Europe Agrochemical Tank Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Application, and Country – Industry Forecast From 2026 to 2034

Europe Agrochemical Tank Market Report Summary

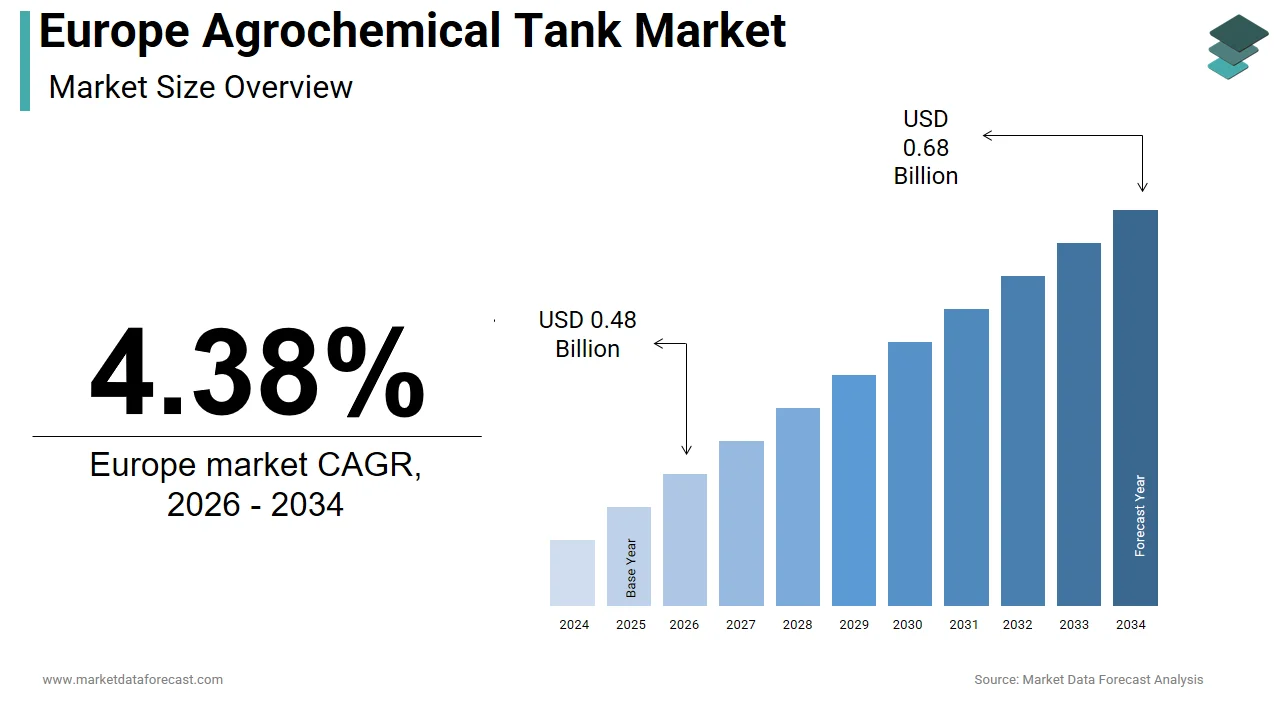

The Europe agrochemical tank market was valued at USD 0.46 billion in 2025 and is projected to grow from USD 0.48 billion in 2026 to USD 0.68 billion by 2034, registering a CAGR of 4.38% from 2026 to 2034. Market growth is driven by the increasing demand for safe storage and handling of agrochemicals, stringent environmental regulations, and the adoption of modern farming practices across Europe. Rising investments in precision agriculture, efficient chemical management systems, and durable storage infrastructure are further supporting market expansion. The growing emphasis on sustainable agriculture and regulatory compliance is also encouraging the use of high-quality agrochemical storage solutions.

Key Market Trends

- Increasing adoption of safe and compliant agrochemical storage systems.

- Rising demand for high-capacity vertical storage tanks in commercial agriculture.

- Growing investments in precision farming and modern agricultural infrastructure.

- Expansion of environmentally compliant chemical storage solutions.

- Increasing focus on durable, corrosion-resistant, and sustainable storage technologies.

Segmental Insights

- Based on type, the vertical tanks segment dominated the Europe agrochemical tank market in 2025, driven by their space-efficient design, high storage capacity, ease of installation, and widespread use for storing fertilizers, pesticides, and other agricultural chemicals.

- Based on application, the chemical storage segment accounted for the largest share of the market in 2025, supported by stringent regulations governing pesticide handling, the need to prevent chemical contamination, and increasing emphasis on safe agrochemical storage practices.

Regional Insights

The Europe agrochemical tank market continues to expand across major agricultural economies, supported by modernization of farming practices, regulatory compliance, and growing demand for efficient chemical storage infrastructure.

- Germany dominated the European market in 2025, driven by advanced agricultural technology adoption, strong environmental compliance standards, and widespread implementation of precision farming practices.

- France held a significant share of the regional market, supported by its extensive agricultural landscape, diverse crop cultivation including cereals, vineyards, and orchards, and increasing investments in modern farm infrastructure.

- Spain maintained a prominent position in the Europe agrochemical tank market due to its status as one of the European Union's largest producers of fruits and vegetables, requiring extensive use of crop protection chemicals and efficient storage systems.

Competitive Landscape

The Europe agrochemical tank market is moderately competitive, with manufacturers focusing on durable storage solutions, regulatory compliance, corrosion-resistant materials, and customized tank designs for agricultural applications. Companies are investing in product innovation, sustainable manufacturing processes, and expansion of distribution networks to strengthen their market presence. Strategic partnerships and continuous advancements in storage technologies continue to shape the competitive landscape.

Prominent companies operating in the Europe agrochemical tank market include KBK Industries, LLC, Snyder Industries, LLC, L.F. Manufacturing, Inc., Denios GmbH, Chemical Containers, Inc., Cubis AG, and ProMinent GmbH.

Note: The source text appears to contain a typographical error under the key players section ("Europe pharmaceutical gelatin market"). Based on the surrounding content, these companies are presented as key players for the Europe agrochemical tank market.

Europe Agrochemical Tank Market Size

The Europe agrochemical tank market was valued at USD 0.46 billion in 2025, is estimated to reach USD 0.48 billion in 2026, and is projected to reach USD 0.68 billion by 2034, growing at a CAGR of 4.38% from 2026 to 2034.

Agrochemical tanks are specialized storage and mixing vessels designed for the safe handling, application, and transport of liquid fertilizers, pesticides, and herbicides across agricultural operations. These critical infrastructure components include stationary bulk storage tanks, portable sprayer tanks, and intermediate bulk containers that ensure precise chemical dosage while minimizing environmental contamination risks. The European agricultural sector operates under stringent regulatory frameworks that mandate rigorous safety standards for chemical storage to protect groundwater quality and human health. As per Eurostat, the European Union utilizes approximately 156 million hectares for agricultural purposes, with intensive crop protection practices prevalent in major producing nations. The region faces increasing pressure to optimize input efficiency as the European Commission aligns with broader climate neutrality goals that emphasize reduced reliance on chemical inputs. This regulatory shift necessitates advanced tank technologies that support precision application systems and reduce waste through accurate measurement capabilities. Climate variability further complicates storage requirements as extreme weather events demand robust containment solutions resistant to corrosion and structural stress. According to the European Environment Agency, agricultural runoff remains a primary source of water pollution, driving investment in leak-proof and sealed storage systems. The transition toward digital farming integrates smart tank sensors that monitor volume levels, temperature, and chemical composition in real-time. This technological evolution aligns with broader sustainability goals while addressing operational efficiency needs for modern European farms managing complex crop protection regimes.

MARKET DRIVERS

Strict Environmental Regulations Mandate Advanced Containment and Safety Standards

The implementation of rigorous environmental legislation across the European Union is primarily driving the expansion of the European agrochemical tank market. The Nitrates Directive and Water Framework Directive impose strict limits on chemical leakage and runoff, requiring farms to adopt certified containment systems that prevent soil and water contamination. According to the European Environment Agency, agriculture is a major source of nitrogen and phosphorus runoff into European water bodies, which is requiring improved storage protocols to mitigate pollution risks. Farmers must comply with secondary containment regulations that mandate double-walled tanks or bunded areas capable of holding 110% of the largest tank volume. For instance, non-compliant storage facilities face substantial fines and operational restrictions, driving widespread replacement of aging infrastructure. The European Chemicals Agency enforces classification, labeling, and packaging regulations that require tanks to maintain chemical integrity without degradation or leaching over extended periods. Modern polyethylene and stainless steel tanks offer superior resistance to corrosive agrochemicals compared to traditional materials, ensuring compliance with safety standards. The Farm to Fork Strategy further emphasizes sustainable input management, prompting investments in tanks equipped with automated dosing systems that minimize excess usage. Regulatory audits have increased in frequency, with national authorities conducting regular inspections of storage facilities to verify adherence to safety protocols. This enforcement landscape compels agricultural operators to prioritize high-quality, compliant tanks that reduce liability risks while supporting environmental stewardship objectives mandated by European policy frameworks.

Expansion of Precision Agriculture Technologies Drives Demand for Smart Storage Solutions

The rapid adoption of precision agriculture techniques across Europe is driving substantial demand for advanced agrochemical tanks integrated with digital monitoring and control systems, further contributing to the expansion of the European agrochemical tank market. Modern farming operations increasingly rely on variable-rate application technologies that require precise chemical mixing and dispensing capabilities supported by smart tank infrastructure. According to industry analysis, a growing share of large-scale farms in Western Europe now utilizes precision farming tools, creating a receptive market for intelligent storage solutions. Smart tanks equipped with ultrasonic level sensors, flow meters, and automated valves enable real-time tracking of chemical inventory and usage patterns, enhancing operational efficiency. As per research from agricultural universities, precision application systems can significantly reduce agrochemical usage while maintaining crop protection efficacy through accurate dosage control. The integration of Internet of Things devices allows farmers to monitor tank conditions remotely, receiving alerts for low levels, leaks, or temperature fluctuations that could compromise chemical stability. Digital platforms analyze data from tank sensors to optimize purchasing schedules and prevent stockouts during critical application windows. The European Commission’s Digital Agriculture Initiative supports connectivity improvements that facilitate seamless data exchange between storage systems and farm management software. This technological synergy reduces labor requirements and minimizes human error in chemical handling processes. Manufacturers are developing modular tank systems compatible with existing precision equipment, enabling scalable upgrades for farms transitioning to digital operations. The economic benefits of reduced waste and improved application accuracy justify the higher initial investment in smart tank technologies for progressive European agricultural enterprises.

MARKET RESTRAINTS

High Capital Costs and Financial Constraints Limit Infrastructure Upgrades for Small Holdings

The substantial financial investment required for purchasing and installing compliant agrochemical storage tanks presents a significant barrier for the European agrochemical tank market, particularly for small and medium-sized farming operations that dominate the European agricultural landscape. A high-capacity stainless steel or reinforced polyethylene tank with secondary containment features can represent a significant expenditure depending on size and technical specifications. This upfront expenditure represents a considerable burden for farmers operating on narrow profit margins. According to Eurostat, almost two-thirds of the EU's farms are less than 5 hectares in size, often resulting in limited access to credit facilities or capital reserves for infrastructure improvements. Many older tanks remain in service beyond their recommended lifespan due to financial constraints, increasing the risk of leaks and regulatory non-compliance. Economic volatility, exacerbated by rising energy costs and inflationary pressures, has further tightened farm budgets. Government subsidy programs often prioritize production equipment over storage infrastructure, leaving farmers to bear the full cost of tank replacements. The fragmented nature of European agriculture complicates economies of scale that could potentially reduce unit costs for standardized tank systems. Maintenance and installation expenses add to the total cost of ownership, deterring budget-conscious operators from upgrading to newer, safer models. Without targeted financial incentives or leasing options, the high entry cost continues to restrict market penetration among the demographic segment that constitutes the majority of European agricultural producers.

Complex Regulatory Compliance and Administrative Burdens Hinder Market Adoption

Navigating the intricate web of environmental safety and chemical storage regulations imposes significant administrative challenges that discourage timely upgrades of agrochemical tank infrastructure across European farms, which is further hindering the expansion of the European market. Each member state implements varying interpretations of European Union directives, resulting in inconsistent compliance requirements that confuse farmers and increase consultation costs. According to reports from agricultural industry associations, farmers spend significant time on regulatory paperwork related to chemical storage and handling, diverting resources from core agricultural activities. The need for regular inspections, certification renewals, and documentation updates creates ongoing administrative burdens that small operators struggle to manage effectively. Local authorities may impose additional zoning restrictions or permit requirements for installing new tanks, particularly in protected water catchment areas, limiting placement options. As per reports from national agricultural ministries, obtaining permits for large-capacity storage facilities can be a lengthy process, delaying critical infrastructure projects during peak seasons. Language barriers and a lack of standardized guidance documents across different regions further complicate compliance efforts for multinational farming groups. The fear of inadvertent non-compliance and subsequent penalties leads some farmers to postpone upgrades until necessary rather than proactively investing in advanced systems. Technical specifications for tanks must meet multiple overlapping standards, including pressure ratings, material compatibility, and spill containment capacities, requiring specialized knowledge to verify. This regulatory complexity increases reliance on external consultants, adding to overall project costs and extending implementation timelines. The administrative overhead associated with compliance acts as a deterrent, particularly for older farmers who may lack familiarity with evolving digital reporting requirements.

MARKET OPPORTUNITIES

Integration of Circular Economy Principles Creates Demand for Recyclable and Sustainable Tank Materials

The growing emphasis on circular economy practices within the European agricultural sector presents significant opportunities for the European agrochemical tank market. Traditional plastic tanks often end up in landfills at the end of their lifecycle, contributing to environmental pollution and resource waste. According to data from industry associations, a substantial portion of agricultural plastic waste is not currently recycled in the EU, highlighting a significant gap that sustainable tank materials can address. Manufacturers are innovating with high-density polyethylene formulations that are fully recyclable without compromising structural integrity or chemical resistance. As per the European Bioplastics association, the market for bio-based plastics in agricultural applications is expanding, driven by regulatory support and consumer preference. Tanks made from recycled content appeal to environmentally conscious farmers seeking to reduce their carbon footprint and align with sustainability certifications. The European Commission’s Action Plan for the Circular Economy encourages industries to design products for durability, repairability, and recyclability, creating favorable conditions for green tank innovations. Government procurement policies increasingly favor suppliers demonstrating commitment to sustainable practices, providing competitive advantages for eco-friendly product lines. Collaborative initiatives between tank manufacturers and recycling firms are establishing take-back schemes that facilitate proper disposal and material recovery. These programs reduce end-of-life costs for farmers while ensuring compliance with waste management regulations. The development of modular tank designs that allow component replacement rather than full unit disposal further extends product lifespans and reduces waste generation. This shift toward sustainable materials positions manufacturers to capture value from the growing segment of farms prioritizing environmental responsibility in their operational decisions.

Growth of Contract Farming and Custom Application Services Expands Professional Storage Needs

The rise of contract farming arrangements and professional custom application services across Europe creates new demand channels for high-capacity and mobile agrochemical storage solutions, which is another prominent opportunity for the European agrochemical tank market. Large agricultural contractors who manage chemical application for multiple farms require robust portable tanks and bulk storage systems that ensure efficient logistics and compliance with safety standards. According to data from agricultural contractor associations, the contract farming sector has seen steady growth as farmers seek to outsource specialized tasks to improve operational efficiency. These service providers invest in advanced tanker trucks and mobile mixing units equipped with precise dosing mechanisms to serve diverse client needs across wide geographic areas. Professional applicators now handle a large share of total pesticide applications in Central Europe, driving demand for durable and versatile storage equipment. The consolidation of farmland into larger operational units facilitates economies of scale that justify investments in centralized bulk storage facilities shared among multiple stakeholders. Custom application companies require tanks that meet stringent transport regulations, including secure locking mechanisms and spill prevention features for road mobility. The professionalization of agricultural services raises standards for equipment quality and maintenance, encouraging the adoption of premium tank solutions with longer lifespans. Training and certification programs for applicators emphasize proper chemical handling practices, reinforcing the importance of reliable storage infrastructure. This trend toward specialized service provision shifts purchasing power from individual smallholders to larger commercial entities with greater financial capacity and technical expertise. Manufacturers can target this segment with tailored products designed for high-frequency use and easy cleaning between different chemical batches.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Volatility Impact Production Stability

The supply chain disruptions and volatile raw material costs that undermine production planning and pricing stability are significant challenges to the European agrochemical tank market expansion. Primary materials such as polyethylene, stainless steel, and specialized polymers are subject to global market fluctuations driven by energy prices and geopolitical tensions. According to industry reports, raw material costs for agricultural plastics have experienced significant increases in recent years, creating margin pressures for tank manufacturers. Dependence on imported raw materials exposes European producers to currency exchange rate risks and international trade policy changes that affect availability and cost. Transportation bottlenecks have led to periodic delivery delays during peak demand seasons, complicating inventory management for both manufacturers and customers. Labor shortages in the manufacturing sector further exacerbate production constraints. Small and medium-sized tank manufacturers lack the bargaining power to negotiate favorable long-term contracts with suppliers, leaving them vulnerable to sudden price spikes. Quality consistency suffers when manufacturers substitute materials to control costs, potentially compromising product performance and safety certifications. The cumulative effect of these supply chain pressures forces producers to pass costs onto farmers who already operate under tight financial constraints. Long-term planning becomes difficult in such volatile conditions, creating uncertainty for investment decisions regarding new production capacity or product development. Manufacturers must balance inventory levels against the risk of holding depreciating assets while ensuring adequate stock to meet seasonal demand peaks.

Technical Complexity of Chemical Compatibility and Material Degradation Risks

Ensuring long-term chemical compatibility between agrochemical formulations and tank materials presents a significant technical challenge that requires continuous research and testing to prevent premature failure. Modern agrochemicals often contain complex mixtures of active ingredients, adjuvants, and solvents that can degrade certain plastic polymers or corrode metal components over time. According to industry standards, improper material selection accounts for a significant share of tank failures, leading to leaks, contamination, and costly cleanup operations. Manufacturers must conduct extensive compatibility testing for each new chemical formulation entering the market, which increases development costs and time to market. As per data from materials research institutes, certain herbicides containing strong acids or bases can cause stress cracking in polyethylene tanks if not properly stabilized during production. The lack of standardized testing protocols across different European countries complicates certification processes and creates confusion for farmers selecting appropriate tanks for specific chemicals. Temperature fluctuations during storage can accelerate material degradation, particularly in outdoor installations where tanks are exposed to direct sunlight and extreme weather conditions. Ultraviolet radiation weakens polymer chains, reducing tensile strength and increasing brittleness unless adequate stabilizers are incorporated into the material formulation. Farmers often lack the technical knowledge to assess chemical compatibility, relying on manufacturer recommendations that may not cover all local product variations. Liability concerns arise when tank failures result in environmental damage or crop loss, prompting manufacturers to invest heavily in warranty coverage and insurance. The dynamic nature of agrochemical innovation requires constant updates to material specifications, challenging manufacturers to maintain broad compatibility portfolios while controlling production complexity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | KBK Industries, LLC, Snyder Industries, LLC, L.F. Manufacturing, Inc., Denios GmbH, Chemical Containers, Inc., Cubis AG, ProMinent GmbH, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The vertical tanks segment dominated the market by accounting for the largest share of the European market in 2025 and is expected to maintain its dominant market share throughout the forecast period as farmers continue to prioritize space optimization and operational efficiency. The limited land availability in intensive agricultural regions where maximizing storage capacity within a minimal footprint is critical for operational viability is further aiding the dominance of this segment in the European market. According to Eurostat, the average farm size in Western Europe necessitates compact infrastructure solutions that do not encroach on arable land. Vertical tanks utilize gravity for efficient dispensing and mixing, reducing the need for complex pumping systems and lowering energy consumption during application processes. As per data from agricultural societies, vertical storage units occupy significantly less ground area compared to horizontal equivalents while offering identical volume capacities. This spatial advantage allows farmers to install secondary containment bunds more easily, ensuring compliance with environmental regulations regarding spill prevention. The cylindrical design of vertical tanks provides uniform stress distribution, enhancing durability against internal pressure fluctuations caused by temperature changes. Manufacturers have optimized vertical tank designs with reinforced bases and anti-vortex baffles that prevent sediment accumulation and ensure complete discharge of viscous agrochemicals. The ease of installation and lower foundation requirements further reduce initial capital expenditure, making vertical tanks the preferred choice for both smallholders and large commercial operations. Their modular nature facilitates scalability, allowing farmers to add additional units as production expands without significant site redesign. This combination of spatial efficiency, regulatory compliance, and operational simplicity solidifies the dominance of vertical tanks in the European market.

On the other end, the conical tanks segment is estimated to register a CAGR of 8.4% over the forecast period in the European market owing to the growing need for high-precision chemical management in professional farming and the increasing adoption of precision agriculture techniques that require precise mixing and complete drainage of specialized chemical formulations. The conical bottom design ensures zero dead space, allowing for total evacuation of liquids, which is essential when handling expensive or hazardous agrochemicals that cannot be left to stagnate. According to agricultural research, incomplete drainage in traditional tanks can lead to residue buildup, causing cross-contamination between different chemical batches and reducing application efficacy. Conical tanks facilitate easy cleaning and maintenance, minimizing downtime during seasonal transitions when farmers switch between herbicides, fungicides, and fertilizers. Industry standards highlight that proper tank hygiene is critical for preventing resistance development in pests and weeds, driving demand for designs that support thorough sanitation. Additionally, conical tanks are increasingly integrated with automated mixing systems that rely on consistent flow dynamics to achieve homogeneous blends of adjuvants and active ingredients. The use of complex tank mixtures has increased in recent years, requiring storage solutions that prevent separation and settling. The ability to handle high-viscosity fluids without clogging makes conical tanks ideal for modern biological pesticides and organic inputs that are gaining popularity under the Farm to Fork Strategy. This technical superiority in mixing and drainage efficiency positions conical tanks as the preferred solution for advanced agricultural operations seeking to optimize input usage and minimize waste.

By Application Insights

The chemical storage segment occupied the dominant share of the European market in 2025 due to the critical nature of pesticide management and associated regulatory risks, the stringent regulatory requirements for the safe handling of pesticides and herbicides, and the European Union’s rigorous enforcement of the Sustainable Use of Pesticides Directive, which mandates secure containment to prevent environmental contamination and human exposure. According to the European Environment Agency, improper storage of agricultural chemicals contributes significantly to groundwater pollution, necessitating robust containment. Farmers must invest in certified chemical storage tanks that offer superior resistance to corrosive substances and feature leak-proof seals to comply with these strict standards. As per data from chemical safety agencies, the volume of hazardous agrochemicals stored on farms requires specialized infrastructure that prevents vapor emission and accidental spills during transfer operations. The complexity of modern pesticide formulations containing multiple active ingredients necessitates tanks made from high-grade polyethylene or stainless steel that do not react with acidic or alkaline components. Regulatory audits have become more frequent, with national authorities imposing heavy fines for non-compliant storage practices, driving widespread replacement of outdated containers. The need for segregated storage areas to prevent incompatible chemical interactions further increases the number of tanks required per farm. This regulatory pressure, combined with the high value of crop protection products, ensures that chemical storage remains the largest application segment as farmers prioritize safety and compliance to protect their livelihoods and avoid legal liabilities.

On the other end, the fertilizer storage segment is expected to exhibit a CAGR of 7.9% over the forecast period in the European market owing to the ongoing shift toward liquid nutrient applications and the need for precision farming equipment, the shift toward liquid fertilizer applications and precision nutrient management. The transition from granular to liquid fertilizers is accelerating due to their ease of application through irrigation systems and foliar sprays, which improve nutrient uptake efficiency. According to fertilizer industry data, liquid fertilizer usage in Europe has seen a steady increase as farmers seek to reduce labor costs and enhance yield uniformity. Liquid nitrogen and phosphate solutions require specialized storage tanks that prevent crystallization and maintain consistent concentration levels throughout the storage period. As per agricultural statistics, rising costs of synthetic fertilizers have prompted farmers to adopt precise dosing technologies that minimize waste and optimize input costs. Storage tanks equipped with agitation systems and temperature control features are essential for maintaining the quality of liquid fertilizers, particularly during winter months when freezing risks are high. Nutrient management plans from the European Commission encourage the use of efficient application methods that reduce runoff and leaching into water bodies. Liquid fertilizers allow for better integration with variable-rate technology, enabling farmers to apply nutrients based on real-time soil data. This technological synergy drives demand for advanced storage solutions that support accurate metering and seamless integration with smart farming equipment. The economic imperative to maximize nutrient use efficiency while complying with environmental regulations positions fertilizer storage as the most dynamic growth segment in the market.

COUNTRY LEVEL ANALYSIS

Germany Agrochemical Tank Market Analysis

Germany dominated the market by holding the largest share of the European market in 2025 due to its advanced agricultural technology adoption and strict environmental compliance standards. The country’s robust manufacturing sector supports the production of high-quality storage solutions that meet rigorous safety regulations. According to national statistical offices, the agricultural sector utilizes extensive liquid fertilizer systems, particularly for maize and wheat cultivation, driving demand for durable chemical storage tanks. The German government’s Fertilizer Ordinance imposes strict limits on nutrient application rates and storage capacities, requiring farms to maintain detailed records and certified containment structures. As per industry association data, a majority of large-scale farms have upgraded their storage infrastructure in the past five years to comply with updated water protection laws. The prevalence of precision farming technologies in Germany necessitates tanks compatible with digital monitoring systems that track inventory and usage in real-time. Local manufacturers focus on innovation, developing tanks with enhanced UV stabilization and corrosion resistance to withstand diverse climatic conditions. The strong cooperative structure among German farmers facilitates collective investment in shared storage facilities, reducing individual financial burdens. Government subsidies under the Common Agricultural Policy support infrastructure improvements that enhance environmental sustainability. The emphasis on reducing nitrogen surplus in groundwater drives continued investment in sealed and leak-proof storage systems. Germany’s commitment to technological excellence and regulatory adherence ensures its sustained leadership in the regional agrochemical tank market.

France Agrochemical Tank Market Analysis

France maintains a significant share in the Europe agrochemical tank market, driven by its extensive agricultural landscape and diverse crop production, including cereals, vineyards, and orchards. The country faces unique challenges related to pesticide reduction targets under the Ecophyto Plan, which mandates a decrease in chemical usage. According to the French Ministry of Agriculture, this regulatory pressure accelerates the adoption of precise application equipment, requiring reliable storage tanks that prevent contamination and ensure accurate dosing. Vineyard owners in regions like Bordeaux and Champagne invest heavily in specialized tanks for copper and sulfur-based treatments, which are permitted under organic certification standards. As per agricultural statistical services, the area under organic farming has expanded, increasing demand for dedicated storage solutions that prevent cross-contamination with conventional chemicals. The fragmentation of farm sizes in France presents challenges, but cooperative purchasing models help smaller producers access high-quality storage infrastructure. Regional authorities enforce strict zoning laws for chemical storage, particularly in protected water catchment areas, limiting installation options and driving demand for compact vertical tanks. French manufacturers emphasize aesthetic integration of storage units in scenic rural landscapes, particularly in tourism-dependent regions. The ongoing modernization of agricultural practices and strong policy support for sustainable input management sustain steady demand for advanced agrochemical tanks across the country.

Spain Agrochemical Tank Market Analysis

Spain occupies a vital position in the Europe agrochemical tank market as the largest producer of fruits and vegetables in the European Union, requiring intensive crop protection measures. The Mediterranean climate exposes Spanish agriculture to high temperatures and pest pressures, necessitating robust storage solutions for frequent pesticide applications. According to the Spanish Ministry of Agriculture, the horticultural sector accounts for a significant portion of total agricultural output, driving substantial demand for chemical and fertilizer storage tanks. The expansion of drip irrigation systems in regions like Andalusia and Murcia has increased the use of liquid fertilizers, requiring specialized tanks with filtration and agitation capabilities. Spain faces significant water scarcity issues, prompting the integration of fertigation systems that combine irrigation and fertilization, thereby increasing the need for precise storage and mixing infrastructure. Hail protection and shade netting often accompany storage facilities in intensive orchards, creating integrated protective zones. The export-oriented nature of Spanish agriculture requires strict adherence to international residue limits, driving investment in accurate dosing systems supported by reliable storage tanks. Local manufacturers have developed heat-resistant tank materials suitable for extreme summer conditions, preventing material degradation. Government initiatives under the National Strategic Plan for the Common Agricultural Policy provide funding for modernizing irrigation and storage infrastructure. The continuous growth of high-value crop production ensures sustained demand for durable and efficient agrochemical storage solutions in Spain.

Italy Agrochemical Tank Market Analysis

Italy plays a crucial role in the Europe agrochemical tank market, characterized by its diverse agricultural sectors, including viticulture, olive cultivation, and intensive greenhouse operations. The country’s commitment to high-quality agricultural output drives demand for storage solutions that ensure chemical stability and prevent environmental damage. According to national agricultural institutes, there is an increasing trend toward precision farming in high-value sectors, necessitating advanced tank systems that integrate with digital monitoring and automation. Italian farmers are increasingly prioritizing infrastructure that supports sustainable viticulture and olive oil production, where residue management is essential for export certification. As per Eurostat data, Italy maintains a large number of agricultural holdings, with many smaller farms forming cooperatives to share the costs of modern, compliant storage infrastructure. Government funding for rural development programs supports the installation of smart irrigation and fertigation systems, boosting the market for tanks compatible with precision nutrient delivery. Regional authorities in Italy enforce strict compliance with EU-wide safety and environmental standards, particularly regarding the protection of water sources in key agricultural regions. Local manufacturers are recognized for their expertise in producing specialized tank designs tailored for small-scale, high-density farm environments where space is at a premium. The ongoing push for digitalization in agriculture and the need to meet international phytosanitary standards for exports ensure a positive growth trajectory for the agrochemical tank market in Italy.

COMPETITIVE LANDSCAPE

The competition in the Europe agrochemical tank market is characterized by a mix of established manufacturers and specialized regional players striving to differentiate through quality and compliance. Leading companies compete primarily on product durability, regulatory adherence, and technological integration rather than price alone. The market features moderate consolidation with key players expanding their geographic footprint through strategic partnerships and facility upgrades. Innovation drives competitive advantage as firms introduce smart tank systems integrated with digital monitoring tools for precision agriculture. Regulatory compliance serves as a significant barrier to entry, favoring established entities with resources to meet stringent European Union directives on chemical storage and environmental protection. Regional players maintain strong positions by offering localized solutions tailored to specific climatic conditions and crop requirements. The threat of substitute products remains low due to the unique safety requirements for hazardous material storage. Competitive intensity is heightened by the growing demand for sustainable materials, prompting continuous investment in recyclable plastics. Customer loyalty is increasingly influenced by after-sales support and technical assistance, ensuring optimal product performance and regulatory adherence throughout the product lifecycle.

KEY MARKET PLAYERS

The leading companies operating in the Europe agrochemical tank market include:

- KBK Industries, LLC

- Snyder Industries, LLC

- F. Manufacturing, Inc.

- Denios GmbH

- Chemical Containers, Inc

- Cubis AG

- ProMinent GmbH

TOP PLAYERS IN THE MARKET

- Snyder Industries maintains a strong presence in the European agrochemical tank market by delivering high-quality polyethylene storage solutions designed for durability and chemical resistance. The company specializes in vertical and conical tanks that meet stringent environmental safety standards required by European regulations. Snyder recently expanded its manufacturing capabilities in Germany to reduce lead times and improve supply chain reliability for local customers. Their investment in advanced rotational molding technology ensures consistent wall thickness and superior structural integrity for large-capacity tanks. The firm actively collaborates with agricultural engineers to develop customized containment systems that integrate seamlessly with precision farming equipment. Snyder emphasizes sustainability by offering recyclable materials and promoting proper end-of-life disposal practices for used tanks. Recent product launches include smart tank options equipped with sensor compatibility for real time monitoring of liquid levels. This focus on innovation and regulatory compliance strengthens their reputation as a trusted partner for European farmers seeking reliable and safe storage infrastructure for agrochemicals.

- Denios GmbH is a leading provider of hazardous substance storage solutions in Europe with a significant focus on agrochemical containment systems. The company offers a comprehensive range of bunded tanks and modular storage facilities that ensure full compliance with European environmental directives. Denios recently enhanced its digital service portfolio by introducing online configuration tools that allow farmers to design custom storage setups tailored to specific site requirements. Their commitment to safety is evident in the rigorous testing protocols applied to all products, ensuring leak-proof performance under extreme conditions. The firm has strengthened its distribution network across Central and Eastern Europe to better serve emerging markets with growing agricultural sectors. Denios also provides extensive training programs for users on proper handling and maintenance of chemical storage units. Recent innovations include eco-friendly materials that reduce the carbon footprint of production while maintaining high durability standards. These strategic initiatives reinforce Denios' position as a key contributor to safe and sustainable agrochemical management in the European agricultural landscape.

- Cubis AG operates as a prominent manufacturer of industrial storage tanks serving the European agricultural sector with robust and versatile containment solutions. The company focuses on producing large-capacity vertical tanks suitable for bulk storage of liquid fertilizers and pesticides on commercial farms. Cubis recently upgraded its production facilities in Switzerland to incorporate automated quality control systems that enhance product consistency and reduce manufacturing defects. Their engineering team develops specialized coatings that protect tank interiors from corrosive agrochemical formulations, extending product lifespan significantly. The firm has established strategic partnerships with local agricultural cooperatives to offer bundled services including installation and regular maintenance checks. Cubis emphasizes customer support by providing detailed technical documentation and compliance guidance for complex regulatory environments. Recent expansions into Southern European markets reflect their strategy to capture growth in regions with intensive horticultural activities. By prioritizing engineering excellence and customer-centric services, Cubis AG continues to strengthen its market position and contribute to the modernization of agrochemical storage infrastructure across Europe.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe agrochemical tank market employ several strategic approaches to maintain competitiveness and drive growth. Product innovation remains central as companies develop advanced materials with enhanced durability and environmental compatibility. Manufacturers invest heavily in research and development to create recyclable and corrosion-resistant tank solutions that comply with stringent European Union regulations. Strategic partnerships with agricultural technology firms facilitate the integration of smart sensors and digital monitoring capabilities into storage systems. Expansion of distribution networks through collaborations with local dealers and cooperatives ensures broader market reach, particularly in emerging regions. Companies also focus on customer education and technical support services to improve installation quality and regulatory compliance. Sustainability initiatives, including take-back schemes and eco-friendly manufacturing processes, strengthen brand reputation among environmentally conscious consumers. Diversification of product portfolios to address specific crop needs and regional climatic conditions allows firms to capture niche market segments effectively. Customization services enable manufacturers to tailor storage solutions to unique farm layouts and operational requirements, enhancing customer loyalty.

MARKET SEGMENTATION

This Europe agrochemical tank market research report is segmented and sub-segmented into the following categories.

By Type

- Conical

- Horizontal

- Vertical

By Application

- Water Storage

- Fertilizer Storage

- Chemical Storage

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe agrochemical tank market?

The Europe agrochemical tank market includes storage solutions for fertilizers, pesticides, and crop protection chemicals used in agricultural operations.

How does the Europe agrochemical tank market work?

The Europe agrochemical tank market supports safe containment, transport, and dispensing of agrochemicals across farms and supply chains.

What drives growth in the Europe agrochemical tank market?

The Europe agrochemical tank market grows from strict safety rules, modern farming needs, and rising demand for secure chemical storage.

Which tank types are common in the Europe agrochemical tank market?

The Europe agrochemical tank market commonly uses polyethylene, stainless steel, and bunded tanks for different chemical storage needs.

Why are bunded tanks important in the Europe agrochemical tank market?

Bunded tanks are important in the Europe agrochemical tank market because they help prevent spills and improve environmental safety.

What role does corrosion resistance play in the Europe agrochemical tank market?

Corrosion resistance is vital in the Europe agrochemical tank market because tanks must safely store harsh fertilizers and pesticides.

How do regulations affect the Europe agrochemical tank market?

The Europe agrochemical tank market is strongly influenced by chemical safety, storage, and environmental compliance requirements.

What end users use the Europe agrochemical tank market?

Farmers, distributors, agrochemical suppliers, and agricultural cooperatives use the Europe agrochemical tank market for storage and handling.

What applications lead the Europe agrochemical tank market?

The Europe agrochemical tank market is led by fertilizer storage, pesticide storage, and crop protection chemical handling.

How do polyethylene tanks support the Europe agrochemical tank market?

Polyethylene tanks support the Europe agrochemical tank market with lightweight, durable, and cost-effective chemical storage.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com