Global Indoor Farming Market Size, Share, Trends & Growth Forecast Report, Segmented By Technology (Hardware, Software & Services, Integrated System), Installation (Greenhouse, Indoor Vertical Farm, Container Farms), Cultivation Method (Hydroponics, Aeroponics, Aquaponics, Soil-Based and Hybrid), Product (Vegetables, Fruits, Microgreens and Herbs, Medicinal Crop, and Others), (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis (2026 to 2034)

Global Indoor Farming Market Size

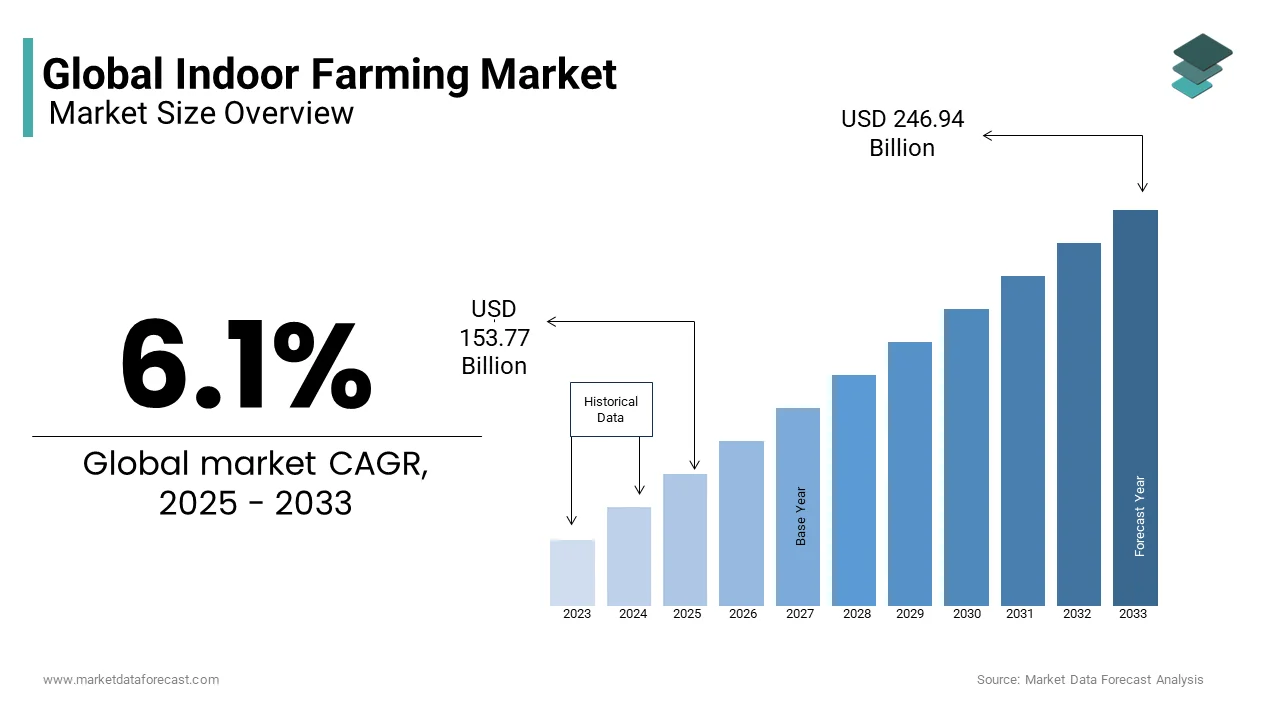

The global indoor farming market size was valued at USD 153.77 billion in 2025, and it is anticipated to reach USD 163.15 billion in 2026, and to USD 262.01 billion by 2034, growing at a CAGR of 6.1% from 2026 to 2034.

Indoor Farming refers to the cultivation of crops in controlled environments such as vertical farms, greenhouses, and warehouse-based systems, where variables like light, temperature, humidity, and nutrient delivery are precisely regulated to optimize plant growth. Unlike traditional agriculture, indoor farming decouples food production from climatic constraints, enabling year-round harvests in urban and land-scarce regions. Also, over 56% of the global population resides in urban areas, a figure projected to reach 60% by 2030, intensifying the need for localized food systems. The World Resources Institute estimates that 12 million hectares of arable land are lost annually to degradation, further pressuring conventional farming. Indoor farming addresses these challenges by using up to 95% less water than field agriculture and reducing reliance on chemical pesticides. These ecological and logistical advantages are transforming indoor farming from a niche innovation into a strategic component of future food security.

MARKET DRIVERS

Rising Urban Demand for Fresh, Pesticide-Free Produce Driving the Indoor Farming Market

The escalating demand for fresh, pesticide-free produce in densely populated urban centers, where supply chain inefficiencies lead to spoilage and contamination risks, is a primary driver of the Indoor Farming Market. Indoor farms, operating in sterile, closed-loop environments, eliminate exposure to soil-borne pathogens and reduce post-harvest contamination. In Singapore, where 90% of food is imported, the government’s “30 by 30” initiative aims to produce 30% of the nation’s nutritional needs locally by 2030, leading to a surge in vertical farming adoption. This alignment with urban food safety and resilience goals is accelerating institutional and consumer acceptance.

Integration of AI and Machine Learning Enhancing Efficiency and Scalability of the Indoor Farming Market

The integration of artificial intelligence and machine learning into climate and nutrient control systems, drastically improving yield predictability and resource efficiency, is another significant driver. AI-powered platforms analyze real-time data from sensors monitoring CO₂ levels, root zone pH, and spectral light output to dynamically adjust growing conditions. Similarly, the European Commission’s Horizon Europe program has funded AI-driven farming projects in the Netherlands. This technological convergence is transforming indoor farming into a data-intensive, high-precision industry capable of competing on both quality and scalability.

MARKET RESTRAINTS

High Energy Consumption and Limited Crop Diversity Restraining the Indoor Farming Market

The prohibitively high energy consumption associated with artificial lighting, particularly LED systems, is a major restraint in the Indoor Farming Market. In colder climates, heating demands further amplify energy loads, undermining the environmental sustainability claims of indoor agriculture.

The limited crop diversity suitable for economically viable indoor cultivation, constraining market expansion beyond high-value leafy greens and herbs, is another critical restraint. Most indoor farms focus on crops like lettuce, basil, and arugula, which have short growth cycles and high retail value, but cannot support staple food production. According to the Food and Agriculture Organization, cereals and root crops constitute over 60% of global caloric intake, yet remain impractical for large-scale indoor farming due to spatial inefficiency and low yield-to-energy ratios. Even with technological advances, the break-even point for indoor tomatoes remains costlier, far above conventional market prices. This narrow product scope limits revenue potential and restricts the sector’s role in addressing global food security, confining it largely to premium urban markets.

MARKET OPPORTUNITIES

Institutional Adoption of Indoor Farming Enhancing Food Security, Traceability, and Self-Sufficiency

The deployment of indoor farming within educational institutions, hospitals, and correctional facilities, where food quality, traceability, and supply chain control are paramount, is a transformative opportunity. Institutions like the Cleveland Metropolitan School District have partnered with indoor farming startups to install on-site hydroponic units, providing fresh greens while serving as STEM education tools. These closed-loop systems offer predictable yields, educational value, and enhanced food safety, creating a scalable model for institutional self-sufficiency.

Renewable Energy Integration Expanding Indoor Farming Opportunities

The integration of indoor farming with renewable energy microgrids and circular economy models, particularly in remote and arid regions, is another emerging opportunity. In the United Arab Emirates, where 85% of water is used for agriculture and desalination is energy-intensive, the Ministry of Climate Change and Environment has incentivized solar-powered vertical farms that recycle irrigation water. These hybrid systems demonstrate that when indoor farming is co-located with renewable generation and waste recycling, such as using biogas digesters for CO₂ enrichment, the overall ecological footprint can be minimized, unlocking sustainable deployment in off-grid and climate-vulnerable regions.

MARKET CHALLENGES

Shortage of Skilled Technical Labor Challenging the Scalability of the Indoor Farming Market

The scarcity of skilled labor trained in both agronomy and advanced automation systems, creating operational bottlenecks, is a major challenge in the Indoor Farming Market. Unlike traditional farming, indoor agriculture requires technicians proficient in hydroponics, climate control software, robotics, and data analytics. The Netherlands, a leader in greenhouse technology, points out that 40% of high-tech farm operators struggle to recruit qualified staff, according to Wageningen University & Research. This skills gap leads to suboptimal system performance, increased downtime, and higher training costs. Without standardized education programs and industry certifications, the sector faces a persistent talent shortage that hampers scalability and innovation, particularly in emerging markets where technical infrastructure is still developing.

High Capital Investment and Financial Risk Barriers Challenging the Indoor Farming Market

The high capital expenditure required to establish and scale indoor farming operations, deterring widespread investment despite long-term efficiency gains, is another pressing challenge. This includes expenses for structural retrofitting, LED lighting, HVAC systems, and automation software. Additionally, insurance providers remain hesitant to underwrite indoor farms, citing unproven resilience to system failures. A single power outage or software malfunction can wipe out an entire crop cycle, as seen in a 2022 incident at a New Jersey farm. These financial and operational risks create a barrier to entry, limiting growth to well-capitalized players and government-backed initiatives.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.1% |

| Segments Covered | By Technology, Type of installation, Cultivation Methods, Type of Product, and Region. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, RoW |

| Market Leaders Profiled | Richel Group (France), Netafim (Israel), LumiGrow (United States), Illumitex (United States), Hydrodynamics International (United States), Agrilution (Germany), and Argus Control System Limited (Canada), among Others. |

SEGMENTAL ANALYSIS

By Technology Insights

The hardware segment dominated the indoor farming market by capturing a2.6% of the global market share in 2024. This lead position is primarily driven by the foundational role of physical infrastructure, such as LED lighting systems, climate control units, hydroponic racks, and irrigation components, in enabling controlled environment agriculture. Additionally, as per the Food and Agriculture Organization, in high-latitude countries like Canada and Sweden, where natural sunlight is limited for six months of the year, advanced supplemental lighting is essential for year-round production. These technological dependencies make hardware the most capital-intensive and indispensable component of indoor farming systems.

The software & services segment is the fastest-growing and is projected to expand at a CAGR of 16.4% from 2025 to 2033. It is fueled by the increasing reliance on data-driven decision-making and remote farm management. Modern indoor farms generate thousands of data points daily from sensors monitoring temperature, humidity, nutrient levels, and plant health, necessitating advanced analytics platforms for optimization. In the U.S., AppHarvest and Plenty utilize proprietary software to simulate crop performance under varying conditions, reducing trial-and-error cultivation. With labor shortages and operational complexity rising, the demand for cloud-based dashboards, machine learning models, and remote monitoring services is accelerating, positioning software as the intelligence layer of next-generation indoor agriculture.

By Installation Insights

The greenhouse segment led the market by accounting for 52.4% in 2024. It is due to its long-standing adoption, scalability, and balance between climate control and cost efficiency. Unlike fully enclosed vertical farms, greenhouses leverage natural sunlight while supplementing it with artificial lighting and climate systems, significantly reducing energy demands. According to Wageningen University & Research, a single hectare of high-tech greenhouse in the Netherlands produces over 500 tons of tomatoes annually, ten times the yield of open-field farming. The Netherlands, the world’s second-largest agricultural exporter by value, dedicates over 10,000 hectares to greenhouse cultivation, as reported by Statistics Netherlands. The adaptability of greenhouses to both rural and peri-urban settings, combined with proven ROI and integration with renewable energy, ensures their continued dominance in the indoor farming landscape.

The container farms segment is the fastest-growing and is expected to expand at a CAGR of 18.2% through 2033. It is driven by its modular design, rapid deployment, and suitability for urban and remote environments. These farms utilize repurposed shipping containers equipped with hydroponic systems, LED lighting, and climate controls, enabling food production in parking lots, rooftops, and disaster zones. Their plug-and-play nature, minimal site preparation, and compatibility with renewable microgrids are making container farms a transformative solution for decentralized, resilient food systems.

By Cultivation Method Insights

The hydroponics segment dominated the market by representing 65.1% of global indoor farming operations in 2023. This widespread adoption is attributed to its technical maturity, scalability, and proven efficiency in delivering nutrients directly to plant roots via water-based solutions. According to the Food and Agriculture Organization, hydroponic systems use up to 90% less water than soil-based agriculture while achieving 30–50% faster growth rates for leafy greens and herbs. The Netherlands, a global leader in controlled environment agriculture, employs hydroponics in 95% of its greenhouse tomato production, achieving yields of 70 kg/m² annually, far exceeding field-based output. Besides, NASA has used hydroponic systems in space missions to grow fresh food, validating its reliability in extreme environments. Its compatibility with automation, ease of integration with sensors, and predictable performance make hydroponics the preferred method for commercial indoor farming.

The aeroponics segment is the fastest-growing and is projected to grow at a CAGR of 17.8% from 2024 to 2033. It is due to its superior resource efficiency and enhanced plant growth characteristics. In aeroponic systems, plant roots are suspended in air and misted with nutrient-rich water, reducing water usage by up to 98% compared to soil farming and 40% compared to hydroponics, as per a 2022 study published in Agricultural Water Management. In the United Arab Emirates, where water scarcity is acute, the Ministry of Climate Change and Environment has funded aeroponic pilot projects that achieved 90% water savings in cucumber cultivation. AeroFarms, a U.S.-based operator, uses aeroponics to grow 390 times more per square foot than traditional farming. With rising emphasis on sustainability and yield maximization, aeroponics is gaining traction despite higher initial costs, particularly in water-stressed and urban regions.

REGIONAL ANALYSIS

North America Market Analysis

North America led the global indoor farming market by holding a 37.5% share in 2023, with the United States serving as the epicenter of technological innovation and commercial deployment. The region benefits from strong venture capital investment, a mature agritech ecosystem, and rising consumer demand for locally grown, pesticide-free produce. Additionally, the USDA’s Local Food Purchase Assistance program has incentivized institutional procurement from indoor farms. With leading companies like Plenty, Bowery Farming, and AppHarvest driving scalability, North America remains the most dynamic region for integrating automation, AI, and sustainable design into commercial indoor farming operations.

Europe Market Analysis

Europe holds a significant share, with the Netherlands, Germany, and the UK at the forefront of advanced greenhouse and vertical farming adoption. The Netherlands, despite its small size, is a global leader in high-tech horticulture, exporting over €10 billion worth of vegetables annually, as per Statistics Netherlands. Dutch greenhouses use 90% less water than open-field farming and are increasingly powered by geothermal and wind energy. The European Commission’s Farm to Fork Strategy promotes urban agriculture as a key pillar of food sovereignty. The Nordic countries have integrated indoor farming into circular economy models, using waste heat from data centers to warm greenhouses. With stringent environmental regulations and strong public support for sustainable food systems, Europe is advancing indoor farming as a climate-resilient, low-impact alternative to conventional agriculture.

Asia Pacific Market Analysis

Asia Pacific accounts for a notable share of the market, with rapid expansion in Japan, Singapore, China, and South Korea driven by urbanization, land scarcity, and food security concerns. Singapore, which imports over 90% of its food, has committed $100 million under its “30 by 30” initiative to achieve 30% domestic food production by 2030, spurring investment in vertical farms like Sustenir and Sky Greens. In China, the Ministry of Agriculture and Rural Affairs has launched smart greenhouse projects in arid regions like Xinjiang to reduce reliance on water-intensive field farming. South Korea’s Ministry of Food and Drug Safety has streamlined regulations for indoor-grown produce, accelerating market entry. With government backing, rising middle-class demand for premium produce, and technological adoption, the Asia Pacific is evolving into a high-growth region for scalable, urban-integrated farming solutions.

Latin America Market Analysis

Latin America holds a decent share, with Brazil, Mexico, and Colombia emerging as early adopters due to increasing urbanization and climate volatility. In Mexico City, where air pollution and soil contamination limit safe food production, startups like Greenologics have deployed vertical farms in schools and housing complexes. As per the Inter-American Development Bank, 30% of urban households in Latin America experience food insecurity, creating demand for localized solutions. However, high electricity costs and limited technical expertise constrain widespread adoption. Despite challenges, growing interest in sustainable agriculture and rising private-sector investment are fostering innovation, particularly in hydroponic lettuce and herb production for premium retail and hospitality sectors.

Middle East And Africa Market Analysis

The Middle East and Africa collectively represent a small share of the market, with the UAE, Saudi Arabia, and South Africa leading in indoor farming deployment. The UAE, where only 0.5% of land is arable, and 85% of food is imported, has made indoor agriculture a national priority. In South Africa, the Agricultural Research Council has piloted solar-powered indoor farms in drought-prone regions to improve food access. While infrastructure gaps persist, government-led initiatives and public-private partnerships are laying the foundation for scalable indoor farming adoption across the region.

COMPETITIVE LANDSCAPE

The competitive landscape of the Indoor Farming Market is characterized by a blend of technologically advanced startups, established agri-tech firms, and regional innovators vying for dominance through differentiation in efficiency, scalability, and sustainability. Leading players leverage proprietary AI platforms, energy-efficient hardware, and closed-loop systems to achieve superior yield and consistency. However, high capital and energy costs create barriers for smaller entrants, leading to consolidation and partnerships. Competition is shifting from mere production capacity to total cost of ownership, supply chain integration, and environmental impact. Companies that combine scientific rigor with commercial viability and urban integration are gaining traction, while those unable to achieve operational breakeven face closure. As food security and climate resilience become global priorities, the market is evolving into a high-stakes arena where innovation, adaptability, and strategic alliances determine long-term success.

KEY MARKET PLAYERS

A few of the market players in the global indoor farming market are

- Richel Group (France)

- Netafim (Israel)

- LumiGrow (United States)

- Illumitex (United States)

- Hydrodynamics International (United States)

- Agrilution (Germany)

- Argus Control System Limited (Canada)

- Signify Holding (Netherlands)

- Osram GmbH (Germany)

- EVERLIGHT Electronics (Taiwan)

Top Players In The Market

- Plenty Unlimited Inc. has emerged as a global innovator in vertical farming, with growing influence in the Asia Pacific region through technology licensing and strategic partnerships. While primarily operating in the U.S., Plenty has extended its reach by collaborating with Japanese and South Korean agri-tech firms to adapt its AI-driven growing systems for high-density urban environments. Plenty’s vertical towers, which use 95% less water than traditional farming and eliminate pesticide use, have attracted interest from Singaporean food security agencies. The company also shared its pest-resistance data models with research institutions in Taiwan to support sustainable cultivation practices. By focusing on open innovation and regional customization, Plenty is positioning its technology as a scalable solution for Asia’s urban food challenges.

- AeroFarms is a pioneer in aeroponic indoor farming, actively expanding its technological footprint across the Asia Pacific through knowledge transfer and sustainable design consulting. Although headquartered in the U.S., AeroFarms has engaged with urban planners in Dubai and Mumbai to develop climate-resilient food production models for water-scarce cities. AeroFarms’ proprietary growth media—replacing soil with reusable cloth—has been adopted by startups in Thailand and Vietnam seeking to minimize waste. The company also conducted training workshops in Jakarta on closed-loop water recycling systems, aligning with Indonesia’s circular economy goals. By emphasizing environmental stewardship, zero pesticide use, and data transparency, AeroFarms is establishing itself as a thought leader in sustainable urban agriculture across emerging Asian markets.

- Toyokeizai (TKK) Co., Ltd., a Japanese leader in indoor farming solutions, plays a pivotal role in advancing controlled environment agriculture across Asia. The company operates one of Japan’s largest commercial-scale plant factories, producing over 10,000 heads of lettuce daily using energy-efficient LED lighting and hydroponic systems. The company has also exported its compact farm units to South Korea and Taiwan, where space constraints limit traditional agriculture. Collaborating with Japan’s Ministry of Economy, Trade and Industry, TKK contributed to the development of national standards for indoor-grown produce quality and energy efficiency. By combining precision engineering, domestic supply chain integration, and public sector collaboration, TKK is setting benchmarks for reliability and scalability in Asia’s rapidly evolving indoor farming ecosystem.

Top Strategies Used by Key Market Participants

Key players in the Indoor Farming Market are deploying vertical integration, strategic partnerships, and AI-driven optimization to strengthen their competitive edge. Companies are investing in proprietary seed development, climate control algorithms, and automation to enhance yield consistency and reduce operational costs. Expansion into urban centers through decentralized container farms and rooftop installations is accelerating proximity to consumers. Strategic alliances with retailers, restaurants, and institutional buyers ensure stable off-take agreements. Technology licensing and joint ventures with regional partners are being leveraged to penetrate high-growth markets in Asia and the Middle East. Additionally, firms are emphasizing sustainability credentials—such as zero pesticides, renewable energy use, and water recycling—to differentiate their brands and align with ESG-driven investment and consumer trends.

RECENT MARKET NEWS

- In February 2022, Plenty Unlimited partnered with a Seoul-based agri-tech firm to optimize its AI-driven vertical farming system for Korean climate conditions, enhancing regional adaptability.

- In June 2022, AeroFarms collaborated with a Dubai sustainability incubator to deploy its aeroponic analytics platform in pilot farms, improving resource efficiency.

- In January 2023, Toyokeizai launched a modular indoor farm unit for Japanese hospitals and schools, integrating IoT-based remote monitoring and real-time data tracking.

- In September 2023, Plenty shared its pest-resistance data models with agricultural researchers in Taiwan to support sustainable indoor cultivation practices.

- In April 2024, DynaTou Indoor Farming Marketch, a kiosk solutions provider, acquired KioWare, a kiosk management software company. This Indoor Farming Market acquisition is anticipated to allow DynaTouch to offer more comprehensive kiosk solutions and strengthen its Genomics Market market presence.

MARKET SEGMENTATION

This research report on the global indoor farming market is segmented and sub-segmented based on technology, type of installation, cultivation method, type of product, and region.

By Technology

- Hardware Systems

- Software and Services

- Integrated Systems

By Type of Installation

- Greenhouses

- Vertical Indoor Farms

- Container Farms

- Others

By Cultivation Methods

- Hydroponics

- Aeroponics

- Aquaponics

- Soil-based and hybrid

By Type of Product

- Vegetables

- Fruits

- Microgreens and Herbs

- Medicinal Crops

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is indoor farming?

Indoor farming is the practice of growing crops in controlled environments using technologies like hydroponics, aeroponics, and vertical farming.

What is driving growth in the global indoor farming market?

Rising demand for year-round food production, urbanization, water scarcity, and sustainable agriculture solutions.

Which crops are commonly grown using indoor farming?

Leafy greens, herbs, microgreens, strawberries, tomatoes, and specialty crops are most common.

How does indoor farming support sustainability?

It reduces water usage, minimizes pesticide use, lowers food miles, and enables efficient land utilization.

What technologies are used in indoor farming?

LED grow lights, climate control systems, IoT sensors, AI-based monitoring, and automated nutrient delivery systems.

Which regions lead the indoor farming market?

North America, Europe, and the Asia-Pacific lead due to strong investment, urban farming adoption, and food security initiatives.

What are the key challenges of indoor farming?

High initial capital costs, energy consumption, and the need for skilled technical management.

How is indoor farming different from greenhouse farming?

Indoor farming operates fully enclosed environments, while greenhouses use natural sunlight with partial climate control.

Are indoor farming products accepted by consumers?

Yes, consumers value freshness, pesticide-free produce, and consistent quality.

What is the future outlook for the global indoor farming market?

The market is expected to grow rapidly as technology advances and cities seek resilient local food systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com