Europe Hyperbaric Oxygen Therapy Devices Market Size, Share, Trends & Growth Forecast By Application, Product and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis, From (2026 to 2034)

Europe Hyperbaric Oxygen Therapy Devices Market Report Summary

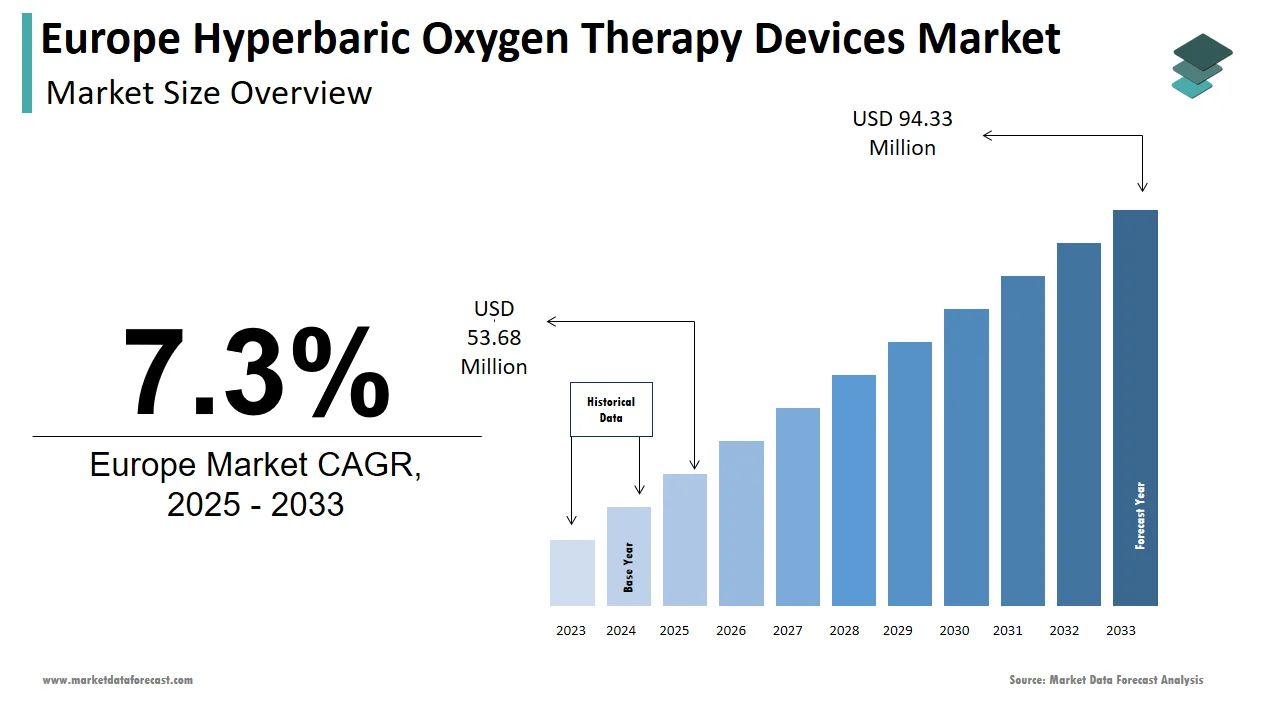

The Europe hyperbaric oxygen therapy (HBOT) devices market was valued at USD 53.68 million in 2025, is estimated to reach USD 57.60 million in 2026, and is projected to reach USD 101.21 million by 2034, growing at a steady CAGR of 7.3% from 2026 to 2034. Market growth is driven by the rising prevalence of chronic wounds, increasing incidence of diabetic foot ulcers, and expanding clinical applications of HBOT in neurology, sports medicine, and post-surgical recovery. Europe’s growing aging population, advancements in monoplace and multiplace chamber technologies, and wider adoption of hospital-based hyperbaric treatment units are further accelerating market demand.

Key Market Trends

- Rising demand for HBOT in chronic wound management, particularly diabetic and pressure ulcers.

- Increasing adoption of monoplace hyperbaric chambers, driven by lower operational complexity and higher patient comfort.

- Expansion of hospital-based hyperbaric facilities across Europe for trauma, infection control, and surgical recovery.

- Growing research interest in HBOT applications for neurological disorders, sports injuries, and long COVID symptoms.

- Shift toward technologically advanced, energy-efficient, and safety-enhanced HBOT systems.

Segmental Insights

- Based on product, the monoplace HBOT devices segment dominated the Europe hyperbaric oxygen therapy devices market in 2024. This segment’s strong position is driven by its cost-effectiveness, simplified installation, higher patient throughput, and increasing preference among hospitals and wound care centers for single-patient treatment setups.

- Based on application, the wound healing segment was the largest in 2024, capturing 64.8% of the market share. The segment’s dominance is attributed to rising cases of chronic wounds, diabetic ulcers, radiation injuries, and post-surgical complications that require HBOT-supported oxygen saturation for accelerated tissue repair.

Regional Insights

The Europe hyperbaric oxygen therapy devices market is experiencing solid growth across leading economies, supported by expanding clinical adoption, growing chronic disease burden, and increasing healthcare investments in specialized wound care technologies.

- Germany outperformed other regions, accounting for 28.6% of the market share in 2024, driven by its advanced healthcare infrastructure, strong insurance coverage, and high adoption of medical device innovations.

- The United Kingdom followed with a 15.2% share in 2024, supported by the increasing use of HBOT in both private healthcare settings and specialized wound care centers.

- France remains an attractive market due to its dense network of hospital-based hyperbaric units and proactive public health policies that support HBOT usage for chronic wound and tissue damage treatments.

Competitive Landscape

The Europe hyperbaric oxygen therapy devices market is shaped by leading global and regional manufacturers offering advanced monoplace and multiplace chamber technologies. Key players are focusing on enhancing safety standards, improving chamber automation, and expanding clinical usability through innovative design improvements. Strategic partnerships with hospitals, research institutions, and wound care centers are strengthening the presence of major manufacturers across Europe’s growing HBOT ecosystem.

Prominent companies operating in the Europe hyperbaric oxygen therapy devices market include Gulf Coast Hyperbarics, Inc., Fink Engineering, ETC Hyperbaric Chambers (Environmental Tectonics Corporation), HAUX-LIFE-SUPPORT, HEARMEC, IHC Hytech B.V. (Royal IHC), Hyperbaric SAC, Sechrist Industries, Inc., OxyHeal International, and SOS Group Europe Ltd.

Europe Hyperbaric Oxygen Therapy Devices Market Size

The hyperbaric oxygen therapy devices market size in Europe was valued at USD 53.68 million in 2025. The European market is estimated to be worth USD 101.21 million by 2034 from USD 57.60 million in 2026, growing at a CAGR of 7.3% from 2026 to 2034.

Hyperbaric oxygen therapy devices are specialized medical systems that administer 100 percent oxygen at pressures greater than atmospheric levels to enhance tissue oxygenation and support healing in specific clinical conditions. In Europe, these devices are primarily deployed in wound care centers, burn units, military hospitals, and specialized neurology clinics for indications including diabetic foot ulcers, carbon monoxide poisoning, and radiation-induced tissue injury. The therapeutic modality operates under strict regulatory oversight with devices classified as Class IIa or IIb medical equipment under the European Union Medical Device Regulation. According to sources associated with the European Wound Management Association, an estimated 1.5 to 2 million people in the EU suffer from chronic wounds at any given time. Diabetic foot ulcers affect approximately 15 percent of individuals diagnosed with diabetes at some point in their lives, with some sources citing a lifetime risk of up to 25% or more. National health systems in countries have integrated hyperbaric oxygen therapy into standard care pathways for non-healing wounds following clinical guidelines issued by the European Committee for Hyperbaric Medicine. As of January 1, 2024, the share of the EU population aged 65 years and over was 21.6%, which is more than one-fifth of the total population, according to Eurostat. This confluence of aging demographics, rising diabetes prevalence, and institutional recognition of hyperbaric efficacy establishes a clinically grounded foundation for device utilization across the region.

MARKET DRIVERS

Rising Prevalence of Chronic Wounds and Diabetic Complications

The escalating burden of diabetes related chronic wounds constitutes a key accelerator for the growth of the Europe hyperbaric oxygen therapy devices market. According to sources, the number of adults in the WHO European Region with diabetes is a significant and growing public health concern. Among these patients, a notable portion of people with diabetes will develop a foot ulcer in their lifetime, and a considerable number of these progress to serious, non-healing wounds. The financial impact of chronic wounds on European healthcare systems is a major economic burden, with diabetic foot ulcers being a leading component of this expense. Clinical evidence supports hyperbaric oxygen therapy as an adjunctive treatment that significantly improves healing rates and reduces amputation risk. These clinical and economic imperatives are compelling hospitals and specialized wound clinics to invest in monoplace and multiplace chambers to meet growing patient demand.

Integration into Military and Emergency Medical Protocols

This therapy has become an institutionalized component of military and emergency medical response systems across several European nations, a development that is driving sustained device deployment and the Europe hyperbaric oxygen therapy market expansion. Countries such as the United Kingdom, France, and Sweden maintain dedicated hyperbaric units within military hospitals like Haslar in the UK and Percy in France, specifically for treating diving accidents, carbon monoxide poisoning, and smoke inhalation from industrial or residential fires. Furthermore, national emergency preparedness frameworks in some countries mandate regional access to hyperbaric capabilities within hours of exposure events. This operational integration ensures continuous public funding for chamber maintenance staff training and protocol updates, which supports both clinical legitimacy and infrastructure investment in the public healthcare and defense sectors.

MARKET RESTRAINTS

Limited Clinical Reimbursement and Restrictive Coverage Policies

Reimbursement constraints are a significant restraint on the Europe hyperbaric oxygen therapy devices market. While countries like Germany, France, and the Netherlands provide coverage for specific indications such as diabetic foot ulcers and radiation necrosis, many EU member states either exclude hyperbaric therapy from national health baskets or impose stringent prior authorization requirements. Moreover, private clinics and smaller hospitals often avoid capital investment in chambers due to uncertain return on investment. Device utilization will remain limited to specialized centers in high-income countries until reimbursement pathways are standardized and expanded to cover emerging indications like traumatic brain injury or refractory osteomyelitis.

High Capital and Operational Costs of Therapy Chambers

The substantial capital outlay and ongoing operational expenses associated with these therapy chambers greatly limit their deployment, especially in public and rural healthcare settings in the region, which further affects the expansion of the Europe hyperbaric oxygen therapy market. Monoplace chambers cost less than multiplace systems, excluding facility modifications for oxygen safety compliance. According to the European Agency for Safety and Health at Work, stringent regulations under Directive 2017 54 require specialized ventilation, fire suppression, and structural reinforcements for chamber rooms, increasing installation costs by 30 to 40 percent. Operational costs further escalate due to mandatory staffing requirements typically involving a physician, nurse, and hyperbaric technician per session, as stipulated. Maintenance contracts and annual recertification add a notable amount yearly. Even in wealthier nations like Spain, regional health authorities prioritize cost per quality-adjusted life year, with hyperbaric therapy often scoring poorly due to limited long-term outcome data. These financial barriers restrict access to urban academic medical centers, thereby excluding rural and underserved populations from potentially beneficial therapy.

MARKET OPPORTUNITIES

Expansion into Neurological and Cognitive Rehabilitation Applications

Emerging clinical evidence supporting hyperbaric oxygen therapy in neurological recovery offers an opportunity for device manufacturers in the region, which drives the growth of the Europe hyperbaric oxygen therapy market. Recent studies indicate that controlled hyperbaric exposure can stimulate neuroplasticity, reduce neuroinflammation, and enhance mitochondrial function in patients with post-stroke deficits, traumatic brain injury, and post-concussion syndrome. The European Academy of Neurology has begun reviewing this data for potential inclusion in future rehabilitation guidelines. Private neurorehabilitation clinics in Switzerland, Sweden, and Austria have already integrated monoplace chambers into multidisciplinary programs. This therapeutic approach has the potential to see adoption beyond traditional wound care settings and into mainstream neurology and psychiatry, especially as health technology assessment bodies reevaluate evidence standards and patient advocacy groups advocate for expanded access.

Growth of Medical Tourism and Cross-Border Healthcare Services

The rise of medical tourism within the European Union is creating new commercial prospects for the expansion of the Europe hyperbaric oxygen therapy market. This growth opens the doors for hyperbaric oxygen therapy centers, particularly in countries with streamlined access and multilingual services. According to research, a large number of patients traveled across EU borders in 2024 specifically for elective or specialized treatments not readily available in their home countries. Some nations have developed hyperbaric wellness and recovery clinics that cater to international clients seeking treatment for sports injuries, chronic fatigue, and post-viral syndromes, including long COVID. These centers often combine therapy with hospitality services and operate outside traditional reimbursement frameworks, enabling flexible pricing and rapid scheduling. The EU facilitates this flow by allowing patients to seek care in another member state and claim partial reimbursement. This market segment offers a promising revenue opportunity for private providers to counteract public sector limitations, as growing public awareness and the accessibility of digital platforms simplify entry. Apart from these, it allows for the expansion of clinical indications through real-world evidence collection.

MARKET CHALLENGES

Lack of Standardized Clinical Practice Guidelines Across Member States

The absence of harmonized clinical protocols for this therapy in the region creates variability in treatment delivery and inhibits the growth of the Europe hyperbaric oxygen therapy market. While the European Committee for Hyperbaric Medicine publishes consensus recommendations, these are non-binding, and national medical societies often develop divergent guidelines or omit hyperbaric therapy entirely. According to a study, only a few EU countries have formal national guidelines that specify pressure duration and session frequency for diabetic foot ulcers. In other treatments, decisions rely on individual physician discretion, leading to inconsistent outcomes and skepticism among payers. This fragmentation complicates multicenter clinical trials as protocol deviations hinder data aggregation and statistical power. Furthermore, regulatory bodies like notified organizations struggle to assess device performance without uniform indication criteria. The resulting uncertainty discourages pharmaceutical and device companies from investing in large-scale European studies. The lack of mandatory treatment standards from the European Medicines Agency or a pan-European clinical body means that adoption will remain anecdotal and geographically uneven, which affects both clinical credibility and commercial planning for manufacturers.

Scarcity of Trained Hyperbaric Medical Personnel

A shortage of certified hyperbaric physicians, nurses, and technicians also obstructs the expansion of the Europe hyperbaric oxygen therapy market. This scarcity constrains therapy delivery and chamber utilization across Europe. Training pathways vary widely, with countries like Sweden offering structured residency modules while others, such as Greece and Portugal, lack formal certification programs. Regulatory requirements under the EU Medical Device Regulation mandate direct physician supervision during pressurization and decompression phases, which further limits throughput. This human resource barrier delays patient access, increases per-session costs, and deters hospitals from acquiring new chambers. The full therapeutic and economic potential of hyperbaric oxygen therapy cannot be achieved without coordinated, EU-level investment in training, accreditation, and workforce planning.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Gulf Coast Hyperbarics, Inc.; Fink Engineering; ETC Hyperbaric Chambers (Environmental Tectonics Corporation); HAUX-LIFE-SUPPORT; HEARMEC; IHC Hytech B.V. (Royal IHC); Hyperbaric SAC; Sechrist Industries, Inc.; OxyHeal International; and SOS Group Europe Ltd. |

SEGMENTAL ANALYSIS

By Product Insights

The monoplace HBOT devices segment dominated the Europe hyperbaric oxygen therapy market by accounting for a substantial share in 2024. Factors such as their compact footprint, lower operational complexity, and cost efficiency compared to multiplace systems are propelling the growth of the monoplace HBOT devices segment. These single-occupancy chambers are ideally suited for outpatient wound clinics, dermatology centers, and private rehabilitation facilities that lack the space or staffing for larger units. According to studies, a notable share of newly established hyperbaric centers installed monoplace devices owing to faster regulatory approval and reduced facility modification requirements under EU fire safety directives. The average installation cost of a monoplace chamber is significantly lower than the investment needed for multiplace systems. Apart from these, monoplace units enable oxygen delivery without the need for masks, simplifying therapy for elderly or cognitively impaired patients. Countries have standardized monoplace use in diabetic foot ulcer protocols, further entrenching their dominance. Their compatibility with telemedicine monitoring and integration into multidisciplinary wound care pathways reinforces their position as the default choice for scalable and sustainable hyperbaric delivery across Europe.

The topical HBOT devices segment is predicted to witness the highest CAGR of 11.3% from 2026 to 2034. Unlike systemic chambers, these localized systems deliver oxygen directly to non-healing wounds through sealed dressings connected to portable oxygen concentrators, enabling treatment in home or primary care settings. This shift is driven by the urgent need to decongest specialized hyperbaric centers and reduce patient travel burden, particularly in rural regions. According to research, a share of the EU population lives more than 30 kilometers from a tertiary care hospital, limiting access to monoplace or multiplace therapy. Topical devices address this gap by allowing community nurses to manage chronic wounds with minimal training. Regulatory support is also accelerating adoption with the European Commission classifying these systems as Class IIa devices, which enables faster CE marking. Some companies have launched CE-certified topical platforms compatible with digital wound tracking, further fueling market momentum.

By Application Insights

The wound healing segment led the Europe hyperbaric oxygen therapy devices market by capturing a 64.8% share in 2024. The dominance of the wound healing segment is attributed to the high prevalence of chronic non-healing wounds, particularly diabetic foot ulcers and venous leg ulcers, which collectively affect millions of Europeans annually. National clinical guidelines recommend hyperbaric oxygen therapy as a second-line intervention for grade 3 or higher diabetic foot ulcers that fail standard care. The demand for advanced wound modalities in Europe remains structurally anchored in the continent's demographic and clinical landscape, driven by the significant share of the EU population aged 65 or older, a group at elevated risk for vascular insufficiency and impaired healing.

The infection treatment segment is estimated to register the fastest CAGR of 9.7% from 2026 to 2034 due to rising cases of antibiotic-resistant soft tissue infections, including necrotizing fasciitis and refractory osteomyelitis, which require adjuvant therapies to enhance antibiotic penetration and immune response. According to sources, antimicrobial resistance accounts for thousands of deaths annually in the EU, with complicated skin and soft tissue infections representing a share of resistant cases. Hyperbaric oxygen therapy combats this by elevating tissue oxygen tension, which enhances neutrophil oxidative killing and reduces anaerobic bacterial proliferation. National infection control protocols include hyperbaric referral pathways for such cases. Furthermore, the European Commission encourages non-antibiotic therapeutic innovations, which creates favourable policy tailwinds for hyperbaric adoption in infectious disease management.

COUNTRY LEVEL ANALYSIS

Germany Hyperbaric Oxygen Therapy Devices Market Analysis

Germany outperformed other regions in the Europe hyperbaric oxygen therapy devices market by occupying a 28.6% share in 2024. Its robust public healthcare infrastructure, strong reimbursement policies, and dominance in chronic disease management drive the prominence of the German market. The country operates certified hyperbaric centers, most integrated into university hospitals and specialized wound clinics. Statutory health insurers reimburse hyperbaric sessions for diabetic foot ulcers and radiation necrosis following strict but clear criteria under the Federal Joint Committee’s guidelines. Germany’s engineering expertise also supports domestic device innovation, with companies maintaining R&D and manufacturing facilities. The national focus on health technology assessment ensures evidence-based adoption, while federal investment in outpatient care expansion under the Hospital Relief Act enables wider chamber deployment beyond urban centers, solidifying Germany’s position as the market’s anchor.

United Kingdom Hyperbaric Oxygen Therapy Devices Market Analysis

The United Kingdom followed closely in the Europe hyperbaric oxygen therapy devices market by capturing a 15.2% share in 2024, which benefited from a centralized yet adaptive National Health Service structure and strong military medical integration. The UK hosts many nationally accredited hyperbaric units, including dedicated facilities at the Royal Navy Hospital, Haslar, and the Welsh Hyperbaric Unit in Swansea. The National Institute for Health and Care Excellence includes hyperbaric oxygen therapy in its quality standards for complex wounds under specific criteria, enabling consistent commissioning. Despite Brexit, the UK continues to align with European safety and training standards through the European Committee for Hyperbaric Medicine, ensuring clinical interoperability and device compatibility across the region.

France Hyperbaric Oxygen Therapy Devices Market Analysis

France is an attractive market for hyperbaric oxygen therapy devices in Europe due to its dense network of hospital-based hyperbaric units and proactive public health policies for chronic wound management. The French National Authority for Health lists hyperbaric oxygen therapy as a reimbursable act for six specific indications, including diabetic foot ulcers and osteoradionecrosis, with most certified nationwide as per the French Society for Hyperbaric and Diving Medicine. Military hospitals also serve civilian populations by enhancing resource utilization. France’s emphasis on multidisciplinary wound teams and integration of hyperbaric therapy into regional care pathways ensures steady device utilization while academic institutions lead European research into novel applications, including post-stroke recovery, further reinforcing the nation’s clinical and technological prowess.

Italy Hyperbaric Oxygen Therapy Devices Market Analysis

Italy experienced consistent growth in the Europe hyperbaric oxygen therapy devices market owing to a high burden of vascular diseases and a growing network of private hyperbaric clinics. According to sources, millions of Italians live with diabetes and the prevalence of peripheral artery disease. The National Health Service reimburses hyperbaric therapy for approved indications, but access varies regionally, prompting private investment in centers, particularly in Lombardy, Tuscany, and Sicily. Italy’s coastal geography and strong diving tourism industry also drive demand for decompression sickness treatment. Recent regulatory reforms under the National Recovery and Resilience Plan have streamlined CE certification for medical devices, encouraging local manufacturers to innovate in monoplace and topical systems. Italy's hybrid public-private healthcare model is fueling dynamic market growth, as regional health authorities increasingly outsource specialized care to accredited private providers.

Sweden Hyperbaric Oxygen Therapy Devices Market Analysis

Sweden is anticipated to expand notably in the Europe hyperbaric oxygen therapy devices market between 2025 and 2033 due to its universal healthcare access, high clinical standards, and integration of hyperbaric therapy into national rehabilitation frameworks. The country operates many nationally coordinated hyperbaric units with standardized protocols for wound care, radiation injury, and carbon monoxide exposure. Sweden’s healthcare system fully reimburses hyperbaric sessions when recommended by a multidisciplinary team, and electronic health records enable seamless referral tracking. Besides, Sweden’s participation in the Nordic Hyperbaric Network ensures cross-border training and equipment harmonization. A scalable and high-quality model for hyperbaric therapy in Northern Europe can be found in Sweden, where there is a strong emphasis on evidence-based practice, sustainability, and positive patient outcomes.

COMPETITIVE LANDSCAPE

The Europe hyperbaric oxygen therapy devices market features a mix of established engineering firms, specialized medical device manufacturers, and emerging innovators focused on niche applications. Competition is primarily driven by clinical performance, regulatory adherence, and service reliability rather than price alone. Leading companies differentiate through advanced safety systems, precise pressure control, and seamless integration with hospital workflows. The market remains moderately fragmented, with no single entity dominating all segments, though German and US-based firms hold strong positions in institutional settings. New entrants are gaining traction in topical and portable segments by targeting cost-sensitive outpatient and home care environments. Regulatory complexity under the EU MDR acts as a barrier to entry, favoring players with robust quality management systems. Clinical evidence generation through partnerships with academic centers is increasingly critical for reimbursement and adoption. As demand grows for decentralized and multidisciplinary wound care models, competition is shifting toward holistic solutions that combine hardware, software training, and outcome tracking to deliver measurable therapeutic value across Europe’s diverse healthcare landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe hyperbaric oxygen therapy devices market include

- Gulf Coast Hyperbarics, Inc.

- Fink Engineering

- ETC Hyperbaric Chambers (Environmental Tectonics Corporation)

- HAUX-LIFE-SUPPORT

- HEARMEC

- IHC Hytech B.V. (Royal IHC)

- Hyperbaric SAC

- Sechrist Industries, Inc.

- OxyHeal International

- SOS Group Europe Ltd.

TOP PLAYERS IN THE MARKET

- HAUX Life Support GmbH is a Germany-based engineering company specializing in the design and manufacture of high-precision monoplace and multiplace hyperbaric oxygen therapy chambers for clinical and military applications. HAUX has reinforced its position through continuous innovation in chamber ergonomics, patient monitoring integration, and fire safety systems. In recent years, the company expanded its service network to include remote diagnostics and technician training programs across Southern and Eastern Europe. It also collaborated with university hospitals in Berlin and Munich to develop protocol-specific chamber configurations for diabetic wound and radiation injury protocols, enhancing clinical adoption.

- Sechrist Industries Inc. is a US-headquartered global leader in hyperbaric oxygen therapy devices with significant penetration in the European market through direct sales and distribution partnerships. Sechrist maintains a European regulatory office in the Netherlands to manage CE certification and post-market surveillance in alignment with EU MDR requirements. Recently, the company introduced enhanced oxygen monitoring and pressure control software compliant with European safety directives. It also launched a technical support hub in France to provide rapid maintenance and staff training services, strengthening its service reliability and customer retention across Western Europe.

- OxyHeal Health Group is an emerging innovator focused on portable and topical hyperbaric oxygen therapy systems with growing influence in Europe’s home care and outpatient segments. Headquartered in the United Kingdom, the company develops lightweight topical HBOT devices that deliver targeted oxygen therapy to chronic wounds without requiring full chamber infrastructure. OxyHeal has secured multiple CE certifications under the EU Medical Device Regulation and established distribution agreements with wound care networks in Spain, Italy, and Poland. The company recently integrated digital wound assessment software into its devices, enabling real-time healing tracking for community nurses. Its strategy centers on decentralizing hyperbaric access through affordable, scalable solutions aligned with Europe’s shift toward integrated and cost-efficient chronic disease management.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Europe hyperbaric oxygen therapy devices market prioritize regulatory compliance through rigorous CE certification under the EU Medical Device Regulation to ensure market access. They invest in product innovation, focusing on enhanced safety features, integrated monitoring systems, and user-friendly interfaces. Companies expand service capabilities by establishing regional technical support hubs and training programs for clinical staff. Strategic collaborations with academic hospitals and wound care networks facilitate clinical validation and protocol integration. Firms also develop compact and portable systems to enable outpatient and home-based therapy, aligning with healthcare decentralization trends. Digitalization through remote diagnostics and electronic treatment logs improves operational efficiency. Furthermore, manufacturers engage in health technology assessment submissions to support reimbursement adoption. These strategies collectively enhance clinical credibility, device reliability, and long-term market sustainability across diverse European healthcare systems.

MARKET SEGMENTATION

This Europe hyperbaric oxygen therapy devices market research report is segmented and sub-segmented into the following categories.

By Product

- Monoplace HBOT Devices

- Multiplace HBOT Devices

- Topical HBOT Devices

By Application

- Wound Healing

- Decompression Sickness

- Infection Treatment

- Gas Embolism

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. Which countries lead the europe hyperbaric oxygen therapy devices market?

The UK and Germany lead the europe hyperbaric oxygen therapy devices market due to advanced healthcare infrastructure and high adoption rates

2. What are the primary applications of hyperbaric oxygen therapy in europe?

Key applications in europe hyperbaric oxygen therapy devices market include decompression sickness, wound healing, infection treatment, and carbon monoxide poisoning

3. How do regulations impact the europe hyperbaric oxygen therapy devices market?

Strict regulations and reimbursement policies influence adoption rates within the europe hyperbaric oxygen therapy devices market

4. What role do monoplace and multiplace chambers play in europe’s market?

Monoplace chambers dominate the europe hyperbaric oxygen therapy devices market due to convenience and cost-effectiveness; multiplace chambers serve hospitals for complex treatments

5. How is technological advancement shaping europe hyperbaric oxygen therapy devices market?

Innovations in portable and digital hyperbaric oxygen therapy devices enhance usability and treatment monitoring in the europe market

6. What are the key drivers for growth in the europe hyperbaric oxygen therapy devices market?

Rising chronic wounds, increased awareness of HBOT benefits, and advancements in device technology drive the europe hyperbaric oxygen therapy devices market growth

7. How does healthcare infrastructure affect the europe hyperbaric oxygen therapy devices market?

Developed healthcare systems in europe foster adoption and integration of hyperbaric oxygen therapy devices for multiple clinical uses

8. What is the impact of medical tourism on the europe hyperbaric oxygen therapy devices market?

Growth of medical tourism in europe contributes to higher demand and investments in hyperbaric oxygen therapy devices

9. Are hyperbaric oxygen therapy devices cost-effective in the european market?

These devices offer cost-effective treatment options in the europe hyperbaric oxygen therapy devices market by reducing healing times and hospital stays

10. What challenges does the europe hyperbaric oxygen therapy devices market face?

High therapy costs, reimbursement issues, and limited specialist availability restrict growth in the europe hyperbaric oxygen therapy devices market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com