- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

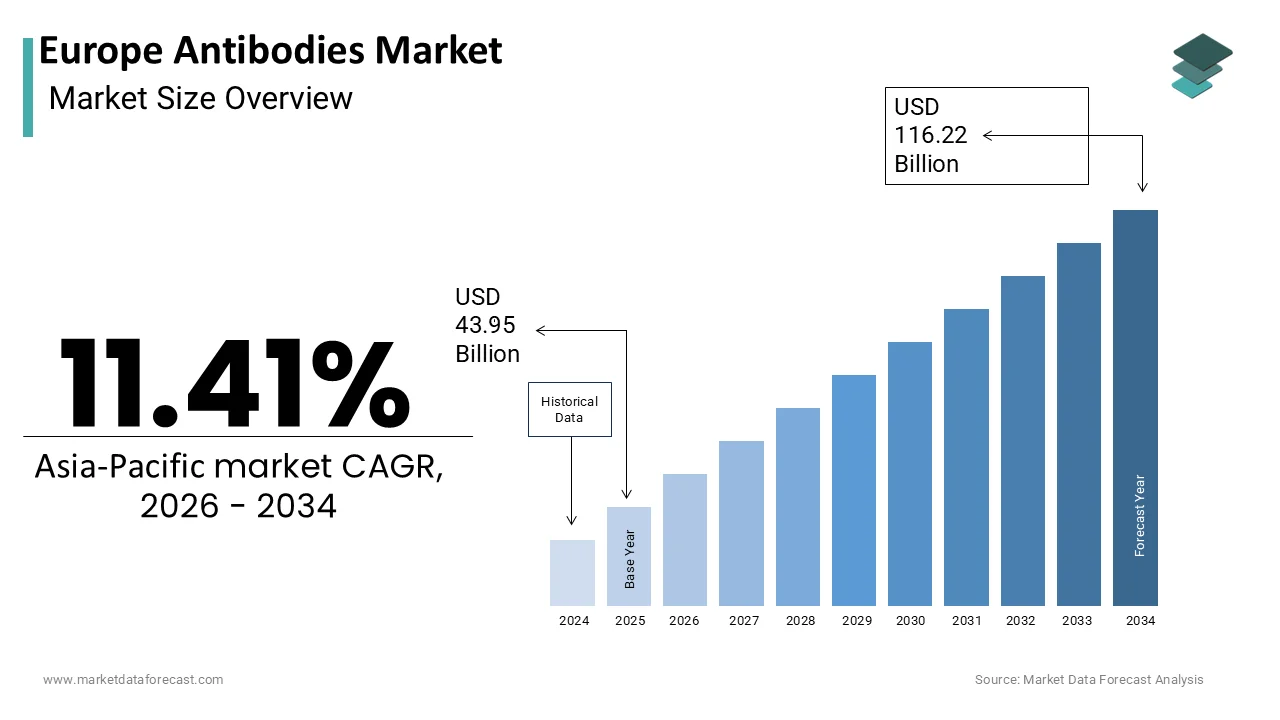

Market Size, 2025

$43.95 BnMarket Estimate, 2026

$48.97 BnMarket Forecast, 2034

$116.22 BnCAGR, 2026–2034

11.41%Europe Antibodies Market Summary

Market Size & Growth

- The Europe Antibodies Market was valued at USD 43.95 billion in 2025.

- Expected to reach USD 48.97 billion in 2026 and USD 116.22 billion by 2034, growing at a CAGR of 11.41% from 2026 to 2034.

- Germany held the largest regional share at 20.9% in 2024, while the United Kingdom ranked second.

Key Market Segments

- By product type: Monoclonal antibodies led the market; antibody drug conjugates are fastest-growing at a CAGR of 15.5%.

- By indication: Cancer held the largest share in 2024; CNS disorders are fastest-growing at a CAGR of 13.3%.

- By end user: Hospitals/clinics held the largest share in 2025; research institutes are the fastest-expanding segment.

- By application: Medical use led in 2024; immunohistochemistry is the fastest-expanding application.

Key Drivers

- Rising prevalence of cancer and autoimmune disorders, with 4.47 million new cancer cases recorded in Europe in 2022 (International Agency for Research on Cancer).

- Expansion of antibody-based diagnostics, with immunoassays comprising a major share of Europe's 1.5 billion annual diagnostic tests.

- Advancement of bispecific antibodies and antibody drug conjugates, with over 25 bispecific antibodies and 16 antibody drug conjugates in late-stage EU trials in 2024.

Key Players

Abbott Diagnostics, Novartis AG, Pfizer Inc., Thermo Fisher Scientific Inc., Eli Lilly and Company, A.G. Scientific Inc., Bristol-Myers Squibb, F. Hoffmann-La Roche Ltd, AbbVie Inc.

Europe Antibodies Market Size

The Europe Antibodies Market is projected to grow from USD 43.95 billion in 2025 to USD 48.97 billion in 2026 and reach USD 116.22 billion by 2034, registering a CAGR of 11.41% during the forecast period from 2026 to 2034.

Antibodies are used across therapeutic, diagnostic,c and research domains. These biomolecules serve as critical tools in targeted cancer therapy, autoimmune disease management,t infectious disease detection, and basic life science research. In Europe, their use is governed by stringent regulatory frameworks from the European Medicines Agency for therapeutics and the In Vitro Diagnostic Regulation for diagnostic assays. According to the European Commission, more than 250 antibody-based medicinal products were under clinical investigation in the European Union in 2024, with oncology and immunology representing the dominant therapeutic areas. As per the European Society for Medical Oncology, over 60% of new cancer drug approvals in Europe since 2020 have included monoclonal antibodies such as trastuzumab, pembrolizumab, and daratumumab. Furthermore, the European Research Council allocated more than €120 million in 2023 to antibody engineering projects under its frontier research grants. These scientific, regulatory, and funding dynamics position antibodies as indispensable instruments in Europe’s precision medicine and biomedical innovation ecosystem.

MARKET DRIVERS

Rising Prevalence of Oncologic and Autoimmune Disorders Drives Therapeutic Demand

The escalating burden of cancer and immune‑mediated diseases across Europe is driving the growth of the European antibodies market. According to the International Agency for Research on Cancer, Europe recorded approximately 4.47 million new cancer cases in 2022, with monoclonal antibodies forming the backbone of treatment for breast, lung, hematologic, and gastrointestinal malignancies. As per the European Alliance of Associations for Rheumatology, rheumatic and musculoskeletal diseases affect nearly 20 million Europeans, which represents a major share of the chronic illness burden. Biologics such as adalimumab and ustekinumab are widely used in autoimmune conditions, and their uptake continues to expand. According to the European Medicines Agency, biologics accounted for the majority of new approvals in 2024, with antibody‑based drugs dominating therapeutic pipelines. Biosimilar expansion is also notable, with over 80 biosimilars approved in Europe since 2006, generating more than €50 billion in cumulative savings. This convergence of high disease incidence, regulatory validation, and reimbursement support ensures robust and expanding demand for therapeutic antibodies across the region, positioning them as indispensable tools in modern healthcare.

Expansion of Antibody‑Based Diagnostics in Infectious Disease and Precision Medicine Fuels Utilization

Antibodies are increasingly integral to advanced diagnostic platforms, enabling rapid detection of pathogens and stratification of patient subpopulations for targeted therapy, which is further contributing to the European antibodies market growth. According to the European Centre for Disease Prevention and Control, antibody‑based assays were central to SARS‑CoV‑2 serological testing, with recombinant monoclonal antibodies widely used for spike and nucleocapsid detection. As per the European Federation of Clinical Chemistry and Laboratory Medicine, multiplex immunoassays using antibody arrays now routinely screen for cardiac biomarkers, tumor antigens, and autoimmune markers in tertiary hospitals across Western Europe. EMA mandates companion diagnostic validation for antibody therapeutics such as trastuzumab, requiring HER2 status confirmation via immunohistochemistry. The In Vitro Diagnostic Regulation, fully enforced in 2022, has acceleratedthe adoption of CE‑marked antibody kits with standardized performance claims. According to the European Diagnostics Manufacturers Association, immunoassays represent a major share of Europe’s 1.5 billion annual diagnostic tests, underscoring their foundational role in precision medicine. With this scale of utilization, antibodies remain central to Europe’s diagnostic infrastructure, pandemic preparedness, and the evolution of personalized healthcare.

MARKET RESTRAINTS

Stringent Regulatory Pathways Increase Development Timelines and Costs

The European Antibodies Market faces significant barriers due to the rigorous and multi‑layered approval processes required for both therapeutic and diagnostic antibodies. According to the European Medicines Agency, the average time to market for a novel monoclonal antibody in Europe exceeds 8–10 years, with clinical development alone costing more than €800 million. As per the European Commission’s 2025regulatory audit, nearly one‑third of antibody marketing authorization applications faced major objections related to manufacturing consistency or non‑clinical toxicity data. The IVDR mandates extensive clinical performance studies and notified body audits for diagnostic antibodies, delaying many legacy immunoassays past the May 2022 deadline. These prolonged timelines disproportionately affect small biotechs with limited regulatory expertise, often forcing them to deprioritize or abandon promising candidates. Consequently, innovation pipelines remain constrained despite strong scientific merit. Until regulatory harmonization and adaptive pathways are fully implemented, the European market will continue to be shaped by high entry barriers, delayed patient access, and uneven innovation outcomes.

Intellectual Property Disputes and Patent Cliffs Restrict Market Entry and Innovation

The European Antibodies Market is heavily influenced by complex patent landscapes and frequent litigation that delay biosimilar and next‑generation antibody launches, which further hinders the regional market growth. According to the European Patent Office, more than 12,000 active patents related to antibody sequences, formulations, and therapeutic uses were in force across EU member states in 2024. As per the European Generic Medicines Association, originator companies routinely file divisional patents covering minor modifications extending market exclusivity beyond the standard 20‑year term. For example, adalimumab biosimilars faced staggered entry across EU markets despite EMA approval in 2016, with broader uptake only after 2023. Conversely, biosimilar competition has sharply reduced originator revenues; rituximab biosimilars cut prices by more than 50% in Germany and France within two years of launch.

MARKET OPPORTUNITIES

Advancement of Bispecific and Antibody Drug Conjugate Platforms Unlocks New Therapeutic Frontiers

The development of next‑generation antibody formats such as bi-specifics and antibody drug conjugates presents a high‑value opportunity for the European antibodies market. According to the European Medicines Agency, more than 25 bispecific antibodies and 16 antibody drug conjugates were in late‑stage trials in Europe in 2024, targeting hematologic malignancies, solid tumors, and neurological disorders. As per the European Society for Medical Oncology, the approval of mosunetuzumab for relapsed follicular lymphoma and trastuzumab deruxtecan for HER2‑low breast cancer has redefined treatment paradigms and expanded addressable patient populations. European biotechs such as Merus and ADC Therapeutics have pioneered formats like Biclonics and pyrrolobenzodiazepine conjugates with strong clinical data. Furthermore, the European Commission’s Innovative Medicines Initiative allocated €45 million in 2025to the ANTICANCER consortium to scale manufacturing of complex antibody constructs. These engineered platforms offer superior efficacy over conventional monoclonals and command premium pricing, creating a strategic growth vector for innovative firms.

Integration of Antibodies into Cell and Gene Therapy Manufacturing Enhances Process Control

Antibodies are increasingly utilized as critical reagents in the production and quality control of advanced therapy medicinal products, including CAR‑T cells and gene therapies, which is another notable opportunity for the European antibodies market. According to the European Medicines Agency, more than 90% of CAR‑T cell manufacturing protocols in Europe use CD3, CD4, and CD8 monoclonal antibodies for T‑cell selection and purity verification. As per the European Society for Gene and Cell Therapy, flow cytometry panels with validated antibody clones are mandatory for release testing of cell therapy products under EU GMP Annex 1. Additionally, antibodies against residual host cell proteins are employed to ensure purity in viral vector production for gene therapies. The European Commission’s Advanced Therapies Action Plan has funded over €30 million since 2022 to standardize antibody‑based analytics for cell and gene products. With more than 150 advanced therapy clinical trials active in Europe in 2024, according to ClinicalTrials.eu, demand for high‑quality research and GMP‑grade antibodies is creating a stable and high‑margin niche within the broader antibodies market.

MARKET CHALLENGES

Shortage of High-Quality GMP-Grade Antibodies for Clinical Applications Limits Therapeutic Scale‑Up

Despite robust discovery pipelines, the European Antibodies Market faces a critical bottleneck in the availability of clinical‑grade antibodies manufactured under Good Manufacturing Practice standards. According to the European Medicines Agency, more than 40% of cell and gene therapy developers in Europe reported delays in clinical trial initiation due to a lack of GMP‑compliant antibodies for cell sorting and release testing. As per a 2025survey by the European Biopharmaceutical Enterprises, only 12 contract manufacturers in the EU offer GMP‑grade monoclonal antibodies with full traceability documentation, viral clearance validation, and endotoxin control. Most research‑grade antibodies lack the batch‑to‑batch consistency required for human use. This gap forces developers to either invest in in‑house production or source from limited US‑based providers, incurring regulatory and logistical hurdles. Until dedicated European GMP antibody manufacturing capacity expands, the scalability of advanced therapies and next‑generation biologics will remain constrained by reagent availability.

High Production Complexity and Cost of Recombinant Antibodies Impede Broad Research Access

The technical and financial barriers associated with recombinant antibody production limit accessibility for academic and small biotech researchers across Europe, which is further challenging the growth of the European market. According to the European Molecular Biology Laboratory, the average cost to produce one milligram of a recombinant monoclonal antibody using mammalian cell culture exceeds €2,500, excluding purification and validation. As per the European Research Council, only 35% of publicly funded life science projects in Southern and Eastern Europe include recombinant antibodies in their budgets due to cost constraints. While phage display and yeast platforms offer alternatives, they require specialized expertise not widely available outside major research hubs in Germany, the United Kingdom, and Switzerland. Consequently, many labs rely on polyclonal or hybridoma‑derived antibodies, which suffer from batch variability and ethical concerns. Although initiatives such as the EU‑funded Recombinant Antibody Network aim to standardize open‑source production, the infrastructure gap persists. Until scalable and affordable recombinant platforms become broadly accessible, the full potential of reproducible and ethically sound antibody research will remain unrealized across the European scientific community.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Indication, End User, Application, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

| Market Leaders Profiled | Abbott Diagnostics, Novartis AG, Pfizer Inc., Thermo Fisher Scientific Inc., Eli Lilly and Company, A.G. Scientific, Inc., Bristol-Myers Squibb, F. Hoffmann-La Roche Ltd, and AbbVie Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The monoclonal antibodies segment accounted for the largest share of the European antibodies market in 2025 due to their high specificity, reproducibility, and extensive use in both therapeutics and advanced diagnostics. According to the European Medicines Agency, over 85% of antibody‑based medicinal products approved in the European Union between 2020 and 2025were monoclonal antibodies targeting cancer, autoimmune, and infectious diseases. As per the European Society for Medical Oncology, monoclonal antibodies such as pembrolizumab, trastuzumab, and rituximab featured in more than 70% of first‑line oncology regimens in 2024. Their dominance is further reinforced in diagnostics, where they serve as core reagents in ELISA, flow cytometry, and immunohistochemistry due to minimal cross‑reactivity and batch consistency. The European Commission’s Innovative Medicines Initiative has funded over fifty public‑private partnerships since 2020 to optimize monoclonal antibody platforms for emerging targets. With biosimilars expanding access and next‑generation formats like Fc‑engineered antibodies entering late‑stage trials, monoclonal antibodies remain the cornerstone of Europe’s precision medicine strategy.

The antibody drug conjugates segment is expected to expand at a CAGR of 15.5% over the forecast period. The growth of the antibody drug conjugates segment in this regional market is likely to be driven by their ability to deliver potent cytotoxic agents directly to tumor cells while sparing healthy tissue, thereby improving therapeutic index and reducing systemic toxicity. As per the European Society for Medical Oncology, the approval of trastuzumab deruxtecan for HER2‑low breast cancer and datopotamab deruxtecan for non‑small cell lung cancer has redefined treatment standards and expanded addressable patient populations across Europe. Over 35 antibody drug conjugates were in Phase II or III trials in the EU in 2024, targeting solid and hematologic malignancies. Furthermore, the European Commission’s Horizon Europe programme allocated fifty‑two million euros in 2025to the ADC Europe consortium to scale manufacturing and analytical validation. With enhanced linker stability and payload diversity,y this segment represents the most dynamic frontier in targeted cancer therapy.

By Indication Insights

The cancer segment was the most dominant therapeutic indication in thEuropeanpe antibodies market and held the leading share of the regional market in 2024. The dominance of the cancer segment in this regional market is driven by high disease burden, expanding biomarker‑guided treatment protocols, and robust reimbursement for biologic therapies. According to the International Agency for Research on Cancer, over three point nine million new cancer cases were diagnosed in Europe in 2023, with monoclonal antibodies integrated into first‑line regimens for breast, colorectal, hematologic, and lung malignancies. As per the European Medicines Agency, more than 0% of oncology drug approvals since 2020 have been antibody‑based, including immune checkpoint inhibitors and bispecifics. National health systems in Germany, France, and the United Kingdom routinely reimburse high‑cost antibody therapies due to proven survival benefits,s with the UK’s NICE recommending pembrolizumab for early‑stage triple‑negative breast cancer in 2024. Additionally, the European Reference Networks for rare cancers mandate HER2, PD‑L1, and CD20 testing to guide antibody selection. This clinical, regulatory, and economic alignment ensures oncology remains the primary driver of therapeutic antibody consumption.

The central nervous system disorders segment is fastest growing indication segment in thEuropeanpe antibodies market and is anticipated to witness a CAGR of 13.3% over the forecast period, owing to the breakthrough approvals for neurodegenerative and neuroinflammatory conditions previously deemed untreatable. As per the European Medicines Agency, lecanemab and donanemab received conditional marketing authorization in 2025for early Alzheimer’s disease based on amyloid plaque reduction demonstrated via antibody‑based PET imaging and cerebrospinal fluid assays. Similarly, ofatumumab was approved for relapsing multiple sclerosis with subcutaneous administration,n enhancing patient compliance. Over 25 monoclonal antibodies targeting alpha‑synuclein, tau, and neuroinflammatory cytokines are in Phase II trials across EU academic centers. The EU’s Joint Programme on Neurodegenerative Disease Research has allocated over three hundred million euros since 2022 to support antibody development. With rising elderly populations and unmet neurological needs, ds this segment is transitioning from symptomatic care to disease‑modifying intervention.

By End User Insights

The hospitals and clinics segment commands the highest share of the European market in 2025by end-user. The leading position commands the majority share of the European Antibodies Market as the primary sites for therapeutic administration, diagnostic testing, and companion biomarker evaluation. According to the European Commission, over ninety percent of monoclonal antibody infusions for cancer and autoimmune diseases are delivered in hospital day units or specialized outpatient clinics. As per the European Society for Medical Oncology, all EU tertiary cancer centers now maintain on‑site immunohistochemistry and flow cytometry labs using validated antibody panels for treatment selection. Hospitals also serve as key trial sites with over 75% of Phase III antibody trials in Europe conducted in academic medical centers. Reimbursement systems in Germany, France, and the Netherlands directly link antibody therapy to diagnostic confirmation, that require hospitals to stock both therapeutic and diagnostic antibodies. This integrated care model ensures that hospitals remain the central hub for antibody consumption across therapeutic and diagnostic applications.

The research institutes segment is the fastest-expanding end-user segment in the European antibodies market and is anticipated to register a promising CAGR during the forecast period, owing to the increased public and private funding for basic and translational immunology, neuroscience, and oncology research. As per the Horizon Europe programme, over one hundred and eighty million euros were allocated in 2025to antibody engineering projects,s including bispecifics, nanobodies, and blood‑brain barrier penetrating formats. Major research infrastructures like EMBL in Germany and CRUK Cambridge Institute use high‑quality recombinant antibodies for target validation, functional assays, and imaging. The European Molecular Biology Laboratory’s antibody validation initiative has also raised quality standards, rds prompting institutes to shift from polyclonal to recombinant monoclonals. With Europe hosting over four hundred and fifty life science research centers actively studying immune path, ways this segment’s demand for rigorously validated research‑grade antibodies in this segment continues to accelerate.

By Application Insights

The medical segment held the major share of the European antibodies market in 2024. The leading position of the medical segment in this regional market can be credited to the widespread clinical adoption and regulatory endorsement. According to the European Medicines Agency, over two hundred and ten monoclonal antibody therapies were commercially available in the EU in 2025for conditions ranging from rheumatoid arthritis to metastatic melanoma. Simultaneously, the European Diagnostics Manufacturers Association reports that over six hundred million antibody‑based diagnostic tests are performed annually in EU hospitals and labs for infectious diseases, cardiac markers, and cancer antigens. The In Vitro Diagnostic Regulation has further standardized performance claims for these assays, enhancing reliability. With national health systems reimbursing both therapies and companion diagnostics, medical use remains the dominant and most economically significant application for antibodies in Europe.

The immunohistochemistry segment is the fastest-expanding application segment in the European antibodies market and is estimated to witness a healthy CAGR during the forecast period. This growth stems from its critical role in cancer diagnosis, biomarker stratification, and treatment selection across European pathology networks. As per the European Commission’s Cancer Mission, over ninety‑five% of solid tumor diagnoses now require immunohistochemical staining for markers such as PD‑L1, HER2, ER, and Ki67 to guide antibody therapy eligibility. The European Reference Networks for rare cancers have standardized antibody clones and scoring systems across twenty‑four member states, improving diagnostic consistency.

COUNTRY LEVEL ANALYSIS

Germany Antibodies Market Analysis

Germany occupied the leading share of 20.9% of the regional market in 2024. The dominance of Germany in the European market is driven by its dense network of university hospitals, biotech clusters, and strong public funding for antibody research and therapy. As per the German Cancer Society, over 120,000 patients received monoclonal antibody treatments in 2025with full reimbursement under the statutory health insurance system. Germany hosts key players like BioNTech and CureVac, which develop novel antibody formats and collaborate with academic centers on target discovery. The Paul Ehrlich Institute ensures rigorous batch release testing for therapeutic antibodies, while the German Society for Pathology enforces standardized immunohistochemistry protocols nationwide. With Europe’s largest biopharmaceutical workforce and advanced healthcare infrastructure, Germany serves as the continent’s primary hub for antibody innovation and delivery.

United Kingdom Antibodies Market Analysis

The United Kingdom held the second leading share of the European antibodies market in 2024. Despite Brexit, the UK maintains influence through its world‑class academic research, clinical trial infrastructure, and streamlined approval pathways. According to the National Institute for Health and Care Excellence, over 80 antibody‑based therapies received positive reimbursement recommendations between 2020 and 2024, including first‑in‑class bispecifics for lymphoma. The National Health Service performs over 15 million immunohistochemistry tests annually, validated through the UK NEQAS scheme. Research powerhouses like the Francis Crick Institute and Cambridge Antibody Technology pioneered phage display and humanized antibodies. With strong venture funding and a cohesive pathway from discovery to patient access, the UK remains a pivotal center for antibody science and application.

France Antibodies Market Analysis

France is predicted to witness a promising CAGR in the European antibodies market during the forecast period. The country’s strength lies in its integrated oncology networks, robust biotech ecosystem, and early adoption of precision diagnostics. As per the French National Cancer Institute, over 90% of cancer centers use standardized antibody panels for PD‑L1, HER2, and ALK testing to guide therapy selection. France is home to innovators like Ablynx and Ipsen, which develop nanobodies and radioimmunoconjugates now used across Europe. The national health insurance system reimburses high‑cost antibody therapies within three months of EMA approval, ensuring rapid patient access. According to the French government’s Investment for the Future Programme, €800 million was allocated in 2023 to advanced therapy platforms, including antibody‑drug conjugates. This blend of clinical rigor, regulatory agility, and public investment sustains France’s leadership in therapeutic and diagnostic antibody adoption.

Switzerland Antibodies Market Analysis

Switzerland is anticipated to account for a notable share of the European antibodies market over the forecast period. The country’s significance arises not from population size but from its role as a global hub for antibody discovery and manufacturing through companies like Roche and Novartis. As per the Swiss Biotech Association, over 60% of Switzerland’s biopharmaceutical exports are antibody‑based therapeutics shipped to EU markets. Swiss research institutions such as ETH Zurich and the University of Zurich pioneer novel formats, including trispecific antibodies and T‑cell engagers, now in European clinical trials. The nation’s political neutrality and dual recognition from EMA and FDA enable seamless regulatory bridging. As per Swissmedic, fast‑track review pathways allow European developers to use Switzerland as a launchpad for EU submissions. With unparalleled scientific excellence and industrial scale, Switzerland exertsan outsized influence on the European antibody landscape.

Netherlands Antibodies Market Analysis

The Netherlands is expected to exhibit a healthy CAGR in the European antibodies market during the forecast period. The country’s role is defined by its leadership in digital pathology, antibody validation, and academic clinical translation. As per the Netherlands Cancer Institute, over 100,000 immunohistochemistry tests are performed annually using EMA‑validated antibody clones, with results integrated into national cancer registries. The Netherlands hosts the European branch of the Human Protein Atlas, which provides open access to antibody‑based tissue maps used by researchers across Europe. Companies like Genmab—though Danish—operate major R&D hubs in Utrecht, focusing on next‑generation antibody engineering. Additionally, as per Dutch healthcare policy, biomarker testing is mandated before initiating antibody therapy, ensuring high diagnostic utilization. With strong data infrastructure and a culture of open science, the Netherlands serves as a critical node for antibody standardization and clinical implementation.

COMPETITIVE LANDSCAPE

Competition in the European Antibodies Market is characterized by intense innovation rivalry among multinational pharmaceutical giants and agile biotech firms vying for leadership in oncology, immunology,y and neurology. The market features high barriers to entry due to the complexity of antibody discovery,ry extensive clinical validation requirements, and stringent EMA regulatory standards. Large players like Roche, Novartis, nd AstraZeneca dominate through vertically integrated models that combine proprietary therapeuticwith in-house use of diagnostics and manufacturing. Meanwhile, European biotechs such as Genmab and Merus compete through novel formats like bispecifics and Biclonics, often licensing to global partners for commercialization. Competition is further shaped by biosimilar entry,ry which pressures pricing but expands access. As precision medicine becomes standard, the market increasingly rewards companies that deliver not just effective antibodies but also validated biomarkers, seamless diagnostics, and real-world evidence of clinical impact across diverse European healthcare systems.

KEY MARKET PLAYERS

A few noteworthy companies in the europe antibodies market analyzed in this report are

- Abbott Diagnostics

- Novartis AG

- Pfizer Inc.

- Thermo Fisher Scientific Inc.

- Eli Lilly and Company

- A.G. Scientific, Inc.

- Bristol-Myers Squibb

- F. Hoffmann-La Roche Ltd

- AbbVie Inc.

TOP LEADING PLAYERS IN THE MARKET

- Roche is a global leader in therapeutic and diagnostic antibodies with a commanding presence across Europe through its oncology and immunology portfolios. The company pioneered monoclonal antibody therapies such as trastuzumab,b rituximab, and atezolizumab, which remain the standard of care for multiple cancers. Roche integrates its therapeutics with companion diagnostics developed by its subsidiary Roche Diagnostics, using validated antibody assays for HER2 PD L1 and other biomarkers. In 2020,r Roche launched next-generationon bispecific T cell engager for multiple myeloma in the European Union following accelerated EMA approval. This innovation reinforces its strategy of coupling cutting-edge antibody engineering with precision diagnostics to maintain leadership in targeted cancer therapy across European healthcare systems.

- Novartis contributes significantly to the European Antibodies Market through its diversified biologics pipeline and strategic focus on next-generation antibody formats. The company markets ofatumumab for multiple sclerosis and is advancing a portfolio of radioimmunoconjugates and T cell redirecting antibodies for hematologic malignancies. Novartis leverages its Swiss manufacturing infrastructure to supply high-quality antibody therapeutics to European markets with full GMP compliance. In twenty twenty four, Novartis partnered with a German biotech to co-develop a trispecific antibody targeting solid tumors using a novel Fc engineering platform. This collaboration enhances its innovation pipeline while aligning with Europe’s emphasis on advanced therapy medicinal products and precision oncology.

- AstraZeneca plays a pivotal role in the European Antibodies Market through its robust oncology portfolio featuring durvalumab, trastuzumab,b deruxtec,, an and datopotamab deruxtecan. The company has transformed antibody drug conjugates into a cornerstone of its cancer strategy with multiple approvals in breast, esophageal, lung, and gastric cancers across Europe. AstraZeneca strengthens its position by integrreal-world world evidence from European cancer registries to demonstrate long term clinical outcomes. In twenty twenty four, it expanded its antibody manufacturing capacity at its Södertälje facility in Sweden to meet rising EU demand for ADC therapies. This investment ensuresa reliable supply while supporting the European Commission’s goals for therapeutic sovereignty in critical oncology medicines.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the European Antibodies Market pursue next-generation antibody engineering, strategic integration of therapeutics with companion diagnostics, expansion of antibody drug conjugate pipeline,s localized manufacturing to ensure supply resilience, and partnerships with academic and clinical networks to accelerate biomarker validation and trial recruitment. Companies are investing in bispecific, trispecific, and Fc-modified platforms to overcome resistance mechanisms and enhance immune engagement. Regulatory strategy focuses on simultaneous EMA and FDA submissions with robust clinical data packages. Manufacturing investments in Switzerland, Sweden,n and Germany align with EU calls for pharmaceutical sovereignty. Additionally, many firms are eembedding real-worlddata collection into post-marketing studies to support reimbursement and update clinical guidelines across national health systems.

MARKET SEGMENTATION

This research report on the European antibodies market has been segmented and sub-segmented into the following categories.

By Product Type

-

Monoclonal Antibodies

-

Murine

-

Chimeric

-

Humanized

-

Human

-

-

Polyclonal Antibodies

-

Type I

-

Type II

-

Type III

-

Type IV

-

Type V

-

Type VI

-

Type VII

-

Type VIII

-

-

Antibody drug complexes

-

Immunogen Technology

-

Seattle Genetics Technology

-

Immunomedics Technology

-

By Indication

- Cancer

- Autoimmune Diseases

- Infectious Diseases

- Cardiovascular Diseases

- CNS Disorders

- Others (Inflammatory, Microbial Diseases, & Other)

By End User

- Hospitals/Clinics

- Research Institute

- Diagnostics laboratories

By Application

- Medical

- Experimental

- Western blot

- ELISA

- Radioimmune Assays

- Immunofluorescence

- Others (Immunohistochemistry, Immunoprecipitation, & Immunocytochemistry)

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe