Europe Milk Replacers Market Research Report Segmented By Type (Medicated, And Non-Medicated), Livestock (Ruminants, And Swine), Source (Milk-Based, Non-Milk-Based, And Blended), Form (Powdered, And Liquid), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe) - Industry Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Market Size, 2025

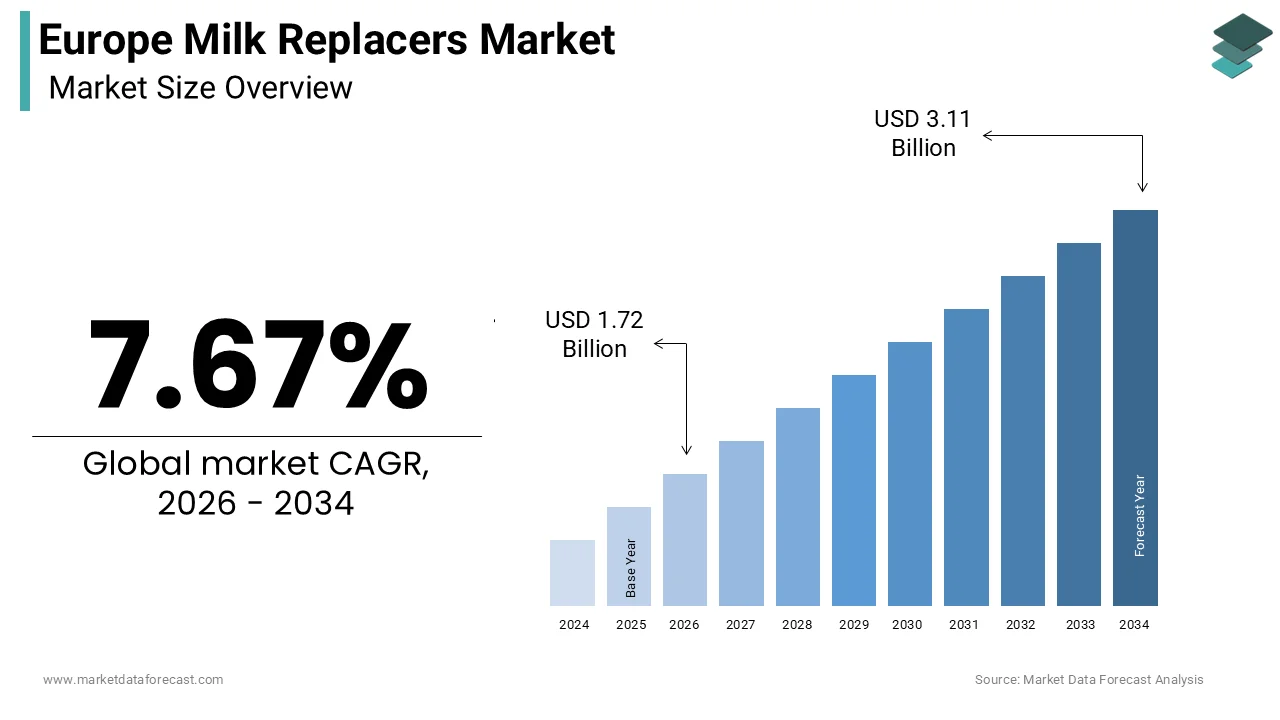

$1.60 BnMarket Estimate, 2026

$1.72 BnMarket Forecast, 2034

$3.11 BnCAGR, 2026–2034

7.67%Europe Milk Replacers Market Size

The Europe Milk Replacers Market size was calculated to be USD 1.60 billion in 2025 and is anticipated to be worth USD 3.11 billion by 2034, from USD 1.72 billion in 2026, growing at a CAGR of 7.67% during the forecast period.

Milk replacers in the European context refer to formulated feed products designed to substitute maternal milk for neonatal livestock, primarily calves, piglets, and lambs, composed of skimmed milk powder, whey proteins, vegetable oils, vitamins, and minerals. These products are engineered to support early growth immunity and digestive development while aligning with stringent EU animal welfare and food safety standards. Unlike generic feed additives, milk replacers serve as a critical nutritional bridge during the first weeks of life when natural milk is unavailable or insufficient. According to the European Food Safety Authority, over 85 percent of dairy farms in the EU now use standardized milk replacers for calf rearing to ensure consistent nutrient intake and reduce disease transmission risks. As per the European Commission’s Farm to Fork Strategy, the use of medicated milk replacers has declined by 32 percent since 2021 due to tightened regulations on antimicrobial use in livestock. National policies such as Germany’s Animal Husbandry Act and France’s Eco Antibio Plan further mandate precise feeding protocols that elevate milk replacers from optional supplements to essential components of responsible livestock management. This regulatory and ethical embedding distinguishes Europe’s market as one driven by science-based husbandry rather than cost arbitrage.

MARKET DRIVERS

Stringent Animal Welfare Regulations Mandating Controlled Neonatal Nutrition

European Union legislation increasingly requires structured and traceable feeding practices for young livestock to improve survival rates and reduce antibiotic dependency. According to the European Commission’s Animal Welfare Strategy 2021–2027, all member states must ensure calves receive a minimum daily energy intake equivalent to 13 percent of their body weight during the first eight weeks—a standard best met through calibrated milk replacers. In Germany, the Federal Ministry of Food and Agriculture reported that 92 percent of dairy farms adopted certified milk replacers in 2024 to comply with the revised Animal Husbandry Ordinance, which prohibits inconsistent or diluted maternal milk feeding. Similarly, the French Agency for Food, Environmental and Occupational Health & Safety confirmed that farms using standardized replacers saw a 28 percent reduction in neonatal diarrhea cases between 2022 and 2024. As per the European Medicines Agency, veterinary guidelines now discourage routine antibiotic inclusion in milk feeds, pushing producers toward functional ingredients like prebiotics and immunoglobulins. These regulatory shifts transform milk replacers from convenience tools into compliance necessities, ensuring stable institutional demand across the EU’s 4.2 million dairy holdings.

Rising Adoption of Precision Livestock Farming and Data-Driven Calf Management

Modern European dairy operations increasingly integrate milk replacers into automated feeding systems that adjust dosage, temperature, and composition based on real-time animal data. According to the European Federation of Animal Science, over 65 percent of large-scale dairy farms in the Netherlands, Denmark, and Germany used computer-controlled calf feeders in 2024, which rely exclusively on consistent powder formulations to function accurately. The Danish Agricultural Advisory Service reported that farms using sensor-monitored replacer systems achieved 12 percent higher average daily weight gain and 19 percent lower mortality compared to manual feeding. As per the European Institute of Innovation and Technology EIT Food, 14 projects in 2024 focused on smart milk replacer dispensers that sync with herd management software to track individual calf performance. This digitization trend demands high solubility, low dust, and batch consistency—qualities only specialized replacers provide. Consequently, precision farming not only increases usage volume but also elevates technical requirements, driving innovation in formulation and delivery rather than price competition.

MARKET RESTRAINTS

High Dependency on Imported Dairy Ingredients and Price Volatility

Europe’s milk replacer industry relies heavily on imported dairy permeate and whey protein concentrates from non-EU countries, creating supply chain vulnerabilities. According to the European Dairy Association, over 40 percent of skimmed milk powder used in European milk replacers was sourced from New Zealand, the United States, and Argentina in 2024 due to domestic shortages caused by declining fluid milk consumption. The European Commission’s Market Observatory for Dairy reported that global dairy commodity prices fluctuated by up to 35 percent in 2023, triggering corresponding cost spikes for replacer manufacturers. In Poland, the National Federation of Dairy Farmers noted that 28 percent of small calf rearers switched back to raw milk feeding in 2024 due to replacer prices exceeding 2.80 euros per kilogram. As per Eurostat, EU dairy exports fell by 12 percent in 2023 while domestic cheese production rose, diverting skim milk away from powder production. This structural imbalance between local supply and industrial demand constrains pricing stability and limits scalability for domestic replacer producers despite strong end-user demand.

Consumer and NGO Pressure Against Intensive Calf Rearing Practices

Growing public scrutiny over early weaning and separation of calves from dams has led to reputational and policy risks for milk replacer use, even when scientifically justified. According to the European Citizens’ Initiative “End the Cage Age,” over 1.4 million signatures were collected in 2023, calling for bans on practices perceived as unnatural, including artificial milk feeding. In Sweden, the National Board of Agriculture reported that 18 percent of organic dairy farms abandoned milk replacers entirely in 2024, opting for extended suckling systems to meet stricter KRAV certification standards. As per the European Food Safety Authority EFSA issued a scientific opinion in 2024, acknowledging that while replacers can be nutritionally adequate, prolonged separation remains a welfare concern under public perception. Retailers like REWE and Coop have introduced “calf with dam” labeling schemes that implicitly devalue replacer-based systems. This social pressure forces producers to justify usage beyond nutrition—framing it within holistic welfare programs—adding complexity and marketing costs even when technical benefits are clear.

MARKET OPPORTUNITIES

Integration of Functional Ingredients for Gut Health and Antimicrobial Reduction

The EU’s aggressive stance against routine antibiotic use in livestock creates a high-value opening for milk replacers fortified with gut health promoters. According to the European Medicines Agency, sales of medicated calf feeds dropped by 41 percent between 2021 and 2024, prompting producers to adopt alternatives like yeast beta-glucans, colostrum derivatives, and medium-chain fatty acids. In the Netherlands, the Central Veterinary Institute confirmed that farms using replacers with added immunoglobulins reduced antibiotic treatments by 33 percent without compromising growth rates. As per the European Feed Manufacturers Federation, over 60 new functional replacer formulations received authorization under Regulation EC 1831/2003 in 2024 alone, focusing on microbiome modulation and pathogen inhibition. Companies like Trouw Nutrition and Agrifirm launched EU-compliant products containing protected organic acids that survive pasteurization and enhance intestinal integrity. With the EU targeting a 50 percent reduction in farm antibiotic use by 2030, this shift from therapeutic to preventive nutrition positions advanced replacers as essential tools in sustainable livestock health management.

Expansion into Small Ruminant and Alternative Livestock Segments

While calves dominate current usage, emerging demand from sheep, goat, and even deer farming offers untapped growth avenues. According to the European Sheep and Goat Farmers Association, over 220 000 small ruminant farms in Southern and Eastern Europe began using species-specific milk replacers in 2024 to offset labor shortages and improve kid lamb survival during peak kidding seasons. In Spain, the Ministry of Agriculture reported a 27 percent increase in goat milk replacer sales between 2022 and 2024, driven by intensification in Murcia and Andalusia. As per the European Bison Conservation Center, specialized replacers are now used in captive breeding programs for endangered ungulates requiring precise fat and protein ratios unattainable with bovine formulas. Additionally, the rise of urban micro dairies raising dwarf goats or sheep creates niche demand for premium small batch replacers. Unlike the saturated calf segment, these markets lack standardized products, allowing innovators to command premium pricing and build loyalty through tailored nutritional science rather than volume discounts.

MARKET CHALLENGES

Fragmented Regulatory Approval Processes for Novel Feed Additives

Despite EU-level frameworks, national divergences in feed additive authorization delay market entry and increase compliance costs. According to the European Commission’s Standing Committee on Plants, Animals, Food and Feed, only 12 out of 27 member states have aligned their national assessment timelines with EFSA’s centralized procedure, causing approval delays of up to 14 months for new replacer ingredients. In 202,4 an Italian manufacturer halted the launch of a selenium-enriched replacer after Germany’s Federal Office of Consumer Protection demanded additional residue studies not required in France. As per the European Feed Additives Association, over 35 percent of innovative replacer formulations remain confined to single-country markets due to inconsistent interpretations of Regulation EC 1831/2003 on zootechnical claims. This fragmentation discourages SMEs from investing in R&D and favors large multinationals with regulatory affairs teams. Until mutual recognition becomes enforceable, Europe’s milk replacer innovation will remain stifled by administrative friction rather than scientific or market barriers.

Limited Technical Expertise Among Small and Medium-Sized Farms

Effective use of advanced milk replacers requires knowledge of mixing ratios, water temperature, hygiene, and feeding schedules—competencies often lacking in smaller operations. According to the European Network for Rural Development, 58 percent of EU farms with fewer than 50 cows do not have access to regular veterinary or nutritional advisory services. In Romania, the National Sanitary Veterinary Authority recorded that 34 percent of calf mortality in 2024 was linked to improper replacer preparation, including incorrect dilution or use of contaminated equipment. As per the Irish Cattle and Sheep Farmers Association, only 29 percent of part-time farmers could correctly identify the protein content required for optimal growth, leading to substandard formulations. While digital tools exist, most are in English or German, limiting accessibility. This knowledge gap results in underperformance of even high-quality products, eroding trust and driving regression to traditional methods. Bridging this advisory deficit through localized training and simplified packaging is critical to unlocking broader adoption beyond large commercial units.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.67% |

| Segments Covered | By Type, Livestock, Source, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Hi-Pro Feeds LP, Manna Pro Products LLC, PBS Animal Health, Milk Products LLC, Cargill Incorporated, Archer Daniels Midland Company, Kent Nutrition Group, Inc, Alltech, Glanbia, Plc, and Y FrieslandCampina |

SEGMENTAL ANALYSIS

By Type Insights

Non-medicated milk replacers account for approximately 78 percent of the Europe milk replacers market in 2025, driven by stringent EU regulations restricting antimicrobial use in livestock. According to the European Medicines Agency, sales of medicated calf feeds declined by 41 percent between 2021 and 2024 as part of the EU’s “One Health” action plan to curb antimicrobial resistance. The European Commission’s Regulation EC 2019/6 prohibits the routine use of antibiotics in feed, with prescriptions now limited to diagnosed clinical cases under veterinary supervision. In Germany, the Federal Office of Consumer Protection reported that 93 percent of dairy farms voluntarily transitioned to non-medicated replacers by 2024 to align with retailer sustainability standards such as those from EDEKA and REWE. As per the European Food Safety Authority EFSA confirmed that farms using high-quality non-medicated replacers with functional additives like immunoglobulins and organic acids achieved comparable health outcomes to medicated systems without contributing to resistance risks. This regulatory and market-driven shift has made non-medicated formulations the default choice across both conventional and organic operations, ensuring sustained dominance.

The non-medicated segment is expanding at a compound annual growth rate of 6.3 percent through 2030, fueled by innovation in gut health nutrition and alignment with public health mandates. According to the European Feed Manufacturers Federation, over 65 new non-medicated replacer formulations received EU authorization in 2024, featuring prebiotics, yeast derivatives, and medium-chain fatty acids that enhance intestinal barrier function. In the Netherlands, the Central Veterinary Institute documented a 29 percent reduction in neonatal diarrhea on farms using advanced non-medicated replacers enriched with colostrum fractions. As per the European Commission’s Farm to Fork Strategy, member states must reduce farm antibiotic sales by 50 percent by 2030, accelerating investment in preventive nutrition. Companies like Trouw Nutrition and Vilofoss launched EU-compliant products with protected organic acids that survive pasteurization and modulate gut microbiota. Retailer pressure further amplifies demand; France’s Carrefour requires all private label veal suppliers to use certified non-medicated feeding protocols. This convergence of science policy and consumer expectation ensures non-medicated replacers lead not only in volume but in value-added innovation.

By Livestock Insights

Ruminants represent roughly 82 percent of the Europe milk replacers market in 2025, primarily due to the scale and structure of the EU dairy sector, where early calf separation necessitates consistent artificial feeding. According to Eurostat, the EU housed over 22 million dairy cows in 2024, with each producing one calf annually, requiring 45 to 60 kilograms of milk replacer during the first eight weeks. The European Commission’s Animal Welfare Strategy mandates minimum daily energy intake for calves—a standard best met through standardized replacers rather than variable raw milk. In Germany, the Federal Ministry of Food and Agriculture reported that 89 percent of dairy farms used calf milk replacers in 2024 to ensure uniform nutrient delivery and reduce pathogen transmission from dam to offspring. As per the European Dairy Association, large-scale operations in the Netherlands, Denmark, and France rely on automated feeding systems that require precise powder solubility and composition, only achievable with commercial ruminant formulations. This structural dependency on controlled neonatal nutrition in a highly regulated dairy ecosystem ensures ruminants remain the dominant application segment.

The swine segment is the fastest growing with a compound annual growth rate of 5.8 percent, driven by intensification of piglet production and rising pre-weaning mortality concerns. According to the European Pig Farmers Association, over 240 million piglets are born annually in the EU, with average pre-weaning mortality hovering at 14 percent, prompting increased use of milk replacers during lactation supplementation and post weaning transition. In Spain, the Ministry of Agriculture reported a 22 percent rise in sow farm adoption of liquid milk replacers between 2022 and 2024 to support large litters exceeding maternal milk capacity. As per the Danish Agricultural Advisory Service, farms using creep feeding with specialized porcine replacers achieved 11 percent higher weaning weights and reduced post-weaning diarrhea by 18 percent. The European Feed Additives Association noted that 40 new swine-specific replacer formulations were authorized in 2024, featuring highly digestible whey protein and egg derivatives tailored to piglet enzymatic profiles. With the EU targeting improved piglet welfare under its revised animal transport rules, this segment offers high potential for precision nutrition solutions beyond traditional ruminant dominance.

By Source Insights

Milk-based milk replacers hold approximately 65 percent of the Europe market in 2025 due to superior digestibility, palatability, and compliance with EU nutritional standards for neonatal livestock. According to the European Food Safety Authority, calves fed milk-based replacers with at least 20 percent crude protein and 15 percent fat achieve optimal growth rates and immune development unmatched by plant alternatives. The European Commission’s Regulation EC 889/2008 permits only milk-derived ingredients in organic calf feeding, reinforcing preference among certified farms. In France, the National Federation of Organic Farmers reported that 94 percent of organic dairy operations exclusively use milk-based replacers to maintain certification. As per the German Agricultural Society, trials confirmed that milk-based formulas reduced abomasal bloat incidence by 37 percent compared to soy-based alternatives. Despite higher cost, the biological performance and regulatory acceptance of dairy ingredients make them the gold standard, particularly in high-value veal and premium dairy systems, where health outcomes directly impact profitability.

The blended segment is growing at a compound annual growth rate of 7.1 percent as producers balance cost performance and sustainability through strategic ingredient hybridization. According to the European Feed Manufacturers Federation, blended replacers combining skim milk powder, whey, and carefully processed plant proteins like potato or pea accounted for 28 percent of new product launches in 2024. In the Netherlands, Wageningen University research showed that replacing up to 30 percent of dairy protein with enzymatically hydrolyzed pea protein maintained digestibility while reducing formulation costs by 12 percent. As per the European Dairy Association, rising skim milk powder prices—up 22 percent in 2023 due to export competition—have accelerated adoption of partial substitution models. Companies like Agrifirm and ForFarmers introduced EU-compliant blended products with protected plant proteins that avoid anti-nutritional factors. Additionally, the EU’s Green Deal encourages reduced reliance on imported dairy concentrates, making locally sourced plant components strategically attractive. This pragmatic fusion of tradition and innovation positions blended replacers as the most dynamic frontier in cost-conscious yet performance-driven markets.

REGIONAL ANALYSIS

Germany Milk Replacers Market Analysis

Germany holds the largest share of the Europe milk replacers market at approximately 22 percent in 2025, driven by its vast dairy sector and strict animal welfare enforcement. According to the Federal Statistical Office, Germany housed 3.8 million dairy cows in 2024, each requiring standardized calf feeding under the revised Animal Husbandry Ordinance. The Federal Ministry of Food and Agriculture reported that 89 percent of farms used certified milk replacers to meet minimum energy intake mandates and reduce antibiotic use. Leading cooperatives like Deutsches Milchkontor supply regionally formulated products aligned with local forage profiles. As per the German Agricultural Society, automated calf feeding systems are installed on 68 percent of large farms, creating consistent demand for high solubility powders. Germany’s dual emphasis on regulatory compliance and technological adoption makes it the undisputed anchor of Europe’s milk replacer ecosystem.

France Milk Replacers Market Analysis

France ranks second with a 17 percent market share in 2025, characterized by the strong integration of replacers into both conventional and organic dairy systems. According to FranceAgriMer, the national agricultural board, over 3.4 million dairy cows produced 24 billion liters of milk in 2024, with nearly all calf rearers using standardized replacers to comply with the Eco Antibio 2 plan. The French Agency for Food, Environmental and Occupational Health & Safety confirmed that organic farms must use 100 percent milk-based replacers under EU Regulation 2018/848—a rule driving premium product demand. In Normandy and Brittany, regional cooperatives like Lactalis Nutrition Animale develop breed-specific formulations for Holstein and Montbéliarde calves. As per the National Federation of Organic Farmers, 92 percent of certified operations prioritize replacers with traceable dairy origins. France’s blend of regulatory rigor, agricultural diversity, and cooperative infrastructure secures its leadership position.

Netherlands Milk Replacers Market Analysis

The Netherlands holds the third largest share at 13 percent in 2025, marked by innovation in precision feeding and functional nutrition. According to the Dutch Central Bureau of Statistics, the country’s 1.5 million dairy cows operate under some of Europe’s highest welfare standards, requiring individualized calf nutrition plans. The Dutch Dairy Association reported that 74 percent of farms use computer-controlled feeding robots that demand consistent replacer solubility and batch quality. Wageningen University research underpins many EU-authorized functional additives, including immunoglobulin-enriched formulations that cut antibiotic use by 30 percent. As per the Netherlands Enterprise Agency, over 20 feed tech startups received funding in 2024 to develop next-generation replacers with microbiome modulators. The country’s compact size, world-class research, and export-oriented dairy model make it a high-intensity laboratory for advanced milk replacer deployment.

Spain Milk Replacers Market Analysis

Spain commands the fourth position with an 11 percent market share in 2025, driven by the rapid intensification of both dairy and swine production. According to the Spanish Ministry of Agriculture, the number of intensive dairy farms grew by 18 percent between 2022 and 2024, particularly in Castile and León, where labor shortages increased reliance on automated calf feeding. Simultaneously,y Spain’s massive pig sector—producing 52 million hogs annually—boosted demand for liquid milk replacers to support oversized litters. The Interprofessional Dairy Organization confirmed that 63 percent of new dairy installations in 2024 included replacer feeding protocols to meet EU welfare audits. As per the Spanish Feed Manufacturers Association, imports of whey protein concentrates rose by 25 percent in 2024 to meet formulation needs. Spain’s dual focus on ruminant and swine applications creates a uniquely diversified demand base within Southern Europe.

Denmark Milk Replacers Market Analysis

Denmark ranks fifth with a 9 percent market share in 2025, reflecting its leadership in data-driven livestock management and cooperative farming. According to Statistics Denmark, the country’s 560 000 dairy cows are managed through integrated herd systems where milk replacer usage is tracked alongside health and growth metrics. The Danish Agricultural Advisory Service reported that 81 percent of farms use replacers with added organic acids and prebiotics to comply with the national “Yellow Card” antimicrobial reduction scheme. Arla Foods Ingredients supplies high-purity whey fractions to domestic replacer producers, ensuring consistent quality. As per the Danish Veterinary and Food Administration, all calf rearers must document feeding protocols during official inspections—a rule that institutionalizes replacer use. Denmark’s combination of small farm density, scientific rigor, and cooperative logistics makes it a benchmark for efficient and welfare-aligned milk replacer adoption in Northern Europe.

COMPETITION OVERVIEW

Competition in the Europe milk replacers market is defined by a convergence of scientific rigor, regulatory compliance, and farmer-centric service rather than price alone. Unlike global markets, where cost dominates, European players compete on nutritional precision, traceability, and alignment with public health and animal welfare policies. The landscape features a mix of multinational nutrition specialists like Trouw Nutrition, integrated dairy ingredient suppliers such as Arla Foods Ingredients, and regional feed cooperatives, including ForFarmers. Regulatory pressure from the EU’s Farm to Fork Strategy and national antimicrobial reduction plans has elevated technical standards favoring companies with robust R&D and quality control. At the same time, fragmentation across 27 member states creates opportunities for localized formulations and advisory models. Innovation is increasingly collaborative, with feed producers partnering with veterinary institutes, universities, and digital agritech firms to develop data-driven solutions. As a result, competition centers less on volume and more on trust, credibility, and the ability to deliver measurable health outcomes within Europe’s evolving ethical and environmental framework for livestock farming.

KEY MARKET PLAYERS

A few major players of the Europe milk replacers market include

- Hi-Pro Feeds LP

- Manna Pro Products LLC

- PBS Animal Health

- Milk Products LLC

- Cargill Incorporated

- Archer Daniels Midland Company

- Kent Nutrition Group, Inc

- Alltech

- Glanbia Plc

- Y FrieslandCampina

Top Strategies Used by the Key Market Participants

Key players in the Europe milk replacers market pursue strategies centered on regulatory alignment, nutritional innovation, and farmer enablement. First, they reformulate products to eliminate antibiotics and incorporate functional additives like immunoglobulins, prebiotics, and protected organic acids to comply with EU antimicrobial reduction mandates. Second, they invest in traceable high-quality dairy and alternative ingredients to ensure consistency and meet organic or sustainability certification requirements. Third, they integrate digital advisory tools that guide feeding protocols based on real-time animal data, enhancing outcomes and compliance. Fourth, they expand local production and blending capabilities to reduce dependency on volatile global dairy markets and shorten supply chains. Fifth, they deliver on-farm education and technical support to bridge knowledge gaps among smallholders, ensuring correct usage and maximizing product efficacy. These strategies reflect a shift from commodity supply to holistic livestock health partnerships.

Leading Players in the Market

- Trouw Nutrition, a Netherlands-based subsidiary of Nutreco, is a leading innovator in the Europe milk replacers market offering science-driven formulations under brands like Sprayfo and Milkiwean. The company focuses on gut health, immunity, and antimicrobial reduction through functional ingredients such as immunoglobulins, organic acids, and precision protein blends. In 202,4 Trouw Nutrition launched a next-generation non-medicated calf replacer compliant with EU Farm to Fork antibiotic reduction targets and integrated with its NutriOpt digital advisory platform for real-time feeding optimization. It also expanded its whey processing facility in Deventer to secure high-quality dairy ingredients amid rising import volatility. By combining nutritional science digital tools and regulatory foresight, Trouw Nutrition has positioned itself as a strategic partner for sustainable livestock production across Europe.

- Arla Foods Ingredients, a Danish cooperative, supplies high-purity whey and milk protein fractions that serve as critical raw materials for premium milk replacers across Europe. The company leverages its integrated dairy supply chain to offer traceable, sustainable, and allergen-controlled ingredients aligned with EU organic and clean label standards. In 2024, Arla Foods Ingredients introduced a new lactose-reduced whey concentrate specifically designed for sensitive piglet and calf digestion, enhancing solubility and reducing osmotic stress. It also partnered with major replacer manufacturers to develop carbon footprint-verified ingredient batches supporting EU Green Public Procurement criteria. Through vertical integration and nutritional R&D, Arla Foods Ingredients ensures consistent quality and ethical sourcing that underpins Europe’s shift toward performance-driven non-medicated formulations.

- ForFarmers Group, headquartered in the Netherlands, is a major integrated feed producer with a strong presence in the European milk replacers segment through tailored solutions for dairy and swine operations. The company emphasizes local production, circular sourcing, and advisory services to support small and medium-sized farms in adopting best practices. In 2024, ForFarmers launched a blended milk replacer series incorporating enzymatically processed pea protein to reduce reliance on imported dairy concentrates while maintaining digestibility. It also rolled out a mobile training program across Germany, France, and Poland to educate farmers on proper mixing hygiene and feeding schedules—addressing a key adoption barrier. By combining localized manufacturing with hands-on knowledge transfer, ForFarmers strengthens trust and technical compliance in diverse regional markets.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Trouw Nutrition launched a non-medicated calf milk replacer with immunoglobulin enrichment certified under EU antimicrobial reduction guidelines for use across dairy farms in Germany and France.

- In April 202,4 Arla Foods Ingredients introduced a lactose-reduced whey concentrate specifically engineered for sensitive neonatal digestion in both calves and piglets to enhance solubility and reduce gastrointestinal stress.

- In June 2024, ForFarmers Group rolled out a blended milk replacer series incorporating enzymatically hydrolyzed pea protein to decrease reliance on imported dairy ingredients while maintaining high digestibility standards.

- In August 2024, Trouw Nutrition integrated its Milkiwean calf replacer portfolio with the NutriOpt digital platform, enabling real-time feeding recommendations based on individual calf weight and health metrics.

- In October 2024, Arla Foods Ingredients partnered with three major European replacer manufacturers to supply carbon footprint-verified whey batches supporting compliance with EU Green Public Procurement criteria.

MARKET SEGMENTATION

This research report on the Europe milk replacers market has been segmented and sub-segmented based on type, livestock, source, and region.

By Type

- Medicated

- Non-Medicated

By Livestock

- Ruminants

- Swine

By Source

- Milk-Based

- Non-Milk-Based

- Blends

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1.What are milk replacers made of?

Milk replacers are typically made from dairy proteins, plant-based proteins, fats, vitamins, minerals, and additives designed to mimic natural milk.

2. What factors are driving the growth of this market in Europe?

Key drivers include increasing livestock farming, rising demand for high-quality animal nutrition, and the need for cost-effective feeding solutions.

3. Which animals commonly use milk replacers?

Milk replacers are mainly used for calves, piglets, lambs, and sometimes for pets and other young animals.

4. What are the benefits of using milk replacers?

They ensure consistent nutrition, improve animal growth rates, reduce disease transmission, and offer cost efficiency compared to natural milk.

5. What challenges does the Europe milk replacers market face?

Challenges include fluctuating raw material prices, concerns about product quality, and regulatory compliance requirements.

6. What are the different types of milk replacers available?

They are mainly categorized into medicated and non-medicated milk replacers, as well as dairy-based and plant-based formulations.

7. How is the market segmented by ingredient type?

It is segmented into milk-based proteins, soy proteins, and other plant-based ingredients.

8. What role does technology play in this market?

Advancements in feed formulation and processing technologies help improve digestibility and nutritional value.

9. What trends are shaping the Europe milk replacers market?

Trends include increased use of plant-based proteins, precision nutrition, and sustainable feed solutions.

10. What is the future outlook of the Europe milk replacers market?

The market is expected to grow steadily due to rising demand for efficient livestock production and improved animal nutrition practices.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com