Global Ancient Grain Market Size, Share, Trends & Growth Forecast Report - Segmented By Applications (Bakery, Confectionary, Sports Nutrition, Infant Formula, Cereals, Frozen Food And Others), Crop Type (Gluten Free Ancient Grains And Gluten Containing Ancient Grains) & Region(North America, Europe, Apac, Latin America, Middle East And Africa) - Industry Analysis 2026 to 2034

Market Size, 2025

$1.67 BnMarket Estimate, 2026

$2.26 BnMarket Forecast, 2034

$25.23 BnCAGR, 2026–2034

35.2%Global Ancient Grain Market Summary

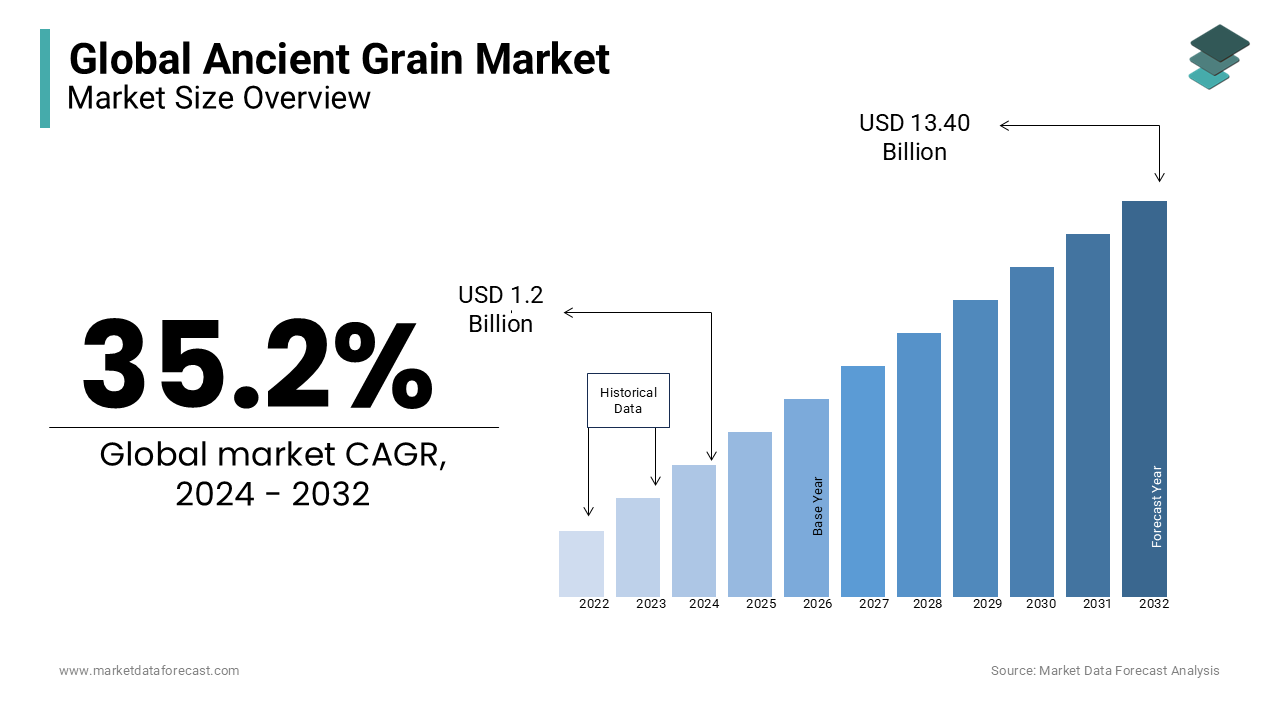

The global ancient grain market was valued at USD 1.67 billion in 2025, is projected to reach USD 2.26 billion in 2026, and is expected to surge to USD 25.23 billion by 2034, registering an exceptional CAGR of 35.2% from 2026 to 2034. Market growth is driven by rising health consciousness, increasing demand for gluten-containing and gluten-free traditional grains, and expanding use of ancient grains in functional foods, bakery products, snacks, and beverages. Consumers’ growing preference for nutrient-dense, clean-label, and minimally processed ingredients is significantly boosting global consumption. Innovation in ancient grain-based products and the rising popularity of superfood trends are further accelerating market momentum.

Key Market Trends

- Rapid rise in demand for nutrient-rich, clean-label grains such as quinoa, amaranth, millet, and spelt.

- Growing incorporation of ancient grains in bakery, snacks, cereals, beverages, and plant-based foods.

- Increasing consumer interest in natural, minimally processed, and traditional crops linked to digestive and nutritional benefits.

- Expanding retail availability and premiumization of superfood grain-based products.

- Strong R&D investment in value-added grain formulations for health-focused product lines.

Segmental Insights

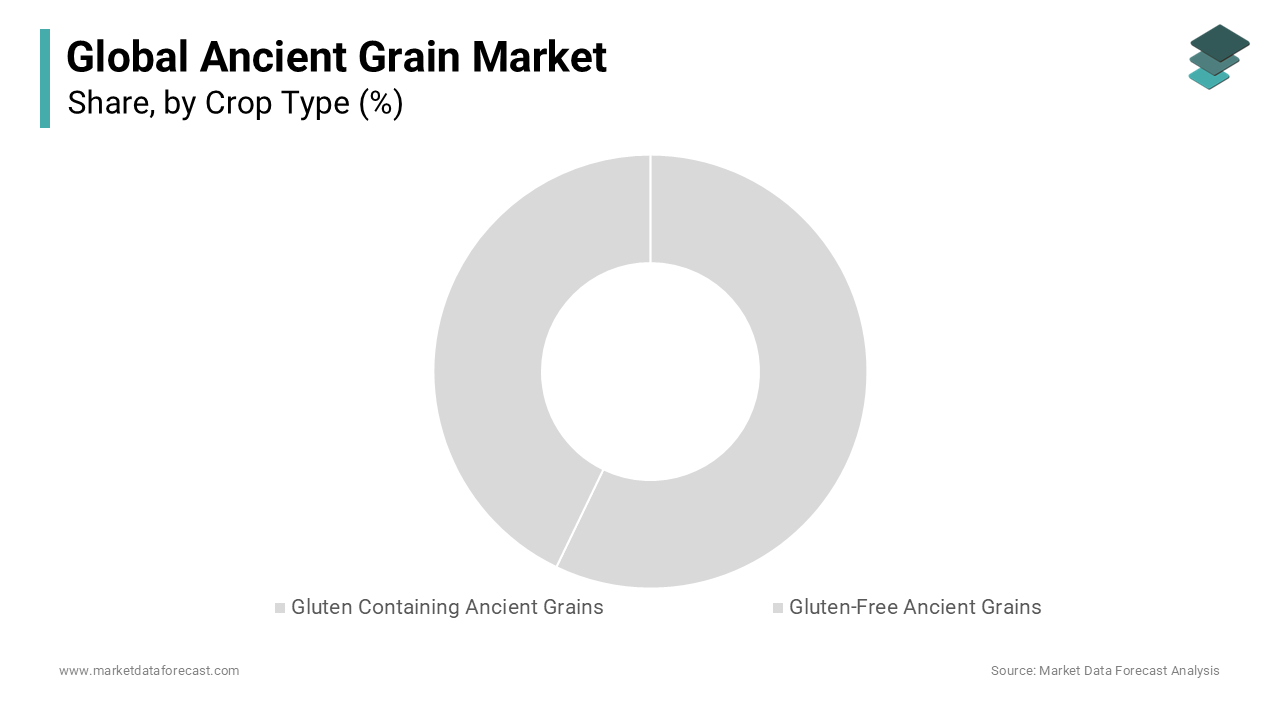

- Based on crop type, the gluten-containing ancient grain segment dominated in 2023 with over 70% share, driven by strong demand for grains such as spelt, barley, and farro across bakery and food processing industries.

- Based on application, the food and beverages segment captured a major share due to wide usage of ancient grains in bakery, snacks, ready-to-eat products, and functional beverages.

Regional Insights

- Europe held the largest market share at 43.06% in 2026, primarily due to high bread consumption and increasing use of ancient grains in bakery and cereal products.

- North America continues to adopt ancient grain-based snacks, cereals, and gluten-free products at a rapid pace.

- Asia Pacific is emerging as a high-growth region with rising awareness of healthy grains and expanding food processing industries.

Competitive Landscape

The ancient grain market is moderately competitive, with companies focusing on product innovation, organic grain sourcing, and expanding distribution networks. Firms are increasingly investing in superfood grain blends, ready-to-cook products, and premium grain-based snacks to capture new consumer segments.

Key players in the global ancient grain market include:

Ardent Mills (U.S.), Snyder’s-Lance Inc. (U.S.), Crunchmaster Inc. (U.S.), SK Food International (U.S.), Purely Elizabeth Inc. (U.S.), Quinoasure Inc. (U.S.), Great River Organic Milling Inc. (U.S.), Urbane Grain Inc. (U.S.), Nature’s Path Foods (Canada), and GFB Great Foods (India).

Global Ancient Grain Market Size

The global ancient grain market size was valued at USD 1.67 billion in 2025, and the global market size is expected to reach USD 25.23 billion by 2034 from USD 2.26 billion in 2026, growing at a CAGR of 35.2% from 2026 to 2034.

Ancient grains are types of cereal grains and pseudocereals (seeds) that have remained largely unchanged by selective breeding or modern genetic modification over the last several hundred to thousands of years. These grains include varieties such as quinoa, amaranth, spelt, kamut, teff, and millet, which are revered for their superior nutritional profiles compared to modern wheat and rice. Consumers are increasingly drawn to these ingredients due to their high content of protein, fiber, vitamins, and minerals, as well as their inherent resistance to pests and diseases. The global shift toward holistic wellness and preventive healthcare has propelled ancient grains from niche health food stores into mainstream dietary habits. As per the Food and Agriculture Organization of the United Nations (FAO), the global production of millet alone reached 30.9 million tonnes in 2022. However, contrary to claims of a resurgence, long-term data indicates that production has remained largely stagnant over the last decade. Furthermore, the rise in gluten intolerance and celiac disease diagnoses has accelerated the adoption of naturally gluten free ancient grains like quinoa and buckwheat. According to the European Society for Paediatric Gastroenterology, Hepatology and Nutrition (ESPGHAN), the prevalence of celiac disease in children in Europe is approximately 1% (1 in 100), creating a steady demand for safe alternative grains. The culinary versatility of these grains allows them to be incorporated into various food formats, ranging from breakfast cereals and snacks to baked goods and plant based meat alternatives. This adaptability, combined with their sustainability credentials, positions ancient grains as a pivotal component in the future of global food security and nutrition.

MARKET DRIVERS

Rising Prevalence of Gluten Intolerance and Celiac Disease

The increasing diagnosis of gluten related disorders serves as a primary factor for the expansion of the ancient grain market. Modern wheat varieties contain higher levels of gluten proteins, which can trigger adverse immune responses in susceptible individuals. Ancient grains such as quinoa, amaranth, buckwheat, and millet are naturally gluten free, offering a safe and nutritious alternative for those managing celiac disease or non celiac gluten sensitivity. As per the World Gastroenterology Organisation, the global prevalence of celiac disease is approximately 1 percent (affecting roughly 1 in 100 individuals), with millions of undiagnosed cases potentially seeking dietary solutions. In Europe, awareness campaigns and improved diagnostic tools have led to a surge in identified cases, driving consumers to seek certified gluten free products. The European Commission has implemented strict labeling regulations for gluten-free foods, ensuring that products containing no more than 20 mg/kg (ppm) of gluten can be safely consumed by affected individuals. This regulatory clarity boosts consumer confidence in ancient grain products. Additionally, the broader wellness trend has led many individuals without diagnosed conditions to adopt gluten free diets for perceived health benefits, further expanding the customer base. Food manufacturers are responding by reformulating existing products and launching new lines featuring ancient grains, thereby enhancing availability and variety. This shift is not merely a dietary restriction but a lifestyle choice that prioritizes digestive health and overall well being, sustaining long term demand for these traditional crops.

Growing Consumer Preference for Nutrient Dense and Functional Foods

The modern consumer’s heightened focus on nutritional density and functional benefits greatly drives the growth of the ancient grain market. Unlike refined grains that often lack essential nutrients, ancient grains are packed with complex carbohydrates, high quality protein, antioxidants, and micronutrients such as magnesium, iron, and zinc. Quinoa, for instance, is a complete protein source containing all nine essential amino acids, making it particularly valuable for vegetarians and vegans. As per the United States Department of Agriculture, one cup of cooked quinoa provides 8 grams of protein and 5 grams of fiber, surpassing the nutritional value of many conventional cereals. Amaranth is another powerhouse, known for its high lysine content and anti inflammatory properties. The rise of chronic lifestyle diseases such as diabetes and cardiovascular conditions has prompted individuals to seek foods with low glycemic indices and heart healthy fats. Ancient grains like barley and oats are rich in beta glucans, which have been shown to lower cholesterol levels. Based on positive scientific opinions from the European Food Safety Authority (EFSA), the European Commission has authorized health claims related to the cholesterol-lowering effects of oat beta-glucan, encouraging manufacturers to highlight these benefits on packaging. This scientific validation enhances the appeal of ancient grains among health conscious consumers who prioritize evidence based nutrition. The integration of these grains into everyday meals supports a proactive approach to health management, fueling their popularity across diverse demographic groups.

MARKET RESTRAINTS

High Production Costs and Limited Agricultural Yield

Higher production costs and lower yields compared to modern commodity crops hinder the economic viability of ancient grain cultivation and the expansion of the ancient grain market. Many ancient grains have not undergone the same level of agricultural optimization and mechanization as wheat, corn, or soy, resulting in labor intensive farming practices. For example, quinoa harvesting can be challenging due to the uneven ripening of seeds, which often requires manual intervention to prevent shattering. As per the International Fund for Agricultural Development, smallholder farmers who predominantly cultivate these crops often lack access to advanced machinery and efficient processing facilities, leading to post harvest losses. The cost of organic certification, which is frequently associated with ancient grains, further adds to the financial burden for producers. These elevated production costs are ultimately passed on to consumers, making ancient grain products significantly more expensive than their conventional counterparts. Price sensitivity remains a barrier for mass adoption, particularly in lower income segments. Additionally, the limited scale of production means that supply chains are less developed and more vulnerable to disruptions. Farmers may hesitate to switch from established crops to ancient grains due to the uncertainty of market demand and the risk of lower profitability. This economic constraint restricts the widespread availability of ancient grains and limits their integration into cost sensitive food applications, posing a significant restraint to market growth.

Complex Supply Chain and Limited Processing Infrastructure

The fragmented and underdeveloped supply chain for these grains is a substantial obstacle to the ancient grain market growth. Unlike major commodities that benefit from established global trading networks and standardized processing protocols, ancient grains often rely on localized and disjointed supply chains. The lack of specialized processing facilities capable of handling diverse grain types efficiently leads to bottlenecks and increased lead times. For instance, dehulling and polishing quinoa or amaranth requires specific equipment that is not widely available in all producing regions. As per the Food and Agriculture Organization (FAO), approximately one-third (33%) of the world's food production, roughly 1.3 billion tons, is lost or wasted annually, with losses in developing nations often exceeding 30% for fresh produce like fruits and vegetables. This inefficiency not only reduces the volume of marketable product but also compromises quality consistency. Retailers and food manufacturers require reliable and uniform supplies to maintain production schedules, but the variability in ancient grain availability can disrupt operations. Furthermore, the geographical concentration of certain grains, such as quinoa in the Andes or teff in Ethiopia, creates dependency on specific regions, exposing the supply chain to geopolitical and climatic risks. Transportation costs from remote farming areas to urban centers further inflate prices. The absence of standardized grading systems also complicates trade, as buyers may struggle to assess quality accurately. These logistical challenges hinder the scalability of ancient grain products and limit their penetration into mainstream retail channels.

MARKET OPPORTUNITIES

Expansion into Plant Based and Alternative Protein Products

The burgeoning plant-based food sector offers a lucrative opportunity for the integration of ancient grains as key ingredients in alternative protein products, which is likely to boost the expansion of the ancient grain market. Consumers are increasingly seeking sustainable and ethical food choices, driving the growth of meat and dairy alternatives. Ancient grains such as quinoa, amaranth, and teff provide high quality plant based proteins with complete amino acid profiles, making them ideal for formulating nutritious meat substitutes. As per the Good Food Institute, the European plant-based retail landscape grew significantly between 2020 and 2022, reaching a record valuation despite high inflation and macroeconomic challenges. Food technology companies are leveraging the functional properties of ancient grains, such as their ability to bind water and fat, to improve the texture and mouthfeel of plant based meats. Additionally, the use of ancient grains in dairy alternatives, such as quinoa milk or amaranth yogurt, caters to consumers with lactose intolerance or those seeking variety beyond almond and soy options. The clean label trend further supports this opportunity, as ancient grains are perceived as natural and minimally processed ingredients. Manufacturers can differentiate their products by highlighting the nutritional benefits and sustainability credentials of these grains. Collaborations between grain producers and food tech startups can accelerate the development of novel formulations that meet the evolving preferences of health conscious and environmentally aware consumers. This synergy positions ancient grains as a vital component in the future of sustainable protein sources.

Innovation in Convenient and Ready to Eat Food Formats

The demand for convenience in modern lifestyles provides a significant prospect for the growth of the ancient grain market. As a result, there is substantial potential for their incorporation into ready-to-eat and easy-to-prepare food formats. Traditional preparation methods for many ancient grains, such as soaking and long cooking times, can be a deterrent for busy consumers. However, advancements in food processing technologies have enabled the creation of pre cooked, instant, and snackable ancient grain products. Puffed quinoa, roasted amaranth bars, and instant millet porridge are examples of innovations that enhance accessibility and appeal. Breakfast cereals and granola blends featuring ancient grains are gaining popularity among health conscious individuals seeking quick yet wholesome meal solutions. Furthermore, the incorporation of ancient grain flours into baked goods, pasta, and crackers allows consumers to enjoy familiar formats with enhanced nutritional benefits. Retailers are expanding their shelf space for these convenient products, recognizing the growing consumer interest in functional foods that fit seamlessly into busy schedules. Marketing strategies that emphasize ease of preparation without compromising on health benefits can effectively capture this market segment. Manufacturers can broaden their consumer base beyond niche health enthusiasts. They can achieve this by addressing the convenience gap for mainstream shoppers looking for practical, nutritious options.

MARKET CHALLENGES

Susceptibility to Climate Variability and Environmental Stressors

They remain vulnerable to extreme weather and shifting climate patterns, which slows down the expansion of the ancient grain market. Yet, these grains are often praised for their resilience. Shifts in temperature and precipitation can significantly impact yield quality and quantity. For instance, quinoa cultivation in the Andean region has faced challenges due to irregular rainfall and frost events, which can damage crops during critical growth stages. As per the Intergovernmental Panel on Climate Change, the frequency of extreme weather events in agricultural zones has increased, posing risks to crop stability. Drought conditions can reduce grain size and nutritional content, while excessive moisture can lead to fungal infections and spoilage. These environmental stressors create uncertainty for farmers and suppliers, affecting the consistency of supply. Unlike major commodity crops that have extensive insurance schemes and government support, ancient grain farmers often lack such safety nets, making them more vulnerable to financial losses. The geographic specificity of certain grains also limits the ability to shift production to more favorable regions quickly. This climatic vulnerability can lead to price volatility and supply shortages, discouraging long term contracts with large food manufacturers. Ensuring stable production requires investment in climate smart agricultural practices and diversified sourcing strategies, but these measures take time to implement effectively. The inherent risk associated with climate dependency remains a persistent challenge for the reliable scaling of the ancient grain market.

Consumer Misconceptions and Lack of Culinary Knowledge

Low consumer familiarity is a significant challenge to the ancient grain market. Many consumers lack the culinary knowledge to prepare and incorporate these ingredients into daily meals. Many consumers perceive ancient grains as difficult to cook or unfamiliar in taste, which acts as a barrier to trial and repeat purchase. Unlike rice or pasta, which have established cooking methods and cultural ubiquity, grains like teff, sorghum, and farro require specific preparation techniques that are not widely known. As per a survey by the International Food Information Council (IFIC), consumer barriers to healthy grain and fiber intake include difficulty identifying high-fiber foods (30%) and perceived high cost (27%).This knowledge gap limits the potential market size and restricts consumption to occasional experimentation rather than regular dietary inclusion. Educational efforts by manufacturers and retailers are often insufficient to overcome this hurdle, as marketing messages may focus more on health benefits than practical usage. Without clear and accessible cooking instructions or recipe ideas, consumers may become frustrated with unsuccessful attempts, leading to negative perceptions. The complexity of integrating these grains into familiar dishes requires creative culinary guidance and demonstration. Overcoming this educational barrier is essential for driving mainstream adoption, but it requires sustained investment in consumer engagement and content creation, which can be resource intensive for smaller brands operating in the niche ancient grain sector.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 35.2% |

| Segments Covered | By Crop Type, Application and Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Ardent Mills (U.S.), Snyder’s-Lance Inc. (U.S.), Crunchmaster Inc. (U.S.), SK Food International (U.S.), Purely Elizabeth Inc. (U.S.), Quinoasure Inc. (U.S.), Great River Organic Milling Inc. (U.S.), Urbane Grain Inc. (U.S.), Nature’s Path Foods (Canada), GFB Great Foods (India) |

SEGMENTAL ANALYSIS

By Crop Type Insights

The gluten free ancient grains segment held the majority share of 65.1% of the global ancient grain market in 2025. This supremacy of the segment is mainly credited to the increasing prevalence of celiac disease and non-celiac gluten sensitivity, which compels consumers to seek safe and nutritious alternatives to wheat-based products. Quinoa, amaranth, buckwheat, and millet are naturally gluten free and offer superior nutritional profiles, making them ideal substitutes. As per the Celiac Disease Foundation, approximately 1 in 133 Americans suffers from celiac disease, while millions more experience gluten sensitivity, creating a substantial and growing consumer base. The Global Burden of Disease study indicates that the prevalence of autoimmune diseases is rising globally, a trend that market analysts associate with the increasing demand for specialized dietary solutions. Additionally, the perception of gluten free diets as healthier options among the general population has expanded the market beyond medical necessity. Consumers associate gluten free ancient grains with weight management, improved digestion, and overall wellness. The versatility of these grains allows them to be incorporated into a wide range of food products, from breakfast cereals to snacks and baked goods, enhancing their accessibility. Regulatory support, such as clear labeling standards for gluten free products in North America and Europe, boosts consumer confidence and facilitates market growth. The strong alignment with clean label trends and the demand for minimally processed foods further solidifies the leading position of this segment. Manufacturers are continuously innovating to improve the texture and taste of gluten free products, addressing previous consumer complaints and encouraging repeat purchases. This combination of health drivers, regulatory clarity, and product innovation ensures that gluten free ancient grains remain the cornerstone of the market.

The gluten containing ancient grains segment is predicted to witness the highest CAGR of 7.8% during the forecast period. This accelerated growth of the segment is propelled by a resurgence of interest in traditional and heritage grains such as spelt, kamut, farro, and einkorn. Consumers are increasingly seeking authentic culinary experiences and diverse flavors that modern wheat varieties often lack. These ancient grains offer unique nutty tastes and chewy textures that appeal to gourmet chefs and home cooks alike. As per the Oldways Preservation Trust, campaigns promoting whole grain diversity have significantly increased consumer awareness and acceptance of heritage grains in mainstream diets. Furthermore, many individuals who do not suffer from celiac disease find that they can tolerate ancient wheat varieties better than modern hybridized wheat due to differences in gluten structure and lower levels of certain antigens. Research published in Food Chemistry suggests that ancient wheat varieties may elicit a reduced inflammatory response in cell models compared to modern wheat, highlighting potential benefits for individuals with non-celiac sensitivities. The agricultural sustainability of these crops also contributes to their growth, as they often require fewer inputs and are more resilient to local climate conditions. Farmers are increasingly adopting these crops to diversify their rotations and improve soil health. The integration of these grains into artisanal breads, pastas, and craft beers further expands their application scope. This blend of cultural appreciation, perceived digestibility, and environmental benefits propels the gluten containing segment to rapid growth, capturing a niche but loyal consumer base.

By Application Insights

The bakery and confectionary segment was the largest segment in the Ancient Grain Market by occupying a 35.7% share in 2025. This prominence of the segment is supported by the widespread incorporation of ancient grain flours into breads, cookies, cakes, and pastries. Bakers are increasingly utilizing flours from spelt, kamut, and quinoa to enhance the nutritional value and flavor profiles of their products. The American Bakers Association (ABA) reports that over 60% of consumers now weigh nutrition and sustainability as key factors in their bakery purchases, leading to a steady increase in the availability of "premium" and "all-natural" options in retail aisles. Ancient grains provide natural sweetness and moisture retention, reducing the need for added sugars and fats in formulations. This aligns with the clean label trend, where consumers seek recognizable and minimal ingredients. The versatility of ancient grain flours allows for seamless integration into existing baking processes, minimizing the need for extensive reformulation. Additionally, the rise of gluten free bakeries has spurred innovation in using rice, almond, and buckwheat flours to create high quality alternatives to traditional wheat based items. Retailers are expanding their shelf space for specialty baked goods, recognizing the premium pricing potential and consumer loyalty associated with these products. Marketing efforts emphasizing the heritage and health benefits of ancient grains resonate strongly with shoppers looking for wholesome options. The ability of ancient grains to improve the texture and shelf life of baked goods further enhances their appeal to manufacturers. This combination of functional advantages, health benefits, and consumer demand solidifies the bakery segment’s leading position in the market.

The sports nutrition segment is estimated to register the fastest CAGR of 9.2% from 2026 to 2034 due to the increasing recognition of ancient grains as superior sources of plant based protein and complex carbohydrates for athletes and fitness enthusiasts. Quinoa and amaranth, in particular, are valued for their complete amino acid profiles, which support muscle repair and recovery. As per the International Society of Sports Nutrition (ISSN), plant-based protein sources such as soy and pea isolates are increasingly recognized as effective alternatives to whey for muscle repair and performance, provided they contain a complete amino acid profile. Ancient grains are being incorporated into protein bars, powders, and ready to drink shakes, offering sustained energy release and essential micronutrients such as magnesium and iron. The low glycemic index of these grains helps maintain stable blood sugar levels during prolonged physical activity, enhancing endurance performance. Furthermore, the anti inflammatory properties of certain ancient grains aid in post exercise recovery, reducing muscle soreness and fatigue. Brands are leveraging these benefits to differentiate their products in a crowded market, appealing to health conscious consumers who prioritize natural and functional ingredients. The expansion of the fitness industry and the growing participation in endurance sports globally further amplify demand. Collaborations between grain producers and sports nutrition companies are leading to innovative formulations that optimize bioavailability and taste. This synergy of performance benefits and natural sourcing positions sports nutrition as a key growth engine for the ancient grain industry.

REGIONAL ANALYSIS

North America Ancient Grain Market Analysis

North America dominated the ancient grain market and captured a 40.5% share in 2025. The region’s dominance is attributed to high consumer awareness regarding health and wellness, coupled with a robust food processing industry. The United States and Canada are early adopters of trends such as gluten free diets and plant based nutrition, driving significant demand for quinoa, amaranth, and chia seeds. As per recent trade data, imports of quinoa into the US have shown moderate growth and stabilization over the past decade, establishing it as a staple health food rather than a niche commodity. The presence of major health food retailers and e commerce platforms facilitates easy access to ancient grain products for a broad consumer base. Government initiatives promoting dietary diversity and sustainable agriculture also support market growth. The region is a hub for innovation in food technology, with numerous startups developing novel ancient grain based snacks and beverages. High disposable incomes allow consumers to pay premium prices for specialized health foods, encouraging manufacturers to invest in product development. The strong influence of social media and health influencers further accelerates the adoption of ancient grains among younger demographics. Additionally, the increasing prevalence of lifestyle diseases such as obesity and diabetes prompts individuals to seek healthier dietary options. This combination of favorable demographic trends, economic factors, and cultural shifts ensures that North America remains the central pillar of the global ancient grain market, setting trends that often ripple to other regions.

Europe Ancient Grain Market Analysis

Europe was the second largest player in the global ancient grain market and occupied a 25.2% share in 2025. The demand for these grains in Europe is driven by a strong emphasis on organic farming and sustainable food systems. Countries such as Germany, France, and the United Kingdom are key contributors, driven by stringent food safety regulations and high consumer standards. As per Eurostat, the area under organic farming in the EU increased by 56 percent between 2012 and 2020, significantly expanding the land available for sustainable cultivation. The European Union’s Farm to Fork Strategy aims to reduce the use of chemical pesticides and fertilizers, creating favorable conditions for organic farming systems and traditional crop varieties. Consumer preference for locally sourced and traditional foods supports the growth of indigenous ancient grains. The rise of vegetarianism and veganism in Europe further boosts demand for plant based protein sources. Retailers are increasingly dedicating shelf space to healthy and ethical food options, responding to consumer demand for transparency and sustainability. The region’s well established distribution networks ensure efficient supply chain management, reducing costs and improving availability. Additionally, government subsidies for sustainable agriculture provide financial incentives for farmers to cultivate ancient grains. This supportive policy environment, combined with a health conscious population, sustains Europe’s significant role in the global market, fostering innovation and quality assurance.

Asia Pacific Ancient Grain Market Analysis

The Asia Pacific is rapidly growing in the Ancient Grain Market. This region is the ancestral home of many ancient grains, including millet, sorghum, and teff, which have been staple foods for centuries. Governments in countries such as India and China are actively promoting the consumption of these traditional crops to combat malnutrition and enhance food security. As per the Food and Agriculture Organization of the United Nations, India is the largest producer of millet globally, contributing to over 40 percent of world production. The United Nations' declaration of 2023 as the International Year of Millets, proposed by India, has raised global awareness and stimulated domestic demand. Rising urbanization and changing lifestyles are leading to a resurgence of interest in traditional diets among younger generations who seek healthier alternatives to processed foods. The growing middle class with increasing disposable income is driving demand for premium and packaged ancient grain products. Additionally, the export potential of these grains from Asia to Western markets provides economic incentives for local producers. Investments in processing infrastructure are improving the quality and consistency of exports, meeting international standards. The region’s vast agricultural base and cultural familiarity with ancient grains provide a strong foundation for market expansion, making it a critical player in the global supply chain.

Latin America Ancient Grain Market Analysis

Latin America is another key player in the Ancient Grain Market due to its role as a major producer and exporter of quinoa and amaranth. Countries such as Peru, Bolivia, and Ecuador are the primary sources of high quality quinoa, benefiting from ideal climatic conditions in the Andean highlands. As per the Ministry of Agrarian Development and Irrigation of Peru, quinoa exports have shown volatility due to climate factors, with a sharp decline in 2023 followed by a rebound in subsequent seasons. The global popularity of quinoa has transformed it from a subsistence crop into a valuable cash crop, improving livelihoods for smallholder farmers. However, the region also faces challenges related to sustainable farming practices and equitable benefit sharing. Domestic consumption of ancient grains is increasing as health awareness rises among urban populations. Governments are implementing programs to promote the nutritional benefits of native crops and encourage their inclusion in school feeding programs. The development of value added products such as quinoa flour and snacks is adding diversity to the local market. Trade agreements with North America and Europe facilitate export growth, although logistical constraints remain a hurdle. The region’s commitment to preserving agricultural biodiversity and promoting indigenous crops ensures its continued relevance in the global ancient grain landscape, balancing export demands with local food security needs.

Middle East and Africa Ancient Grain Market Analysis

The Middle East and Africa region is likely to expand notably in the global Ancient Grain Market. This region is the origin of several ancient grains, including teff, sorghum, and fonio, which are staple foods in many African countries. As per the African Development Bank, initiatives like TAAT (Technologies for African Agricultural Transformation) are encouraging the cultivation of drought-resistant crops like sorghum and millet to enhance food security in arid regions. In Ethiopia, teff is a crucial crop, supporting millions of smallholder farmers and providing essential nutrients to the local population. The Middle East is seeing a gradual increase in the adoption of ancient grains due to rising health consciousness and the influence of global dietary trends. Urban centers in countries such as the United Arab Emirates and Saudi Arabia are witnessing a surge in demand for healthy and organic food options. Import dependencies for certain grains are driving investments in local production and processing capabilities. International development agencies are supporting projects to improve yield and quality of ancient grains, facilitating their integration into global supply chains. The region’s strategic location offers opportunities for trade with Europe and Asia. While currently a smaller market, the combination of agricultural heritage, climate resilience needs, and emerging health trends positions the Middle East and Africa as an emerging frontier for ancient grain cultivation and consumption.

COMPETITIVE LANDSCAPE

The competition in the Ancient Grain Market is characterized by a mix of large multinational corporations and specialized niche players who vie for market dominance through differentiation and innovation. Large agribusinesses leverage their extensive distribution networks and economies of scale to offer competitive pricing and reliable supply to industrial clients. In contrast, smaller companies focus on premium quality organic certification and unique heritage varieties to appeal to health conscious consumers. The market is fragmented with no single entity holding absolute dominance, leading to intense rivalry in specific segments such as quinoa and spelt. Companies are increasingly competing on sustainability credentials, highlighting their commitment to fair trade and environmental stewardship. Product differentiation through novel formats such as puffed grains and instant mixes serves as a key competitive tool. Brand loyalty plays a significant role as consumers often prefer established names known for quality and transparency. Price volatility due to supply constraints can shift competitive dynamics rapidly, favoring those with robust risk management strategies. Innovation in processing technologies that enhance texture and flavor also provides a competitive edge. Overall the market remains dynamic with continuous entry of new players and evolving consumer trends shaping the competitive landscape significantly.

KEY MARKET PLAYERS

Some of the major companies in the global ancient grain market are

- Ardent Mills (U.S.)

- Snyder’s-Lance Inc. (U.S.)

- Crunchmaster Inc. (U.S.)

- SK Food International (U.S.)

- Purely Elizabeth Inc. (U.S.)

- Quinoasure Inc. (U.S.)

- Great River Organic Milling Inc. (U.S.)

- Urbane Grain Inc. (U.S.)

- Nature’s Path Foods (Canada)

- GFB Great Foods (India)

Top Players in the Market

- The Quinoa Corporation stands as a premier supplier of high quality quinoa and other ancient grains globally. Headquartered in the United States, the company focuses on sustainable sourcing from the Andean region to ensure ethical trade practices. They have recently expanded their processing facilities to enhance product purity and consistency for industrial clients. The corporation actively collaborates with farmers to implement regenerative agricultural techniques that improve soil health and crop yield. By investing in advanced cleaning and packaging technologies, they maintain superior product standards that meet rigorous international food safety regulations. Their strategic partnerships with major food manufacturers enable the integration of quinoa into diverse product lines ranging from snacks to ready meals. This commitment to quality and sustainability strengthens their reputation as a trusted partner in the global supply chain. The company also engages in consumer education initiatives to highlight the nutritional benefits of quinoa, driving demand across various demographic segments and reinforcing their leadership in the niche ancient grain sector.

- Archer Daniels Midland Company leverages its extensive global network to distribute a wide variety of ancient grains including millet sorghum and amaranth. The multinational food processor integrates these ingredients into its broad portfolio of human nutrition and animal feed products. Recent investments in research and development have focused on improving the functional properties of ancient grain flours for bakery and confectionery applications. The company has strengthened its position by acquiring specialized processing units that enhance the efficiency of handling minor crops. Their robust logistics infrastructure ensures reliable supply to customers worldwide, mitigating risks associated with seasonal variations. Archer Daniels Midland emphasizes transparency in sourcing, working directly with agricultural communities to promote sustainable farming practices. This approach not only secures raw material availability but also supports rural economies. The company offers customized solutions and technical support to help food manufacturers seamlessly incorporate ancient grains into mainstream products. This approach expands their market reach and fosters long-term customer relationships in the competitive global ingredient landscape.

- Bob’s Red Mill Natural Foods is a renowned brand dedicated to providing whole grain and ancient grain products to health conscious consumers. The company offers an extensive range of items including spelt kamut and teff flours as well as whole grain blends. Their commitment to stone grinding methods preserves the nutritional integrity and flavor of the grains. Recent expansions in production capacity have allowed the company to meet growing demand while maintaining strict quality control standards. Bob’s Red Mill actively promotes employee ownership and community engagement, which enhances brand loyalty and trust among consumers. The company participates in various health and wellness events to educate the public about the benefits of ancient grains. Their innovative packaging solutions ensure freshness and convenience for home cooks and professional chefs alike. By consistently delivering high quality products and championing transparency in labeling, Bob’s Red Mill solidifies its position as a preferred choice for individuals seeking nutritious and authentic grain options. Their dedication to traditional processing methods combined with modern distribution capabilities drives sustained growth and market presence.

Top Strategies Used by the Key Market Participants

Key players in the Ancient Grain Market primarily employ strategies centered on sustainable sourcing and vertical integration to secure supply chains. Companies are increasingly establishing direct partnerships with farmers in origin regions to ensure ethical procurement and consistent quality. This approach helps mitigate risks related to climate variability and price fluctuations. Another major strategy involves product innovation and diversification, where firms develop value added items such as ready to eat snacks and fortified flours. These innovations cater to evolving consumer preferences for convenience and nutrition. Strategic acquisitions of smaller specialized processors allow larger entities to expand their technological capabilities and market reach. Additionally, marketing efforts focus on educating consumers about the health benefits and culinary versatility of ancient grains. Digital platforms are utilized to engage directly with end users and build brand loyalty. Collaborations with research institutions help in developing improved crop varieties with higher yields and better resistance to pests. By combining these strategic initiatives, market participants aim to enhance operational efficiency and differentiate their offerings in a competitive landscape.

MARKET SEGMENTATION

This research report on the global ancient grain market has been segmented and sub-segmented based on crop type, application, & region.

By Crop Type

- Gluten Containing Ancient Grains

- Gluten-Free Ancient Grains

By Application

- Bakery and Confectionary

- Sports Nutrition

- Infant Formula

- Cereals

- Frozen Food

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East Africa

Frequently Asked Questions

1. What is the global ancient grain market?

The global ancient grain market includes grains that have remained unchanged for thousands of years, such as quinoa, amaranth, millet, sorghum, spelt, chia, and einkorn, used in food products for their nutritional and functional benefits.

2. What are ancient grains, and why are they popular?

Ancient grains are minimally processed, non-hybridized grains with high nutritional value. They are popular due to rising health consciousness, gluten-free trends, and demand for natural, whole-food ingredients.

3. What factors are driving the growth of the ancient grain market?

Key growth drivers include increasing demand for healthy foods, product innovation in bakery and snack categories, rising vegan and gluten-free diets, and growing awareness of plant-based proteins.

4. Which ancient grains are most commonly consumed worldwide?

The most popular ancient grains include quinoa, amaranth, millet, spelt, chia seeds, teff, farro, sorghum, and barley.

5. Which region dominates the global ancient grain market?

North America and Europe hold significant market shares due to strong consumer demand for clean-label and functional foods, while Asia-Pacific is experiencing rapid growth.

6. What are the main applications of ancient grains?

Ancient grains are widely used in bakery products, cereals, snacks, pasta, beverages, health supplements, gluten-free foods, and ready-to-eat meals.

7. Why is quinoa one of the fastest-growing ancient grains?

Quinoa is rich in protein, iron, fiber, and essential amino acids, making it a preferred ingredient in health foods, vegan meals, and gluten-free alternatives.

8. What challenges does the ancient grain market face?

Challenges include fluctuating crop yields, limited supply in some regions, higher production costs, and competition from conventional grains.

9. What is the future outlook for the global ancient grain market?

The market is expected to grow steadily as demand increases for clean-label foods, plant-based proteins, gluten-free products, and innovative ancient grain-based snacks and bakery items.

10. Who are the key players in the global ancient grain market?

Major companies include The Hain Celestial Group, Bob’s Red Mill, Ardent Mills, Nature’s Path Foods, Healthy Food Ingredients, Inc., and Associated British Foods.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com