgeons reports that over 650 hospitals in the United States are certified to perform TAVR, collectively conducting more than 100,000 procedures annually.

The ambulatory surgical centres (ASCs) segment is likely to grow with an expected CAGR of 22.4% during the forecast period, with the shift toward outpatient TAVR models for low- and intermediate-risk patients, supported by improved procedural safety, shorter recovery times, and cost-efficiency. The EVOLVT RCT trial demonstrated that 85% of low-risk TAVR patients could be safely discharged within 48 hours, making ASCs viable alternatives to traditional hospitals.

REGIONAL ANALYSIS

North America led the market and had the largest share of 34% of the global market in 2023. In contrast, the Asia-Pacific is estimated to grow at the highest CAGR of 21.20% during the forecast period. The United States dominated the market in 2023, accounting for over 45% of the transcatheter aortic valve implant market. It can be attributed to the high adoption of technologically advanced products, mergers and acquisitions, and favorable reimbursement policies. For example, reimbursement from government organizations such as the Centers for Medicare and Medicaid Services (CMS) helps patients opt for a transcatheter aortic valve replacement procedure. The primary payer for almost 92% of TAVR procedures was Medicare in 2019. It reinforced the economic advantage of TAVR over surgical aortic valve replacement (SAVR). The well-established healthcare industry can drive market growth in the region. The presence of several reputable market players who release continuous iterations of existing products can also play a critical role.

Europe accounted for a substantial share of the global market in 2024. Europe has similar growth factors to the Americas due to the increasing diagnosis of endovascular disease and a large senior population. In addition, the global transcatheter market will thrive in the region due to favorable regulations and many patients with sustainable income levels to pay for high-standard treatment. Recently, FEops received a USD 4.1 million fund to promote research and development of structural heart interventions. The Feops HEART Guide is a predictive planning guide that can provide information about the device's size and position during surgery to reduce injury risk.

APAC is predicted to witness the fastest CAGR in the global market during the forecast period. The presence of emerging economies, the growing prevalence of valvular heart diseases, particularly aortic stenosis, the increasing aging population in the Asia-Pacific region who are more prone to cardiovascular diseases, including aortic valve disorders, the growing number of investments to improve healthcare infrastructure including cardiac care facilities and specialized centers for cardiovascular interventions like TAVR primarily drive the market growth in the APAC region. The growing availability of advanced imaging systems and catheterization labs, the increasing number of well-trained interventional cardiologists and cardiac surgeons, the rising number of initiatives from the governments of APAC countries, and favorable reimbursement programs further contribute to the regional market growth. China, Japan, India, South Korea, and Australia are predicted to control the major share of the Asia-Pacific market during the forecast period.

Latin America is a noteworthy regional market for TAVR worldwide and is predicted to grow at a healthy CAGR during the forecast period. The MEA market accounted for a moderate share of the worldwide market in 2024 and is estimated to grow steadily during the forecast period.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Notable companies leading the Global TAVR Market profiled in the report are Edwards Lifesciences Corporation (U.S.), Medtronic, Inc. (Ireland), Boston Scientific Corporation (U.S.), Abbott Laboratories (U.S.), St. Jude Medical Inc. (U.S.), JenaValve Technology, Inc. (Germany), Symetis SA (Switzerland), Direct Flow Medical, Inc. (U.S.), Sorin Group (Italy), Meril Life Sciences India Pvt Ltd (India) and Braile Biomedica (Brazil).

The TAVR market is highly competitive, driven by technological innovation, clinical evidence, and global expansion efforts. Leading companies continuously refine valve designs to enhance procedural success and reduce complications such as paravalvular leak and conduction disturbances. The competition centers on product differentiation, with firms introducing valves featuring repositionable systems, lower-profile delivery devices, and improved durability. Clinical trial data plays a crucial role, as companies seek approvals for lower-risk and younger patient populations. Beyond product features, competition extends to training programs, physician support, and digital integration for pre-procedural planning and post-market surveillance. Edwards Lifesciences, Medtronic, and other emerging players engage in strategic partnerships, geographic expansion, and regulatory submissions to gain an advantage. The entry of new competitors and increasing regulatory scrutiny add pressure to demonstrate long-term safety and cost-effectiveness. Reimbursement landscapes and healthcare infrastructure also influence competitive dynamics across regions.

Top Players in the Market

Edwards Lifesciences Corporation

Edwards Lifesciences is a global leader in structural heart disease technologies and a pioneer in transcatheter aortic valve replacement (TAVR) therapies. The company developed the first FDA-approved transcatheter heart valve, SAPIEN, revolutionizing treatment for patients with severe aortic stenosis. Edwards continues to innovate with next-generation valve systems, including the SAPIEN 3 and SAPIEN X4, which offer improved delivery systems and reduced complications. The company actively invests in clinical trials to expand TAVR indications to lower-risk patient groups. Recently, Edwards launched the CENTERA THV in Europe, enhancing its European footprint. It also strengthened its global training programs for physicians and expanded manufacturing capacity to meet rising demand.

Medtronic plc

Medtronic is a key innovator in the TAVR market, offering the Evolut series of self-expanding transcatheter heart valves. Medtronic has expanded the use of its valves through robust clinical trials like the Evolut Low Risk Trial, supporting broader regulatory approvals. In recent years, the company launched the Evolut PRO+ in the U.S. and Europe, featuring enhanced sealing and reduced paravalvular leak. Medtronic has also invested in digital health integration, enabling remote monitoring and procedural planning tools. The company continues to strengthen its global commercial infrastructure and supports comprehensive training for structural heart teams.

Boston Scientific Corporation

Boston Scientific entered the TAVR market with the acquisition of Edwards’ rival, Direct Flow Medical, and later advanced with the development of the ACURATE neo2 and neo2 PRO valves through its partnership with Biotronik. However, the company has since refocused its structural heart strategy. Boston Scientific emphasizes innovation in delivery systems and valve design to improve procedural efficiency and patient outcomes. It has invested heavily in clinical research to support its technologies and expand into emerging markets. Recently, the company enhanced its structural heart portfolio by integrating imaging and navigation tools to support TAVR planning and execution. Boston Scientific also collaborates with key opinion leaders and hospitals to improve TAVR accessibility and training.

Top Strategies Used by the Key Market Participants

Key players in the TAVR market employ several strategic initiatives to maintain dominance and drive growth. Product innovation is central, with companies launching next-generation valves featuring improved deliverability, sealing, and reduced complications. Expanding clinical indications through robust trials allows broader patient eligibility. Geographic expansion, especially into Asia-Pacific and Latin America, helps tap into underserved markets. Strategic collaborations with hospitals and physicians enhance training and adoption. Companies also invest in digital health tools, including AI-based imaging and procedural planning platforms, to improve precision. Mergers and acquisitions enable rapid portfolio expansion and technology integration. Educational initiatives and real-world data collection strengthen clinical credibility. Additionally, manufacturers focus on streamlining manufacturing and supply chains to meet rising demand.

RECENT HAPPENINGS IN THE MARKET

- In April 2022, Medtronic received FDA approval for the Evolut PRO+ TAVR system, enhancing its U.S. market presence with a valve designed to reduce paravalvular leak and improve hemodynamic performance.

- In September 2022, Edwards Lifesciences launched the SAPIEN 3 Ultra with Annie Delivery System in Europe, offering improved maneuverability and control during complex TAVR procedures.

- In January 2023, Boston Scientific announced a strategic collaboration with Biotronik to co-develop and commercialize the ACURATE neo2 PRO valve, strengthening its structural heart portfolio.

- In June 2023, Edwards Lifesciences initiated the CENTERA CE Mark Trial in Europe, aiming to support approval of its next-generation valve with enhanced sealing technology.

- In November 2023, Medtronic expanded its TAVR training program globally, launching new Structural Heart Academies to enhance physician education and procedural standardization.

MARKET SEGMENTATION

This research report has segmented and sub-segmented the global TAVR market based on surgery method, valve frame material, valve size, valve leaflet material, end users and region.

By Surgery Method

- Transfemoral Implantation

- Transapical Implantation

- Transaortic Implantation

- Transcaval Implantation

By Valve Frame Material

- Nitinol

- Stainless Steel

- Cobalt-Chromium

By Valve Size

- 14mm to 18 mm

- 18mm to 22 mm

- 22mm to 29mm

By Valve Leaflets Material

- Bovine Heart Tissue

- Cow Heart Tissue

- Other Valve Leaflet Materials

By End Users

- Hospitals

- Ambulatory Surgical Centres

- Cardiac Catheterization Laboratories

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What factors are driving the growth of the TAVR market?

Edwards Lifesciences Corporation, Medtronic, Boston Scientific Corporation, Abbott Laboratories, and JenaValve Technology, Inc. are some of the notable companies in the TAVR market.

What are the major players in the TAVR market?

The global TAVR market size was worth USD 4.28 billion in 2024.

What are the challenges facing the TAVR market?

The growth of the TAVR market is primarily driven by the increasing prevalence of heart valve diseases, the rising adoption of minimally invasive procedures, and advancements in technology.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com