Europe Peas Market Size, Share, Trends, and Growth Analysis Report, Segmented by Category, Type of Peas, Application, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

Europe Peas Market Report Summary

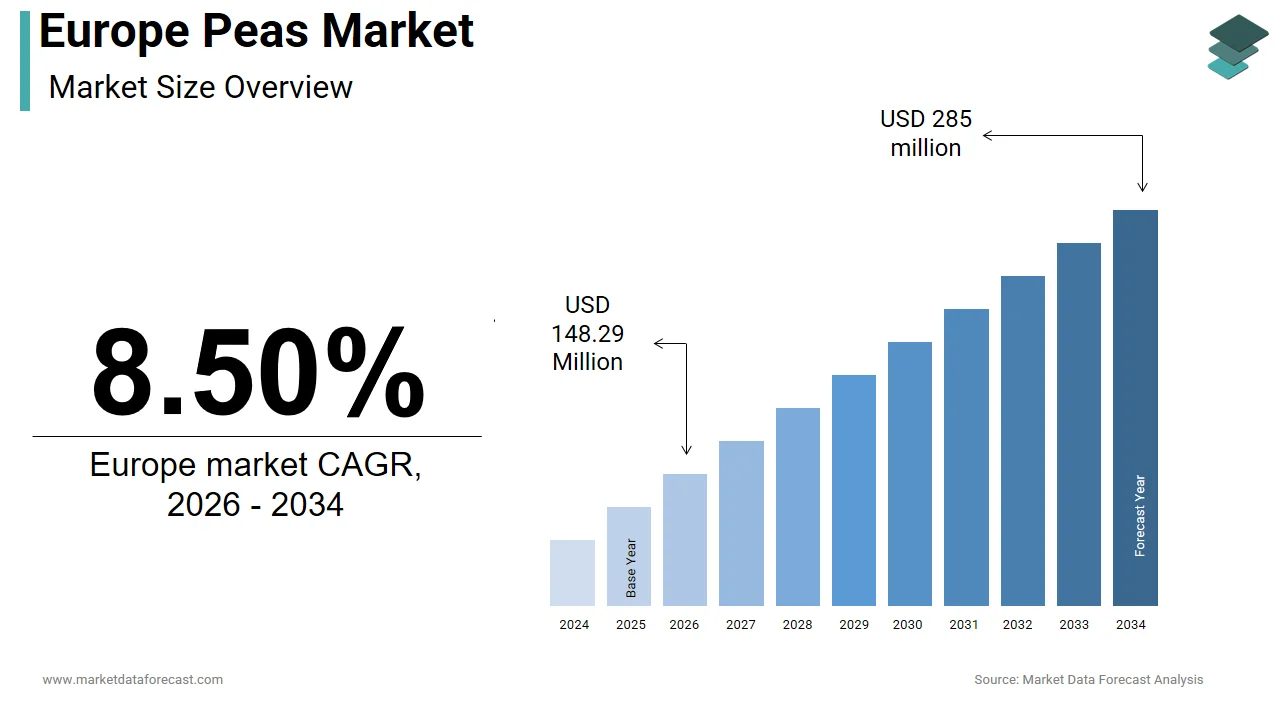

The Europe peas market was valued at USD 137 million in 2025 and is projected to grow from USD 148.29 million in 2026 to USD 285 million by 2034, registering a CAGR of 8.50% from 2026 to 2034. Market growth is driven by increasing consumer demand for plant-based foods, rising health consciousness, and expanding applications of peas in food processing and functional nutrition. Growing adoption of sustainable agricultural practices, increasing demand for protein-rich ingredients, and the expanding use of peas in convenience foods, meat alternatives, and beverage formulations are further supporting market expansion.

Key Market Trends

- Rising demand for plant-based and protein-rich food ingredients.

- Increasing consumption of fresh, frozen, and processed peas across Europe.

- Growing use of peas in functional foods, meat alternatives, and plant-based beverages.

- Expansion of sustainable farming practices and environmentally friendly crop production.

- Increasing retail availability through supermarkets, hypermarkets, and online distribution channels.

Segmental Insights

- Based on category, the inorganic peas segment dominated the Europe peas market in 2025, driven by lower production costs, established cultivation practices, and well-developed supply chains that ensure consistent availability for mainstream consumers.

- Based on type, the green peas segment accounted for the largest market share in 2025, supported by their widespread culinary use, nutritional value, and strong demand from both household consumers and the food processing industry.

- Based on application, the food and beverages segment held the leading market share in 2025, owing to the growing use of peas in frozen foods, ready-to-eat meals, soups, snacks, plant-based products, and nutritional ingredients.

- Based on distribution channel, the indirect distribution segment dominated the market in 2025, driven by the extensive presence of supermarkets, hypermarkets, wholesalers, specialty retailers, and foodservice distribution networks across Europe.

Regional Insights

The Europe peas market continues to expand across major agricultural economies, supported by increasing consumer demand, strong agricultural production, and growing investments in sustainable food systems.

- France dominated the European peas market in 2025, serving as the region's leading producer and consumer of peas due to its extensive agricultural land, favorable climatic conditions, and strong food processing industry.

- The United Kingdom held the second-largest position in the regional market, supported by high per capita consumption, strong demand for frozen peas, and well-established retail distribution networks.

- Germany maintained a significant share of the Europe peas market, driven by its large consumer base, increasing demand for fresh and processed peas, and growing preference for healthy and plant-based food products.

Competitive Landscape

The Europe peas market is moderately competitive, with leading food manufacturers and agricultural companies focusing on product innovation, sustainable sourcing, and expansion of plant-based food portfolios. Market participants are investing in advanced processing technologies, strategic partnerships, and distribution network expansion to strengthen their market presence. Growing demand for functional foods and plant-based nutrition continues to create new opportunities across the value chain.

Prominent companies operating in the Europe peas market include Blue Lake Milling, Grain Millers, Inc., Greenyard, Morning Foods Ltd., Bonduelle, Ardo, General Mills, Inc., Avena Foods Limited, Richardson International Limited, Cerealto Siro Foods, Premier Nutrition Company, LLC, Nestlé SA, Molino Spadoni S.p.A., Weetabix, Valsemøllen, Grillon D'Or, Clif Bar & Company, Associated British Foods plc, and Danone SA.

Europe Peas Market Size

The Europe peas market was valued at USD 137 million in 2025, is estimated to reach USD 148.29 million in 2026, and is projected to reach USD 285 million by 2034, growing at a CAGR of 8.50% from 2026 to 2034.

A pea is a small, round, edible green seed that grows inside a pod on a climbing vine (Pisum sativum). This sector is integral to the European agricultural landscape, serving as a critical source of plant-based protein and a staple ingredient in diverse culinary traditions. The market is characterized by a strong emphasis on sustainability, driven by the crop’s ability to fix nitrogen in the soil, which aligns with the European Union’s Green Deal objectives. According to Eurostat, France remains the leading producer of fresh green peas in Europe, harvesting 270 thousand tonnes in 2023. Meanwhile, European Commission market forecasts independently project total EU-27 field pea production to reach roughly 2.27 million metric tonnes. The regulatory environment is shaped by strict food safety standards and labeling requirements that ensure transparency for consumers. As per the European Commission, the total agricultural land dedicated specifically to pea cultivation in the EU-27 reached 827 thousand hectares, marking a sharp year-over-year increase of 7.53% due to national eco-schemes rewarding crop rotation. Consumer preferences are shifting toward convenience and health, driving demand for value-added products such as ready-to-eat meals and protein isolates. The industry is also witnessing a surge in organic pea production, responding to the rising demand for chemical-free produce. Supply chains are becoming increasingly integrated, with vertical coordination between farmers and processors ensuring consistent quality and supply stability. This dynamic ecosystem supports a wide range of stakeholders from smallholder farmers to large multinational food manufacturers.

MARKET DRIVERS

Surging Demand for Plant-Based Protein and Alternative Meat Sources

The escalating global shift toward plant-based diets fuels the growth of the Europe peas market. This is particularly due to the high protein content and functional properties of pea derivatives. Peas are increasingly utilized as a key ingredient in meat alternatives, dairy-free milks, and protein supplements, offering a sustainable and allergen-friendly option compared to soy or wheat. According to The Good Food Institute Europe, while overall alternative protein retail trajectories experienced country-specific value shifts, pea protein remained an industry-preferred texturization substrate due to its versatile structural functionality and flavor neutrality in food applications. Consumers are actively seeking foods that reduce their environmental footprint while maintaining nutritional adequacy, and peas fit this profile perfectly due to their low water usage and carbon sequestration capabilities. Food manufacturers are investing heavily in extraction technologies to produce high-purity pea protein isolates, which are then incorporated into burgers, sausages, and snacks. This industrial demand creates a robust secondary market for dry peas, stabilizing prices for growers. Health-conscious individuals also consume whole peas for their fiber and micronutrient content, supporting digestive health and blood sugar regulation. The versatility of peas allows them to be seamlessly integrated into various product formats, from powders to textured chunks. Regulatory support for sustainable agriculture further incentivizes the use of legumes in food systems. This structural shift in consumer behavior ensures long-term growth for the pea sector beyond traditional fresh consumption.

Expansion Of Organic Farming and Sustainable Agricultural Practices

Organic farming is expanding rapidly across the region, which has propelled significant demand for organic peas, further boosting the expansion of the Europe peas market. This is driven by consumers who increasingly prioritize chemical-free and environmentally responsible food sources. Peas are well suited for organic cultivation due to their natural nitrogen-fixing abilities, which reduce the need for synthetic fertilizers and improve soil health for subsequent crops. As per the Research Institute of Organic Agriculture FiBL, overall European organic retail markets expanded past 54 billion euros, sustained by strong consumer pull for plant-based staples, pulses, and organic crop alternatives. Retailers are expanding their organic assortments to include frozen and canned organic peas, catering to the convenience needs of busy households. Government policies under the EU Farm to Fork Strategy aim to increase the share of organic farmland to 25 percent by 2030, providing financial incentives and technical support for farmers transitioning to organic methods. This policy framework lowers the barrier to entry for organic pea production and encourages investment in sustainable practices. Consumers perceive organic peas as safer and higher quality, willing to pay a premium for certified products. The alignment with broader sustainability goals enhances brand reputation for retailers and producers. This trend is not limited to niche markets but is becoming mainstream, driven by heightened environmental awareness. The integration of peas into crop rotation systems further supports biodiversity and reduces pest pressure, making them an attractive option for organic farmers.

MARKET RESTRAINTS

Volatility In Weather Patterns and Climate Change Impacts

The increasing volatility of weather patterns and the adverse effects of climate change on crop yields and quality impede the growth of the Europe peas market. Peas are sensitive to extreme temperatures, particularly during flowering and pod filling stages, where heat stress can lead to reduced seed set and lower productivity. According to the European Environment Agency, the frequency of heatwaves and droughts in major producing regions such as France and Germany has increased, posing a serious threat to stable production levels. Unpredictable rainfall patterns can also cause waterlogging or drought stress, affecting root development and nutrient uptake. These climatic disruptions lead to yield variability, making it difficult for processors to secure consistent volumes of raw material at stable prices. Farmers may hesitate to expand pea acreage if the risk of crop failure remains high, limiting supply growth. Adaptation measures such as irrigation infrastructure are costly and not always feasible for all growers. The changing climate may also alter the geographic suitability of traditional pea growing areas, requiring shifts in production zones. This environmental uncertainty adds complexity to supply chain planning and contract negotiations. The reliability of the European pea supply could be compromised without effective mitigation strategies. This would negatively impact downstream industries reliant on steady inputs.

Limited Processing Infrastructure and Supply Chain Bottlenecks

The limited availability of specialized processing infrastructure for peas hinders the expansion of the Europe peas market. This shortage especially impacts the production of value-added products like protein isolates and textured concentrates. While basic cleaning and freezing facilities are widespread, advanced extraction plants required for high-purity pea protein are concentrated in a few locations, creating logistical bottlenecks. According to a study, the capacity for pea protein processing in Europe lags behind the growing demand, forcing some manufacturers to rely on imports from North America or China. This dependency increases transportation costs and carbon footprints, contradicting sustainability goals. Small and medium-sized farmers often lack direct access to processing facilities, relying on intermediaries who may offer lower prices. The seasonal nature of pea harvests requires processors to operate at high capacity for short periods, leading to inefficiencies and higher operational costs. Investment in new processing plants is capital intensive and requires long lead times, slowing down the response to market opportunities. Regulatory approvals for new facilities can also be time-consuming, further delaying expansion. These infrastructure gaps limit the ability of the European market to fully capitalize on the booming plant-based protein trend. Addressing these bottlenecks requires coordinated investment and policy support to build a robust domestic processing network.

MARKET OPPORTUNITIES

Development Of Novel Pea-Based Ingredients And Functional Foods

The development of novel pea-based ingredients and functional foods offers a significant opportunity for the Europe peas market. This allows the market to diversify its applications and capture higher-value segments. Innovations in food technology are enabling the creation of pea starch, fiber, and protein fractions with specific functional properties such as emulsification, gelation, and foaming. According to research, the global market for plant-based ingredients is expanding rapidly, with pea-derived components gaining traction in bakery, confectionery, and beverage applications. These ingredients allow manufacturers to create clean-label products with improved nutritional profiles, appealing to health-conscious consumers. Pea fiber, for instance, is used to enhance texture and satiety in low-calorie foods, while pea starch serves as a gluten-free alternative in baking. Collaborations between research institutions and food companies are accelerating the commercialization of these innovative ingredients. The versatility of pea components allows for customization to meet specific technical requirements of different food categories. This diversification reduces reliance on traditional bulk markets and opens new revenue streams for processors. The growing interest in personalized nutrition further supports the development of tailored pea-based solutions. The market can leverage scientific advancements. This allows them to transform peas from a commodity crop into a high-value functional ingredient.

Integration Into Regenerative Agriculture And Crop Rotation Systems

Integrating peas into regenerative agriculture and crop rotation systems creates new pathways for the Europe peas market. This practice significantly enhances sustainability and soil health. Peas play a crucial role in breaking disease cycles and improving soil structure, making them an ideal companion crop for cereals and oilseeds. As per research frameworks managed by the European Commission, prioritizing nitrogen-fixing legumes within regular crop rotations directly supports the EU Green Deal's macro-goals of reducing synthetic fertilizer application while optimizing long-term soil health. This agronomic benefit encourages conventional farmers to adopt pea cultivation, expanding the total production base. Policy incentives under the Common Agricultural Policy reward farmers for implementing sustainable practices, providing financial support for pea production. The environmental credentials of peas align with corporate sustainability targets, attracting investment from food companies committed to net zero goals. Marketing campaigns highlighting the ecological benefits of pea farming resonate with environmentally aware consumers, enhancing brand loyalty. The potential for carbon farming credits further adds value to pea cultivation, offering additional income streams for farmers. This holistic approach positions peas as a cornerstone of sustainable European agriculture. The industry can secure its long-term viability by promoting regenerative practices. Doing so will also contribute significantly to climate change mitigation.

MARKET CHALLENGES

Labor Shortages and Mechanization Challenges in Harvesting

Labor shortages and the technical difficulties associated with mechanizing the harvesting of certain pea varieties, particularly those intended for fresh consumption, inhibit the growth of the Europe peas market. While dry peas are easily harvested with combine harvesters, fresh peas require precise timing and gentle handling to prevent damage, often necessitating manual labor or specialized machinery that is not widely available. According to the European Agricultural Machinery Industry Association (CEMA), the industrial farm equipment sector addresses broader farm labor deficits by prioritizing high-tech automation, specialized crop harvesters, and smart-farming robotic machinery to control operational overhead. The high cost of developing and deploying automated harvesting robots remains a barrier for many farmers, especially smaller holdings. Delays in harvesting due to labor constraints can lead to overmaturity and quality degradation, reducing market value. The reliance on seasonal migrant labor introduces uncertainty due to changing immigration policies and post-pandemic restrictions. These operational challenges constrain supply growth and increase price volatility. Investing in mechanization solutions requires significant capital and research, which may not be feasible for all producers. Without adequate technological advancements and workforce support, the fresh pea segment may struggle to meet rising demand. Addressing this issue is essential for maintaining the competitiveness of European pea production.

Price Competition from Global Imports and Substitute Proteins

Global imports and substitute protein sources are creating intense competition in the Europe peas market. As a result, this environment puts heavy downward pressure on both prices and market share. Cheap imports of dry peas from Canada and Russia often undercut domestic producers, making it difficult for European farmers to compete on price alone. As per the European Commission, the European market relies heavily on substantial annual volumes of imported plant proteins, which actively influence domestic commodity pricing baselines and local farm gate dynamics. Additionally, the rise of other plant-based proteins such as soy, lentils, and chickpeas provides consumers with alternative options, fragmenting demand. Soy protein, in particular, benefits from established supply chains and lower production costs, posing a formidable challenge to pea protein adoption. Price sensitivity among consumers and manufacturers leads to switching behavior when pea prices rise due to poor harvests or high input costs. The lack of strong branding for generic peas makes it difficult to differentiate them from imported counterparts. To remain competitive, European producers must focus on quality, sustainability, and local provenance, but these attributes do not always justify higher prices in commoditized markets. Overcoming this price disparity requires strategic differentiation and value addition. The global nature of the pulse market means that European producers must constantly adapt to international supply and demand fluctuations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Category, Type of Peas, Application, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Blue Lake Milling, Grain Millers, Inc., Greenyard, Morning Foods Ltd., Bonduelle, Ardo, General Mills, Inc., Avena Foods Limited, Richardson International Limited, Cerealto Siro Foods, Premier Nutrition Company, LLC, Nestlé SA, Molino Spadoni S.p.A., Weetabix, Valsemøllen, Grillon D'Or, Clif Bar & Company, Associated British Foods plc, Danone SA, and Others. |

SEGMENTAL ANALYSIS

By Category Insights

In 2025, the inorganic peas segment held the majority share of the Europe peas market because of its lower production costs and well-established supply chains that ensure consistent availability and affordability for mass-market consumers. Conventional farming methods utilize synthetic fertilizers and pesticides to maximize yields and protect crops from pests, resulting in higher productivity per hectare compared to organic systems. According to Eurostat, conventional agriculture still accounts for over 90 percent of total arable land use in the European Union, reflecting the entrenched nature of standard farming practices. This scale allows producers to offer competitive pricing, making inorganic peas accessible to a broad demographic including price-sensitive households and institutional buyers. The existing infrastructure for cleaning, drying, and processing conventional peas is extensive and optimized for high-volume throughput. Retailers prioritize inorganic peas for their private label ranges because they offer better margins and stable supply volumes. Industrial users such as animal feed manufacturers and protein extractors prefer inorganic peas due to their lower input costs and standardized quality parameters. The familiarity of consumers with conventional produce also supports steady demand, as many shoppers do not perceive a significant difference in taste or nutritional value sufficient to justify the premium for organic options. This economic advantage ensures that inorganic peas remain the default choice for the majority of applications across the continent.

The inorganic segment was spearheaded by the high yield stability provided by modern agronomic inputs, which is crucial for meeting the large-scale demands of industrial and commercial sectors. Synthetic nutrients and crop protection products help mitigate the risks associated with weather variability and pest outbreaks, ensuring predictable harvest volumes year after year. As per the Food and Agriculture Organization (FAO), conventional field pea cultivation patterns in Europe provide higher average regional yield security and lower volume volatility per hectare than corresponding organic systems. This reliability is essential for food processors and manufacturers who require consistent raw material supplies to maintain production schedules and fulfill contracts. The ability to secure large quantities of peas at stable prices allows companies to plan long-term strategies and invest in capacity expansion. Inorganic peas are also preferred for certain processed applications where uniformity in size and color is critical, as conventional breeding and growing techniques can be more precisely controlled. The widespread adoption of high-yielding varieties in conventional farming further enhances productivity. This operational efficiency makes inorganic peas the backbone of the European pulse industry, supporting everything from frozen vegetable packs to livestock feed formulations. The focus on volume and consistency cements the leadership of the inorganic category.

The organic peas segment is anticipated to witness the fastest CAGR of 8.5% between 2026 and 2034 owing to rising consumer health consciousness and increasing awareness of the environmental impacts of conventional agriculture. Shoppers are actively seeking food products free from synthetic pesticide residues and genetically modified organisms, viewing organic peas as a safer and more natural option. According to the Research Institute of Organic Agriculture (FiBL), the European organic food segment is sustaining progressive year-over-year revenue growth, with plant-based organic pulses and shelf-stable legumes capturing key retail expansion niches. Parents are particularly inclined to purchase organic peas for children due to concerns about chemical exposure. The perception of organic farming as beneficial for biodiversity and soil health resonates with environmentally conscious consumers who want to support sustainable agricultural practices. Retailers are responding by expanding their organic assortments and promoting pea-based products through sustainability-focused marketing campaigns. The alignment with clean label trends encourages food manufacturers to source organic peas for premium product lines. This shift in consumer values is not transient but represents a structural change in purchasing behavior. The willingness to pay a premium for certified organic products supports higher margins for farmers and retailers. This demand driver ensures sustained and rapid expansion of the organic pea segment.

The rapid growth of the organic peas segment is accelerated by supportive government policies and financial subsidies that encourage farmers to convert to organic production methods. The European Union’s Farm to Fork Strategy aims to increase the share of organic farmland to 25 percent by 2030, providing direct payments and technical assistance to farmers making the transition. According to the European Commission, billions of euros have been allocated through the Common Agricultural Policy to support organic farming initiatives, reducing the financial risk for growers. These incentives make organic pea cultivation more economically viable, attracting new entrants and encouraging existing farmers to expand their organic acreage. National governments in countries like France and Germany have implemented additional measures to boost domestic organic production, including research funding and market development programs. The regulatory framework for organic certification provides a clear and trusted standard that builds consumer confidence. As more farmers adopt organic practices, the supply of organic peas increases, improving availability and potentially lowering prices through economies of scale. This policy-driven support creates a favorable environment for market expansion. The combination of financial incentives and regulatory clarity ensures that the organic segment continues to outpace conventional growth rates.

By Type of Peas Insights

The green peas segment was the largest in the Europe peas market and occupied a commanding share in 2025. This supremacy of the segment was credited to its deep-rooted culinary tradition and strong consumer preference for their sweet flavor and vibrant color. Green peas are a staple ingredient in many European dishes, from soups and stews to side dishes and salads, making them a familiar and accepted food item across all age groups. According to the CBI Ministry of Foreign Affairs, consumer food preferences heavily lean toward green sweet pea varieties, establishing them as a core staple within European vegetable markets across both frozen and canned formats. Consumers associate green peas with freshness and nutrition, often choosing them over yellow peas for immediate consumption. The visual appeal of bright green peas enhances the presentation of meals, driving demand in the food service sector. Retailers stock a wide variety of green pea products, including fresh pods, frozen kernels, and canned varieties, catering to diverse consumer needs. The versatility of green peas allows them to be used in both traditional and modern recipes, maintaining their relevance in contemporary cuisine. Marketing efforts often highlight the natural sweetness and tender texture of green peas, reinforcing their positive image. This cultural and sensory preference ensures that green peas remain the dominant type in the European market.

The dominance of the green peas segment is further supported by extensive processing infrastructure dedicated to freezing and canning, which preserves quality and extends shelf life. The European frozen vegetable industry relies heavily on green peas as a core product, with major processors investing in advanced blanching and quick-freezing technologies to lock in nutrients and flavor. According to the European Frozen Food Federation, peas are one of the top three frozen vegetables sold in Europe, with green varieties leading in volume. This industrial capacity ensures year-round availability, smoothing out seasonal fluctuations in fresh supply. Canned green peas also contribute significantly to the segment, offering a convenient and affordable option for households and institutions. The established supply chains for green peas enable efficient distribution to retail outlets across the continent. Processors have optimized their operations for green peas, achieving high efficiency and low waste rates. This logistical advantage makes green peas a reliable and cost-effective choice for retailers and food manufacturers. The ability to deliver consistent quality through processed formats sustains the leadership of green peas in the market.

The yellow peas segment is likely to experience the fastest CAGR of 9.2% during the forecast period owing to the surging demand for plant-based protein isolates used in meat alternatives and functional foods. Yellow peas are preferred for protein extraction due to their high protein content, neutral flavor, and excellent functional properties such as solubility and emulsification. According to a study, the global pea protein market is expanding rapidly, with yellow peas serving as the primary raw material for most European protein manufacturers. Food technology companies are increasingly utilizing yellow pea protein to create textured vegetable proteins for burgers, sausages, and dairy-free cheeses. The neutral taste of yellow pea protein allows it to be easily incorporated into various formulations without altering the final product's flavor profile. This industrial application creates a robust and growing demand for dry yellow peas, distinct from the fresh market dynamics of green peas. Investors are pouring capital into pea protein processing facilities, further stimulating production. The alignment with vegan and vegetarian trends ensures long-term growth potential. This shift toward value-added ingredients transforms yellow peas from a commodity crop into a high-value industrial input.

The swift expansion of the yellow peas segment is also fueled by its expansion into gluten-free and specialty food applications, catering to consumers with dietary restrictions and health preferences. Yellow pea flour is gaining popularity as a nutritious alternative to wheat flour in baking, pasta, and snack production, offering higher protein and fiber content. According to sources, the gluten-free food market in Europe is growing steadily, with pea-based ingredients becoming a key component of new product launches. Manufacturers appreciate the binding and textural qualities of pea flour, which improve the quality of gluten-free baked goods. Snack brands are using roasted yellow peas to create healthy, high-protein crunchy snacks that appeal to health-conscious consumers. The versatility of yellow peas allows for innovation in diverse food categories, from breakfast cereals to energy bars. This diversification reduces dependency on traditional markets and opens new revenue streams. Consumer education about the benefits of pulse flours is driving trial and adoption. The functional advantages of yellow peas make them an attractive ingredient for food formulators. This broadening application scope ensures sustained and rapid growth for the yellow pea segment.

By Application Insights

The Food and Beverages segment led the Europe peas market and captured a significant share in 2025. Peas continue to remain a staple dietary component valued for their nutritional benefits and culinary versatility. Moreover, peas are consumed in various forms, including fresh, frozen, canned, and dried, fitting seamlessly into daily meals across European households. According to Eurostat, household expenditure on vegetables remains a significant portion of food budgets, with peas being a frequent purchase due to their affordability and nutritional value. The integration of peas into ready meals, soups, and snacks drives consistent demand from the food processing industry. Consumers appreciate peas for their high fiber and protein content, which supports digestive health and satiety. The rise of plant-based diets has further boosted the inclusion of peas in mainstream food products, from meat substitutes to dairy alternatives. Retailers dedicate substantial shelf space to pea-based products, recognizing their broad appeal. The familiarity of peas in traditional cuisines ensures steady consumption regardless of economic conditions. This foundational role in the diet secures the leadership of the Food and Beverages segment. The continuous innovation in pea-based food products keeps the category dynamic and relevant.

The top position of the Food and Beverages segment is supported by extensive industrial processing and the development of value-added pea products that cater to modern consumer needs. Food manufacturers utilize peas to create innovative ingredients such as protein isolates, starches, and fibers, which are incorporated into a wide range of processed foods. According to research, the use of pea derivatives in the food industry has grown significantly, driven by the demand for clean-label and functional ingredients. Pea protein is used to enhance the nutritional profile of beverages, bakery items, and confectionery. Pea starch serves as a thickening agent and stabilizer in sauces and dressings. These value-added applications command higher margins and create new market opportunities beyond whole peas. The ability to transform peas into specialized ingredients allows manufacturers to differentiate their products and meet specific technical requirements. This industrial utilization absorbs large volumes of pea production, stabilizing prices for growers. The focus on functionality and nutrition ensures that peas remain a key ingredient in the modern food system. This processing capability underpins the sustained leadership of the Food and Beverages segment.

The Animal Feed segment is on the rise and is expected to be the fastest-growing segment in the market with a CAGR of 7.8% from 2026 to 2034. This quick surge of the segment is propelled by sustainability goals and the need to diversify protein sources in livestock diets. The European Union is actively promoting the use of locally grown protein crops to reduce dependency on imported soybeans, which are associated with deforestation and high carbon footprints. According to the European Commission, initiatives such as the EU Protein Plan aim to increase the production and use of European protein crops, including peas, in animal feed. Peas offer a high-quality protein source for poultry, pigs, and aquaculture, with good digestibility and amino acid profiles. Farmers are increasingly incorporating peas into feed rations to improve sustainability credentials and comply with environmental regulations. The agronomic benefits of growing peas, such as nitrogen fixation, also make them an attractive option for crop rotation, indirectly supporting feed supply. Feed manufacturers are reformulating products to include higher levels of pea meal, responding to customer demand for sustainable options. This policy-driven shift creates a robust and growing market for feed-grade peas. The alignment with circular economy principles further enhances the appeal of peas in animal nutrition.

The rapid growth of the Animal Feed segment is fueled by the improved palatability and nutritional benefits of peas for livestock, which enhance animal performance and health. Peas are highly palatable to most animals, encouraging feed intake and improving growth rates. According to various sources, substituting part of the soybean meal with pea meal in pig and poultry diets does not negatively affect performance and can even improve gut health due to the fiber content. Aquaculture producers are also exploring peas as a sustainable alternative to fishmeal, reducing pressure on marine resources. The non-GMO status of European peas is a significant advantage in markets where consumers prefer non-GMO animal products. Feed mills are investing in processing technologies to optimize the nutritional value of peas, such as heat treatment to improve protein digestibility. The local availability of peas reduces transportation costs and supply chain risks compared to imported proteins. This combination of nutritional efficacy and sustainability drives adoption among feed producers and farmers. The expanding use of peas in specialized feeds for young animals and high-performance livestock further accelerates growth. This segment offers a stable and expanding outlet for pea production.

By Distribution Channel Insights

The indirect distribution segment dominated the Europe peas market and accounted for a substantial share in 2025. This dominance of the segment was driven by the extensive retail networks and wholesale infrastructure that ensure widespread availability and convenience for consumers. Supermarkets, hypermarkets, and grocery stores are the primary points of sale for peas, reaching millions of customers daily. According to Eurostat, modern retail formats account for the majority of food sales in Europe, providing efficient distribution channels for both fresh and processed peas. Wholesalers play a crucial role in aggregating supply from farmers and distributing it to retailers and food service providers, ensuring consistent stock levels. The established logistics networks allow for efficient transportation and storage, minimizing waste and maintaining quality. Consumers prefer the convenience of buying peas alongside other groceries, making indirect channels the default choice for most households. Private label brands sold through these channels offer competitive pricing and consistent quality, driving volume sales. The reach of indirect distribution extends to rural and urban areas alike, ensuring market penetration. This broad accessibility cements the leadership of the indirect channel. The efficiency of these networks supports the high volume turnover required for perishable and semi-perishable pea products.

Food service providers and industrial buyers rely on wholesalers for a consistent supply. This dependence further reinforces the dominance of the indirect distribution segment. Restaurants, cafes, and institutional caterers purchase peas in bulk through distributors who offer reliable delivery and credit terms. According to a study, the food service sector is a major consumer of frozen and canned peas, relying on indirect channels for efficient procurement. Industrial processors also source peas through intermediaries who manage quality control and logistics. These B2B relationships are built on trust and long-term contracts, ensuring stable demand for producers. Distributors provide value-added services such as inventory management and technical support, enhancing their importance in the supply chain. The complexity of serving diverse industrial clients makes indirect distribution more efficient than direct sales for many producers. This network effect creates high barriers to entry for direct competitors. The scale and efficiency of indirect distribution ensure that it remains the primary channel for moving large volumes of peas across the European market.

The Direct Distribution segment is expected to exhibit a noteworthy CAGR of 10.5% over the forecast period. This rapid growth of the segment is fuelled by the rise of e-commerce and direct-to-consumer models that bypass traditional retail intermediaries. Online grocery platforms and specialized farm-to-table websites allow consumers to purchase fresh and organic peas directly from producers or niche retailers. According to Statista, online food sales in Europe have surged in recent years, with fresh produce being a key growth category. Consumers value the transparency and traceability offered by direct channels, often willing to pay a premium for locally sourced and sustainably grown peas. Subscription boxes featuring seasonal vegetables introduce consumers to high-quality peas and build loyal customer bases. Social media marketing enables small producers to reach targeted audiences effectively, reducing marketing costs. The convenience of home delivery appeals to busy urban consumers who prioritize time-saving solutions. Direct distribution allows producers to capture higher margins by eliminating retailer markups. This model fosters a stronger connection between farmers and consumers, enhancing brand loyalty. The flexibility and personalization of direct channels drive rapid adoption and growth.

Local pea growers are benefiting from the expansion of farmers' markets and Community Supported Agriculture (CSA) schemes. Consequently, these alternative marketing channels fuel the rapid growth of the Direct Distribution segment. These platforms offer fresh, seasonal peas that are often harvested at peak ripeness, providing superior flavor and nutritional value compared to store-bought alternatives. According to surveys, participation in CSA programs has increased in Europe, with members appreciating the support for local economies and sustainable farming practices. Farmers markets provide a venue for producers to educate consumers about different pea varieties and cooking methods, driving trial and repeat purchases. The social aspect of these direct interactions builds community and trust. Consumers are increasingly interested in knowing the origin of their food and supporting small-scale agriculture. Direct sales allow farmers to receive fair prices for their produce, improving their economic viability. This grassroots movement supports the growth of direct distribution channels. The emphasis on freshness and locality resonates with modern consumer values. This trend is expected to continue as awareness of local food systems grows.

COUNTRY LEVEL ANALYSIS

France Peas Market Analysis

France was the top performer in the European peas market in 2025. It served as the leading producer and consumer of peas on the continent. The country’s diverse agricultural regions, particularly in the north and center, provide ideal conditions for pea cultivation. According to Agreste, France’s collective protein crop production, encompassing both field peas and faba beans, reached an estimated 820,000 metric tonnes in 2023, driven by an intentional expansion of agricultural land and improved average crop yields. French consumers have a strong tradition of consuming fresh and frozen peas, integrating them into classic dishes. The government supports pea production through CAP subsidies and research initiatives aimed at improving sustainability. Major food processors in France rely on domestic peas for their product lines, ensuring stable demand. The organic sector is also growing, with increasing acreage dedicated to organic pea farming. France’s strategic location facilitates exports to neighboring countries. The strong domestic market and robust processing infrastructure sustain its leadership position. Innovation in pea-based ingredients is driving new opportunities. France remains a key driver of the European pea market.

United Kingdom Peas Market Analysis

The United Kingdom followed closely behind in the Europe peas market in 2025. This standing was driven by its high per capita consumption and a strong preference for frozen peas. British consumers view peas as a staple vegetable, often served with traditional meals. According to the Department for Environment, Food and Rural Affairs, the UK produces substantial volumes of peas, primarily in East Anglia and Lincolnshire, supplying both domestic and export markets. The frozen food sector is highly developed, with major brands relying on high-quality British peas. Retailers promote peas as a healthy and affordable option, driving volume sales. The post Brexit landscape has led to adjustments in trade flows, but domestic production remains robust. Consumer interest in plant-based proteins is boosting demand for pea protein ingredients. The UK market is mature but continues to innovate with new product formats. Strong supply chains ensure consistent availability. The cultural affinity for peas sustains steady demand.

Germany Peas Market Analysis

Germany commands a notable share of the Europe peas market. This position is supported by its large population and the country's robust demand for fresh and processed peas alike. The country is a major importer of peas to supplement domestic production, which is concentrated in the northern regions. According to the Federal Office for Agriculture and Food, Germany consumes significant quantities of frozen and canned peas, with retail chains offering wide assortments. German consumers are increasingly interested in organic and sustainable pea products, driving growth in these segments. The food processing industry utilizes peas for ready meals and snacks. Government policies support sustainable agriculture and protein crop cultivation. The market is characterized by high quality standards and consumer awareness. Retailers play a key role in promoting pea-based products. Germany’s central location makes it a hub for distribution. The focus on health and convenience drives market dynamics.

Spain Peas Market Analysis

Spain is a growing player in the Europe peas market. The country’s rising production and consumption of fresh and frozen peas are fueling this growth. Moreover, the country’s favorable climate allows for early-season production, supplying European markets when other regions are offline. As per the Ministry of Agriculture, Fisheries and Food, Spain experienced a sharp 12% expansion in total pea cultivation acreage, largely incentivized by European Union agricultural eco-schemes that financially reward farmers for integrating nitrogen-fixing legumes into crop rotation cycles. Domestic consumption is rising, influenced by Mediterranean dietary patterns that include legumes. The export market is important, with Spanish peas reaching other European countries. Organic production is gaining traction, supported by consumer demand. Retailers are expanding their fresh produce sections to include more pea varieties. The food service sector is also adopting peas in modern cuisine. Spain’s strategic position enhances its role in the supply chain. Growth is driven by both domestic and export demand.

Italy Peas Market Analysis

Italy secured a considerable position in the Europe peas market. This is fuelled by a strong tradition of legume consumption and a growing interest in pea-based products. While traditionally focused on beans and lentils, Italians are increasingly incorporating peas into their diets. According to ISTAT, pea production in Italy is modest but growing, with a focus on quality and regional varieties. The food industry uses peas for soups, purees, and snacks. Consumer awareness of plant-based proteins is driving demand for pea ingredients. Retailers are introducing more pea-based products to meet this trend. Organic farming is expanding, supported by government incentives. The culinary heritage of Italy supports the integration of peas into modern dishes. The market is evolving with new product innovations. Italy’s focus on quality and tradition defines its market approach.

COMPETITIVE LANDSCAPE

The competition in the Europe peas market is characterized by a mix of large multinational food processors and regional cooperatives who vie for dominance through supply chain efficiency and product innovation. The market exhibits moderate consolidation with established players holding strong positions in specific retail channels and geographic regions. Key competitors distinguish themselves through verified sustainable sourcing practices, consistent quality, and innovative product formats rather than price alone. Barriers to entry remain significant due to high capital requirements for processing infrastructure and compliance with strict food safety regulations. Companies invest significantly in research and development to create climate-resilient varieties and improved processing techniques. Brand reputation and trust are critical assets as retailers prioritize reliable suppliers with consistent delivery records. Strategic alliances with agricultural producers enhance supply security and cost competitiveness. The competitive landscape is further shaped by the growing demand for transparency, which forces players to adopt digital traceability systems. Innovation in sustainable packaging serves as a key differentiator. Overall, the market rewards entities that can combine operational excellence with genuine commitment to environmental and social responsibility.

KEY MARKET PLAYERS

The leading companies operating in the Europe peas market include:

- Blue Lake Milling

- Grain Millers, Inc.

- Greenyard

- Morning Foods Ltd

- Bonduelle

- Ardo

- General Mills, Inc.

- Avena Foods Limited

- RICHARDSON INTERNATIONAL LIMITED

- CEREALTO SIRO FOODS

- Premier Nutrition Company, LLC

- Nestlé SA

- Molino Spadoni S.p.A.

- WEETABIX

- Valsemøllen

- Grillon D'Or

- Clif Bar & Company

- Associated British Foods plc

- DANONE SA

TOP PLAYERS IN THE MARKET

- Bonduelle operates as a leading European producer and distributor of canned and frozen vegetables with a strong focus on high-quality peas sourced from sustainable farms. The company maintains extensive partnerships with growers across France and other European regions to ensure consistent supply and premium standards. Recent actions include investing in advanced freezing technologies that preserve the natural sweetness and texture of green peas for extended periods. Bonduelle has strengthened its market position by launching organic pea ranges and eco-friendly packaging solutions to align with consumer sustainability preferences. The company actively promotes regenerative agriculture practices among its supplier network to enhance soil health and biodiversity. Their commitment to traceability allows consumers to verify the origin of their products, building trust and loyalty. Bonduelle continues to innovate with convenient ready-to-eat formats catering to busy lifestyles. This strategic focus on quality and sustainability ensures long-term competitiveness in the dynamic European vegetable sector.

- Greenyard is a major player in the European frozen food industry specializing in the processing and distribution of frozen peas and other vegetables to retail and food service sectors. The company leverages its large-scale production facilities to deliver consistent quality and volume to major supermarket chains across the continent. Recent strategic initiatives include optimizing energy efficiency in processing plants to reduce carbon footprint and operational costs. Greenyard has strengthened its position by expanding its portfolio of value-added pea products such as seasoned mixes and protein-rich blends. The company focuses on direct sourcing relationships with farmers to ensure fair prices and sustainable farming methods. Their investment in digital supply chain tools enhances transparency and operational efficiency. Greenyard actively engages in corporate social responsibility programs supporting local communities and environmental conservation. This holistic approach reinforces their reputation as a reliable and responsible partner in the European frozen food market.

- Ardo serves as a key family-owned manufacturer of frozen vegetables in Europe with a significant presence in the pea market through its high-quality processing capabilities. The company sources peas from trusted local farmers, ensuring freshness and adherence to strict quality standards. Recent actions include upgrading production lines with state-of-the-art sorting and freezing equipment to improve product consistency and reduce waste. Ardo has strengthened its market position by introducing innovative pea-based snacks and convenience meals targeting health-conscious consumers. The company emphasizes sustainable packaging initiatives, replacing traditional plastics with recyclable materials. Ardo collaborates closely with retailers to develop private label products that meet specific consumer needs. Their focus on continuous improvement and customer satisfaction drives brand loyalty and repeat purchases. Ardo’s commitment to environmental stewardship and community support distinguishes them in the competitive European frozen vegetable landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe peas market employ several strategic approaches to maintain competitiveness and drive growth amidst evolving consumer preferences and regulatory requirements. Vertical integration and direct partnerships with farmers serve as primary strategies to ensure supply chain stability and quality control. Companies invest heavily in sustainable agricultural practices, including organic certification and regenerative farming, to align with environmental goals. Innovation in processing technologies such as advanced freezing and drying methods enhances product quality and shelf life. Diversification into value-added products like protein isolates and ready-to-eat meals captures higher-margin segments. Digital transformation through traceability platforms builds consumer trust by providing transparency about origin and farming methods. Strategic collaborations with retailers facilitate private label opportunities and expanded distribution channels. Marketing campaigns emphasize health benefits and sustainability credentials to resonate with conscious consumers. These combined strategies enable participants to navigate market volatility and capitalize on emerging opportunities.

MARKET SEGMENTATION

This Europe peas market research report is segmented and sub-segmented into the following categories.

By Category

- Organic

- Inorganic

By Type of Peas

- Yellow peas

- Green peas

By Application

- Food & Beverages

- Animal Feed

- Household/Retail

By Distribution Channel

- Direct

- Indirect

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe peas market?

The Europe peas market includes the growing, processing, and selling of peas for food, feed, and ingredient uses across European countries.

How does the Europe peas market work?

The Europe peas market works through farming, processing, trade, and retail supply chains that move peas from field to end users.

What drives growth in the Europe peas market?

The Europe peas market grows from plant-based protein demand, steady fresh pea use, and expanding food and feed applications.

Which segment leads the Europe peas market?

The Europe peas market is led by food use, while feed demand and ingredient applications also play major roles.

Why are green peas important in the Europe peas market?

Green peas are important in the Europe peas market because they support demand for fresh, frozen, and processed food across Europe.

What role do dry peas play in the Europe peas market?

Dry peas support the Europe peas market through ingredient use, feed use, and long shelf-life trade flows.

How does plant-based protein affect the Europe peas market?

Plant-based protein strengthens the Europe peas market by increasing demand for pea ingredients in food and beverage production.

What is the role of feed in the Europe peas market?

Feed is a key part of the Europe peas market because field peas are used in animal nutrition and livestock rations.

Which countries matter most in the Europe peas market?

France, Spain, Romania, and other major growers matter strongly in the Europe peas market because they influence supply and trade.

What trends shape the Europe peas market?

The Europe peas market is shaped by crop yields, cultivated area changes, trade flows, and shifting demand for sustainable proteins.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com