Global Sleep Aids Market Size, Share, Trends & Growth Forecast Report - Segmented By Sleep Order (Insomnia, Sleep Apnea, Restless legs syndrome, Narcolepsy and sleepwalking), Product (Mattresses & Pillows, Sleep Laboratories, Medication and Sleep Apnea Devices), Medication Type, and Region - Industry Analysis From 2024 to 2033

Global Sleep Aids Market Summary

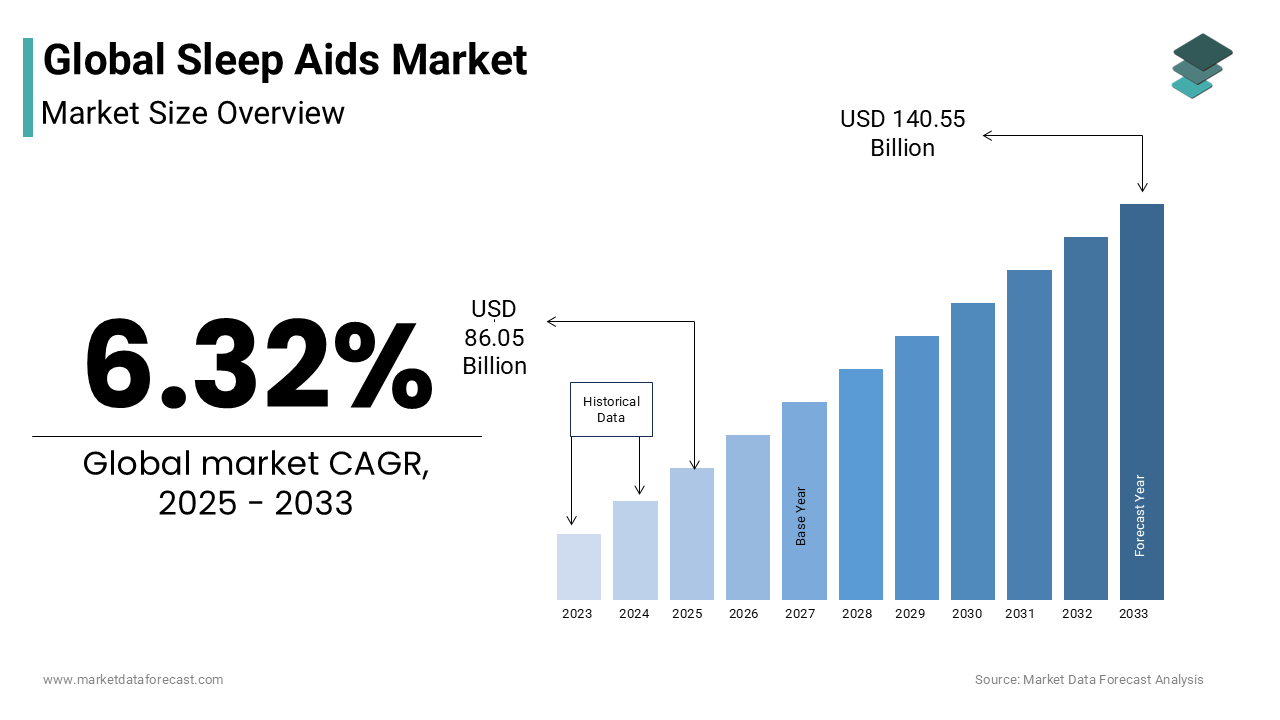

The global sleep aids market was valued at USD 80.96 billion in 2024 and is projected to reach USD 140.55 billion by 2033, expanding at a CAGR of 6.32% from 2025 to 2033. The growth of the global sleep aids market is attributed to the increasing prevalence of sleep disorders such as insomnia, rising stress levels, lifestyle changes, and growing awareness about the health risks of untreated sleep problems. In addition, the surge in demand for sleep medications, wearable monitoring devices, and non-pharmacological therapies is further fueling market expansion.

Key Market Trends

- Rising cases of insomnia and sleep apnea worldwide due to urbanization and stress.

- Increasing adoption of sleep tracking technologies and digital health platforms.

- Growth of OTC sleep aids and natural/herbal supplements.

- Rising investments in sleep disorder diagnostics and therapeutic devices.

- Expanding elderly population, highly susceptible to chronic sleep disorders.

Segmental Insights

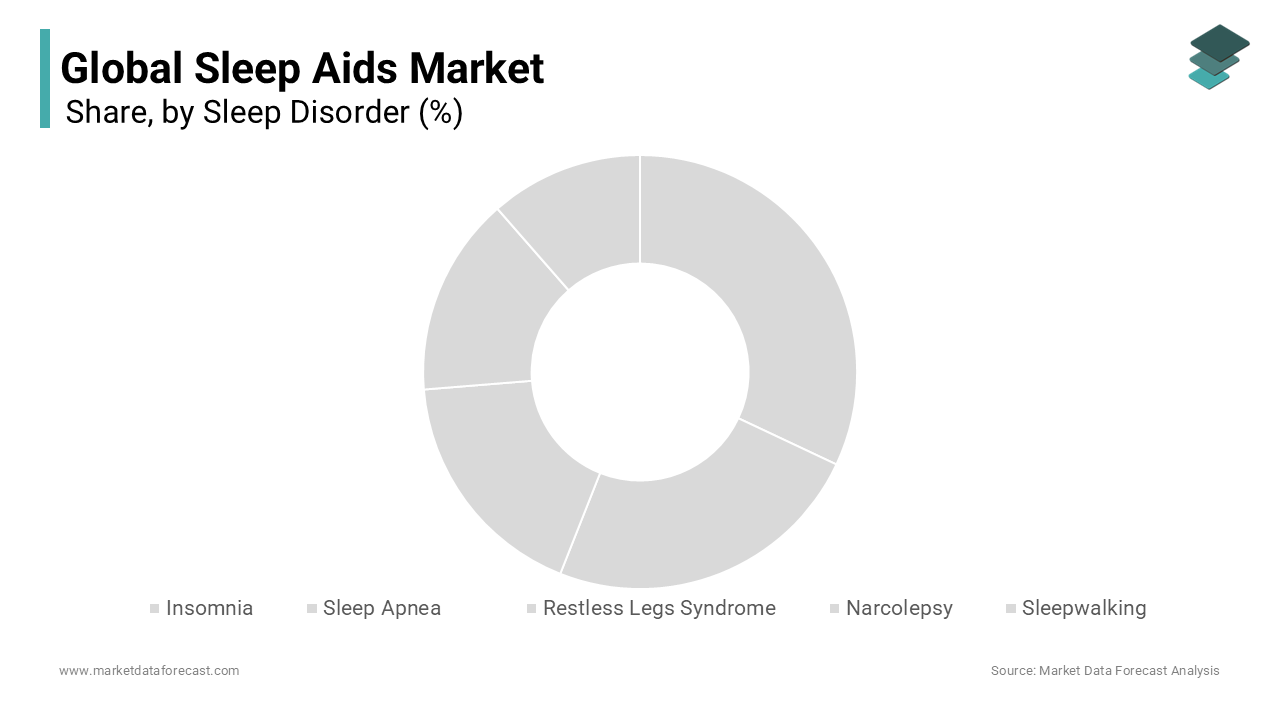

- Based on sleep disorder, the insomnia segment held the largest share of 46.5% in 2024, driven by high prevalence rates and rising dependency on medication and therapy solutions.

- Based on product, the medication segment dominated the global sleep aids market with 38.2% share in 2024, supported by the availability of prescription drugs and OTC sleep remedies.

Regional Insights

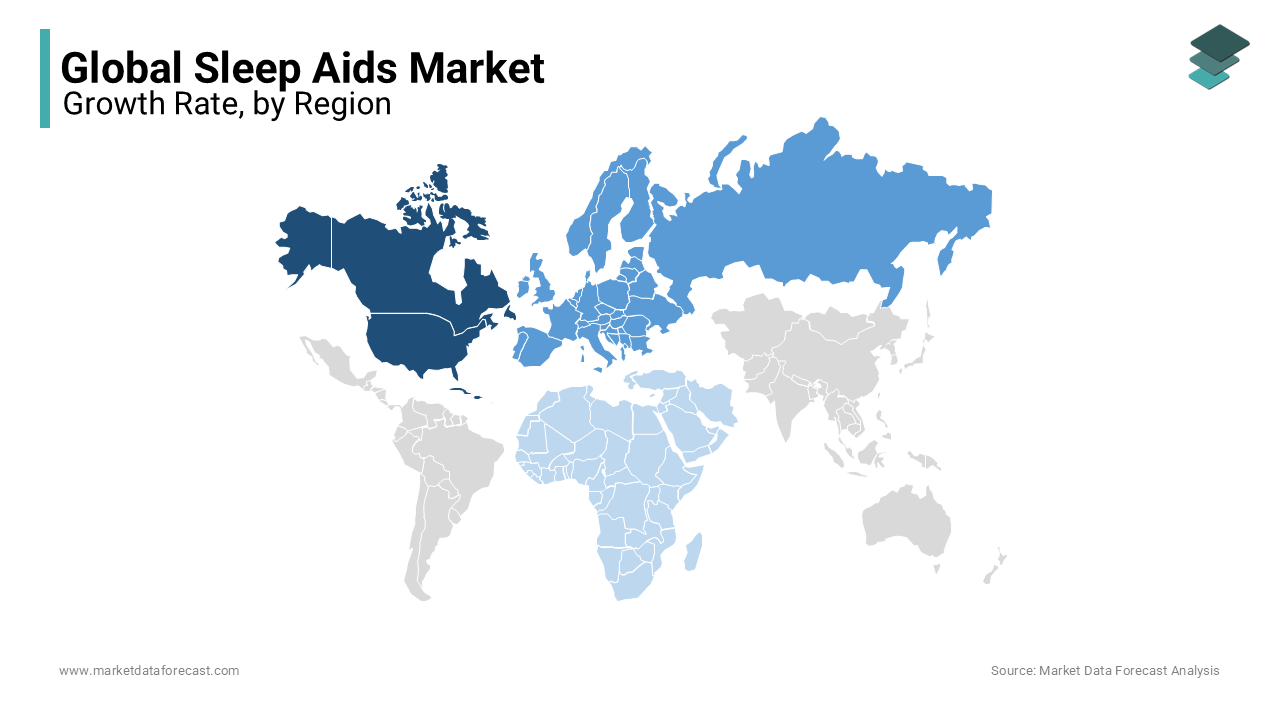

- North America led the global sleep aids market with a 37.4% share in 2024, driven by advanced healthcare infrastructure, high diagnosis rates, and strong product adoption.

- Europe represented a significant market, driven by rising demand for OTC sleep aids and innovative devices.

- Asia-Pacific is forecasted to witness the fastest growth, fueled by rising awareness, growing disposable incomes, and expanding healthcare accessibility.

Competitive Landscape

The global sleep aids market is moderately fragmented, with companies focusing on product innovation, mergers & acquisitions, and expansion into emerging regions. Notable players profiled include Sanofi, Merck & Co., Pfizer, Koninklijke Philips N.V. (Philips), GlaxoSmithKline Plc, Care Fusion Corporation, Cadwell, SleepMed, Natus Medical Inc., and DeVilbiss Healthcare LLC.

Global Sleep Aids Market Size

The global sleep aids market is estimated to grow from USD 80.96 billion in 2024 to USD 140.55 billion in 2033, representing a CAGR of 6.32%.

The sleep aids are therapeutic interventions designed to address sleep disturbances, including prescription medications, over-the-counter (OTC) remedies, natural supplements, medical devices, and digital therapeutics. These solutions target conditions such as insomnia, sleep apnea, restless legs syndrome, and circadian rhythm disorders, which collectively impair restorative sleep and diminish daytime functionality. Sleep is a biologically essential process, during which the body undergoes neural consolidation, metabolic regulation, and immune system reinforcement. Chronic disruption of this process has been linked to severe health consequences. According to the World Health Organization, more than 45% of the global population experiences some form of sleep disturbance, with long-term insomnia affecting approximately 10–15% of adults. The American Academy of Sleep Medicine emphasizes that consistent sleep deprivation increases the risk of hypertension, type 2 diabetes, and neurodegenerative diseases such as Alzheimer’s.

MARKET DRIVERS

Escalating Prevalence of Mental Health Disorders and Stress-Induced Insomnia

The growing global burden of anxiety, depression, and work-related stress is propelling the growth pf the Sleep Aids Market. Psychological distress directly disrupts the neurochemical balance required for sleep onset and maintenance, particularly through dysregulation of cortisol and melatonin. According to the World Health Organization, cases of anxiety and depression rose by over 25% globally in the wake of the post-pandemic period, with sleep disturbances reported in 70% of affected individuals. Corporate environments are amplifying this trend; as per the International Labour Organization, 43% of knowledge workers in high-income countries report sleep difficulties due to job pressure and digital overload. Employers in Japan, where “karoshi” (death from overwork) remains a societal concern, have introduced mandatory sleep monitoring for employees, driving adoption of non-pharmacological aids such as wearable sleep trackers and cognitive behavioral therapy (CBT) apps.

Expansion of Digital Therapeutics and AI-Driven Sleep Solutions

The emergence of digital therapeutics (DTx) as clinically validated tools for managing sleep disorders is additionally propelling the growth of the Sleep Aids Market. These software-based interventions, including cognitive behavioral therapy for insomnia (CBT-I) apps and AI-powered sleep coaches, offer scalable, non-invasive alternatives to pharmacological treatments. As per the U.S. Food and Drug Administration, seven digital therapeutics for insomnia received regulatory clearance between 2021 and 2023, including Pear Therapeutics’ reSET-S and Big Health’s Daylight. The latter demonstrated a 76% improvement in sleep onset latency in a randomized controlled trial involving 2,400 participants, as published in The Lancet Digital Health. Artificial intelligence now enables real-time analysis of sleep patterns through wearable integration, allowing personalized feedback and adaptive interventions

MARKET RESTRAINTS

Safety Concerns and Risk of Dependency Associated with Pharmacological Aids

The use of prescription and over-the-counter sleep medications due to risks of dependency, cognitive impairment, and long-term health consequences is limiting the growth of the Sleep Aids Market. Benzodiazepines and non-benzodiazepine hypnotics such as zolpidem, while effective for short-term relief, are associated with tolerance development, withdrawal symptoms, and next-day drowsiness that impairs driving and work performance. According to the U.S. Centers for Disease Control and Prevention, emergency department visits related to non-medical use of sleep medications increased by 34% between 2015 and 2022, with older adults disproportionately affected.

Limited Access to Sleep Diagnostics and Specialized Care in Low- and Middle-Income Countries

The scarcity of diagnostic infrastructure and trained sleep specialists in developing regions is also to hinder the growth of the Sleep Aids Market. Polysomnography, the gold standard for diagnosing sleep disorders, requires specialized equipment and expert interpretation, both of which are concentrated in urban medical centers of high-income nations. According to the World Sleep Society, fewer than 10% of sleep clinics in sub-Saharan Africa offer comprehensive diagnostic services, and only 3% of the population has ever undergone a sleep study. In India, where an estimated 90 million people suffer from obstructive sleep apnea, the Indian Council of Medical Research notes there are fewer than 500 accredited sleep laboratories nationwide. This diagnostic gap prevents accurate identification of conditions, leading to under-treatment or inappropriate use of over-the-counter remedies.

MARKET OPPORTUNITIES

Integration of Sleep Aids with Wearable Technology and Smart Home Ecosystems

The integration of sleep aids with wearable devices and ambient intelligence systems is ascribed to showcase new opportunities for the growth of the sleep aids market. As per the University of California, San Francisco’s Center for Digital Health Innovation, integration of wearable data with smart lighting, temperature controls, and soundscapes can improve sleep efficiency by up to 37%. Companies like Withings and Oura have partnered with home automation platforms such as Apple HomeKit and Google Nest to create “sleep environments” that automatically dim lights, lower room temperature, and play white noise upon detecting bedtime routines. The European Commission’s Horizon Europe program funded a 2023 pilot in Finland where AI-adjusted bedroom conditions reduced sleep onset time by 22 minutes on average. Additionally, insurance providers in Germany are offering premium discounts to policyholders who maintain healthy sleep scores derived from wearable data.

Growing Adoption of Natural and Plant-Based Sleep Supplements

The consumer preference for non-pharmaceutical, holistic solutions is amplifying the growth of the Sleep Aids Market. These substances are perceived as safer and more sustainable alternatives to synthetic drugs, aligning with global wellness trends and clean-label movements. According to the American Botanical Council, sales of herbal sleep supplements in the U.S. grew by 18% annually between 2020 and 2023, with valerian and passionflower among the fastest-growing categories. A double-blind, placebo-controlled trial published in Phytomedicine demonstrated that a standardized extract of valerian and hops reduced sleep latency by 14 minutes without next-day sedation. In Japan, traditional Kampo medicine formulations containing ashwagandha and jujube seed are increasingly integrated into over-the-counter sleep products, supported by the Ministry of Health’s endorsement of integrative approaches. The European Food Safety Authority has approved health claims for magnesium’s role in reducing tiredness and supporting normal nervous system function, enhancing consumer trust.

MARKET CHALLENGES

Heterogeneity in Regulatory Standards for Sleep Aids Across Geographies

The complexity due to divergent regulatory classifications and approval pathways for different product types is limiting the growth of the global sleep aids market. Prescription drugs are subject to rigorous clinical trials and monitoring, while dietary supplements and digital therapeutics often operate under looser frameworks, creating inconsistencies in safety and efficacy validation. In the United States, the FDA regulates prescription sleep medications strictly but does not evaluate the claims of herbal supplements, leading to variability in product quality. As per the U.S. Government Accountability Office, 20% of melatonin supplements tested in 2022 contained significantly higher or lower doses than labeled. Conversely, the European Medicines Agency requires stricter substantiation for health claims, yet member states differ in enforcement. In India, the Central Drugs Standard Control Organization only recently began drafting guidelines for nutraceuticals, leaving a regulatory vacuum.

Persistent Stigma and Low Public Awareness Regarding Sleep Disorders

The societal attitudes toward sleep disorders remain marked by trivialization and stigma, which is solely challenging the growth of the global sleep aids market. Insomnia and other sleep conditions are often dismissed as lifestyle issues rather than legitimate medical concerns, discouraging individuals from seeking professional help. According to a global survey conducted by the World Sleep Society, 54% of respondents in 15 countries believed that people with insomnia “just need to relax,” reflecting widespread misconceptions. Educational gaps persist even among healthcare providers; a 2023 study by the European Respiratory Society revealed that fewer than 30% of general practitioners routinely screen for sleep disorders during patient consultations. Public health campaigns remain underfunded; the U.S. National Institutes of Health allocates less than 1% of its annual budget to sleep research, despite sleep-related conditions affecting over 70 million Americans. This lack of institutional prioritization perpetuates underdiagnosis and reliance on self-medication.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2024 to 2033 |

| Segments Covered | By SleeDisorderer, Product, Medication Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | Sanofi, Merck & Co, Pfizer, Koninklijke Philips N.V. (Philips), GlaxoSmithKline Plc, Care Fusion Corporation, Cadwell, SleepMed, Natus Medical Manufacturers, and DeVilbiss Healthcare LLC. |

SEGMENTAL ANALYSIS

By Sleep Disorder Insights

The insomnia segment held 46.5% of the sleep aids market share in 2024 with its widespread prevalence and multifactorial etiology, which spans psychological, environmental, and physiological domains. The condition is particularly prevalent among urban populations, where stress, artificial light exposure, and irregular work schedules disrupt circadian rhythms. As per the American Academy of Sleep Medicine, individuals in high-income countries spend an average of 6.8 hours in bed but achieve only 5.4 hours of actual sleep, which is reflecting significant sleep efficiency deficits. Moreover, corporate wellness programs in the U.S. and Western Europe increasingly include cognitive behavioral therapy for insomnia (CBT-I) as a standard offering, with over 60% of Fortune 500 companies providing digital sleep coaching platforms.

The sleep apnea segment is likely to grow with an estimated CAGR of 12.8% from 2025 to 2033 owing to the heightened clinical recognition, technological advancements in diagnostic and therapeutic devices, and increasing prevalence linked to obesity and aging populations. Obstructive sleep apnea (OSA) affects over 936 million adults globally, with moderate to severe cases exceeding 425 million, according to a meta-analysis published in The Lancet Respiratory Medicine. Continuous positive airway pressure (CPAP) devices remain the gold standard, and innovations such as auto-adjusting algorithms, heated humidification, and compact designs have improved patient compliance. Regulatory support is also accelerating adoption; in 2022, the European Commission expanded reimbursement for home sleep testing, enabling faster diagnosis. In Japan, where 15% of men over 40 suffer from OSA, the Ministry of Health launched a national screening initiative in 2023, distributing portable sleep monitors through primary care clinics. Additionally, smart CPAP machines now integrate with mobile apps to track usage and provide motivational feedback, which is improving long-term engagement.

By Product Insights

The medication segment was accounted in holding 38.2% of the sleep aids market share in 2024 with the immediate symptom relief offered by pharmacological interventions, their widespread availability, and entrenched prescribing practices within primary care. Prescription hypnotics such as zolpidem, eszopiclone, and suvorexant are frequently deployed for short-term management of insomnia, while over-the-counter (OTC) agents like diphenhydramine and melatonin remain popular for self-directed care. According to the U.S. Food and Drug Administration, more than 9 million Americans filled prescriptions for sleep medications in 2023, with melatonin-based supplements consumed by an estimated 3.1 million adults weekly. The accessibility of OTC options in pharmacies, supermarkets, and e-commerce platforms further amplifies reach in regions with limited access to specialized sleep clinics.

The sleep apnea devices segment is expected to grow at a CAGR of 13.2% from 2025 to 2033 with the technological innovation, rising diagnosis rates, and growing awareness of the severe health consequences associated with untreated obstructive sleep apnea (OSA). Continuous positive airway pressure (CPAP) machines remain the cornerstone of treatment, with global shipments exceeding 5.8 million units in 2023, as reported by the Global Asthma and Airways Federation. Newer models feature integrated humidifiers, leak compensation algorithms, and wireless connectivity for real-time adherence monitoring, significantly improving patient comfort and compliance. The U.S. Centers for Medicare & Medicaid Services expanded reimbursement for auto-titrating PAP devices in 2023, encouraging adoption among elderly beneficiaries. Additionally, smart devices now sync with mobile applications to provide usage analytics, motivational prompts, and clinician alerts, enhancing long-term engagement.

REGIONAL ANALYSIS

North America Sleep Aids Market Insights

North America was the largest and held 37.4% of the global sleep aids market share in 2024. The country has pioneered the integration of digital therapeutics into mainstream care, with the FDA clearing multiple prescription-based sleep apps for cognitive behavioral therapy. Leading insurers, including UnitedHealthcare and Aetna, now cover CPAP devices and sleep studies, reducing financial barriers. Corporate wellness programs in tech hubs like Silicon Valley have institutionalized sleep health monitoring, often providing employees with wearable trackers and access to sleep coaches.

Europe Sleep Aids Market Insights

Europe sleep aids market was positioned second by holding 28.3% of share in 2024. Germany, the UK, and France lead in device adoption and clinical research, with national health programs increasingly incorporating sleep diagnostics. The UK’s National Health Service launched a national sleep strategy in 2023, aiming to reduce undiagnosed sleep apnea by 40% over five years. In Germany, statutory health insurers fully reimburse CPAP therapy, contributing to one of the highest treatment adherence rates in Europe at 68%, as reported by the German Sleep Society. The European Medicines Agency has approved several next-generation hypnotics with improved safety profiles by fostering confidence in pharmacological treatments.

Asia-Pacific Sleep Aids Market Insights

Asia-Pacific sleep aids market is likely to grow with significant CAGR in the next coming years. Urban centers in these countries are witnessing a surge in sleep disorders due to high-stress work cultures, extended screen time, and environmental noise. China’s sleep aid market grew by 18% annually from 2020 to 2023, driven by rising middle-class spending on wellness products. India, despite having over 90 million undiagnosed OSA cases, has only 300 accredited sleep labs, as reported by the Indian Council of Medical Research. Consumer preference leans toward OTC supplements and herbal remedies, with melatonin and ashwagandha gaining popularity. E-commerce platforms like Alibaba and Flipkart have accelerated access to sleep aids, while startups develop low-cost CPAP alternatives.

Latin America Sleep Aids Market Insights

Latin America sleep aids market growth is driven by rising awareness and public health initiatives. Brazil leads the region with 45% of market activity, supported by a growing network of sleep clinics and medical device imports. The Brazilian Society of Sleep reports that sleep disorder prevalence exceeds 30% in urban areas, with insomnia and OSA being the most common. In 2023, Mexico’s Ministry of Health integrated sleep screening into its national hypertension program, recognizing the bidirectional link between sleep apnea and cardiovascular disease. Argentina has introduced tax incentives for medical device manufacturers, encouraging local production of CPAP machines. However, access remains limited in rural regions; only 15% of Peruvians with severe insomnia have ever consulted a specialist, according to the Andean Health Organization. Cultural stigma persists, with many viewing sleep disorders as personal weaknesses.

Middle East and Africa Sleep Aids Market Insights

The Middle East and Africa sleep aids market is expected to grow eventually in the next coming years. The UAE has accredited over 40 sleep centers, one of the highest densities in the region. Conversely, sub-Saharan Africa faces severe diagnostic shortages; the African Sleep Research Network reports that fewer than 10 sleep specialists serve the entire population of West Africa. In Kenya and Nigeria, most cases go undiagnosed due to lack of equipment and training. However, mobile health innovations are emerging; a 2023 pilot in Ghana used smartphone-based questionnaires and pulse oximetry to screen for OSA in rural clinics.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Some of the notable companies dominating the global sleep aids market profiled in this report are Sanofi, Merck & Co., Pfizer, Koninklijke Philips N.V. (Philips), GlaxoSmithKline Plc, Care Fusion Corporation, Cadwell, SleepMed, Natus Medical Inc., and DeVilbiss Healthcare LLC.

The competitive dynamics of the sleep aids market are shaped by a convergence of medical technology, consumer wellness, and digital innovation. Established medical device manufacturers leverage clinical credibility and global distribution to dominate the prescription and sleep apnea device segments, while agile consumer brands are redefining over-the-counter solutions with lifestyle-oriented products. The market is increasingly polarized between high-tech, regulated interventions and low-barrier, wellness-focused offerings, each appealing to distinct user needs. Differentiation hinges on trust, efficacy, and user experience, with companies striving to balance scientific rigor with accessibility. Regulatory scrutiny for supplements and digital therapeutics, where claims must navigate fine lines between wellness and medical intent. Strategic alliances between device makers, software developers, and healthcare systems are becoming essential to deliver integrated care models. At the same time, rising consumer demand for natural, non-addictive alternatives is pressuring traditional pharmaceutical players to innovate beyond sedative-hypnotics.

Top Players in the Sleep Aids Market

ResMed

ResMed is a global leader in sleep apnea treatment and digital health solutions, renowned for its innovation in non-invasive ventilation and connected care platforms. The company has pioneered the development of advanced CPAP and bilevel devices that integrate seamlessly with cloud-based monitoring systems, enabling real-time patient engagement and therapy adherence tracking. Its focus on user-centric design, quiet operation, and personalized pressure delivery has set industry benchmarks. ResMed also invests heavily in telehealth infrastructure, offering end-to-end ecosystems that link patients, clinicians, and payers.

Philips Respironics

Philips Respironics holds a prominent position in the sleep aids market through its comprehensive portfolio of diagnostic and therapeutic devices for sleep-disordered breathing. The company is recognized for its technological leadership in adaptive servo-ventilation, auto-titrating PAP systems, and integrated humidification solutions that enhance patient comfort and compliance. Its strong clinical partnerships and global distribution network have enabled widespread adoption in both hospital and home settings. Philips has also advanced digital integration by linking its devices to mobile applications and remote monitoring platforms, allowing for proactive therapy management. Despite past recalls, the company has reinforced its commitment to quality and innovation, maintaining trust among healthcare providers.

Som Sleep

Som Sleep has emerged as a disruptive force in the over-the-counter sleep aids sector by redefining consumer engagement through direct-to-consumer branding and science-backed formulations. The company specializes in melatonin-infused beverages and powdered supplements that combine natural ingredients like magnesium, L-theanine, and chamomile to promote relaxation and sleep onset. Unlike traditional pharmaceutical approaches, Som Sleep emphasizes transparency, clean labeling, and lifestyle integration, appealing to health-conscious millennials and Gen Z demographics. Its products are designed for convenience and rapid absorption, aligning with modern routines that prioritize wellness without prescription dependency. The brand’s success reflects a broader cultural shift toward preventive, non-pharmacological solutions, positioning it as a key player in the evolving landscape of consumer-driven sleep wellness.

Top Strategies Used by Key Market Participants

One major strategy employed by leading companies is the integration of digital health platforms with physical sleep aids, creating closed-loop ecosystems that enhance treatment adherence and clinical outcomes. Firms are embedding connectivity into devices to enable remote monitoring, real-time feedback, and data sharing with healthcare providers, thereby transforming passive tools into active components of chronic care management.

Another key approach involves the development of hybrid therapeutic models that combine pharmacological or device-based treatments with behavioral interventions such as cognitive behavioral therapy for insomnia (CBT-I). By partnering with digital health startups or developing proprietary apps, companies offer comprehensive solutions that address both physiological and psychological aspects of sleep disorders, increasing long-term efficacy and patient retention.

A third strategic focus is on consumer education and brand positioning in the wellness space. Companies are investing in public awareness campaigns, sleep literacy programs, and collaborations with employers and insurers to destigmatize sleep disorders and promote early intervention

RECENT MARKET DEVELOPMENTS

- In February 2023, ResMed launched a new digital sleep health platform that integrates CPAP device data with electronic health records, enabling clinicians to remotely monitor patient adherence and adjust therapy in real time. This initiative is expected to enhance treatment outcomes and strengthen ResMed’s position in connected care.

- In July 2023, Philips Respironics introduced a next-generation auto-adjusting PAP device with built-in artificial intelligence to predict airway obstructions and optimize pressure delivery. The innovation aims to improve comfort and compliance for sleep apnea patients, reinforcing Philips’ leadership in respiratory technology.

- In October 2023, Som Sleep partnered with a leading mental wellness app to co-develop a sleep support program combining its supplements with guided meditation and sleep coaching. This collaboration is designed to offer a holistic solution for stress-related insomnia and expand Som Sleep’s reach in the digital wellness space.

- In January 2024, Reckitt Benckiser expanded its Nytol product line with a plant-based, non-habit-forming sleep aid formulated for younger consumers, reflecting a strategic shift toward natural ingredients and broader demographic targeting.

- In May 2023, Bose discontinued its sleep-focused noise-masking earbuds but transferred the underlying technology to a new health-focused subsidiary, signaling a repositioning of its sleep innovation toward medical applications and strategic partnerships.

MARKET SEGMENTATION

This research report on the global sleep aids market has been segmented and sub-segmented based on sleep disorder, product, medication type, and region.

By Sleep Disorder

- Insomnia

- Sleep Apnea

- Restless Legs Syndrome

- Narcolepsy

- Sleepwalking

By Product

- Mattresses & Pillows

- Sleep Laboratories

- Medication

- Sleep Apnea Devices

By Medication Type

- Prescription-Based Drugs

- OTC Drugs

- Herbal Drugs

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

Which segment by disorder led the sleep aids market in 2025?

The global sleep aids market size was valued at USD 86.08 billion in 2025.

Which region dominated the sleep aids market in 2024?

Geographically, the North American region accounted for the most dominant share in the global market in 2024.

Who are some of the noteworthy players in the sleep aids market?

Sanofi, Merck & Co, Pfizer, Koninklijke Philips N.V. (Philips), GlaxoSmithKline Plc, Care Fusion Corporation, Cadwell, SleepMed, Natus Medical Manufactures, and DeVilbiss Healthcare LLC. are some of the promising players in the sleep aids market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com