- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

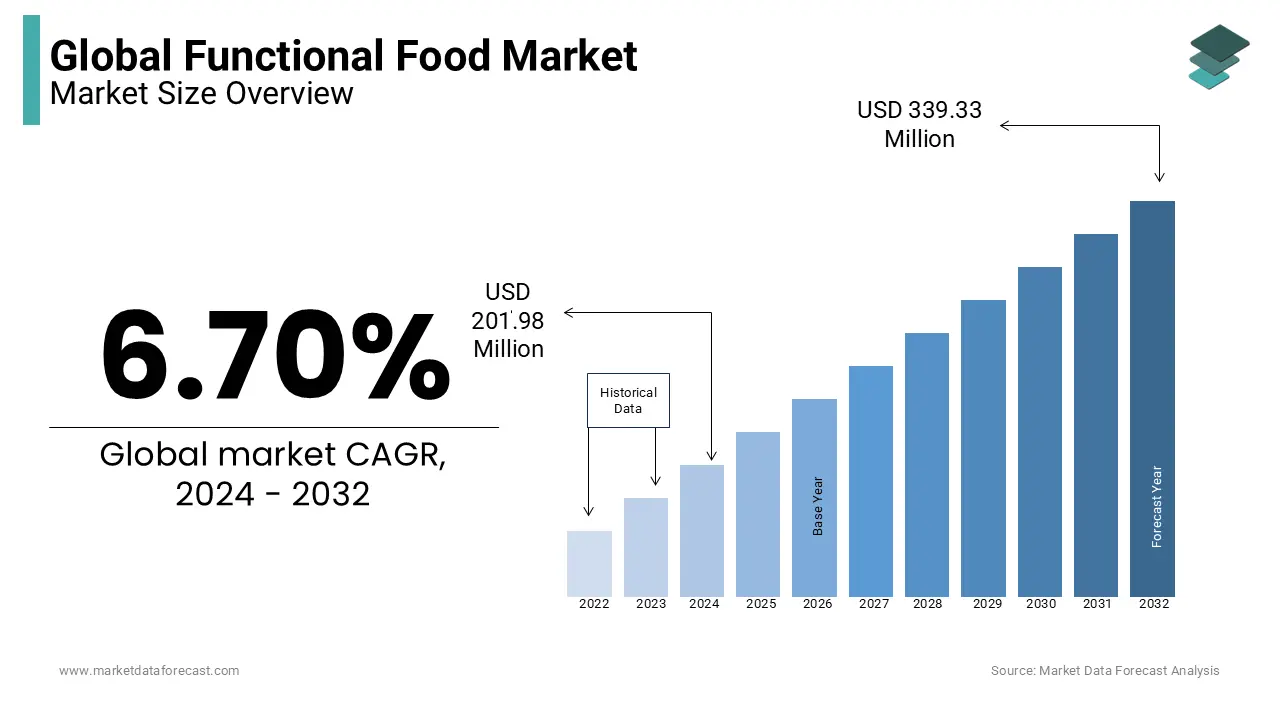

Market Size, 2025

$215.5 BnMarket Estimate, 2026

$230 BnMarket Forecast, 2034

$386.3 BnCAGR, 2026–2034

6.7%Executive Summary: Global Functional Food Market

- Market Scope: Comprehensive global functional food market analysis covering functional ingredients, product categories, application verticals, regional leadership frameworks, and consumer wellness adoption metrics.

- Market Valuation: Valued at USD 215.5 billion (2025), estimated at USD 230.0 billion (2026), and projected to reach USD 386.3 billion by 2034, registering a solid CAGR of 6.7% (2026–2034).

- Primary Growth Drivers: Shift toward preventive nutrition, rising chronic-disease prevalence, increased gut-health awareness, and high consumer demand for nutrient-dense foods. Key consumer insights include 74% of consumers believing food and beverages directly affect mental and emotional well-being, and 61% believing mental well-being influences dietary choices.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Ingredient | Prebiotics and probiotics (dominated with a 38.4% share in 2025) | Dietary fibers (forecast to grow fastest at a 9.6% CAGR through 2034) |

| By Product | Dairy products (led with a 35.2% share in 2025) | Beverages (projected to expand at a 9.2% CAGR) |

| By Application | Digestive health (captured 39.1% share in 2025) | Immunity (forecast to register the fastest 9.9% CAGR) |

| By Region | Asia Pacific (dominated with a 39.5% share in 2025) | North America (projected to record robust expansion driven by increasing health consciousness and demand for preventive nutrition) |

Major Market Players & Market Structure

Market Structure: Highly competitive global functional food landscape featuring multinational food and beverage giants competing intensely on product innovation, probiotics, adaptogens, plant-based proteins, personalized nutrition, scientific substantiation, acquisitions, digital engagement, sustainable sourcing, and direct-to-consumer channels.

Key Companies: Sanitarium Health & Wellbeing Company, Unilever, Red Bull, Royal FrieslandCampina, PepsiCo, Nestlé, Arla Foods, Kellogg Company, Danone, General Mills, Glanbia, The Coca-Cola Company, and Abbott Laboratories.

Global Functional Food Market Size

The global functional food market size was calculated to be US$ 215.51 million in 2025 and is anticipated to be worth USD 386.32 million by 2034, from USD 229.95 million in 2026, growing at a CAGR of 6.70% during the forecast period.

Functional foods are everyday foods that provide health benefits beyond basic nutrition. These items include fortified dairy, probiotic beverages, and fiber-enriched grains designed to enhance overall well-being. The sector has evolved from niche dietary supplements into a mainstream consumer category driven by heightened health consciousness. As per the WHO European Regional Obesity Report 2022, approximately 60 percent of adults in the broader WHO European Region are overweight or obese. Looking strictly at the European Union, Eurostat records show that nearly 53 percent of adults are overweight or obese. This demographic shift underscores the critical role functional foods play in public health strategies across the region. Furthermore, according to the most recent World Health Organization data (2024/2025 reporting on 2019-2021 statistics), noncommunicable diseases (NCDs) now account for 90% of deaths and 85% of years lived with disability (disease burden) in the WHO European Region. Such alarming statistics compel consumers to seek preventive measures through daily dietary choices rather than relying solely on pharmaceutical interventions post diagnosis. The integration of bioactive compounds into everyday staples allows individuals to address these health concerns proactively. Regulatory frameworks within Europe continue to adapt, with the European Food Safety Authority rigorously evaluating health claims to ensure scientific validity. This scrutiny builds consumer trust while maintaining high safety standards. The convergence of nutritional science and culinary innovation defines the current landscape, where taste and efficacy must coexist. Consumers increasingly scrutinize ingredient lists, favoring transparency and clean labels. This evolving dynamic positions functional foods as a pivotal component of modern preventive healthcare systems across diverse demographic segments in Europe.

MARKET DRIVERS

Rising Prevalence of Chronic Lifestyle Diseases Drives Preventive Dietary Shifts

The escalating incidence of chronic lifestyle diseases is a major factor driving the expansion of the functional food market. Consumers are increasingly adopting proactive health management strategies, viewing food as a preventive tool rather than merely a source of sustenance. According to the World Health Organization, cardiovascular diseases remain the leading cause of death globally, accounting for an estimated 19.8 million deaths each year. In Europe specifically, these conditions place a substantial burden on healthcare systems, prompting individuals to seek dietary alternatives that support heart health and regulate blood pressure. Foods enriched with plant sterols, omega-3 fatty acids, and soluble fibers have gained traction due to their clinically proven ability to lower cholesterol levels and improve lipid profiles. The International Diabetes Federation reports that approximately 61 million adults in the European Region were living with diabetes in 2021, a number projected to rise significantly by 2045. This surge drives demand for low glycemic index products and those containing chromium or magnesium, which aid in glucose metabolism. Additionally, the aging population in countries like Germany and Italy exhibits higher susceptibility to osteoporosis and cognitive decline. As per Eurostat, the share of people aged 65 and over in the EU population reached 21.3 percent in 2022. This demographic trend amplifies the need for calcium-fortified foods and antioxidants that support bone density and neural function. Consequently, manufacturers are innovating to deliver targeted nutritional benefits that address these specific pathological risks, thereby embedding functional foods into daily therapeutic routines for millions of Europeans seeking to mitigate long-term health complications.

Increasing Consumer Awareness and Health Consciousness Fuel Demand for Nutrient-Dense Options

Heightened consumer awareness regarding the link between diet and overall wellness significantly propels the functional food market forward. Modern shoppers are more informed and discerning, actively seeking products that offer tangible health advantages alongside convenience. As per the annual Food and Health Survey conducted by the International Food Information Council, 74 percent of consumers agree that what they eat and drink has a direct impact on their mental and emotional well-being, while 61 percent believe their mental well-being in turn dictates their dietary choices. This paradigm shift encourages the adoption of nutrient-dense foods that support immune function, gut health, and energy levels. The global pandemic further accelerated this trend, with sales of immune-boosting ingredients such as vitamin C, vitamin D, and zinc surging across retail channels. Moreover, the rise of digital health platforms and social media has democratized access to nutritional information, enabling individuals to make evidence-based dietary choices. Younger demographics, particularly Millennials and Generation Z, prioritize transparency and sustainability, often choosing functional foods that align with their ethical values. This educated consumer base demands clear labeling and scientific backing for health claims, pushing brands to invest in research and development. The resulting market dynamics favor companies that can effectively communicate the physiological benefits of their offerings, thereby fostering brand loyalty and driving repeat purchases in a competitive landscape.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Approval Processes Hinder Product Innovation

The rigorous regulatory environment is a major hindrance to the rapid expansion and innovation within the functional food market. The European Food Safety Authority maintains strict guidelines for approving health claims, requiring extensive scientific evidence to substantiate any alleged benefit. As per the European Commission, only a small fraction of submitted health claim applications receive authorization, with many rejected due to insufficient data or vague causal relationships. This high barrier to entry discourages smaller manufacturers from investing in novel functional ingredients, as the cost and time required for clinical trials and regulatory compliance are prohibitive. For instance, the approval process can take several years and cost millions of euros, limiting the diversity of products available to consumers. Furthermore, the Nutrition and Health Claims Regulation prohibits claims that suggest a food can prevent, treat, or cure a human disease, restricting marketing language and potentially confusing consumers who expect therapeutic outcomes. This regulatory caution, while ensuring safety, stifles creativity and slows the introduction of cutting-edge nutritional solutions. Companies often face uncertainty regarding the acceptability of new bioactive compounds, leading to risk aversion in product development. According to industry analyses, the complexity of navigating these regulations results in delayed market launches and reduced competitiveness against regions with more flexible frameworks. Additionally, inconsistent enforcement across member states creates fragmentation, complicating pan-European distribution strategies. Manufacturers must allocate substantial resources to legal and regulatory affairs, diverting funds from research and marketing. This bureaucratic hurdle ultimately limits the pace at which innovative functional foods reach the shelf, constraining market growth and consumer access to advanced nutritional options.

High Production Costs and Premium Pricing Limit Mass Market Accessibility

The elevated production costs associated with functional foods create a serious financial barrier that restricts widespread consumer adoption and the growth of the functional food market. Incorporating bioactive ingredients, such as probiotics, prebiotics, and specialized vitamins, requires advanced processing technologies and high-quality raw materials, which drive up manufacturing expenses. These increased costs are passed on to consumers, resulting in premium pricing that excludes price-sensitive segments of the population. In times of economic uncertainty and inflation, households prioritize essential groceries over specialized health products, reducing demand for higher-priced functional items. According to Eurostat, the inflation rate in the euro area reached record highs in recent years, eroding purchasing power and forcing consumers to trade down to cheaper alternatives. This economic pressure disproportionately affects lower-income groups, who stand to benefit most from preventive nutrition but are least able to afford it. Furthermore, the perishability of certain functional ingredients necessitates cold chain logistics, adding another layer of expense to the supply chain. Retailers may hesitate to stock these items due to lower turnover rates compared to standard goods, limiting availability in mainstream outlets. The perception of functional foods as luxury items rather than essential health tools persists, hindering mass market penetration. Manufacturers struggle to balance cost efficiency with product efficacy, often compromising on ingredient potency to maintain competitive pricing. This dynamic creates an accessibility gap, where the health benefits of functional foods remain out of reach for a significant portion of the population, thereby constraining overall market volume and growth potential.

MARKET OPPORTUNITIES

Expansion into Personalized Nutrition and Digital Health Integration Offers Growth Avenues

The emergence of personalized nutrition offers a transformative opportunity for the functional food market. This shift leverages advancements in biotechnology and digital health. Consumers are increasingly seeking tailored dietary solutions that align with their unique genetic makeup, metabolic profiles, and lifestyle habits. As per a study, the personalized nutrition market is projected to grow significantly, driven by consumer willingness to pay for customized health recommendations. Companies are integrating artificial intelligence and machine learning algorithms to analyze individual health data, enabling the creation of bespoke functional food products. For example, DNA-based testing kits allow users to identify specific nutrient deficiencies or sensitivities, guiding them toward fortified foods that address their personal needs. This level of customization enhances product efficacy and consumer satisfaction, fostering deeper brand engagement. The rise of wearable health devices further supports this trend, providing real-time data on glucose levels, sleep patterns, and activity metrics. Functional food brands can partner with tech companies to develop integrated ecosystems where dietary recommendations adjust dynamically based on user data. This synergy between food and technology creates new revenue streams and differentiates offerings in a crowded marketplace. Moreover, personalized nutrition appeals to health-conscious millennials and Gen Z consumers who value individuality and precision in their wellness routines. By moving away from one-size-fits-all approaches, manufacturers can command higher margins and build loyal customer bases. The ability to deliver targeted health outcomes through customized functional foods positions the industry at the forefront of the preventive healthcare revolution, unlocking substantial growth potential in the digital age.

Innovation in Plant-Based and Sustainable Functional Ingredients Attracts Eco-Conscious Consumers

The growing demand for sustainable and plant-based functional ingredients provides a lucrative opening for the expansion of the functional food market. This helps to align with broader environmental and ethical consumer trends. As per the Good Food Institute Europe, sales of plant-based foods in Europe have surged, with consumers increasingly prioritizing products that minimize ecological footprints. Functional foods derived from algae, fungi, and legumes offer rich sources of protein, fiber, and antioxidants while requiring fewer natural resources to produce than animal-based alternatives. Innovations in fermentation technology enable the creation of novel bioactive compounds from plant sources, enhancing their nutritional profile and functional benefits. For instance, pea protein fortified with iron and vitamin B12 addresses common deficiencies in vegan diets, appealing to an expanding segment of flexitarian consumers. According to data from ProVeg International, the number of vegans in Europe doubled from 1.3 million to 2.6 million (about 3.2% of the population). Concurrently, broader consumer transitions have expanded the total addressable plant-forward market, inclusive of vegetarians, pescatarians, and flexitarians, to represent nearly 40% of all European consumers, driving a substantial spike in mainstream functional food demand. Manufacturers are also focusing on upcycled ingredients, such as fruit pomace and grain bran, to reduce food waste and create value-added functional products. This circular economy approach resonates with environmentally conscious shoppers who seek transparency and sustainability in their purchases. Additionally, clean label trends favor natural preservatives and colorants derived from plants, replacing synthetic additives with healthier alternatives. The integration of these sustainable practices not only meets regulatory expectations but also enhances brand reputation and consumer trust. By capitalizing on the intersection of health and sustainability, companies can differentiate their offerings and capture market share among ethically driven demographics. This strategic alignment with global sustainability goals ensures long-term viability and growth in an increasingly eco-aware marketplace.

MARKET CHALLENGES

Scientific Substantiation and Consumer Skepticism Challenge Credibility and Trust

The persistent gap between scientific evidence and consumer understanding is a major challenge to the functional food market. This fuels skepticism and undermines trust. Despite rigorous regulatory oversight, many consumers remain confused about the actual benefits of functional ingredients, often perceiving health claims as marketing hype rather than factual information. As per a study published in the British Medical Journal, public trust in nutritional science has fluctuated due to conflicting dietary advice and high-profile retractions of previous health recommendations. This uncertainty leads to hesitation in purchasing functional foods, particularly among older demographics who are most in need of preventive nutrition. Manufacturers struggle to communicate complex biological mechanisms in simple, accessible language, resulting in misinterpretation or dismissal of product benefits. Furthermore, the proliferation of unverified health claims on social media exacerbates misinformation, making it difficult for consumers to distinguish between evidence-based products and pseudoscientific trends. According to data backed by BEUC and the European Public Health Association (EUPHA), front-of-pack labels are highly popular, with 60% to 70% of consumers reporting high levels of attention to them. Rather than doubting accuracy, consumer associations and public surveys strongly favor making evaluative, graded labels mandatory across the EU to simplify quick, health-conscious retail purchasing. This lack of confidence hinders adoption rates and limits market penetration. Companies must invest heavily in educational campaigns and third-party certifications to bridge this knowledge gap, yet these efforts often yield slow returns. The challenge is compounded by the variability in individual responses to functional ingredients, meaning that a product effective for one person may not work for another. This inconsistency reinforces skepticism and reduces perceived value. The functional foods industry faces ongoing difficulties in establishing credibility. This struggle continues because the sector lacks clear, transparent, and universally understood communication strategies to convince consumers of its genuine health advantages.

Supply Chain Volatility and Raw Material Sourcing Instability Impact Production Consistency

Supply chain volatility and the instability of raw material sourcing are impeding the expansion of the functional food market. This disrupts production consistency and increases operational risks. Many functional ingredients, such as specific probiotics, exotic botanicals, and marine-derived omega-3s, are sourced from limited geographic regions or specialized suppliers, making them vulnerable to climate change, political instability, and logistical disruptions. As per the Food and Agriculture Organization of the United Nations, extreme weather events have increasingly affected agricultural yields, leading to fluctuations in the availability and price of key raw materials. For instance, droughts in major producing regions can drastically reduce the harvest of crops like chia seeds or turmeric, essential for many functional formulations. This scarcity forces manufacturers to seek alternative suppliers, often at higher costs or with varying quality standards, compromising product uniformity. Additionally, geopolitical tensions and trade restrictions can interrupt the flow of imported ingredients, causing delays and shortages. According to sources, the global supply chain crisis experienced in recent years highlighted the fragility of just-in-time inventory models, prompting companies to reassess their sourcing strategies. However, building resilient supply chains requires significant investment in storage infrastructure and diversified supplier networks, which may be prohibitive for smaller firms. The perishable nature of many bioactive compounds further complicates logistics, requiring precise temperature control and rapid transportation to maintain potency. Any deviation in these conditions can render ingredients ineffective, leading to product recalls and reputational damage. These systemic vulnerabilities create uncertainty in production planning and pricing, ultimately affecting market stability and consumer confidence in the reliability of functional food products.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.70% |

| Segments Covered | By Ingredients, Application, Product, And Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Sanitarium Health & Wellbeing Company, Unilever, Red Bull GmbH, Royal FrieslandCampina, PepsiCo Inc, Raisio Group, Nestlé, Arla Foods, Ocean Spray Cranberries Inc, Meiji Group, Murray Goulburn, Kraft Foods Inc, Mars Inc, Kellogg Company, Kirin Holdings, GlaxoSmithKline Company, Danone, General Mills Inc, Glanbia Plc, Dean Foods, Dr. Pepper Snapple Group, BNL Food Group, The Coca-Cola Company, and Abbott Laboratories |

SEGMENTAL ANALYSIS

By Ingredients Insights

The prebiotics and probiotics segment dominated the functional food market and accounted for a 38.4% share in 2025. This dominance of the segment was driven by the escalating scientific understanding of the gut microbiome's role in overall health. Consumers are increasingly aware that a balanced gut flora is essential for digestion, immunity, and even mental well-being. Consumer data evaluated by global ingredient networks shows that while over 80% of individuals recognize the word probiotics, peer-reviewed research tracked by healthcare platforms indicates that only 21.9% of consumers self-report a high level of functional awareness regarding specific digestive and immune system applications. This widespread recognition drives consistent demand for yogurt, kefir, and fortified beverages containing live cultures. The World Gastroenterology Organisation highlights that probiotics are effective in managing conditions such as irritable bowel syndrome and antibiotic-associated diarrhea, further validating their therapeutic potential. Consequently, healthcare professionals frequently recommend these ingredients, reinforcing consumer trust. The integration of probiotics into everyday foods like cereals and snacks has expanded accessibility beyond traditional dairy products. The versatility of these ingredients allows manufacturers to innovate across various product categories, ensuring sustained market presence. Furthermore, the rise of synbiotics, which combine prebiotics and probiotics, offers enhanced efficacy, appealing to health-conscious consumers seeking comprehensive gut support. This scientific backing and broad application scope solidify the dominance of this segment in the functional food landscape.

The domination of the prebiotics and probiotics segment is further reinforced by emerging research linking gut health to immune function and mental health, known as the gut-brain axis. Consumers are increasingly seeking functional foods that offer holistic health benefits beyond simple digestion. As per the National Institutes of Health, studies have shown that specific probiotic strains can modulate the immune response, reducing the severity and duration of respiratory infections. This finding has spurred demand for immune-boosting products, particularly in the post-pandemic era, where health prevention is a priority. Additionally, the connection between gut bacteria and mood regulation has gained significant attention. Research published in Nature Reviews Gastroenterology and Hepatology indicates that certain probiotics can alleviate symptoms of anxiety and depression, opening new avenues for functional food applications in mental wellness. This expanding scope attracts a broader demographic, including younger consumers interested in mental health optimization. The European Food Safety Authority continues to evaluate new health claims related to immune and psychological benefits, providing a regulatory pathway for innovation. This diversification into high-value health areas ensures that prebiotics and probiotics remain at the forefront of the functional food industry, maintaining their leading market position through continuous innovation and expanded health narratives.

However, the dietary fibers segment is estimated to register the fastest CAGR of 9.6% from 2026 to 2034 due to the increasing prevalence of metabolic disorders and the need for effective diabetes management. Dietary fibers play a crucial role in regulating blood sugar levels and improving insulin sensitivity, making them essential for individuals with or at risk of type 2 diabetes. As per the International Diabetes Federation, the number of adults living with diabetes worldwide is expected to rise to 783 million by 2045, creating a substantial demand for low glycemic index foods enriched with soluble fibers. Ingredients such as inulin, beta-glucan, and resistant starch are widely incorporated into bakery products, beverages, and snacks to help control postprandial glucose spikes. The American Diabetes Association recommends a high fiber diet as part of medical nutrition therapy for diabetes, reinforcing consumer adoption. Furthermore, dietary fibers contribute to satiety, aiding in weight management, which is closely linked to metabolic health. According to the World Health Organization, obesity rates have nearly tripled since 1975, prompting governments and health organizations to promote fiber-rich diets as a preventive measure. This public health focus accelerates the integration of fiber into mainstream food products. Manufacturers are innovating with clean-label fiber sources to meet consumer preferences for natural ingredients. The combination of regulatory support, clinical evidence, and rising disease prevalence ensures that the dietary fibers segment experiences rapid growth, outpacing other ingredient categories in the functional food market.

A further key factor propelling the rapid growth of the dietary fibers segment is the strong consumer demand for solutions that promote digestive regularity and cardiovascular health. Constipation and other digestive issues affect a significant portion of the global population, driving the search for natural remedies through diet. As per the World Gastroenterology Organisation, dietary fiber is the first line of treatment for chronic constipation, leading to increased consumption of fiber-fortified foods. Soluble fibers, in particular, have been proven to lower low-density lipoprotein cholesterol levels, reducing the risk of heart disease. The American Heart Association recommends consuming 25 to 30 grams of fiber daily from food sources to maintain heart health, yet most consumers fall short of this target. This gap presents a significant opportunity for functional food manufacturers to bridge the deficiency through fortified products. According to a survey by the International Food Information Council, over 60 percent of consumers actively seek out foods with added fiber for digestive and heart health benefits. The versatility of fiber ingredients allows for easy integration into a wide range of products, from breakfast cereals to plant-based meat alternatives. Innovations in texture and taste have improved the sensory profile of high fiber foods, overcoming previous barriers to adoption. As consumers become more educated about the multifaceted benefits of fiber, the demand for these functional ingredients continues to surge, driving the segment's exceptional growth rate in the global market.

By Product Insights

The dairy products segment led the functional food market and captured a 35.2% share in 2025. This leading position of the segment was attributed to entrenched consumer habits and the inherent versatility of dairy matrices for fortification. Milk, yogurt, and cheese are staple items in many diets, providing a familiar and trusted vehicle for delivering functional ingredients such as calcium, vitamin D, and probiotics. As per the Food and Agriculture Organization of the United Nations, milk is consumed by billions of people globally, establishing a massive baseline audience for functional dairy innovations. The natural nutrient profile of dairy, rich in protein and minerals, complements added functional components, enhancing overall nutritional value without compromising taste or texture. Yogurt, in particular, has become synonymous with gut health, driven by the widespread acceptance of probiotic cultures. According to Danone, a major player in the industry, functional dairy products account for a significant portion of their global sales, reflecting strong consumer preference. The ease of incorporating vitamins and minerals into liquid and semi-solid dairy products allows manufacturers to address specific health concerns, such as bone health and immune support, efficiently. Regulatory approvals for health claims related to calcium and vitamin D in dairy further bolster consumer confidence. The established supply chain and distribution networks for dairy ensure wide availability, making functional dairy accessible to diverse demographic groups. This combination of familiarity, nutritional synergy, and logistical efficiency sustains the dominance of the dairy segment in the functional food market.

The continued spearheading of this segment is supported by continuous innovation in protein enrichment and the expansion of lactose-free options, catering to evolving consumer needs. The growing fitness culture and awareness of protein's role in muscle maintenance and satiety have driven demand for high-protein dairy products. Manufacturers are utilizing ultra-filtration technologies to increase protein content while reducing sugar, appealing to health-conscious consumers and athletes. Additionally, the prevalence of lactose intolerance, affecting approximately 68 percent of the global population as per the National Institutes of Health, has spurred the development of lactose-free functional dairy products. These products retain the nutritional benefits of dairy while eliminating digestive discomfort, expanding the market reach. The introduction of A2 beta casein milk, which is easier to digest for some individuals, represents another innovation driving growth. According to various studies, the global market for lactose-free products is expanding rapidly, with dairy companies investing heavily in this niche. The ability to combine functional benefits such as probiotics and vitamins with lactose-free and high-protein formulations creates a compelling value proposition. This adaptability allows the dairy segment to remain relevant and competitive, addressing both traditional health concerns and modern dietary preferences, thereby maintaining its leading status in the functional food industry.

On the other hand, the beverages segment is anticipated to witness the fastest CAGR of 9.2% during the forecast period, owing to the surging demand for convenient functional hydration and energy solutions. Modern lifestyles characterized by busy schedules and on-the-go consumption patterns favor ready-to-drink formats that deliver health benefits instantly. Energy drinks fortified with vitamins, amino acids, and natural caffeine sources are gaining popularity among young professionals and students seeking sustained mental focus and physical energy. Additionally, hydration beverages enriched with electrolytes and minerals cater to active individuals and athletes, supporting performance and recovery. The convenience of liquid formats allows for rapid absorption of nutrients, enhancing perceived efficacy. The innovation in flavor profiles and natural sweeteners has improved the taste appeal of functional beverages, attracting a broader audience. Brands are leveraging digital marketing to highlight the immediate benefits of these products, resonating with health-conscious millennials and Gen Z consumers. The low barrier to entry for new brands in the beverage sector fosters intense competition and rapid innovation, further accelerating market growth. This dynamic environment ensures that the beverages segment remains the fastest-growing category in the functional food market.

This fast-growing segment is pushed forward by the integration of adaptogens and plant-based ingredients, aligning with the trend towards natural and holistic wellness. Consumers are increasingly seeking beverages that offer stress relief, mental clarity, and immune support through botanical extracts such as ashwagandha, turmeric, and ginger. As per the Global Wellness Institute, the wellness economy is expanding, with consumers prioritizing mental and emotional well-being alongside physical health. Functional beverages featuring adaptogens provide a convenient way to manage stress and anxiety in daily life. The rise of plant-based diets has also fueled demand for non-dairy functional drinks, such as oat milk fortified with vitamins and almond milk with added protein. According to the Plant Based Foods Association, sales of plant-based beverages continue to rise, with functional variants capturing a growing share of the market. The combination of traditional herbal wisdom with modern food science creates unique selling propositions that differentiate these products. Regulatory bodies are increasingly recognizing the safety and efficacy of many botanical ingredients, facilitating their inclusion in commercial products. The aesthetic appeal and Instagrammable nature of these innovative beverages further drive social media engagement and consumer trial. This convergence of natural ingredients, mental health benefits, and plant-based trends positions the beverages segment for sustained rapid growth, making it the most dynamic category in the functional food market.

By Application Insights

In 2025, the digestive health segment held the majority share of 39.1% of the functional food market because of the high prevalence of gastrointestinal disorders and heightened consumer awareness of gut health. Conditions such as irritable bowel syndrome, bloating, and constipation affect a significant portion of the global population, creating a steady demand for functional solutions. As per the World Gastroenterology Organisation, functional gastrointestinal disorders are among the most common reasons for visiting primary care physicians, highlighting the widespread nature of these issues. Consumers are increasingly educated about the importance of a healthy microbiome for overall well-being, leading to proactive dietary choices. Probiotics, prebiotics, and fiber-rich foods are widely recognized for their ability to improve digestion and alleviate symptoms. According to a survey by the International Food Information Council, a majority of consumers associate gut health with overall health, driving purchases of functional foods targeting this area. The visibility of digestive health campaigns by major brands has further normalized the conversation around gut wellness, reducing stigma and encouraging open discussion. This cultural shift has expanded the market beyond those with diagnosed conditions to include health-conscious individuals seeking preventive care. The scientific validation of gut health benefits through numerous clinical studies reinforces consumer trust and loyalty. Consequently, the digestive health segment maintains its leadership position by addressing a universal and persistent health concern with effective and accessible functional food solutions.

The top position of this segment is also strengthened by the expanding research on the gut-brain axis and the broader trend towards holistic wellness. Emerging science reveals the intricate connection between gut health and mental well-being, influencing mood, cognition, and stress levels. According to research highlighted across Nature Portfolio journals, the gut-brain axis is heavily influenced by the digestive tract, where more than 90% of the body's mood-regulating serotonin is synthesized. The gut microbiome plays an indispensable role by releasing metabolic signals that regulate and prompt the host system to produce these vital neurotransmitters. This discovery has sparked interest in psychobiotics, functional foods that support both digestive and mental health. Consumers are increasingly seeking products that offer dual benefits, addressing physical and emotional well-being simultaneously. The holistic wellness movement emphasizes the interconnectivity of bodily systems, encouraging a comprehensive approach to health. According to the Global Wellness Institute, the mental wellness market is growing rapidly, with consumers integrating dietary strategies into their mental health routines. Functional foods targeting digestive health are positioned at the intersection of these trends, appealing to a wide audience. The marketing of these products often highlights their potential to reduce stress and improve mood, resonating with modern consumers facing high-pressure lifestyles. This expanded value proposition enhances the appeal of digestive health functional foods, driving repeat purchases and brand loyalty. The ongoing scientific exploration of the gut-brain connection promises further innovations, ensuring the continued leadership of the digestive health segment in the functional food market.

On the contrary, the immunity application segment is likely to experience the fastest CAGR of 9.9% between 2026 and 2034. This swift growth is fueled by heightened health consciousness following the global pandemic and a shifted focus towards preventive care. Consumers are prioritizing immune system support to protect against infections and maintain overall resilience. These nutrients are widely recognized for their role in enhancing immune function and reducing the severity of illnesses. The integration of immune-supporting ingredients into everyday foods such as juices, snacks, and dairy products makes it easier for consumers to incorporate these benefits into their daily routines. The perception of food as medicine has gained traction, with individuals seeking natural ways to strengthen their defenses. Government health initiatives promoting healthy diets for immune support further reinforce this trend. The availability of scientific evidence supporting the efficacy of specific nutrients in immune modulation builds consumer confidence. This sustained focus on prevention and protection ensures that the immunity segment continues to expand rapidly, outpacing other application areas in the functional food market.

A further significant driver of the rapid growth in the immunity segment is the innovation in bioactive ingredients and the emergence of personalized immune support solutions. Manufacturers are exploring novel ingredients such as beta-glucans, elderberry, echinacea, and mushroom extracts to create differentiated products with enhanced immune benefits. As per the Journal of Functional Foods, these bioactive compounds have demonstrated promising results in modulating immune responses and reducing inflammation. The development of synergistic blends that combine multiple immune-boosting ingredients offers comprehensive support, appealing to discerning consumers. Personalization is also gaining momentum, with brands offering products tailored to individual immune needs based on age, lifestyle, and health status. Digital health tools enable users to track their immune health and receive personalized dietary recommendations, driving engagement and loyalty. The integration of technology and nutrition creates a dynamic ecosystem that supports continuous immune optimization. The constant introduction of new and effective ingredients keeps the market vibrant and attractive to early adopters. This cycle of innovation and personalization ensures that the immunity segment remains the fastest-growing application area, capturing the attention and spending of health-conscious consumers globally.

REGIONAL ANALYSIS

North America Functional Food Market Analysis

North America followed closely behind in the global functional food market and captured a 27.4% share in 2025. This position of the regional market was supported by high consumer spending power and advanced healthcare infrastructure. The region is a leader in innovation and adoption of new functional ingredients, driven by a strong culture of health and wellness. As per the Centers for Disease Control and Prevention, chronic diseases such as heart disease and diabetes are prevalent in the United States, motivating consumers to seek preventive dietary solutions. The United States accounts for the largest share of the regional market, with Canada also showing significant growth. The presence of major functional food manufacturers and research institutions fosters a conducive environment for product development. According to the Nutrition Business Journal, the US market for functional foods and beverages continues to expand, with consumers increasingly prioritizing clean labels and transparency. The regulatory framework provided by the Food and Drug Administration ensures safety and quality, building consumer trust. The high level of health literacy among North American consumers drives demand for scientifically backed products. Additionally, the rise of e-commerce platforms facilitates easy access to a wide variety of functional foods, reaching remote areas. The region's emphasis on fitness and active lifestyles further boosts demand for sports nutrition and weight management products. With continuous innovation and strong consumer engagement, North America remains a key driver of global market growth, setting trends that influence other regions.

North America and Europe are the main markets for functional foods. Increasing consumer interest and a better understanding of the immune-boosting properties of proper diet and eating habits are some of the key factors driving the growth of vitamin and mineral-rich foods and beverages. Asia Pacific region is expected to lead the global functional foods business over the forecast period. This is due to the rate of population growth in Asian countries, coupled with the increase in disposable income and the higher consumption of processed foods. With the growing awareness of health and fitness in developing countries, the rapid consumption of processed foods is a major factor promoting the regional market. The area is characterized by growing concern for food safety among consumers, influencing consumer behavior and driving growth accordingly. Improving food is supposed to be a key approach for governments to address growing concerns about malnutrition and poverty, which will contribute significantly to industry growth.

Europe Functional Food Market Analysis

Europe holds a strong position within the global functional food market because of stringent regulatory standards and a strong tradition of healthy eating. The region is home to some of the oldest and most respected food safety authorities, ensuring high quality and credible health claims. As per the European Food Safety Authority, the approval process for health claims is rigorous, which enhances consumer confidence in functional products. Germany, France, and the United Kingdom are the largest markets within the region, driven by aging populations and the increasing prevalence of lifestyle diseases. According to Eurostat, the proportion of elderly people in Europe is rising, increasing the demand for foods that support bone health, cognitive function, and cardiovascular wellness. The European consumer is highly informed and skeptical, demanding transparency and scientific evidence for health benefits. This has led to a preference for natural and organic functional ingredients. The Mediterranean diet, rich in fruits, vegetables, and healthy fats, influences the development of functional foods in Southern Europe. In Northern Europe, there is a strong focus on fortification due to limited sunlight and vitamin D deficiency. The European Union's support for research and innovation in food technology fosters continuous product improvement. With a balanced approach to regulation and innovation, Europe maintains a stable and growing market, emphasizing quality and sustainability in functional food production.

Asia Pacific Functional Food Market Analysis

The Asia Pacific was the top performer in the functional food market and accounted for a 39.5% share in 2025. This dominance of the APAC market was driven by increasing disposable incomes, urbanization, and changing lifestyles. Countries such as China, Japan, and India are at the forefront of this growth, with a large population base and rising health awareness. As per the World Health Organization, the burden of noncommunicable diseases is increasing in the region, prompting governments and consumers to focus on preventive health measures. Japan has a mature market for functional foods, known as Foods for Specified Health Uses, which serves as a model for other countries. China is experiencing rapid growth due to the expanding middle class and increasing interest in Western-style health trends. The traditional use of herbal ingredients in Asian medicine integrates seamlessly with modern functional food concepts, creating unique product offerings. Urban consumers are increasingly adopting busy lifestyles, driving demand for convenient and healthy food options. The rise of e-commerce and digital marketing in the region facilitates wider distribution and consumer education. Government initiatives promoting healthy aging and disease prevention further support market expansion. With its vast population and economic growth, the Asia Pacific represents a significant opportunity for functional food manufacturers, poised to become a dominant force in the global market.

Latin America Functional Food Market Analysis

Latin America is an emerging region within the global functional food market due to growing health consciousness and economic stabilization. Brazil and Mexico are the largest markets in the region, driven by increasing urbanization and exposure to global health trends. As per the Pan American Health Organization, the prevalence of obesity and diabetes is rising in Latin America, creating a demand for healthier food options. Consumers are becoming more aware of the benefits of functional ingredients, particularly those derived from native plants such as acai, chia, and quinoa. According to industry reports, the functional food market in Latin America is growing steadily, with local manufacturers leveraging indigenous ingredients to create unique products. The region's rich biodiversity offers a wealth of natural functional ingredients, attracting international investment. Economic challenges and inflation can impact purchasing power, but the demand for affordable health solutions remains strong. Retail expansion and improved distribution networks are making functional foods more accessible to a broader population. The influence of North American and European trends is evident, with consumers seeking similar benefits such as weight management and digestive health. Government efforts to improve public health through nutrition education are also contributing to market growth. With its natural resources and growing consumer base, Latin America presents significant potential for expansion in the functional food sector.

Middle East and Africa Functional Food Market Analysis

The Middle East and Africa region is likely to expand significantly in the functional food market during the forecast period, with growth driven by increasing health awareness and economic development in key countries. The Gulf Cooperation Council countries, particularly Saudi Arabia and the United Arab Emirates, lead the market due to high disposable incomes and government initiatives promoting healthy lifestyles. As per the World Health Organization, the region faces high rates of diabetes and cardiovascular diseases, prompting a shift towards preventive nutrition. Consumers are increasingly interested in functional foods that address these specific health concerns. According to market analyses, the demand for halal-certified functional foods is rising, reflecting the cultural and religious preferences of the population. The African market is still in its early stages, with South Africa and Nigeria showing growth potential. Urbanization and the expansion of modern retail channels are improving access to functional products. The region's traditional use of herbs and spices provides a foundation for functional food innovation. Government investments in healthcare and nutrition programs are raising awareness about the benefits of functional diets. Challenges such as supply chain infrastructure and varying regulatory frameworks exist, but growth opportunities are significant. With increasing health consciousness and economic progress, the Middle East and Africa region is poised for steady expansion in the functional food market.

COMPETITION OVERVIEW

The competition in the functional food market is intense and characterized by rapid innovation and diverse participant types. Established multinational corporations compete alongside agile startups and private label brands, creating a dynamic landscape. Large companies leverage their extensive distribution networks and marketing budgets to dominate shelf space and consumer awareness. However, smaller entities often lead in niche categories by offering unique formulations and transparent sourcing practices. The barrier to entry is relatively low for new brands, fostering continuous disruption and variety. Competitive advantage is increasingly derived from scientific substantiation and regulatory compliance rather than just branding. Companies must navigate complex health claim regulations, which can limit marketing flexibility. Price sensitivity remains a factor, although many consumers are willing to pay premiums for verified health benefits. Collaboration between food manufacturers and healthcare providers is becoming a key differentiator. Digital engagement and personalized nutrition services are emerging as critical competitive tools. The market sees frequent mergers and acquisitions as larger firms seek to absorb innovative technologies and talent. Sustainability and ethical sourcing are no longer optional but essential for brand reputation. This multifaceted competitive environment drives constant evolution in product offerings and consumer engagement strategies, ensuring that only the most adaptable and credible brands thrive in the long term.

KEY MARKET PLAYERS

A few major players of the global functional food market include

- Sanitarium Health & Wellbeing Company

- Unilever

- Red Bull GmbH

- Royal FrieslandCampina

- PepsiCo Inc

- Raisio Group

- Nestlé

- Arla Foods

- Ocean Spray Cranberries Inc

- Meiji Group

- Murray Goulburn

- Kraft Foods Inc

- Mars Inc

- Kellogg Company

- Kirin Holdings

- GlaxoSmithKline Company

- Danone

- General Mills Inc

- Glanbia Plc

- Dean Foods

- Dr. Pepper Snapple Group

- BNL Food Group

- The Coca-Cola Company

- Abbott Laboratories

Top Strategies Used by Key Market Participants

Key players in the functional food market primarily employ product innovation and strategic acquisitions to strengthen their positions. Companies invest heavily in research and development to create novel formulations that address specific health concerns, such as immunity and digestive wellness. They frequently incorporate trending ingredients like probiotics, adaptogens, and plant-based proteins to appeal to health-conscious consumers. Mergers and acquisitions allow established firms to integrate niche brands with specialized expertise into their portfolios. This strategy expands their product range and accelerates entry into emerging subsegments. Partnerships with biotechnology firms enable access to cutting-edge scientific advancements and proprietary ingredients. Marketing efforts focus on educating consumers about the science behind functional benefits to build trust and credibility. Digital platforms are leveraged for personalized marketing and direct-to-consumer sales channels. Sustainability initiatives are increasingly central to corporate strategies as consumers prioritize ethical sourcing and environmental impact. Companies also optimize supply chains to ensure consistent quality and availability of raw materials. These combined approaches help market leaders maintain competitiveness and drive growth in a dynamic industry landscape.

Leading Players in the Functional Food Market

- General Mills Inc maintains a robust presence in the United States functional food sector through its diverse portfolio of fortified cereals and yogurt brands. The company actively innovates by integrating probiotics and prebiotic fibers into mainstream products like Yoplait and Annie’s Homegrown. Recent strategic initiatives include expanding their plant-based offerings and enhancing nutritional profiles to meet consumer demand for clean-label ingredients. General Mills invests heavily in research and development to create products that support digestive health and immune function. They have also focused on sustainable sourcing practices to appeal to environmentally conscious shoppers. By leveraging its extensive distribution network and strong brand recognition, General Mills continues to influence market trends. Their commitment to transparency and scientific validation of health claims strengthens consumer trust. The company frequently collaborates with health experts to ensure product efficacy. These efforts position General Mills as a key driver of innovation and accessibility in the functional food landscape across the nation.

- Danone North America is a pivotal player in the functional food market with a strong emphasis on gut health and plant-based nutrition. The company owns prominent brands such as Activia and Silk, which are fortified with probiotics and essential nutrients. Danone prioritizes sustainability and social responsibility, aligning with modern consumer values. Recent actions include launching new product lines featuring adaptogens and immune-boosting ingredients to address evolving health needs. They have invested in digital health platforms to provide personalized nutrition advice to consumers. Danone actively engages in educational campaigns to raise awareness about the benefits of fermented foods. Their focus on clinical research supports the scientific credibility of their health claims. The company also works closely with healthcare professionals to promote functional foods as part of preventive care. By continuously expanding its portfolio and emphasizing holistic wellness, Danone strengthens its market position. Their strategic partnerships with startups foster innovation and keep them at the forefront of industry developments.

- Kellogg Company plays a significant role in the US functional food market through its extensive range of fortified breakfast cereals and snacks. Brands like Special K and Rice Krispies are enhanced with vitamins, minerals, and fiber to support overall health. Kellogg focuses on reducing sugar content while increasing nutritional value to meet health-conscious demands. Recent strategies include acquiring emerging brands that specialize in plant-based and organic functional foods. The company invests in innovative packaging solutions to improve shelf life and convenience. Kellogg actively promotes the benefits of whole grains and dietary fiber for heart health and digestion. They collaborate with nutritionists to develop products that cater to specific dietary needs, such as gluten-free and high-protein options. Their marketing campaigns emphasize the role of breakfast in maintaining energy levels and metabolic health. Kellogg also prioritizes sustainable agriculture practices to ensure the responsible sourcing of ingredients. These initiatives help Kellogg maintain a competitive edge and resonate with health-focused consumers across the United States.

DETAILED SEGMENTATION OF THE GLOBAL FUNCTIONAL FOOD MARKET IS INCLUDED IN THIS REPORT

This research report on the global functional food market has been segmented and sub-segmented based on ingredient, product, application, & region.

By Ingredient

- Dietary Fibers

- Carotenoids

- Minerals

- Fatty Acids

- Vitamins

- Prebiotics & Probiotics

- Others

By Product

- Dairy

- Fruits & Vegetables

- Beverages

- Others

By Application

- Weight Management

- Sports Nutrition

- Digestive Health

- Immunity

- Cardio Health

- Clinical Nutrition

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa