Global Women’s Health Market Size, Share, Trends & Growth Forecast Report By Age, Application and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034

Global Women’s Health Market Report Summary

The global women’s health market was valued at USD 50 billion in 2025, is estimated to reach USD 52.77 billion in 2026, and is projected to reach USD 81.23 billion by 2034, growing at a CAGR of 5.54% from 2026 to 2034. Market growth is driven by increasing awareness of women-specific health conditions, rising prevalence of chronic and reproductive health disorders, and growing focus on preventive healthcare. Advancements in diagnostics, therapeutics, and digital health solutions tailored for women are further supporting market expansion. Additionally, supportive government initiatives, improved access to healthcare services, and increasing investments in women’s health research are contributing to steady growth globally.

Key Market Trends

- Increasing focus on preventive and personalized women’s healthcare.

- Rising prevalence of reproductive and hormonal health disorders.

- Growing demand for contraceptives and fertility-related solutions.

- Expansion of digital health and telehealth services for women.

- Increasing investments in women-specific drug development and research.

Segmental Insights

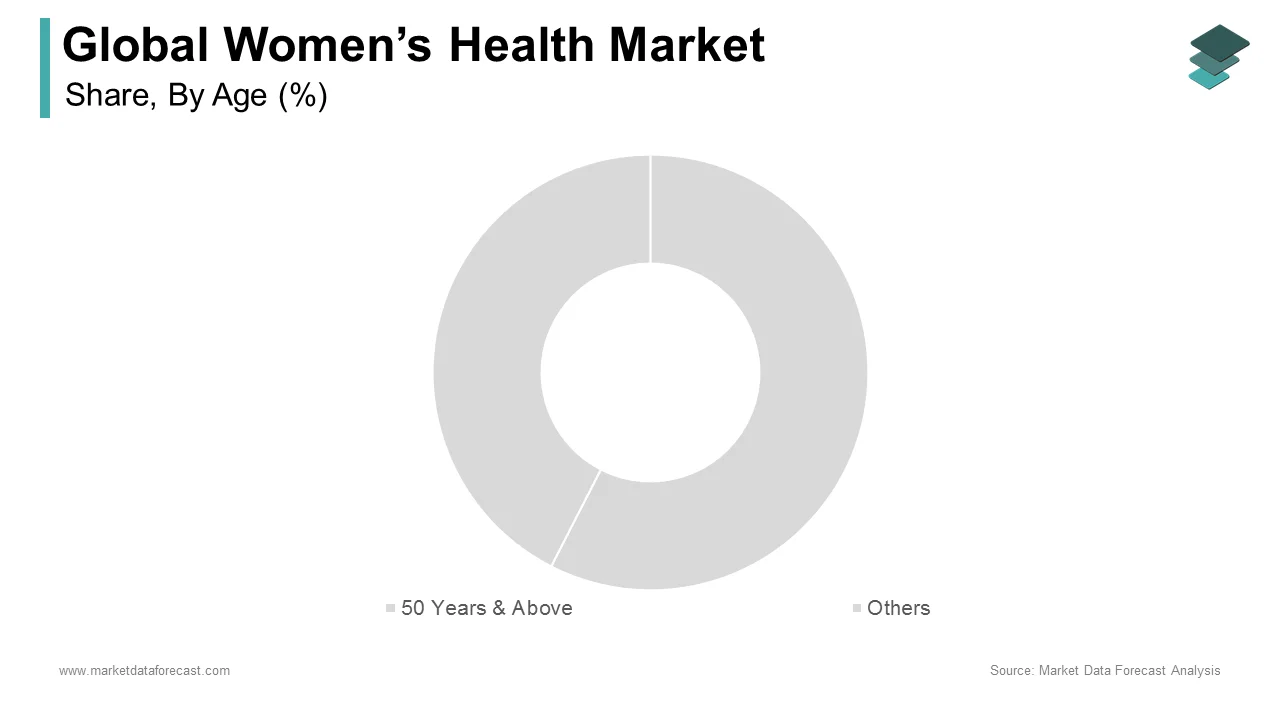

- Based on age, the 50 years & above segment dominated the global women’s health market by capturing 42.1% share in 2025, driven by higher incidence of age-related health conditions.

- Based on application, the contraceptives segment led the market with 34.2% share in 2025, supported by widespread usage and increasing awareness of family planning.

Regional Insights

The global women’s health market is witnessing steady growth across major regions due to improving healthcare access and rising awareness.

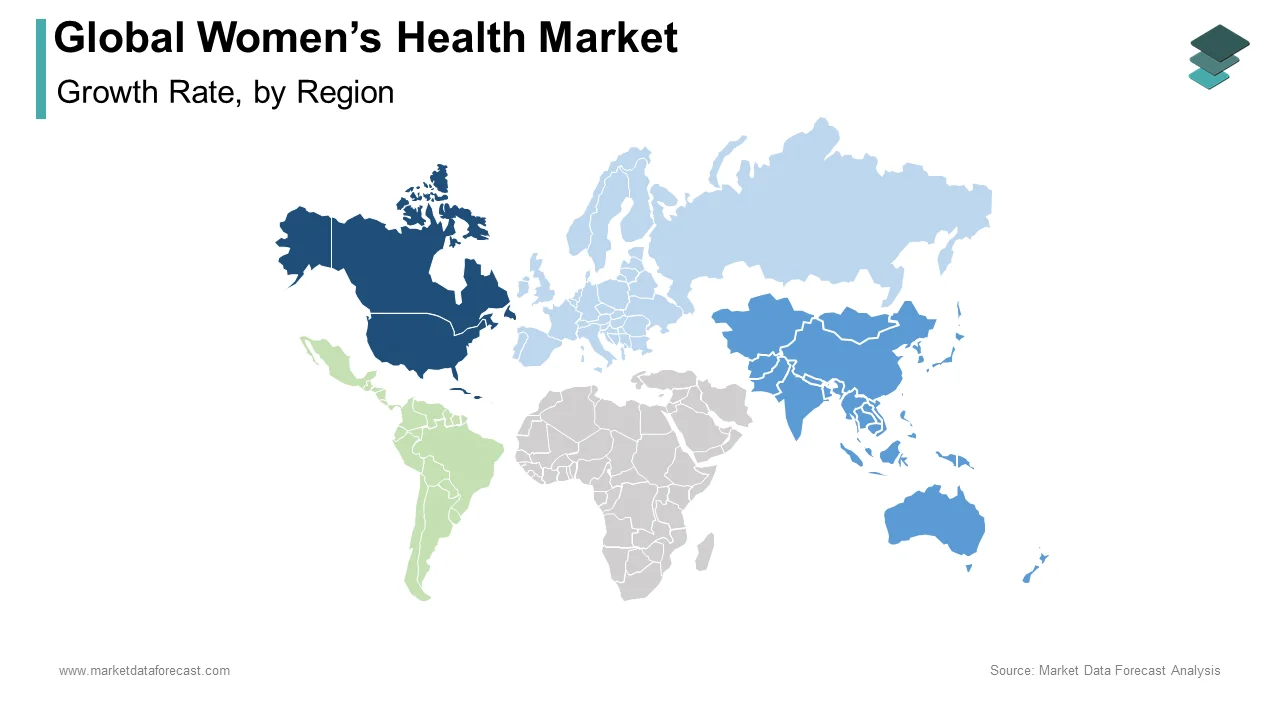

- North America led the market in 2025 with 39.3% share, supported by advanced healthcare infrastructure and high awareness levels.

- Europe followed with 27.4% share in 2025, driven by strong healthcare systems and government support.

- Asia-Pacific is emerging as the fastest-growing region due to large population base, improving healthcare infrastructure, and increasing awareness of women’s health issues.

Competitive Landscape

The global women’s health market is moderately competitive, with the presence of major pharmaceutical companies and healthcare providers focusing on innovation and expanding product portfolios. Companies are investing in research and development, strategic partnerships, and new product launches to strengthen their market position.

Prominent companies operating in the global women’s health market include Agile Therapeutics Inc., Ferring Pharmaceuticals, Mylan N.V., Lupin, Bayer AG, Blairex Laboratories, Apothecus Pharmaceutical, AbbVie Inc., Merck & Co. Inc., Eli Lilly and Company, Novartis AG, and Johnson & Johnson.

Global Women's Health Market Size

The size of the global women's health market was worth USD 50 billion in 2025. The global market is anticipated to grow at a CAGR of 5.54% from 2026 to 2034 and be worth USD 81.23 billion by 2034 from USD 52.77 billion in 2026.

Women's health refers to a branch of medicine that focuses on the treatment and diagnosis of diseases and conditions that affect a woman's physical and emotional well-being. This market extends beyond reproductive health to include menopause management, oncology, cardiovascular care, and mental wellness, recognizing the distinct biological trajectories women experience. The definition now includes femtech innovations that leverage artificial intelligence for early detection of conditions like endometriosis and breast cancer. According to World Bank data (2023), women constitute 49.7% of the global population. Despite this near-parity, women have historically been underrepresented in clinical trials, a legacy of exclusionary policies that has created a significant data gap in women's health that the current market is actively addressing. Data from the American Cancer Society indicates that one in eight women in the United States will develop invasive breast cancer in her lifetime. This high prevalence drives a critical, sustained demand for specialized screening technologies and advanced therapeutic interventions in the North American market. The market operates at the intersection of hormonal biology and personalized medicine, driven by a demographic shift where women are increasingly proactive about their long-term vitality. Eurostat reports that women in the European Union live on average 5.4 years longer than men (2022 data). This longevity gap has resulted in a growing demographic of elderly women, necessitating robust market expansion in chronic disease management and menopausal care. This longevity paradox necessitates robust healthcare solutions tailored to post-reproductive health stages. The sector is evolving from a niche focus on contraception to a holistic approach that integrates genetic profiling and lifestyle management to optimize female health outcomes globally.

MARKET DRIVERS

Rising Global Prevalence of Hormone-Related Chronic Conditions

The escalating incidence of hormone-dependent chronic diseases requires lifelong management and specialized therapeutic interventions, which boost the growth of the women’s health market. Examples of these conditions include polycystic ovary syndrome, endometriosis, and osteoporosis. These conditions affect a substantial portion of the female population, creating a sustained and growing demand for both pharmacological and non-pharmacological treatments. According to statistics from the World Endometriosis Research Foundation, endometriosis affects approximately 10 percent of women and girls of reproductive age worldwide, translating to roughly 190 million individuals who suffer from chronic pain and infertility. Similarly, the International Osteoporosis Foundation reports that one in three women over the age of 50 will experience osteoporotic fractures, a rate significantly higher than that of men, driving the need for bone density monitoring and anabolic therapies. The Centers for Disease Control and Prevention notes that polycystic ovary syndrome impacts up to 12 percent of women of reproductive age in the United States alone, leading to increased risks of diabetes and cardiovascular disease. This high prevalence forces healthcare systems to prioritize dedicated care pathways, fueling investment in novel drug delivery systems and minimally invasive surgical devices. The chronic nature of these ailments ensures recurring revenue streams for manufacturers of hormonal regulators and diagnostic tools. Furthermore, increased awareness and reduced stigma around these conditions are encouraging more women to seek medical help, expanding the addressable patient pool beyond those with severe symptoms to include individuals seeking early intervention and quality of life improvements.

Demographic Shift Toward an Aging Female Population

The global demographic transition toward an aging population, in which women represent the majority of older adults, further propels the expansion of the global women’s health market. This shift is amplifying the demand for age-specific health solutions, including menopause management and geriatric care. Women now spend a significantly larger proportion of their lives in post-menopausal states due to rising life expectancy. These extended years often involve navigating serious health issues, including urogenital atrophy and cardiovascular diseases tied to decreasing estrogen levels. As per data from the United Nations Department of Economic and Social Affairs, women aged 65 and older outnumber men in almost every country, with this gap widening in developed nations where female longevity is most pronounced. The North American Menopause Society indicates that over 6000 women enter menopause every day in the United States, creating a massive daily influx of patients seeking relief from vasomotor symptoms and metabolic changes. Eurostat emphasizes that by the middle of the century, a significant portion of the European population will consist of older adults, with women comprising the majority of this aging demographic. This shift drives the market for hormone replacement therapies, non-hormonal alternatives, and supplements tailored to senior women. Additionally, the aging female population requires specialized screening for cancers that predominantly affect older women, such as breast and ovarian cancer, further stimulating the diagnostics and therapeutics sectors. The economic power of this demographic, often controlling significant household wealth, allows for higher spending on premium health products and wellness services, making them a highly attractive target for innovation and market expansion.

MARKET RESTRAINTS

Historical Underrepresentation in Clinical Research and Data Gaps

The persistent historical exclusion of women from clinical trials is the primary obstacle to the optimal development of the women’s health market. As a result, there are substantial data gaps regarding drug efficacy, dosing, and safety profiles specific to female physiology. For decades, regulatory guidelines and research protocols often excluded women of childbearing potential to avoid liability related to fetal harm, leading to a knowledge base derived primarily from male subjects. An analysis of cardiovascular drug trials supporting FDA approvals (2005–2015) found that women represented only about one-third of participants, despite heart disease being the leading cause of death for women. Research into sex bias in biomedical research reveals that neuroscience has historically excluded female animals at high rates (with male-only studies vastly outnumbering female-only ones), which skews the understanding of neurological disorders. This lack of sex-specific data forces clinicians to prescribe medications based on extrapolated male data, potentially leading to adverse events or suboptimal therapeutic outcomes for female patients. The resulting uncertainty discourages pharmaceutical companies from investing heavily in female-specific indications due to the perceived regulatory risks and the complexity of designing trials that account for hormonal cycles. Furthermore, the absence of robust longitudinal data on female health trajectories limits the ability of developers to create precision medicine solutions. Regulatory bodies need to enforce stricter mandates for sex-disaggregated data and funding agencies must prioritize female-inclusive research. Without this, systemic bias will continue to slow the pace of innovation and limit the availability of tailored treatments.

Socio-Cultural Stigma and Barriers to Care Access

Deep-rooted socio-cultural stigma surrounding women's health issues, such as menstruation, infertility, sexual dysfunction, and menopause, is a critical restraint to the global women’s health market. It prevents many women from seeking timely medical attention. In many cultures globally, discussions about reproductive health are considered taboo, leading to silence, shame, and the normalization of severe symptoms that should be treated medically. Independent surveys (such as those by Jo's Cervical Cancer Trust in the UK) have found that nearly half of young women delay gynecological screenings specifically due to embarrassment, a trend often conflated with global data. The Guttmacher Institute highlights that restrictive laws and limited access to reproductive health services in certain regions further exacerbate these barriers, forcing women to rely on unsafe or ineffective remedies. In conservative societies, the decision-making power regarding healthcare often lies with male family members, delaying diagnosis and treatment for conditions like cervical cancer or endometriosis. Data from UNESCO estimates that one in ten adolescent girls in Sub-Saharan Africa misses school during their menstrual cycle due to a lack of hygiene facilities, creating a gender gap in educational attainment that affects long-term life outcomes. This cultural suppression reduces the effective market size for advanced therapies as a large segment of the potential patient population remains undiagnosed or untreated. Consequently, market players face difficulties in penetrating these regions and educating consumers, as marketing efforts must navigate sensitive cultural norms that restrict open communication about female bodily functions.

MARKET OPPORTUNITIES

Explosion of Femtech and Digital Health Solutions

The rapid proliferation of femtech creates new opportunities for the growth of the women’s health market. Femtech is a sector utilizing software, diagnostics, and connected devices to address specific female health needs through personalized digital interventions. This domain includes apps for cycle tracking, telehealth platforms for menopause support, and wearable devices for monitoring fertility and pregnancy, offering scalable solutions that bypass traditional healthcare bottlenecks. According to investment data from Rock Health, femtech startups have seen a resilient flow of venture capital, signaling sustained investor confidence in the scalability of digital female health tools despite broader market fluctuations. The global adoption of smartphones among women, which the International Telecommunication Union reports has reached parity with men in many regions, provides a ready infrastructure for deploying these solutions. Artificial intelligence algorithms can now predict ovulation windows with over 98 percent accuracy by analyzing basal body temperature and hormonal markers, empowering women with actionable insights previously available only through clinical testing. Furthermore, telemedicine platforms have democratized access to specialists for conditions like pelvic floor dysfunction, allowing women in rural areas to receive expert care without travel. Research suggests that digital health engagement is notably higher among women than men, driven by a desire for convenient and discreet care management. Companies that integrate these digital tools with traditional therapeutics can create closed-loop ecosystems that enhance patient adherence and outcomes. The potential to aggregate vast amounts of real-world data from these devices also offers unprecedented opportunities for research and drug development, closing the historical data gap.

Expansion of Personalized Medicine and Genetic Profiling

The advent of personalized medicine and accessible genetic profiling provides a path to tailor women’s health interventions based on individual genomic signatures, which is likely to promote the expansion of the global women’s health market. This is particularly relevant in the fields of oncology and reproductive health. Advances in next-generation sequencing allow for the identification of specific mutations such as BRCA1 and BRCA2, enabling proactive risk management and targeted therapies for breast and ovarian cancers. As per findings from the American Society of Clinical Oncology, genetic testing has become the standard of care for many female cancers, guiding treatment decisions that improve survival rates compared to empirical approaches. The decreasing cost of genome sequencing makes these tests accessible to a broader population, driving demand for companion diagnostics and targeted drugs. In reproductive health, preimplantation genetic testing allows couples to screen embryos for chromosomal abnormalities, increasing success rates for in vitro fertilization procedures. The European Society of Human Reproduction and Embryology indicates that the use of genetic screening in IVF cycles has doubled in the last five years. Furthermore, pharmacogenomics is emerging as a tool to optimize hormone replacement therapy dosing, minimizing side effects and maximizing efficacy for menopausal women. Providers can offer superior outcomes and foster patient loyalty by shifting from a one-size-fits-all model to precision health. In turn, this opens new revenue streams for laboratories and biotech firms specializing in female genomics.

MARKET CHALLENGES

Complex Regulatory Pathways for Reproductive and Hormonal Therapies

The intricate and often stringent regulatory landscape governing reproductive health products and hormonal therapies acts as a serious barrier slowing down the growth of the global women’s health market. This landscape varies significantly across jurisdictions and can delay product launches. Regulatory bodies like the Food and Drug Administration and the European Medicines Agency impose rigorous safety requirements for drugs affecting fertility, pregnancy, and hormonal balance due to the potential risks to fetal development and long-term metabolic health. Regulatory guidelines for contraceptives and hormone therapies necessitate rigorous long-term safety monitoring given the healthy patient population, which can extend development timelines; however, industry analyses consistently identify chronic underinvestment and reimbursement challenges. The classification of certain reproductive technologies as medical devices versus drugs adds another layer of complexity, requiring different validation protocols and clinical evidence standards. Major studies identify limited access to venture capital and early-stage funding, rather than regulatory uncertainty, as the primary barrier for biotech firms entering the women’s health space, with gene therapy applications in this sector remaining in nascent stages of development. Furthermore, changing political landscapes in various countries can lead to sudden shifts in policy regarding reproductive rights, creating an unstable environment for investment and commercialization. The requirement for diverse clinical trial populations that accurately reflect hormonal fluctuations adds cost and logistical difficulty to study designs. Regulatory frameworks must become more harmonized and adaptive to the nuances of female biology. Until then, the path to market for breakthrough women’s health innovations will remain arduous and unpredictable.

Significant Disparities in Global Access and Healthcare Equity

The profound disparity in access to women’s health services and products between developed and developing nations further obstructs the expansion of the global women’s health market. This gap limits market penetration and perpetuates poor health outcomes for billions of women. While advanced therapies and digital tools are readily available in high-income countries, vast populations in low-resource settings lack access to basic essentials like cervical cancer screening, safe contraception, and maternal care. As per data from the World Bank, maternal mortality ratios in sub-Saharan Africa remain 40 times higher than in Europe, reflecting a catastrophic failure in healthcare delivery infrastructure. The United Nations Population Fund reports that over 250 million women in developing regions have an unmet need for family planning, often due to supply chain disruptions, cost barriers, or lack of trained personnel. This inequity creates a fragmented market where high-margin innovations thrive in the West while basic needs go unmet elsewhere, complicating global strategies for pharmaceutical and device companies. Economic instability and currency fluctuations in emerging markets further hinder the affordability of imported medicines and technologies. Recent economic reports from major global forums indicate that the investment gap for broad women’s health conditions, spanning beyond reproductive health to chronic diseases, has persisted, leaving a significant portion of the global female population underserved despite the potential for substantial economic returns. Addressing these disparities requires innovative business models, public-private partnerships, and localized manufacturing, but progress is slow. The global women’s health market will remain bifurcated until equitable access becomes a reality. This bifurcation prevents the market from fully realizing its potential to improve lives universally.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Age, Application, and Country. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East & Africa. |

| Market Leaders Profiled | Agile Therapeutics Inc., Ferring Pharmaceuticals, Mylan N.V., Lupin, Blairex Laboratories, Apothecus Pharmaceutical, Eli Lilly and Company, Novartis AG, and Johnson & Johnson. |

SEGMENTAL ANALYSIS

By Age Insights

In 2025, the 50 Years & Above segment remained the largest segment in the global women's health market and occupied a share of 42.1%. This dominance of the segment is driven by the sheer volume of the aging female population and the complex array of chronic conditions that emerge post-menopause, requiring sustained medical intervention and monitoring. One of the main market drivers of this segment is the unprecedented global increase in the number of women living beyond age 50, which directly correlates with a higher prevalence of age-related chronic diseases such as osteoporosis, cardiovascular disorders, and cognitive declineUnlike younger demographics who may only require intermittent care for reproductive issues, this cohort necessitates lifelong management of multiple comorbidities, driving recurring revenue for pharmaceutical and device manufacturers. Furthermore, the North American Menopause Society indicates that women spend approximately one-third of their lives in post-menopause, a period characterized by significant physiological changes that require specialized healthcare solutions. The economic power of this demographic, particularly in developed nations where they often control substantial household wealth, allows for higher spending on premium health products and wellness services. This combination of population growth, extended life expectancy, and high disease burden ensures that the 50 Years & Above segment remains the financial cornerstone of the women's health market. A further reason for this growth is the shifting societal paradigm that prioritizes quality of life and active aging for women past reproductive age, leading to greater utilization of hormone replacement therapies, bone health supplements, and mental wellness services. Historically, menopause was viewed as a natural transition to be endured, but modern medical perspectives frame it as a treatable condition impacting long-term vitality. As per studies, a significant share of women now seek medical assistance for menopausal symptoms such as hot flashes, sleep disturbances, and mood swings, a significant increase from previous decades. This cultural shift has destigmatized treatments like bioidentical hormone therapy and non-hormonal alternatives, expanding the addressable market for pharmaceutical companies. Additionally, the rising awareness of the link between estrogen loss and Alzheimer's disease has spurred investment in neuroprotective therapies tailored for older women. Healthcare providers are increasingly offering comprehensive "menopause clinics" that address physical, emotional, and sexual health holistically. This proactive approach to aging transforms the 50 plus demographic from passive recipients of care into active consumers of advanced health solutions, solidifying the segment's dominant market position through diversified service uptake.

The Endometriosis & Uterine Fibroids segment is estimated to register the fastest CAGR of 8.9% from 2026 to 2034. Factors such as improved diagnostic capabilities, reduced stigma, and the introduction of novel non-surgical therapeutic options targeting these debilitating conditions fuel the rapid growth of this segment. The exceptional growth rate of this segment is primarily driven by revolutionary advancements in non-invasive diagnostic technologies that have significantly reduced the time to diagnosis for endometriosis and uterine fibroids, historically known for being underdiagnosed or misdiagnosed for years. For decades, definitive diagnosis required invasive laparoscopic surgery, deterring many patients and delaying treatment initiation. However, the advent of high-resolution transvaginal ultrasound, specialized MRI protocols, and emerging blood-based biomarker tests has transformed the diagnostic landscape. According to research, the implementation of specialized ultrasound imaging has increased the detection rate of deep infiltrating endometriosis compared to standard examinations. A study notes that the average delay in diagnosis has decreased in regions with access to advanced imaging, bringing millions of previously undiagnosed women into the treatment pipeline. Furthermore, artificial intelligence algorithms are now being deployed to analyze medical images with greater accuracy than human radiologists, identifying subtle markers of fibroids and lesions earlier in the disease progression. Research indicates that early detection leads to more conservative and effective management strategies, increasing patient engagement with healthcare systems. As these technologies become more widely available and affordable, the pool of diagnosed patients expands rapidly, driving immediate demand for pharmacological and interventional treatments. In addition, this area is supported by the recent approval and commercialization of novel pharmacological agents and minimally invasive surgical techniques that offer effective relief without the need for hysterectomy or extensive recovery time. Historically, treatment options were limited to painkillers, hormonal contraceptives with significant side effects, or major surgery, leaving many women underserved. The introduction of gonadotropin-releasing hormone antagonists and selective progesterone receptor modulators has provided targeted therapies that shrink fibroids and reduce endometriotic lesions with fewer systemic effects. Additionally, innovations such as focused ultrasound surgery and radiofrequency ablation allow for the destruction of fibroid tissue through small incisions or no incisions at all, preserving fertility and reducing hospital stays. Pharmaceutical companies are also investing heavily in pipeline drugs targeting specific inflammatory pathways involved in endometriosis pain. This influx of effective, less invasive options encourages women who previously resigned themselves to suffering to seek treatment, thereby accelerating market growth and expanding the therapeutic landscape for these common gynecological disorders.

By Application Insights

The Contraceptives segment maintained dominance in the global women's health market and accounted for a 34.2% share in 2025. This dominance of the segment is attributed to the universal and recurring need for family planning across all reproductive-age demographics, supported by robust government initiatives and widespread availability of diverse product formats. The primary factor driving the domination of contraceptives is the sustained global emphasis on family planning as a cornerstone of public health, economic development, and women's empowerment, leading to widespread government subsidies and distribution programs. Access to reliable contraception is recognized by international bodies as essential for reducing maternal mortality and enabling educational and economic participation for women. Governments in developing nations often provide free or subsidized contraceptives, ensuring high volume uptake even in low-income populations. Furthermore, the diversification of contraceptive methods, ranging from long-acting reversible contraceptives like intrauterine devices to daily pills and patches, allows women to choose options that fit their lifestyles, broadening market penetration. The recurring nature of these products, whether through monthly refills or periodic device replacements, ensures a stable and dominant market position that outweighs episodic treatments for other conditions. Also, this segment is boosted by the continuous innovation in contraceptive delivery mechanisms designed to improve user compliance, reduce side effects, and offer greater convenience, thereby retaining users and attracting new adopters. Traditional methods often suffered from adherence issues due to daily dosing requirements or unpleasant side effects, but newer formulations and devices address these pain points effectively. The development of non-hormonal copper IUDs and hormone-releasing IUDs that last up to seven years has revolutionized the market by offering "set and forget" protection, appealing to women seeking long-term reliability without daily maintenance. Furthermore, advancements in biodegradable implants and microarray patches promise to eliminate the need for clinical removal procedures, further enhancing user experience. Manufacturers are also focusing on reducing androgenic side effects in progestin-only pills to minimize acne and weight gain concerns. These technological improvements transform contraception from a grudging necessity into a manageable and integrated part of women's health routines, securing the segment's leading market share through superior product performance and user satisfaction.

The Polycystic Ovary Syndrome (PCOS) segment is anticipated to witness the fastest CAGR of 9.4% during the forecast period due to rising diagnosis rates, the recognition of PCOS as a metabolic disorder requiring multidisciplinary care, and the launch of targeted therapeutics. A key driver for this fast growth is the escalating global prevalence of the condition, which is strongly correlated with rising obesity rates and sedentary lifestyles that exacerbate insulin resistance, a key pathophysiological feature of PCOS. As the global obesity epidemic worsens, the incidence of PCOS is climbing sharply, bringing millions of additional women into the diagnostic and treatment funnel. The condition's association with type 2 diabetes, cardiovascular disease, and infertility necessitates long-term management involving endocrinologists, gynecologists, and nutritionists, multiplying the touchpoints for healthcare spending. As urbanization spreads in developing nations, lifestyle shifts are triggering earlier onset of PCOS, expanding the affected demographic to include teenagers and young adults. This convergence of lifestyle trends and biological susceptibility ensures a steep growth trajectory for diagnostics, medications, and lifestyle interventions targeting PCOS. This segment is supported by the shift toward holistic, multidisciplinary treatment approaches for PCOS that integrate pharmacological therapy with digital health tools, nutritional counseling, and mental health support, creating a broader ecosystem of care. Unlike conditions treated solely with a single drug, PCOS management increasingly involves a combination of metformin, anti-androgens, fertility agents, and lifestyle modifications, increasing the overall value per patient. The rise of femtech startups specifically targeting PCOS has created a booming sub-sector offering personalized coaching and community support, attracting significant venture capital investment. Furthermore, the growing understanding of the mental health impact of PCOS, including anxiety and depression, has led to the inclusion of psychological services in treatment plans, further expanding the market scope. Pharmaceutical companies are also developing novel drugs targeting specific metabolic pathways involved in PCOS, moving beyond off-label use of existing medications. This comprehensive evolution in care delivery transforms PCOS from a niche gynecological issue into a major chronic disease management category, fueling its status as the fastest-growing segment.

REGIONAL ANALYSIS

North America Women’s Health Market Analysis

North America led the global women's health market and captured a 39.3% share in 2025. This supremacy of the North American market is driven by its advanced healthcare infrastructure, high per capita spending on health, and a progressive regulatory environment that accelerates the approval of innovative therapies and devices. The United States is the main supporter of growth, driven by a highly developed pharmaceutical sector and a strong culture of proactive health management among women. The presence of major biotechnology hubs in Boston, San Francisco, and San Diego fosters rapid innovation in areas like fertility preservation, oncology, and menopause management. The Food and Drug Administration has been instrumental in fast-tracking approvals for female-specific drugs, including the first dedicated treatments for hypoactive sexual desire disorder and postpartum depression. Furthermore, the high prevalence of chronic conditions such as obesity and autoimmune diseases among American women drives robust demand for therapeutic interventions. The region also leads in the adoption of digital health tools and telemedicine, with a portion of women using apps for health tracking. Despite challenges related to insurance coverage disparities, the sheer volume of innovation and purchasing power ensures that North America remains the most lucrative and influential market for women's health globally.

Europe Women’s Health Market Analysis

Europe followed closely behind in the global women's health market and occupied a 27.4% share in 2025. This growth of the European market is propelled by strong government-funded healthcare systems, stringent safety regulations, and a growing focus on gender-specific medicine. The region presents a mature market where public policy plays a decisive role in shaping access to contraceptives, cancer screening, and menopause care. The European market is distinguished by the influence of the European Medicines Agency and national health services that prioritize equitable access to essential women's health services across member states. Countries like Germany, France, and the United Kingdom are leading the adoption of advanced diagnostic technologies for breast and cervical cancer, supported by nationwide screening programs that ensure high participation rates. The region is also at the forefront of regulatory changes regarding hormone replacement therapy, with updated guidelines encouraging safer usage for menopausal women. Furthermore, the European Union's commitment to gender equality in health research mandates the inclusion of women in clinical trials, addressing historical data gaps. While cost-containment measures in some countries pressure pricing, the comprehensive coverage provided by public systems ensures stable demand. The rising awareness of endometriosis and the establishment of specialized care centers across the continent further stimulate market growth, making Europe a critical hub for high-quality, regulated women's health solutions.

Asia-Pacific Women’s Health Market Analysis

The Asia-Pacific region is emerging as the most dynamic and rapidly expanding player in the global market due to the massive populations of China and India, improved healthcare infrastructure, and rising awareness of women's health issues. While historically underserved, the region is undergoing a transformative shift driven by economic growth and changing social norms. China and India are at the forefront of this expansion, driven by government initiatives to improve maternal health and expand access to family planning and cancer screening for their billions of citizens. In India, the Ayushman Bharat scheme aims to provide health insurance to millions of low-income families, significantly increasing access to surgical and pharmaceutical interventions for conditions like fibroids and complications of pregnancy. Japan, with its super-aged society, drives demand for menopause management and osteoporosis treatments, maintaining high standards of care. The rising middle class is increasingly willing to spend on premium fertility treatments and aesthetic gynecological procedures. Furthermore, the proliferation of mobile health platforms in Southeast Asia is bridging the gap between urban specialists and rural patients. Although challenges remain regarding infrastructure and affordability, the sheer scale of the population and the rapid pace of modernization position Asia-Pacific as the primary growth engine for the future of the women's health market.

Latin America Women’s Health Market Analysis

Latin America witnessed consistent growth in the global market, supported mainly by Brazil and Mexico where healthcare reforms, a growing private sector, and increasing female workforce participation are beginning to unlock the sector. The region benefits from high fertility rates in some areas and a rising burden of chronic diseases, creating a dual demand for reproductive and age-related care. Brazil is the leading player in the region, boasting the most sophisticated healthcare system in Latin America and a high rate of cesarean sections and cosmetic gynecological procedures, reflecting a strong cultural emphasis on female aesthetics and reproductive control. In Mexico, proximity to the United States facilitates the flow of medical trends and technologies, with increasing adoption of latest-generation contraceptives and menopause therapies. However, the region faces challenges related to economic volatility and unequal access between urban and rural populations. Despite these hurdles, the growing awareness of rights regarding reproductive health and the increasing prevalence of lifestyle diseases like diabetes among women are driving market expansion. The rise of female entrepreneurship and economic independence is also empowering women to invest more in their own health, fostering a conducive environment for market growth in the coming decade.

Middle East and Africa Women’s Health Market Analysis

The Middle East and Africa region is anticipated to expand notably in the global women's health market over the forecast period by showing pockets of high potential in Gulf Cooperation Council countries and South Africa. However, it is constrained by infrastructure deficits, cultural barriers, and political instability in some areas. The region represents a long-term frontier where gradual investments in healthcare and shifting social dynamics could unleash substantial demand. South Africa and the Gulf states serve as the anchors of advancement in the region, with state-of-the-art medical cities in Saudi Arabia and the UAE importing the latest women's health technologies and therapies. However, the broader African continent faces significant challenges. Efforts by international NGOs and governments to expand vaccination programs for HPV and distribute contraceptives are slowly building the foundation for a robust market. As education levels rise and cultural stigma around women's health begin to erode, particularly among younger generations, the Middle East and Africa are expected to transition from a marginal player to a meaningful contributor to the global market. This growth is expected particularly for essential health products and increasingly for advanced therapies in affluent enclaves.

COMPETITIVE LANDSCAPE

The competition in the women's health market is characterized by a dynamic mix of large pharmaceutical conglomerates and agile biotechnology startups vying to address historically underserved areas such as endometriosis and menopause. Major players compete fiercely on innovation launching first-in-class therapies that offer better safety profiles and efficacy compared to traditional hormonal treatments. The landscape is shifting from a sole focus on contraception to a holistic approach encompassing chronic disease management and digital wellness solutions. Rivalry often manifests through strategic collaborations with femtech companies to integrate data-driven insights into product development and patient care. Smaller niche firms differentiate themselves by targeting specific rare diseases or offering personalized medicine solutions that big pharma overlooks. Pricing pressure remains significant in generic contraceptive segments while premium pricing is sustainable for novel specialty drugs. Regulatory hurdles regarding reproductive health create barriers that favor established companies with robust compliance frameworks. Ultimately the battle for market share is increasingly fought on the ability to combine scientific breakthroughs with empathetic patient engagement and comprehensive care ecosystems that empower women globally.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global women's health market include

- Agile Therapeutics Inc.

- Ferring Pharmaceuticals

- Mylan N.V.

- Lupin

- Bayer AG

- Blairex Laboratories

- Apothecus Pharmaceutical

- AbbVie Inc

- Merck & Co Inc

- Eli Lilly and Company

- Novartis AG

- Johnson & Johnson

TOP PLAYERS IN THE MARKET

- Bayer AG stands as a global powerhouse in the women's health sector with a historic and extensive portfolio of contraceptive solutions and hormonal therapies. The company plays a pivotal role in providing access to family planning products worldwide through its diverse range of oral contraceptives, intrauterine devices, and patches. Recent actions include the strategic expansion of its digital health offerings by integrating apps that support cycle tracking and medication adherence for users of its contraceptive products. Bayer has also invested heavily in research and development to launch next-generation non-hormonal treatments for heavy menstrual bleeding. The firm actively collaborates with global health organizations to improve access to contraception in developing nations. Bayer is strengthening its market position as a leader dedicated to empowering women through comprehensive reproductive health solutions and advanced therapeutic options. They achieve this by focusing on innovation in both pharmaceutical and device categories.

- AbbVie Inc has established a dominant presence in the women's health market particularly through its leadership in treating endometriosis and uterine fibroids with specialized hormonal therapies. The company leverages its robust immunology and neuroscience expertise to develop targeted treatments that address the complex pain and inflammatory symptoms associated with these conditions. Recent actions involve the acquisition of specialized biotech firms to bolster its pipeline for non-surgical interventions in gynecological health. AbbVie has also launched extensive patient support programs to help women navigate insurance coverage and manage chronic symptoms effectively. The firm continues to invest in clinical trials exploring new mechanisms of action for managing menopausal symptoms and reproductive disorders. By prioritizing patient-centric innovation and expanding its therapeutic arsenal AbbVie reinforces its status as a critical partner for women seeking relief from debilitating gynecological conditions and improves quality of life globally.

- Merck & Co Inc is a key contributor to the women's health market renowned for its vaccines preventing cervical cancer and its broad portfolio of fertility and contraceptive products. The company plays an essential role in global public health by distributing the human papillomavirus vaccine which significantly reduces the incidence of cervical cancer among women worldwide. Recent actions include the expansion of manufacturing capabilities to meet the surging global demand for its vaccines and fertility treatments. Merck has also partnered with digital health startups to create integrated platforms that support women through their fertility journeys and pregnancy. The firm is actively researching novel therapies for ovarian cancer and other female-specific malignancies. By combining preventive care with advanced treatment options Merck strengthens its market position as a guardian of women's long-term health. Their commitment to accessibility and scientific excellence ensures they remain at the forefront of efforts to reduce cancer rates and support reproductive goals.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the women's health market primarily employ strategic acquisitions and partnerships to expand their product portfolios and gain access to innovative technologies in fertility and gynecological care. Companies frequently invest heavily in research and development to create novel non-hormonal therapies and targeted treatments for conditions like endometriosis and menopause. Another major strategy involves the integration of digital health tools and mobile applications to enhance patient engagement and improve medication adherence among female consumers. Market participants are also focusing on expanding their global reach by entering emerging markets where demand for contraceptives and maternal care is rising rapidly. Building strong advocacy networks and patient support programs helps firms build brand loyalty and address the stigma surrounding certain women's health issues. Additionally, companies are diversifying their distribution channels by leveraging telemedicine platforms to provide direct-to-consumer access to prescriptions and consultations. These strategies collectively enable leaders to drive growth and address unmet needs in the evolving landscape.

MARKET SEGMENTATION

This research report on the global women's health market has been segmented and sub-segmented based on age, application & region.

By Age

- 50 Years & Above

- Endometriosis & Uterine Fibroids

- Menopause

- Others

By Application

- Menopause

- Contraceptives

- Hormonal infertility

- Endometriosis and uterine fibroids

- Hormonal infertility

- Polycystic ovary syndrome (PCOS)

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Which regions dominate the global women's health market?

North America dominates the global women's health market, accounting for over 43% share in 2024, supported by strong healthcare infrastructure and active health initiatives

2. What factors drive growth in the global women's health market?

Growth drivers include rising awareness of women-specific health issues, increasing chronic disease prevalence, government initiatives, and innovations in personalized and telehealth care

3. How does technology impact the global women's health market?

Advances in telehealth, wearable devices, AI diagnostics, and women's health apps improve accessibility and personalized care, expanding the global women's health market

4. What role do women's health apps play in the market?

Women's health apps aid in fertility tracking, menopause management, and mental health support, accelerating growth in the global women's health market through digital health solutions

5. What are primary health conditions in the global women's health market?

Key conditions include breast and cervical cancer, osteoporosis, menopause-related disorders, and mental health, driving demand for specialized treatments and diagnostics

6. How does aging population influence the global women's health market?

An increasing geriatric female population boosts demand for menopause care, osteoporosis management, and chronic disease treatments in the global women's health market

7. What are the challenges in the global women's health market?

Challenges include high treatment costs, regulatory complexities, social stigma around certain conditions, and access disparities in emerging markets

8. How does mental health factor into the global women's health market?

Growing recognition of mental health's role in women's overall health expands specialized services, enhancing the global women's health market's scope

9. What are prominent trends in the global women's health market?

Trends include personalized medicine, non-hormonal contraceptives, fertility technology advances, and integrated care models focusing on comprehensive women's wellness

10. How does maternal health contribute to the global women's health market?

Improved pregnancy monitoring and maternal care reduce mortality and morbidity, positively affecting growth in the global women's health market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com