Asia Pacific Car Sharing Market Size, Share, Trends & Growth Forecast Report By Booking Type (Online, Offline), Application (Business/Corporate, Leisure), Vehicle Type (Hatchback, Sedan, SUVs, MPVs), Type (Peer-To-Peer, Free Floating), Trip Type (One-Way, Round Trip), and Country (India, China, Japan, South Korea, Australia, New Zealand, Rest of APAC) – Industry Analysis From 2025 to 2033.

Asia Pacific Car Sharing Market Size

The size of the Asia Pacific car-sharing market was worth USD 2.27 billion in 2024. The Asia Pacific market is anticipated to grow at a CAGR of 20.86% from 2025 to 2033 and be worth USD 12.49 billion by 2033 from USD 2.74 billion in 2025.

Car sharing services which allow users to rent vehicles for short durations through digital platforms are gaining traction as an alternative to traditional car ownership. Urbanization in the Asia region is accelerating which intensifies the need for sustainable and flexible transportation solutions. Cities like Tokyo along with Singapore and Sydney have embraced car sharing as a means to reduce traffic congestion and carbon emissions. Transportation is a major contributor to global CO2 emissions which emphasizes governments to promote shared mobility initiatives as part of their sustainability efforts. Additionally, the proliferation of smartphones and mobile payment systems has facilitated seamless access to car sharing platforms which enhance user convenience. s

MARKET DRIVERS

Rising Urbanization and Traffic Congestion

The rapid pace of urbanization in the Asia Pacific region serves as a significant driver for the car sharing market. Cities like Jakarta and Bangkok consistently rank among the most congested globally with commuters spending up to 60 hours annually in traffic jams. Car sharing offers a practical solution by reducing the number of privately owned vehicles on the road. Additionally, government initiatives to promote sustainable urban mobility further amplify demand. For example, Singapore’s Land Transport Authority has implemented strict vehicle ownership policies which encourage residents to adopt car sharing as a cost-effective and eco-friendly alternative.

Increasing Adoption of Smart Mobility Solutions

Increasing adoption of smart mobility solutions driven by advancements in digital technologies and evolving consumer preferences is another key driver of market growth. Over 70.45% of urban millennials in the region prioritize access over ownership favoring on-demand services like car sharing. For instance, South Korea’s Socar has integrated AI-driven algorithms to optimize vehicle availability and pricing which enhance user experience and operational efficiency. Moreover, the integration of IoT and GPS technologies enables real-time tracking and seamless booking processes making car sharing more accessible and convenient.

MARKET RESTRAINTS

Limited Awareness and Trust Issues

Limited awareness and trust issues among consumers particularly in rural and semi-urban areas remain one of the primary restraints in the Asia Pacific car sharing market. Over 60.23% of households in these regions still prefer traditional car ownership due to concerns about reliability and safety. Additionally, incidents such as vehicle damage or theft during rentals often deter potential users from adopting car sharing. Without robust insurance and customer support systems these companies struggle to address these concerns effectively which slows market penetration.

High Operational Costs and Infrastructure Gaps

High operational costs and infrastructure gaps present another significant restraint limiting the scalability and widespread implementation of car sharing services across the Asia Pacific region. Setting up a car sharing fleet in urban areas can incur costs exceeding $1 million primarily due to vehicle procurement, maintenance and parking space rentals. For example, India’s Mahindra Zoom faced challenges in expanding its operations due to insufficient charging stations for electric vehicles. Moreover, fragmented regulatory frameworks across countries create additional barriers which require companies to adapt to varying compliance standards.s

MARKET OPPORTUNITIES

Integration of Electric Vehicles (EVs)

The integration of electric vehicles (EVs) presents a significant opportunity for the Asia Pacific car sharing market. Governments across the region are incentivizing the adoption of EVs to reduce carbon emissions and dependence on fossil fuels. The number of EVs in the region is projected to exceed 10 million by 2025 creating immense demand for EV-based car sharing services. For instance, China’s Didi Chuxing has launched an EV-focused car sharing platform which offers affordable and eco-friendly rides. Additionally, falling battery costs and advancements in charging infrastructure further amplify the feasibility of EV integration.

Expansion into Tier-II and Tier-III Cities

Expansion into tier-II and tier-III cities presents a promising opportunity for car sharing services as these areas experience rapid economic growth and urbanization while creating a fertile ground for market penetration. Indonesia’s Grab has introduced affordable car sharing options in cities like Surabaya and Bandung catering to the rising middle-class population. Moreover, the increasing penetration of smartphones and internet connectivity ensures seamless access to car sharing platforms which foster adoption. These factors ensure sustained growth for the market as companies explore new geographies.

MARKET CHALLENGES

Regulatory and Policy Uncertainty

Regulatory and policy uncertainty poses a significant challenge for the Asia Pacific car sharing market as the lack of harmonized frameworks hinders the consistent implementation and growth of shared mobility services across the region. Compliance standards vary significantly between countries with some imposing strict mandates while others maintain lenient policies. For example, Australia’s stringent vehicle safety and emissions regulations require car sharing providers to invest heavily in compliance whereas similar services in Indonesia may operate with minimal oversight. This inconsistency creates operational inefficiencies for companies operating across multiple jurisdictions often requiring them to adapt their business models to meet varying standards. Addressing these disparities is crucial to fostering a cohesive and efficient market ecosystem.

Resistance to Behavioral Change

Another challenge is resistance to behavioral change among traditional consumers particularly in rural and semi-urban areas. Over 70.29% of households in these regions still view car ownership as a status symbol deterring them from adopting car sharing services. Additionally, cultural and generational factors contribute to this resistance with older consumers preferring personal vehicles over shared alternatives. This reluctance to embrace innovation slows down the pace of adoption which limits the market’s potential impact.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Booking Type, Application Type, Vehicle Type, Type, Trip Type, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Zipcar Inc., Zoomcar Ltd., Share Now GmbH, Getaround Inc., and SOCAR Group. |

SEGMENTAL ANALYSIS

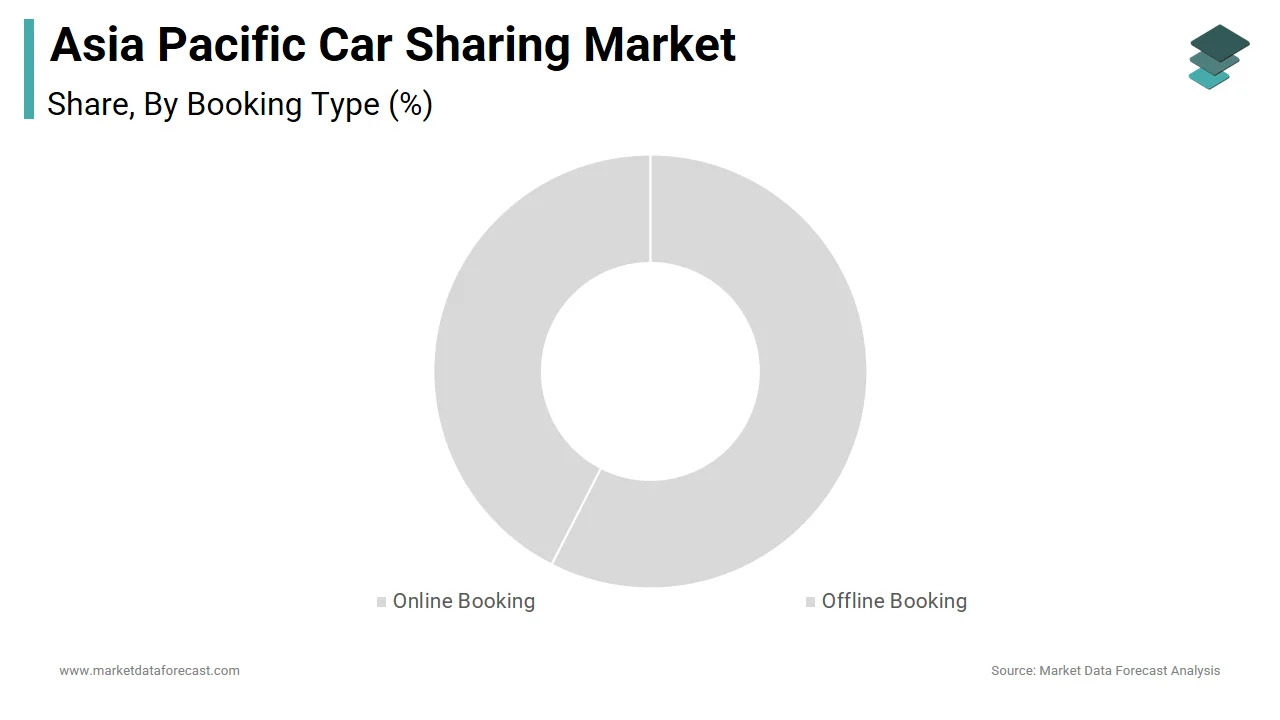

By Booking Type Insights

The online booking segment dominated the Asia Pacific car sharing market by capturing 65.08% of the share in 2024 with the region’s rapid digital transformation and widespread adoption of smartphones and mobile payment systems. China’s Didi Chuxing reported that over 80.7% of its bookings are made through mobile apps. Another key factor is the convenience and flexibility offered by online booking systems. Over 70.4% of urban millennials in the region prefer on-demand services favoring platforms that integrate real-time vehicle tracking and instant reservations.

The offline booking segment is projected to witness a CAGR of 12.3% during the forecast period. This growth is fueled by the increasing adoption of kiosks and physical counters in tier-II and tier-III cities where digital literacy remains limited. Over 40.22% of rural households still rely on traditional methods for transactions creating demand for offline booking options.Additionally, partnerships with local businesses and transportation hubs further amplify demand. For example, Indonesia’s Grab collaborates with convenience stores to offer offline booking services which ensure accessibility for first-time users.s

By Application Type Insights

The leisure applications segment dominated the Asia Pacific car sharing market with 55.88% of the share in 2024 and is driven by the growing preference for flexible and cost-effective transportation options during vacations and weekend getaways. Australia’s GoGet reported a 30.54% increase in weekend bookings.Another key factor is the integration of tourism platforms with car sharing services. Over 40.2% of travelers in Southeast Asia use shared mobility solutions to explore tourist destinations, which amplifies demand for leisure-focused offerings.

The business/corporate applications segment is projected to witness a CAGR of 15% during the forecast period. This growth is propelled by the increasing adoption of car sharing services for corporate travel and employee commutes. Additionally, government incentives promoting sustainable business practices further amplify demand. For example, South Korea’s Hyundai Motor Group offers corporate car sharing packages integrated with EV fleets aligning with carbon neutrality goals.s

By Vehicle Type Insights

The hatchbacks segment was the largest of the with 45.3% of the sAsia Pacific car sharing market share in 2024. Hatchbacks account for over 60.01% of shared vehicles in cities like Mumbai and Jakarta. Another key factor is the growing adoption of electric hatchbacks. EV-based hatchbacks are gaining popularity due to lower maintenance costs and environmental benefits. These dynamics position hatchbacks as a preferred choice for shared mobility providers.

The Sport utility vehicles (SUVs) segment is lucratively to witness a CAGR of 18.12% during the forecast period. This growth is fueled by the increasing demand for spacious and versatile vehicles particularly for leisure and long-distance travel. Over 40.57% of car sharing users in the region prefer SUVs for family outings which amplifies demand for these vehicles. Additionally, advancements in battery technology have enabled the integration of electric SUVs into car sharing fleets. For example, China’s NIO has launched an EV-based SUV car sharing service targeting urban professionals.

By Type Insights

The Peer-to-peer car sharing segment was the largest in the Asia Pacific market by capturing 60.23% of the share. This growth is driven by its cost-effectiveness and community-driven model which appeals to budget-conscious consumers. Over 50.3% of car sharing users in the region prefer peer-to-peer platforms due to lower rental rates compared to traditional models. Another key factor is the rising adoption of shared economy principles.s

The free-floating car sharing segment is expected to register a CAGR of 20.09% during the forecast period with sthe increasing adoption of on-demand mobility solutions in densely populated urban areas. Additionally, advancements in GPS and IoT technologies enable real-time vehicle tracking and seamless access which enhance user convenience. These innovations ensure sustained growth for the free-floating segment.s

By Trip Type Insights

The round-trip car sharing dominated the market by capturing 50.33% of the share in 2024. This growth is driven by its structured model which ensures predictable usage patterns and reduces operational complexities. Over 60.3% of car sharing users in the region prefer round-trip services for planned activities such as airport transfers and weekend getaways. sAnother key factor is the reliability of round-trip services. Round-trip models minimize vehicle downtime and enhance fleet utilization making them a preferred choice for providers.

The one-way car sharing segment is projected to witness a CAGR of 22.1% during the forecast period. This growth is fueled by the increasing demand for flexible and spontaneous travel options. Over 50.2% of urban commuters in the region prefer one-way services for daily commutes and last-mile connectivity which amplifies demand. Additionally, the integration of AI-driven algorithms optimizes vehicle availability and pricing which enhances user experience.

COUNTRY LEVEL ANALYSIS

China was the top performer of the Asia Pacific car sharing market and accounted for 35.23% of the regional market share in 2024 with the country’s status as the world’s largest automotive market and a leader in electric vehicle (EV) adoption. Over 5 million EVs are in use across the country which creates immense opportunities for EV-based car sharing services. Another factor is the government’s push for sustainable urban mobility. Initiatives like the “Green GDP” framework promote shared mobility solutions while ensuring alignment with environmental goals.

India was positioned second in holding the dominant share of the Asia Pacific car sharing market. The country’s rapid urbanization and rising middle-class population drive demand for affordable and flexible transportation options. Over 40.34% of urban households prefer shared mobility services while fostering innovation in the sector. Additionally, the integration of mobile payment systems enhances accessibility which ensures sustained growth for the market.

Japan’s advanced technological infrastructure and aging population drive demand for convenient and eco-friendly mobility solutions. Over 30.23% of urban residents use car sharing services which amplifies demand. Another factor is the focus on reducing carbon emissions. EV-based car sharing services align with Japan’s carbon neutrality goals which ensure long-term sustainability.

South Korea’s car sharing market is driven by its emphasis on smart city initiatives and technological innovation. Over 50.76% of urban commuters use shared mobility solutions which create immense opportunities for growth. Additionally, government policies promoting EV adoption further amplify demand. These initiatives emphasize South Korea’s proactive approach to adopting advanced mobility solutions.

Australia and New Zealand’s car-sharing market is driven by their focus on sustainable and flexible transportation options. Over 40.33% of urban households use car sharing services which ensure steady adoption. Another factor is the integration of tourism platforms with car sharing services which enhance accessibility for travelers. These efforts position the region as a leader in responsible mobility practices.

KEY MARKET PLAYERS

Some of the noteworthy companies in the Asia Pacific car sharing market profiled in this report are Zipcar Inc., Zoomcar Ltd., Share Now GmbH, Getaround Inc., and SOCAR Group.

TOP LEADING PLAYERS IN THE MARKET

Didi Chuxing

Didi Chuxing is a global leader in shared mobility with a significant presence in the Asia Pacific car sharing market. The company leverages its extensive technological expertise to offer innovative solutions such as EV-based car sharing and AI-driven route optimization. Didi’s contribution to the global market lies in its ability to integrate sustainable practices into shared mobility while aligning with environmental goals. Its focus on affordability and accessibility ensures widespread adoption across diverse demographics. Additionally, Didi’s partnerships with local governments and EV manufacturers position it as a pioneer in eco-friendly urban transportation.

Grab

Grab is a key player in the Asia Pacific car sharing market renowned for its versatile platform that combines ride-hailing, car sharing and delivery services. The company’s emphasis on localized solutions tailored to regional needs has amplified its impact in emerging markets like Indonesia and Vietnam. Grab’s commitment to innovation is evident in its integration of AI and IoT technologies enhancing user experience and operational efficiency. Globally, Grab plays a pivotal role in shaping the future of shared mobility by introducing scalable and inclusive solutions. Its strong ecosystem ensures consistent growth in the region.

GoGet

GoGet is a leading provider of car sharing services with a strong foothold in Australia and New Zealand. The company specializes in flexible round-trip and one-way models catering to both leisure and business users. GoGet’s contributions to the global market include pioneering innovations in fleet management and customer-centric services. Its focus on sustainability and community-driven models further amplifies its impact on the shared mobility landscape.

TOP STRATEGIES USED BY KEY PLAYERS IN THE MARKET

Strategic Partnerships and Collaborations

Strategic partnerships and collaborations are a top priority for key players in the Asia Pacific car sharing market enabling them to enhance technological capabilities and broaden their market reach. By collaborating with EV manufacturers and technology firms along with local governments these companies gain access to innovative solutions and regional expertise. Partnerships with EV providers allow companies to integrate eco-friendly fleets while fostering innovation and adoption.

Focus on Sustainability and Eco-Friendly Solutions

Sustainability remains a cornerstone of competitive strategies adopted by leading players. Companies invest heavily in electric vehicles (EVs) and renewable energy solutions to reduce carbon footprints and operational costs. This approach not only enhances brand reputation but also aligns with stringent regulatory standards. Additionally, the integration of green technologies ensures compliance with global environmental goals while positioning car sharing as a critical enabler of sustainable urban mobility.

Expansion of Flexible and Inclusive Services

Expansion of flexible and inclusive services is a key strategy for leading players as they broaden their offerings with features such as adaptable booking options and inclusive pricing models to meet the growing demand for accessible mobility solutions. Implementing features like offline booking and multi-language support ensures seamless access for diverse user groups. This strategy aligns with the region’s focus on digital transformation while fostering innovation and adoption across geographies.

COMPETITION OVERVIEW

The Asia Pacific car-sharing market is characterized by intense competition driven by the presence of both global giants and regional innovators vying for dominance. Global leaders like Didi Chuxing along with Grab and GoGet leverage their extensive experience as well as in advanced technologies and strong distribution networks to maintain leadership positions. Meanwhile, regional players focus on niche markets while offering cost-effective solutions tailored to local regulatory frameworks and consumer preferences. The competitive landscape is further shaped by rapid advancements in EVs, IoT and AI which redefine the capabilities of shared mobility solutions. Players must continuously innovate to keep pace with evolving customer expectations and urbanization trends.

RECENT MARKET DEVELOPMENTS

- In February 2023, Didi Chuxing partnered with a leading Chinese EV manufacturer to launch an EV-based car sharing platform in tier-II cities.

- In May 2023, Grab expanded its offline booking services to rural areas in Indonesia.

- In July 2023, Hyundai Motor Group introduced corporate car-sharing packages integrated with EV fleets in South Korea.

- In October 2023, GoGet launched a marketing campaign targeting leisure travelers in Australia.

- In December 2023, NIO acquired a Singapore-based AI startup specializing in GPS and IoT technologies.

MARKET SEGMENTATION

This Asia Pacific car-sharing market research report is segmented and sub-segmented into the following categories.

By Booking Type

- Online Booking

- Offline Booking

By Application Type

- Business/Corporate

- Leisure

By Vehicle Type

- Hatchback

- Sedan

- Sports Utility Vehicles (SUVs)

- Multi-Purpose Vehicles (MPVs)

By Type

- Peer-To-Peer

- Free Floating

By Trip Type

- One-Way

- Round Trip (You may want to add this if it's applicable)

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What factors are driving the Asia Pacific car sharing market?

The Asia Pacific car sharing market is driven by rapid urbanization, government support for sustainable mobility, smartphone adoption, digital payments, and the demand for affordable, flexible transportation in congested cities.

2. What challenges are impacting the Asia Pacific car sharing market?

The Asia Pacific car sharing market faces challenges from high operational costs, fragmented regulations, limited awareness in rural areas, trust and safety concerns, and resistance to changing traditional car ownership habits.

3. What opportunities exist in the Asia Pacific car sharing market?

The Asia Pacific car sharing market offers opportunities in integrating electric vehicles, expanding into tier-II and tier-III cities, leveraging AI and IoT for better services, and forming partnerships for sustainable, inclusive mobility solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com