Global Food and Agriculture Technology and Products Market Size, Share, Trends, & Growth Forecast Report By Industry (Animal, Agriculture, Cold Chain, Food & Beverage and Cannabis), Technology, And Region (North America, Europe, Asia-Pacific, Latin America, Middle East And Africa) Industry Analysis From 2026 To 2034

Global Food and Agriculture Technology and Products Market Size

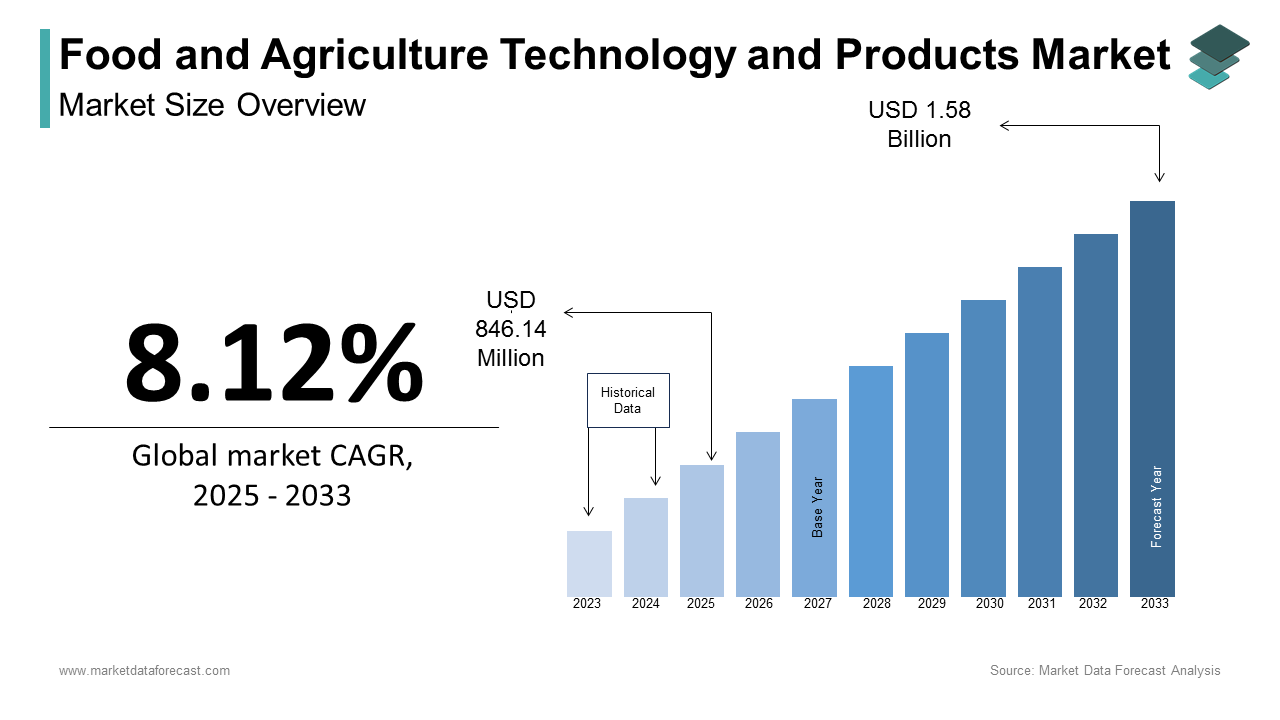

The size of the global food and agriculture technology and products market was valued at USD 846.14 million in 2025 and is expected to be worth USD 914.85 million in 2026 and grow at a CAGR of 8.12% from 2026 to 2034 to achieve USD 1.70 billion by 2034.

Food and agriculture technology and products include a broad spectrum of innovations designed to enhance the efficiency, sustainability, and productivity of agricultural practices and food supply chains. This sector integrates advanced technologies such as precision farming, biotechnology, Internet of Things sensors, and artificial intelligence into traditional agricultural processes. It also includes novel food products derived from cellular agriculture, plant-based alternatives, and fermented proteins. The primary objective is to address global food security challenges while minimizing environmental impact. According to the Food and Agriculture Organization of the United Nations, the global population is projected to reach 9.7 billion by 2050, which is demanding a 70% increase in food production. Furthermore, data from the World Resources Institute indicates that agriculture currently accounts for approximately 25% of global greenhouse gas emissions, highlighting the urgent need for sustainable technological interventions. The market is characterized by a convergence of biological sciences and digital engineering, enabling farmers to optimize resource usage, such as water and fertilizers. Consumers are increasingly demanding transparency and ethical sourcing, driving the adoption of traceability technologies. This dynamic landscape reflects a critical transition from conventional farming methods to data-driven and biologically enhanced systems that promise higher yields with reduced ecological footprints. The integration of these technologies is not merely an operational upgrade but a fundamental shift in how food is produced, processed, and consumed globally.

MARKET DRIVERS

Urgent Need for Enhanced Food Security amidst Population Growth

The imperative to secure adequate food supplies for a rapidly expanding global population is one of the key factors propelling the growth of the global food and agriculture technology and products market. Traditional farming methods are struggling to keep pace with the increasing demand for calories and nutrients, particularly in developing regions. According to the United Nations Department of Economic and Social Affairs, the world population is expected to grow by nearly 2 billion people over the next three decades, which is placing immense pressure on existing arable land. This demographic shift necessitates significant improvements in crop yields and livestock productivity without expanding agricultural land use, which contributes to deforestation. Precision agriculture technologies, such as drone-based monitoring and automated irrigation systems, enable farmers to maximize output per hectare. According to the International Food Policy Research Institute, adopting these technologies can increase crop yields by up to 30% while reducing input costs. Additionally, advancements in seed technology, including drought-resistant and pest-resistant varieties, help stabilize production in the face of climate variability. Governments and international organizations are increasingly investing in agricultural research and development to support these innovations. The drive for food security is not only about quantity but also about nutritional quality, prompting the development of biofortified crops. This comprehensive approach ensures that agricultural systems can sustain future generations while maintaining ecological balance.

Increasing Adoption of Precision Farming and Digital Solutions

The widespread adoption of precision farming and digital solutions is significantly accelerating growth in the food and agriculture technology and products market. Farmers are increasingly leveraging data analytics, satellite imagery, and Internet of Things devices to make informed decisions about planting, watering, and harvesting. This shift towards data-driven agriculture allows for precise application of inputs, reducing waste and environmental impact. According to the American Farm Bureau Federation, the use of precision agriculture technologies has grown by 15% annually in recent years, with over 80% of large-scale farms in North America and Europe utilizing some form of digital tool. These technologies enable real-time monitoring of soil health, weather conditions, and crop status, leading to optimized resource management. For instance, variable rate technology allows farmers to apply fertilizers and pesticides only where needed, reducing chemical runoff and saving costs. According to the European Commission, digital farming can reduce pesticide use by up to 20% and water consumption by 15%. Furthermore, the integration of artificial intelligence helps predict pest outbreaks and disease patterns, allowing for proactive interventions. The availability of affordable sensors and connectivity solutions has made these technologies accessible to smaller farms as well. This digital transformation enhances overall farm efficiency and profitability, driving sustained investment in agricultural technology solutions.

MARKET RESTRAINTS

High Initial Investment Costs and Financial Barriers

The high initial investment costs associated with advanced agricultural technologies pose a significant restraint to their widespread adoption, particularly among small and medium-sized farmers. Precision equipment, automated machinery, and software platforms require substantial capital outlays that many agricultural operators cannot afford without external financing. According to the World Bank, access to credit remains a major challenge for smallholder farmers in developing countries, with less than 20% having access to formal financial services. This financial barrier limits the ability of a large segment of the agricultural community to benefit from technological advancements. Even in developed nations, the return on investment for some technologies can be uncertain due to fluctuating commodity prices and weather risks. According to the United States Department of Agriculture, the average cost of implementing a comprehensive precision farming system can exceed $50,000, which is prohibitive for many family-owned farms. Additionally, the rapid pace of technological obsolescence means that investments may lose value quickly if newer, more efficient solutions emerge. Maintenance and repair costs for sophisticated equipment also add to the financial burden. Without adequate subsidies, grants, or flexible financing options, the uptake of agricultural technology will remain skewed towards large agribusinesses, exacerbating inequalities within the sector. This economic constraint hinders the potential for broad-based productivity improvements and sustainability gains.

Lack of Technical Expertise and Digital Literacy

The lack of technical expertise and digital literacy among farmers and agricultural workers is impeding the expansion of the food and agriculture technology and products market. Many traditional farmers are accustomed to conventional methods and may find it difficult to adapt to complex digital tools and data analytics platforms. According to the Organisation for Economic Co-operation and Development, a significant portion of the agricultural workforce in rural areas lacks basic digital skills, limiting their ability to utilize modern technologies effectively. This skills gap requires extensive training and support, which are often unavailable or insufficiently funded. According to the International Labour Organization, rural education levels lag behind urban areas, with fewer opportunities for vocational training in technology-related fields. Furthermore, the complexity of some agricultural software interfaces can be intimidating for users who are not tech-savvy. This reluctance to adopt new technologies is compounded by a lack of trust in data privacy and security, as farmers may be concerned about how their data is used by technology providers. Without adequate education and user-friendly designs, the potential benefits of agricultural technology remain unrealized. Bridging this knowledge gap is essential for ensuring that technological innovations are accessible and usable by all segments of the agricultural community, regardless of their background or location.

MARKET OPPORTUNITIES

Expansion of Vertical Farming and Controlled Environment Agriculture

The expansion of vertical farming and controlled environment agriculture is a lucrative opportunity for the food and agriculture technology market, particularly in urban areas. These systems allow for year-round production of crops in stacked layers, using significantly less water and land than traditional farming. According to the Association for Vertical Farming, the global vertical farming market is projected to grow at a compound annual growth rate of 25% through 2030, driven by increasing urbanization and demand for locally sourced produce. Vertical farms can be established in abandoned buildings or warehouses, reducing transportation costs and carbon emissions associated with food logistics. According to the United Nations-Habitat program, 68% of the world’s population will live in urban areas by 2050, creating a strong market for fresh, local produce. These systems also offer greater control over growing conditions, resulting in higher yields and consistent quality. Advances in LED lighting and hydroponic systems have reduced energy costs, making vertical farming more economically viable. Additionally, the ability to grow crops without pesticides appeals to health-conscious consumers. Investors are increasingly recognizing the potential of this sector, leading to increased funding for startups and established players. This trend offers significant opportunities for technology providers specializing in automation, climate control, and nutrient delivery systems.

Growth of Alternative Proteins and Cellular Agriculture

The rapid growth of alternative proteins and cellular agriculture offers substantial opportunities for the food and agriculture technology and products market. Consumers are increasingly seeking sustainable and ethical protein sources, driving demand for plant-based meats, fermented proteins, and cultivated meat. According to the Good Food Institute, global investment in alternative proteins reached $5 billion in 2024, which reflects strong investor confidence in this emerging category. Plant-based meat alternatives are becoming mainstream, with major food companies launching diverse product lines to meet consumer preferences. According to NielsenIQ, sales of plant-based foods grew by 12% in 2024, outpacing the overall food market. Cellular agriculture, which involves producing meat from animal cells in a laboratory setting, promises to reduce the environmental impact of livestock farming significantly. This technology eliminates the need for slaughter and reduces land and water usage. Regulatory approvals in key markets such as Singapore and the United States are paving the way for commercialization. As production costs decrease and scalability improves, cultivated meat is expected to become more competitive with conventional meat. This shift creates opportunities for biotechnology firms, food processors, and retailers to collaborate on new product development. The alignment of alternative proteins with sustainability goals and health trends ensures long-term growth potential.

MARKET CHALLENGES

Regulatory Uncertainty and Complex Approval Processes

Regulatory uncertainty and complex approval processes are a significant challenge to the growth of the food and agriculture technology and products market. Innovations such as genetically modified organisms, gene-edited crops, and cultivated meat face stringent regulatory scrutiny that varies widely across different jurisdictions. According to the European Food Safety Authority, the approval process for novel foods can take several years and require extensive safety assessments, delaying market entry. This regulatory fragmentation creates uncertainty for companies investing in research and development, as they must navigate differing requirements in each target market. According to the Biotechnology Innovation Organization, regulatory delays can increase development costs by up to 30%, discouraging innovation. In some regions, public skepticism and political opposition further complicate the regulatory landscape, leading to bans or restrictions on certain technologies. For instance, the European Union maintains strict regulations on genetically modified crops, limiting their cultivation and import. This inconsistency hinders global trade and collaboration, slowing the adoption of beneficial technologies. Companies must invest heavily in compliance and lobbying efforts to navigate these challenges. Until harmonized and science-based regulatory frameworks are established, the pace of innovation and market penetration will remain constrained, posing a persistent challenge to industry growth.

Consumer Skepticism and Acceptance Issues

Consumer skepticism and acceptance issues regarding new food and agriculture technologies pose a significant challenge to market expansion. Despite the potential benefits of innovations such as genetically modified organisms and cultivated meat, many consumers remain wary of their safety and ethical implications. According to a survey by the International Food Information Council, 40% of consumers express concern about the safety of genetically engineered foods, while 35% are hesitant to try cultivated meat. This skepticism is often fueled by misinformation and a lack of transparency in the food supply chain. According to Eurobarometer, trust in food safety authorities varies significantly across European countries, with lower trust levels correlating with higher resistance to new technologies. Negative media coverage and activist campaigns can further amplify consumer fears, which can lead to boycotts or demands for strict labeling. The perceived unnaturalness of some technologies also contributes to resistance, as consumers prefer familiar and traditional food sources. Overcoming these barriers requires extensive consumer education and engagement strategies to build trust and demonstrate the benefits of these innovations. Companies must prioritize transparency and communicate clearly about the science behind their products. Without broader consumer acceptance, the commercial viability of many agricultural technologies will remain limited, hindering their potential to contribute to food security and sustainability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.12% |

| Segments Covered | By Industry, Technology, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Evonik, ADM, DSM, Deere & Company, AKVA Group, United Technologies, Daikin, SGS SA, Signify Holdings, Zoetis, Pentair, GEA, Intertek, Neogen, Genus, Mosa Meat, and Others |

SEGMENTAL ANALYSIS

By Industry Insights

The smart agriculture technology segment dominated the market by capturing 26.9% of the global market share in 2025. The dominance of the smart agriculture technology segment in the global market is attributed to the urgent need to optimize resource utilization and enhance crop yields through data-driven decision-making. The seamless integration of Internet of Things devices and sophisticated data analytics platforms into daily farming operations is further contributing to the expansion of the smart agriculture technology segment in the food and agriculture technology and products market. These technologies enable precise monitoring of soil moisture, nutrient levels, and weather patterns, allowing for optimized irrigation and fertilization strategies. According to the International Telecommunication Union, the number of connected agricultural devices globally surpassed 15 million in 2024, facilitating comprehensive data collection across vast farmlands. This connectivity empowers farmers to make informed decisions that reduce waste and improve productivity. According to the Food and Agriculture Organization of the United Nations, precision irrigation systems can reduce water usage by up to 30% while maintaining or increasing crop yields. The ability to analyze historical and real-time data helps predict pest outbreaks and disease risks, enabling proactive management. Furthermore, cloud-based platforms allow for remote monitoring and control, which is particularly beneficial for large-scale operations. The scalability of these solutions makes them accessible to farms of various sizes, driving widespread adoption. As connectivity infrastructure improves in rural areas, the penetration of smart agriculture technologies continues to expand, solidifying its position as the cornerstone of modern agricultural efficiency and sustainability.

On the other side, the cultured meat products segment is estimated to record a promising CAGR of 5.5% over the forecast period owing to the advancements in cellular agriculture technology, increasing consumer demand for sustainable protein sources, and supportive regulatory developments in key markets. The significant technological advancements in cellular agriculture that are improving production efficiency and reducing costs are also supporting the growth of the cultured meat products segment in the global market. Innovations in cell line development, scaffold materials, and bioreactor design are enabling manufacturers to produce cultivated meat at scales that are increasingly commercially viable. According to the Good Food Institute, the cost of producing cultivated meat has decreased by 90% since 2020, making it more competitive with conventional meat prices. Recent breakthroughs in serum-free media formulations have further reduced production expenses while enhancing product quality and safety. According to McKinsey and Company, global investment in alternative protein technologies, including cultivated meat, reached $6.5 billion in 2024, reflecting strong confidence in the sector’s potential. Major food companies and startups are collaborating to scale up production facilities, with several pilot plants coming online in Europe and Asia. These facilities are designed to produce thousands of tons of cultivated meat annually, addressing previous concerns about supply constraints. As production processes become more streamlined and automated, the ability to meet growing consumer demand improves significantly. This technological progress is crucial for transitioning cultured meat from a niche novelty to a mainstream protein source, driving its status as the fastest-growing segment in the market.

By Technology Insights

The precision agriculture segment led the market by accounting for 36.2% of the global market share in 2025. The capability of precision agriculture to optimize resource usage and improve input efficiency, which is critical for sustainable farming practices, is majorly propelling the dominance of this segment in the global market. By utilizing technologies such as GPS-guided machinery, variable rate technology, and soil sensors, farmers can apply water, fertilizers, and pesticides only where and when they are needed. According to the American Society of Agronomy, precision agriculture techniques can reduce fertilizer use by up to 20% and pesticide application by 15% without compromising crop yields. This targeted approach not only lowers production costs but also mitigates environmental pollution caused by chemical runoff. According to the International Fertilizer Association, global fertilizer prices remained volatile in 2024, prompting farmers to adopt precision methods to maximize return on investment. Furthermore, precision irrigation systems help conserve water, a scarce resource in many agricultural regions. The United Nations Water Report highlights that agriculture accounts for 70% of global freshwater withdrawals, making efficient water management essential. Precision agriculture enables real-time monitoring of soil moisture levels, allowing for automated irrigation adjustments that prevent overwatering. These efficiency gains translate into higher profitability for farmers and reduced ecological footprints, reinforcing the widespread adoption of precision agriculture technologies across diverse cropping systems.

However, the agricultural robots segment is expected to expand at a CAGR of 35.5% over the forecast period in the global market, owing to the labor shortages in the agricultural sector and the need for automation to handle repetitive and labor-intensive tasks. The urgent need to address chronic labor shortages in the agricultural sector is also fuelling the growth of the agricultural robots segment in the global market. Aging farming populations and migration of rural workers to urban areas have created a significant gap in the availability of manual labor for planting, weeding, and harvesting. According to the International Labour Organization, the agricultural workforce in developed countries has declined by 15% over the past decade, forcing farmers to seek automated solutions. Agricultural robots, such as autonomous harvesters and weeding machines, can operate continuously and efficiently, compensating for the lack of human workers. According to the European Agricultural Machinery Industry Association, sales of agricultural robots increased by 30% in 2024, reflecting the growing reliance on automation. These robots are equipped with advanced vision systems and artificial intelligence algorithms that allow them to identify and handle crops with precision, reducing damage and waste. The ability to operate in challenging weather conditions and during extended hours further enhances their value proposition. As labor costs continue to rise, the economic case for investing in agricultural robots becomes increasingly compelling. This trend is particularly evident in high-value crops such as fruits and vegetables, where manual harvesting is both expensive and labor-intensive. The deployment of robots ensures consistent productivity and helps stabilize food supply chains amidst labor uncertainties.

REGIONAL ANALYSIS

North America Food and Agriculture Technology and Products Market

North America dominated the food and agriculture technology and products market in 2025 with 33.7% of the global market share due to the advanced technological infrastructure, high adoption rates of precision farming, and substantial investment in agricultural research and development. The United States and Canada are home to numerous leading agri-tech companies and startups that pioneer innovations in biotechnology, robotics, and digital agriculture. According to the United States Department of Agriculture, federal funding for agricultural research exceeded $4 billion in 2024, supporting the development of next-generation farming solutions. The presence of large-scale commercial farms facilitates the rapid deployment of expensive technologies such as autonomous tractors and drone-based monitoring systems. According to Statistics Canada, over 60% of Canadian farms utilize some form of precision agriculture technology, reflecting high digital literacy among farmers. Furthermore, strong regulatory frameworks that support the approval of genetically modified crops and novel food products encourage innovation and commercialization. The region also benefits from a robust venture capital ecosystem that provides ample funding for agri-tech startups. Consumer demand for sustainable and transparent food sources further drives the adoption of traceability and food safety technologies. This combination of technological readiness, financial support, and favorable policies ensures North America’s continued leadership in the global market.

Europe Food and Agriculture Technology and Products Market

Europe held the second-largest share of the food and agriculture technology and products market in 2025. The stringent environmental regulations and a strong emphasis on sustainability that drive the adoption of eco-friendly agricultural technologies are primarily driving the European market expansion. The European Union’s Farm to Fork Strategy aims to reduce the use of chemical pesticides by 50% and fertilizers by 20% by 2030, prompting farmers to adopt precision agriculture and biological alternatives. According to the European Commission, investments in sustainable agricultural technologies increased by 18% in 2024, supported by grants from the Common Agricultural Policy. Countries such as Germany, France, and the Netherlands are at the forefront of adopting smart farming solutions, including vertical farming and automated greenhouse systems. According to Eurostat, the area of organic farming in the EU expanded by 12% in 2024, driving demand for technologies that support organic production methods. Additionally, consumer awareness regarding food safety and origin is high, leading to increased adoption of traceability and blockchain technologies. The region is a hub for alternative protein innovation, with significant investments in plant-based and cultivated meat startups. Despite regulatory hurdles for certain biotechnologies, the commitment to sustainability and digital transformation ensures steady growth in the European market.

Asia Pacific Food and Agriculture Technology and Products Market

The Asia Pacific region is estimated to be the fastest-growing regional segment in the global market during the forecast period, owing to the rapid urbanization, growing population, and the need to enhance food security through technological interventions. China, India, and Japan are key contributors to market growth, driven by government initiatives to modernize agriculture and reduce reliance on imports. According to the Ministry of Agriculture and Rural Affairs of China, the country aims to achieve 70% mechanization in major crop production by 2025, driving demand for agricultural machinery and automation technologies. India’s National Mission on Sustainable Agriculture promotes the use of precision farming tools to improve water use efficiency and crop productivity. According to the Food and Agriculture Organization of the United Nations, Asia accounts for 60% of the world’s irrigated land, creating significant opportunities for smart irrigation solutions. The region is also witnessing a surge in aquaculture technology adoption, as seafood consumption rises. Japan is a leader in agricultural robotics, addressing labor shortages in its aging farming community. Additionally, the growing middle class is increasing demand for high-quality and safe food products, stimulating investments in food safety and processing technologies. These factors collectively drive the dynamic growth of the food and agriculture technology market in the Asia Pacific.

Latin America Food and Agriculture Technology and Products Market

Latin America is predicted to account for a notable share of the global market during the forecast period, owing to its role as a major exporter of agricultural commodities such as soybeans, coffee, and beef, which drives the adoption of technologies to enhance productivity and meet international standards. Brazil and Argentina are the primary markets, with large-scale farms increasingly adopting precision agriculture and biotechnology to optimize yields. According to the Brazilian Agricultural Research Corporation, the adoption of genetically modified crops in Brazil reached 95% for soybeans in 2024, reflecting high acceptance of biotechnological solutions. The region faces challenges related to deforestation and climate change, prompting efforts to implement sustainable farming practices. According to the Inter-American Development Bank, investments in climate-smart agriculture technologies in Latin America grew by 15% in 2024. Technologies such as satellite monitoring and soil sensors are used to manage large land holdings efficiently. Additionally, there is growing interest in traceability technologies to ensure compliance with export regulations and consumer demands for sustainable sourcing. The expansion of digital infrastructure in rural areas is further facilitating the adoption of smart farming solutions. These developments position Latin America as a significant and growing player in the global agri-tech landscape.

Middle East and Africa Food and Agriculture Technology and Products Market

The Middle East and Africa region is projected to showcase steady growth during the forecast period due to harsh climatic conditions, water scarcity, and the need to improve food self-sufficiency. Countries in the Gulf Cooperation Council are investing heavily in controlled environment agriculture, such as vertical farming and hydroponics, to reduce dependence on food imports. According to the Food and Agriculture Organization of the United Nations, the Middle East imports over 50% of its food requirements, driving initiatives to boost local production. The United Arab Emirates and Saudi Arabia have launched national food security strategies that prioritize technological innovation in agriculture. According to the African Development Bank, investment in agricultural technology in Africa increased by 20% in 2024, focusing on solutions for smallholder farmers. Mobile-based platforms providing weather information, market prices, and financial services are gaining traction in sub-Saharan Africa. Additionally, drought-resistant crop varieties and efficient irrigation systems are being adopted to cope with water scarcity. While the market is smaller compared to other regions, the urgent need for food security and sustainable practices creates significant opportunities for growth and innovation in agricultural technologies.

COMPETITION OVERVIEW

The Food and Agriculture Technology and Products Market features a highly competitive landscape characterized by established multinational corporations and innovative startups. Large agribusinesses leverage extensive distribution networks and substantial research budgets to dominate mainstream segments while niche players focus on specialized technologies such as vertical farming or alternative proteins. Competition intensifies as companies strive to differentiate through sustainability credentials and digital integration capabilities. Regulatory compliance varies globally, requiring firms to adapt strategies for different regional markets. Price sensitivity among farmers drives competition for cost-effective solutions that deliver measurable return on investment. Collaborative ecosystems are emerging where traditional manufacturers partner with tech companies to offer integrated smart farming solutions. Intellectual property rights play a crucial role in maintaining competitive advantages, particularly in biotechnology and seed genetics. The rapid pace of technological advancement necessitates continuous innovation to prevent obsolescence. Market participants must balance scalability with customization to meet diverse agricultural needs. This dynamic environment fosters constant evolution and strategic realignment among key industry players seeking long-term growth.

KEY MARKET PLAYERS

A few major players of the food and agriculture technology and products market include

- Evonik

- ADM

- DSM

- Deere & Company

- AKVA Group

- United Technologies

- Daikin

- SGS SA

- Signify Holdings

- Zoetis

- Pentair

- GEA

- Intertek

- Neogen

- Genus

- Mosa Meat

Top Strategies Used by the Key Market Participants

Key players in the Food and Agriculture Technology and Products Market employ strategic initiatives to maintain competitiveness and drive growth. Product innovation remains central with companies developing advanced seed precision tools and biological solutions to enhance productivity. Strategic partnerships and collaborations with technology firms enable the integration of digital platforms and data analytics into farming operations. Mergers and acquisitions allow large corporations to expand their portfolios and access new markets or technologies rapidly. Investment in research and development focuses on sustainability goals such as reducing chemical inputs and improving water efficiency. Companies also prioritize customer education and support services to facilitate the adoption of complex technologies among farmers. Expansion into emerging markets provides opportunities for growth as agricultural modernization accelerates in developing regions. These strategies collectively strengthen market positions and address global food security challenges effectively.

Leading Players in the Food and Agriculture Technology and Products Market

- Deere and Company stands as a global leader in agricultural machinery and technology with a strong focus on precision agriculture solutions. The company integrates advanced sensors, artificial intelligence, and automation into its equipment to enhance farm productivity and sustainability. Recent initiatives include the expansion of its See and Spray technology, which uses computer vision to target weeds precisely, reducing herbicide usage significantly. Deere has also invested heavily in autonomous tractor development, allowing for continuous field operations without human intervention. These innovations help farmers optimize input costs while minimizing environmental impact. By leveraging data analytics and machine learning, Deere provides actionable insights that improve decision-making processes for growers worldwide. Their commitment to smart farming technologies strengthens their position as a key enabler of modern agricultural efficiency and resource management across diverse cropping systems globally.

- Bayer AG is a prominent life science company with a significant presence in the agricultural sector through its Crop Science division. The company focuses on developing innovative seed crop protection products and digital farming solutions to address global food security challenges. Bayer recently expanded its digital agriculture platform, FieldView, which collects and analyzes field data to provide personalized recommendations for farmers. This platform helps optimize planting, fertilization, and irrigation strategies, leading to higher yields. The company also invests in biological solutions and gene editing technologies to create resilient crop varieties capable of withstanding climate stress. Bayer collaborates with startups and research institutions to accelerate innovation in sustainable agriculture. Their integrated approach, combining chemistry, biology, and digital tools, enables them to offer comprehensive solutions that support productive and environmentally responsible farming practices worldwide.

- Corteva Agriscience is a leading pure play agriculture company dedicated to providing farmers with innovative seed and crop protection solutions. The company leverages advanced breeding techniques and biotechnology to develop high-performing hybrids and traits that enhance crop productivity and resilience. Corteva recently launched new drought-tolerant corn varieties designed to maintain yields under water-scarce conditions, addressing critical climate challenges. The company also emphasizes sustainable practices by offering integrated pest management solutions that reduce chemical dependency. Corteva invests in digital tools that assist farmers in monitoring crop health and optimizing field operations. Their focus on research and development ensures a robust pipeline of novel products that meet evolving agricultural needs. By prioritizing sustainability and innovation, Corteva supports global food systems while helping farmers achieve economic stability and environmental stewardship in their operations.

MARKET SEGMENTATION

This research report on the global food and agriculture technology and products market has been segmented and sub-segmented based on industry, technology, and region.

By Industry

- Animal

- Animal Health

- Animal Genetics

- Aquaculture Products

- Agriculture

- Indoor Farming Technology

- Smart Agriculture Technology

- Pre-Harvest Equipment

- Grow Lights

- Autonomous Tractors

- Cold Chain

- Refrigerated Storage

- Refrigerated Transport

- Food & Beverage

- Algae Products

- Food Safety Technology

- Traceability Technology

- Food & Beverage Processing Equipment

- Cultured Meat Products

- Plant-Based Protein Products

- Others

- Cannabis

By Technology

- Precision Agriculture

- Digital Agriculture

- Biotechnology

- Agricultural Robots

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What are the current trends in the food and agriculture technology and products market?

Current trends include the adoption of precision agriculture, the integration of Internet of Things (IoT) and smart farming technologies, advancements in biotechnology, increasing use of drones and robotics, and the development of sustainable and organic farming practices.

2. What is the future outlook for the food and agriculture technology market?

The future outlook is promising with continuous advancements in technology, increasing investment in agri-tech startups, and growing awareness of sustainable farming practices. The market is expected to see significant growth, driven by the need to feed a growing global population efficiently and sustainably.

3. How is climate change influencing trends in agriculture technology?

Climate change is prompting the development and adoption of technologies that enhance resilience to extreme weather conditions. This includes drought-resistant crop varieties, advanced irrigation systems, and climate-smart agricultural practices that mitigate the impact of climate variability.

4. How big is the global market and what’s the growth outlook?

Estimates vary by source, but the market is substantial and growing rapidly, with projections showing it could more than double over the next decade. For example, one forecast projects growth from around USD 494.9 billion in 2024 to roughly USD 1,019 billion by 2034 at ~7.4% CAGR.

5. What technologies are driving innovation in this market?

Advanced technologies shaping the sector include Internet of Things (IoT) sensors and devices, AI and machine learning for data analysis, robotics and autonomous machines, blockchain for traceability, and big data analytics and cloud platforms

6. What role does precision agriculture play?

Precision agriculture using tools like GPS, sensors, AI, and data analytics helps optimize inputs (like water and fertilizers), improve yields, reduce waste, and lower environmental impact. It’s widely seen as a key growth driver

7. How do food safety and traceability technologies fit into the market?

Technologies that improve food safety, quality control, and traceability (e.g., blockchain tracking, automated HACCP systems) are essential to modern supply chains and help meet regulatory and consumer demands.

8. What are some real-world applications of agricultural robots and automation?

Agricultural robots and drones are used for tasks like planting, weeding, harvesting, and environmental monitoring, enhancing efficiency in labor-intensive farm operations.

9. How does this market impact sustainability and climate goals?

Adoption of technology improves efficient use of water, fertilizers, and land, reduces greenhouse gas emissions, and supports climate-smart farming practices essential for long-term food security and sustainability.

10. Who are the main end-users of these technologies and products?

End users include farmers and agricultural producers, food and beverage manufacturers, supply chain and logistics companies, government bodies and research institutions, and agribusiness cooperatives and service providers

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com