Asia Pacific Mobile Phone Insurance Market Size, Share, Trends & Growth Forecast Report By Phone Type (New Phone, Refurbished), Coverage (Physical Damage, Electronic Damage, Virus Protection, Data Protection, Theft Protection), Distribution Channel (Mobile Operators, OEMs, Retailers, Online), End User (Corporate, Personal), and Country (India, China, Japan, South Korea, Australia) – Industry Analysis From 2024 to 2033.

Asia Pacific Mobile Phone Insurance Market Summary

The Asia Pacific mobile phone insurance market size was estimated at USD 7.6 billion in 2024 and is projected to reach USD 18.22 billion by 2033, growing at a CAGR of 10.2% from 2024 to 2033. Increasing smartphone adoption, rising device repair costs, and bundled insurance offerings are driving market expansion across both urban and emerging markets.

Key Market Trends & Insights

- China accounted for the largest share of 30.3% in 2024.

- India held the second-largest share with 18.6% in 2024.

- Based on distribution channel, the online channel is projected to grow at the fastest CAGR of 20.3% from 2024 to 2033.

- Based on coverage, the physical damage segment dominated the market with a 45.4% share in 2024.

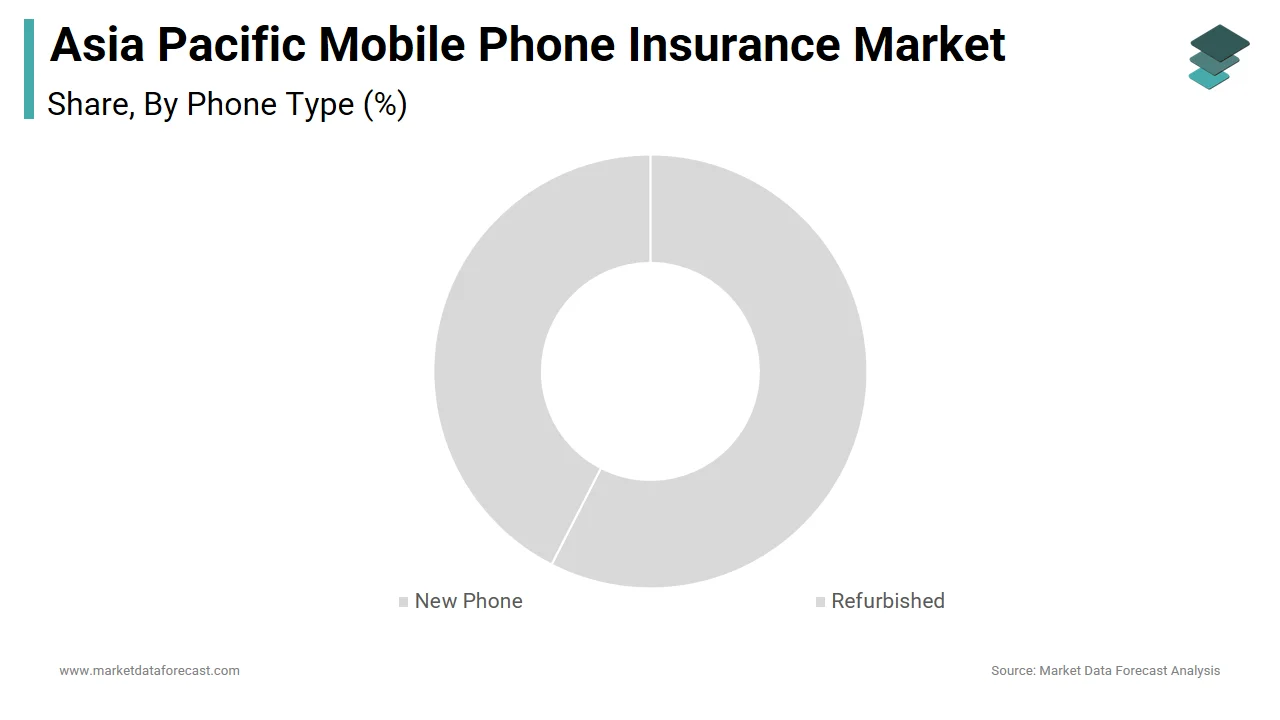

- Based on phone type, the new phone insurance segment held the leading share in 2024.

Market Size & Forecast

- 2024 Market Size: USD 7.6 Billion

- 2033 Projected Market Size: USD 18.22 Billion

- CAGR (2024–2033): 10.2%

- China: Largest market in 2024

- Online Channel: Fastest growing segment

Asia Pacific Mobile Phone Insurance Market Size

The Asia Pacific mobile phone insurance market is projected to grow from USD 7.6 billion in 2024 to reach USD 18.22 billion by 2033, at a CAGR of 10.2% from 2024 to 2033.

Mobile phone insurance has emerged as an essential service in a region where smartphone penetration is exceptionally high, with over 70% of the population owning a mobile device, according to the International Telecommunication Union. The region’s rapid urbanization, increasing disposable incomes, and rising adoption of premium smartphones have further fueled demand for mobile phone insurance. As per the Asian Development Bank, the proliferation of expensive flagship models from brands like Apple and Samsung has created a pressing need for affordable and comprehensive insurance solutions. Similarly, Australia’s Department of Communications and the Arts emphasizes the role of mobile phone insurance in reducing repair costs and enhancing consumer confidence.

MARKET DRIVERS

Rising Smartphone Penetration and Premiumization

The exponential rise in smartphone penetration and the growing preference for premium devices are primary drivers of the Asia Pacific mobile phone insurance market. According to the United Nations Economic and Social Commission for Asia and the Pacific, smartphone ownership in the region is projected to grow by 25% by 2030, which is creating a surge in demand for protective services. For example, India’s Ministry of Electronics and Information Technology reports that over 60% of urban consumers now purchase smartphones priced above $400, necessitating insurance coverage for accidental damage and theft. These trends demonstrate how the shift toward premium devices is propelling the adoption of mobile phone insurance tailored to meet diverse customer needs.

Increasing Incidence of Device Damage and Theft

Another significant driver is the rising incidence of device damage and theft, which compels consumers to seek reliable insurance solutions. Similarly, Malaysia’s Ministry of Home Affairs reports that accidental damage accounts for over 40% of claims filed under mobile phone insurance policies, ensuring steady growth in demand. Moreover, the integration of online platforms enables insurers to offer seamless claim processes, enhancing customer satisfaction and trust in these services.

MARKET RESTRAINTS

High Premium Costs and Limited Awareness

High premium costs and limited awareness pose significant restraints to the mobile phone insurance market, particularly among price-sensitive consumers. The Federation of Indian Chambers of Commerce and Industry notes that over 70% of rural consumers hesitate to invest in insurance due to perceived expenses, deterring widespread adoption. Additionally, the lack of standardized pricing models across the region exacerbates this issue, which is limiting the ability of smaller players to compete effectively. These financial barriers hinder the seamless adoption of mobile phone insurance in emerging markets.

Fraudulent Claims and Operational Challenges

Fraudulent claims and operational challenges also act as restraints regarding the efficiency of claim processing and fraud detection systems. The Australian Securities and Investments Commission warns that fraudulent claims targeting mobile phone insurance have increased by over 35% annually, undermining public trust in these services. Moreover, the absence of advanced fraud detection technologies forces companies to invest heavily in upgrading their infrastructure. These challenges limit the widespread adoption of mobile phone insurance among risk-averse stakeholders.

MARKET OPPORTUNITIES

Integration of AI and IoT Technologies

The integration of artificial intelligence (AI) and the Internet of Things (IoT) presents transformative opportunities for the mobile phone insurance market. AI-driven analytics can process vast amounts of data to detect fraudulent claims and enhance decision-making, improving operational efficiency. As per China’s Ministry of Science and Technology, the use of IoT-enabled sensors to monitor device conditions and predict potential damages, reducing claim processing times by up to 40%. Similarly, Australia’s Department of Industry, Science and Resources emphasizes the role of AI in personalizing insurance plans, aligning with global consumer-centric trends. These advancements position AI and IoT as key enablers of innovation in the mobile phone insurance market.

Expansion into Emerging Economies

Emerging economies in the Asia Pacific offer untapped potential for mobile phone insurance, driven by industrialization and digital transformation. The Asian Development Bank reports that over $1 trillion is being invested annually in digital infrastructure projects across Southeast Asia, creating demand for scalable and affordable solutions. As per Indonesia’s Ministry of Communication and Information Technology, the use of mobile phone insurance to support first-time smartphone users, which is ensuring inclusivity and accessibility. Vietnam’s growing middle class relies on insurance to protect their investments in premium devices.

MARKET CHALLENGES

Regulatory Fragmentation Across Countries

Regulatory fragmentation across countries represents a pressing challenge for the mobile phone insurance market regarding cross-border operations and compliance. The International Association of Insurance Supervisors states that many countries in the region have stringent regulations governing insurance offerings, limiting the adoption of unified platforms. For instance, South Korea’s Financial Supervisory Service mandates strict guidelines for transparency and pricing, complicating implementation for multinational operators.

Limited Accessibility in Rural Areas

Malaysia’s Ministry of Communications and Multimedia reports that over 30% of rural populations lack reliable internet access, hindering the adoption of online insurance platforms. According to the India’s Ministry of Rural Development, only 25% of villages have access to stable electricity, further complicating the deployment of digital solutions. These infrastructural gaps force companies to invest heavily in offline solutions, such as agent-based sales, to cater to underserved populations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Phone Type, Coverage, Distribution Channel, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Allianz SE, AIG (American International Group), Assurant Inc., Asurion LLC, Chubb Limited, Samsung Fire & Marine Insurance, Ping An Insurance, Brightstar Corp., Apple Inc. (via AppleCare), and Servify. |

SEGMENTAL ANALYSIS

By Phone Type Insights

The new phone insurance segment was the largest and held a dominant share of the Asia Pacific mobile phone insurance market in 2024. This dominance is driven by the rising adoption of premium smartphones and the increasing cost of repairs and replacements for new devices. According to the China’s Ministry of Industry and Information Technology, over 65% of urban consumers now purchase flagship models priced above $800, necessitating comprehensive insurance coverage. Another factor is the focus on customer trust. Japan’s Financial Services Agency notes that insurers offer tailored plans for new devices by enhancing consumer confidence and driving widespread adoption.

The refurbished phone insurance segment is more likely to experience a CAGR of 15.2% in the next coming years. This growth is fueled by the increasing popularity of refurbished devices as a cost-effective alternative to new phones. A key factor is the rise of sustainability initiatives. Similarly, India’s Ministry of Electronics and Information Technology emphasizes the role of insurance in boosting consumer confidence in second-hand devices, which is aligning with global circular economy goals. Another factor is the focus on affordability. Malaysia’s Ministry of Domestic Trade and Consumer Affairs reports that refurbished phone insurance reduces ownership costs by up to 30%, further accelerating adoption in emerging markets.

By Coverage Insights

The physical damage coverage dominated the Asia Pacific mobile phone insurance market with 45.4% of the total share in 2024. One key factor is the exponential rise in smartphone usage. According to the Japan’s Ministry of Internal Affairs and Communications, over 70% of claims filed under mobile phone insurance are related to physical damage with its importance. Similarly, South Korea’s National Police Agency notes that accidental damage accounts for over 40% of smartphone incidents by ensuring steady demand for this type of coverage. Another factor is the focus on affordability. Vietnam’s Ministry of Finance reports that physical damage insurance reduces repair costs by up to 50%, which is making it an attractive option for price-sensitive consumers.

The data protection coverage is lucratively growing with a CAGR of 18.5%. A significant factor is the rise of cybersecurity threats. Australia’s Cyber Security Centre warns that cyberattacks targeting mobile devices have increased by over 40% annually, which is creating a pressing need for data protection services. Similarly, Japan’s Ministry of Economy, Trade and Industry emphasizes the role of data protection insurance in enhancing consumer confidence by aligning with global privacy regulations. Another factor is the focus on innovation. Malaysia’s Ministry of Communications and Multimedia reports that insurers are integrating AI-driven tools to detect and prevent data breaches, which is further accelerating adoption among tech-savvy users.

By Distribution Channel Insights

The mobile operators dominated the Asia Pacific mobile phone insurance market with 50.4% of the share in 2024. One major factor is the growing collaboration between insurers and telecom providers. As per the India’s Ministry of Communications, over 60% of mobile phone insurance policies are sold through operator channels by ensuring seamless integration with customer acquisition strategies. Similarly, Singapore’s Infocomm Media Development Authority notes that bundled offerings enhance convenience and affordability, mobile operators’ position as the largest distribution channel. Another factor is the focus on customer retention. Thailand’s Ministry of Digital Economy and Society reports that insurance bundles improve customer loyalty by ensuring sustained demand for these services.

The online distribution channel is likely to grow with a projected CAGR of 20.3%. This growth is fueled by the increasing adoption of e-commerce platforms and digital payment systems. As per Australia’s Department of Industry, Science and Resources, over 70% of consumers prefer purchasing insurance online due to convenience and transparency. Similarly, South Korea’s Ministry of SMEs and Startups emphasizes the role of online platforms in reducing operational costs for insurers, aligning with global efficiency goals. Another factor is the focus on accessibility. Indonesia’s Ministry of Communication and Information Technology reports that online channels enable rural populations to access insurance services without requiring physical infrastructure.

By End User Insights

The personal segment dominated the Asia Pacific mobile phone insurance market, holding approximately 80% of the total share, according to the Federation of Asian Chambers of Commerce and Industry. This dominance is driven by the widespread adoption of smartphones for personal use and the increasing awareness of protective services.

One key factor is the exponential rise in smartphone ownership. As per China’s Ministry of Industry and Information Technology, over 90% of urban households rely on smartphones for daily activities, necessitating insurance coverage for accidental damage and theft. Similarly, Japan’s Ministry of Internal Affairs and Communications notes that personal insurance reduces repair costs by up to 60% by ensuring affordability and accessibility for individual consumers. Another factor is the focus on inclusivity.

The corporate segment is lucratively to grow with a projected CAGR of 12.8% in the next coming years. A significant factor is the rise of remote work trends. According to the Australia’s Department of Employment and Workplace Relations, over 60% of businesses now provide company-issued smartphones to employees by creating demand for comprehensive insurance coverage. Similarly, South Korea’s Ministry of Trade, Industry and Energy emphasizes the role of corporate insurance in reducing operational risks, aligning with global enterprise goals. Another factor is the focus on efficiency. Malaysia’s Ministry of Human Resources reports that insurers offer group plans to streamline claim processes, which is accelerating adoption among corporate entities.

COUNTRY LEVEL ANALYSIS

China was the top performer in the Asia Pacific mobile phone insurance market with 30.3% of the share in 2024 due to its status as a global leader in smartphone manufacturing and consumption, supported by robust investments in digital infrastructure. The Chinese Academy of Sciences reports that over 70% of urban consumers own premium smartphones by necessitating comprehensive insurance coverage. Additionally, China’s Belt and Road Initiative promotes cross-border collaborations, which is creating demand for scalable and innovative mobile phone insurance solutions tailored to diverse markets.

India was next by holding 18.6% of the Asia Pacific mobile phone insurance market share in 2024. The country’s rapid adoption of mobile phone insurance is driven by its growing middle class and increasing smartphone penetration. According to India’s Ministry of Electronics and Information Technology, over 60% of first-time smartphone users purchase insurance to protect their investments, ensuring steady growth in demand. Furthermore, India’s focus on affordability has accelerated the adoption of bundled offerings, which is aligning with global consumer-centric trends.

Japan mobile phone insurance market is swiftly growing with prominent growth opportunities with its advanced technological expertise and reliance on smartphones for daily activities. The Ministry of Internal Affairs and Communications emphasizes the adoption of physical damage and data protection coverage to enhance consumer confidence. Additionally, Japan’s emphasis on sustainability ensures widespread adoption of refurbished phone insurance by aligning with global standards.

South Korea’s focus on innovation and cybersecurity driving mobile phone insurance adoption . As per the National Police Agency, the use of theft protection and data security solutions to combat rising cybercrime rates. Additionally, South Korea’s vast network of mobile operators and retailers necessitates scalable solutions to ensure safe and efficient operations in urban areas.

Australia's mobile phone insurance market growth is due to the growing reliance on smartphones for personal and professional use. According to the Department of Communications and the Arts, over 50% of consumers rely on mobile phone insurance to reduce repair costs and enhance accessibility. Additionally, Australia’s focus on digital transformation has fueled the transition to online distribution channels, further boosting demand.

KEY MARKET PLAYERS

Some of the noteworthy companies in the APAC mobile phone insurance market profiled in this report are Allianz SE, AIG (American International Group), Assurant Inc., Asurion LLC, Chubb Limited, Samsung Fire & Marine Insurance, Ping An Insurance, Brightstar Corp., Apple Inc. (via AppleCare), and Servify.

TOP LEADING PLAYERS IN THE MARKET

Allianz Group

Allianz Group is a global leader in mobile phone insurance, with a significant presence in the Asia Pacific market. The company’s contribution to the global market lies in its innovative and customer-centric insurance solutions tailored to meet diverse needs, such as accidental damage, theft protection, and data security. Allianz leverages advanced technologies like AI and IoT to enhance claim processing efficiency and transparency. Its focus on sustainability and affordability ensures inclusivity for both urban and rural consumers, which is positioning it as a trusted partner for individuals and businesses seeking reliable mobile phone insurance.

AIG (American International Group)

AIG plays a pivotal role in advancing mobile phone insurance through its comprehensive coverage options and strategic partnerships with telecom operators and device manufacturers. Known for its robust portfolio of digital solutions, AIG empowers customers to purchase and manage policies seamlessly via online platforms. The company’s emphasis on integrating cybersecurity tools enhances data protection offerings by aligning with the growing demand for secure mobile ecosystems. By fostering collaborations with regional stakeholders, AIG continues to expand its footprint, contributing significantly to global advancements in the mobile phone insurance sector.

Assurant Inc.

Assurant Inc. is renowned for its innovative approach to mobile phone insurance, making it a key player in the Asia Pacific market. Through partnerships with leading smartphone brands and retailers, Assurant offers scalable solutions for physical damage, electronic failure, and theft protection. The company’s dedication to improving accessibility and affordability has strengthened its global reputation.

TOP STRATEGIES USED BY KEY PLAYERS IN THE MARKET

Strategic Partnerships with Telecom Operators and OEMs

Key players frequently collaborate with mobile operators, device manufacturers, and retailers to bundle insurance with smartphone purchases or service plans. These partnerships ensure seamless integration of insurance offerings into the customer journey, enhancing accessibility and adoption. For instance, insurers work closely with telecom providers to offer affordable plans tailored to first-time smartphone users, ensuring widespread reach and customer retention.

Investment in Digital Platforms and AI Technologies

To meet evolving consumer preferences, companies are investing heavily in digital platforms and AI-driven tools to streamline claim processes and enhance user experiences. For example, insurers are developing AI-powered fraud detection systems and mobile apps that enable customers to file claims instantly. This focus on innovation not only differentiates brands but also aligns with the growing demand for convenience and transparency in the region.

Expansion into Emerging Markets

Players are increasingly targeting emerging economies within the Asia Pacific region, such as Vietnam, Indonesia, and Thailand, where rising smartphone penetration is driving adoption. By establishing local distribution networks and offering localized solutions, companies aim to reduce costs and improve accessibility. This strategy allows them to capture untapped opportunities and amplify their presence in high-growth markets.

COMPETITION OVERVIEW

The Asia Pacific mobile phone insurance market is characterized by intense competition, with both global giants and regional players vying for dominance. Global leaders like Allianz Group, AIG, and Assurant leverage their technological expertise and extensive distribution networks to maintain their stronghold. Meanwhile, regional players focus on cost-effective solutions and localized services to cater to price-sensitive markets. The competitive landscape is further shaped by rapid technological advancements, with companies striving to integrate AI, IoT, and cloud computing into their offerings. Additionally, stringent regulatory frameworks governing transparency and pricing have compelled insurers to innovate continuously. Supply chain disruptions and cybersecurity threats add complexity, forcing players to adopt agile strategies. As a result, the market fosters an environment of constant evolution, where differentiation through innovation, customer-centric approaches, and strategic expansion becomes critical for sustained success.

RECENT MARKET DEVELOPMENTS

- In April 2024, Allianz Group launched a new AI-driven platform specifically designed for real-time claim processing in South Korea. This move aimed to capitalize on the country’s growing reliance on smartphones, enhancing Allianz’s market presence in the region.

- In June 2023, AIG partnered with a leading Australian telecom provider to offer bundled insurance plans for premium smartphones. This collaboration strengthened AIG’s visibility in the region’s retail sector and expanded its customer base.

- In September 2023, Assurant Inc. acquired a local insurtech startup in Singapore to expand its production capabilities for scalable and affordable insurance solutions. This acquisition enabled the company to better serve Southeast Asia’s burgeoning middle class and increase its regional footprint.

- In January 2024, IBM, a U.S.-based technology provider, introduced a suite of cloud-based insurance tools tailored for data protection in Japan. This initiative aligned with the country’s push toward enhanced cybersecurity, allowing IBM to position itself as a leader in innovative insurance technologies.

- In November 2023, SAP SE, a German software provider, signed an agreement with a Philippine retailer to develop specialized mobile phone insurance plans for refurbished devices. This partnership reinforced SAP’s prominence in precision retailing technology and expanded its application portfolio.

MARKET SEGMENTATION

This Asia Pacific mobile phone insurance market research report is segmented and sub-segmented into the following categories.

By Phone Type

- New Phone

- Refurbished

By Coverage

- Physical Damage

- Electronic Damage

- Virus Protection

- Data Protection

- Theft Protection

By Distribution Channel

- Mobile Operators

- Device OEMs

- Retailers

- Online

- Others

By End User

- Corporate

- Personal

By Country

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest Of APAC

Frequently Asked Questions

1. What drives the Asia Pacific mobile phone insurance market?

The Asia Pacific mobile phone insurance market is driven by rising smartphone adoption, urbanization, premium device sales, and growing awareness of device protection, especially in China and India

2. What challenges affect the Asia Pacific mobile phone insurance market?

The Asia Pacific mobile phone insurance market faces challenges such as low rural penetration, price sensitivity, high premiums, complex claims, and regulatory variations across countries

3. What opportunities exist in the Asia Pacific mobile phone insurance market?

Opportunities in the Asia Pacific mobile phone insurance market include digital distribution, AI-driven claims, bundled plans with telecoms, microinsurance, and growing demand in emerging economies

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com