Global Ultrasound Devices Market Size, Share, Trends & Growth Forecast Report – Segmented By Technology (Diagnostic Ultrasound and Therapeutic Ultrasound), Device Display (Color and Black and White), Portability (Trolley/Cart-based and Compact/Handheld), Application and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2026 to 2034

Market Size, 2025

$10.54 BnMarket Estimate, 2026

$11.14 BnMarket Forecast, 2034

$17.36 BnCAGR, 2026–2034

5.7%Global Ultrasound Devices Market Report Summary

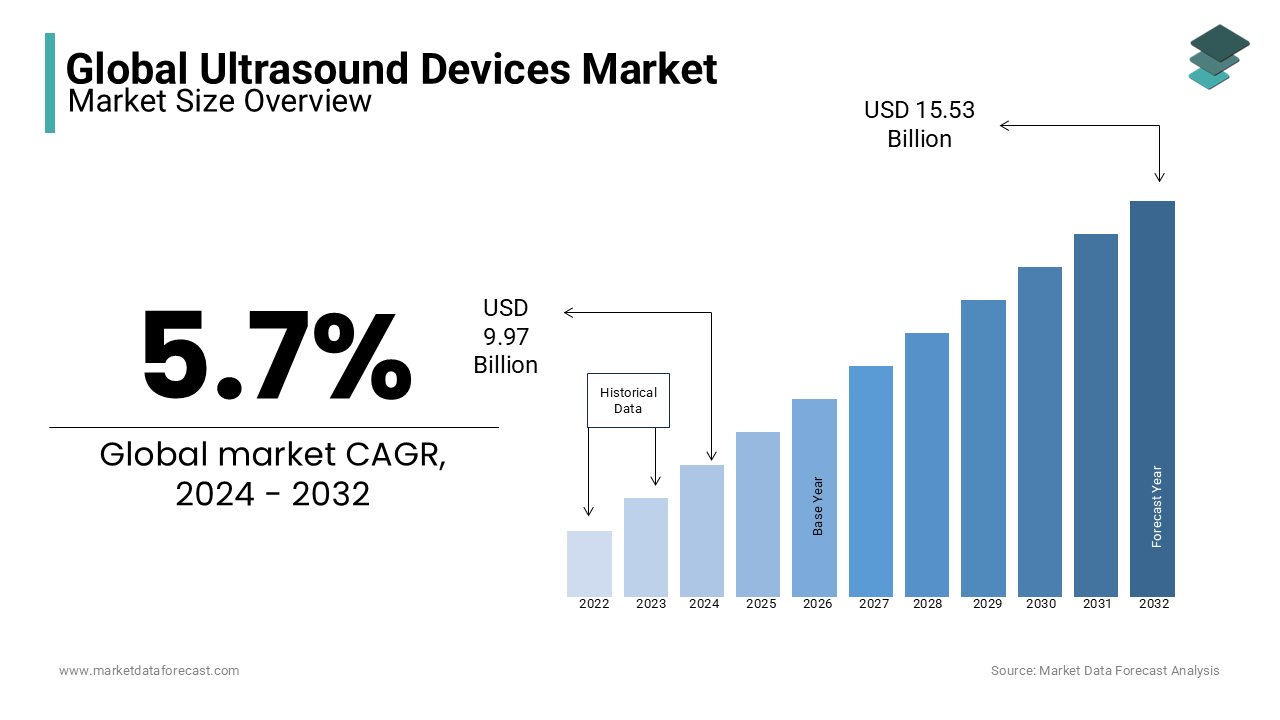

The global ultrasound devices market was valued at USD 10.54 billion in 2025, is estimated to reach USD 11.14 billion in 2026, and is projected to reach USD 17.36 billion by 2034, growing at a CAGR of 5.70% during the forecast period from 2026 to 2034. The growth of the global ultrasound devices market is driven by the rising prevalence of chronic diseases, increasing geriatric population, and growing demand for non-invasive diagnostic imaging technologies. Continuous technological advancements in portable ultrasound systems, increasing adoption of point-of-care ultrasound, and integration of artificial intelligence into imaging workflows are further accelerating market growth. Moreover, expanding healthcare infrastructure, rising demand for early disease diagnosis, and growing utilization of ultrasound across multiple clinical specialties are supporting the expansion of the global ultrasound devices market.

Key Market Trends

-

Rising adoption of portable and handheld ultrasound devices for point-of-care diagnostics.

-

Increasing integration of artificial intelligence and automation to improve imaging accuracy and workflow efficiency.

-

Growing demand for wireless and cloud-connected ultrasound systems supporting telemedicine applications.

-

Rising utilization of ultrasound in emergency medicine, primary care, and home healthcare settings.

-

Increasing technological advancements in high-resolution imaging, elastography, and three-dimensional ultrasound systems.

Segmental Insights

- Based on technology, the diagnostic ultrasound segment dominated the global ultrasound devices market in 2025. The dominance of the segment is attributed to its widespread application across obstetrics, gynecology, cardiology, abdominal imaging, and emergency medicine, along with its non-invasive nature, absence of ionizing radiation, affordability, and real-time imaging capabilities that make it a preferred first-line diagnostic modality.

- The therapeutic ultrasound segment is projected to witness the fastest CAGR of 9.05% during the forecast period owing to increasing adoption of focused ultrasound therapies, growing demand for non-invasive treatment alternatives, rising prevalence of musculoskeletal disorders, expanding applications in oncology and neurology, and continuous advancements in image-guided therapeutic technologies.

- Based on device display, the color display segment dominated the global ultrasound devices market in 2025. The growth of the segment is driven by superior visualization of blood flow through Doppler imaging, enhanced tissue differentiation, improved diagnostic accuracy, high-resolution imaging capabilities, and increasing adoption across cardiology, vascular imaging, and obstetric applications.

- The black and white display segment is anticipated to register the fastest CAGR of 6.8% during the forecast period due to increasing demand for affordable diagnostic equipment, expanding deployment in primary healthcare facilities, rising adoption in resource-constrained settings, improved grayscale imaging technologies, and growing utilization for basic diagnostic and emergency care applications.

- Based on portability, the trolley/cart-based segment dominated the global ultrasound devices market in 2025. The dominance of the segment is attributed to its comprehensive imaging capabilities, superior image quality, multiple probe compatibility, advanced software features, and extensive utilization in hospitals and specialized diagnostic centers.

- The compact and handheld segment is projected to witness the fastest CAGR of 13.5% during the forecast period owing to increasing demand for bedside diagnostics, expanding point-of-care applications, affordability, wireless connectivity, growing adoption by primary care physicians, and rising emphasis on decentralized healthcare delivery.

Regional Insights

- North America dominated the global ultrasound devices market in 2025 owing to its advanced healthcare infrastructure, high healthcare expenditure, widespread adoption of advanced diagnostic imaging technologies, strong presence of leading manufacturers, favorable reimbursement policies, and increasing utilization of point-of-care ultrasound across healthcare settings.

- Europe held a significant share of the global ultrasound devices market due to its well-established healthcare systems, stringent regulatory standards, increasing adoption of digital imaging technologies, growing aging population, and continuous investments in medical device innovation and diagnostic imaging infrastructure.

- Asia-Pacific is projected to witness the fastest growth during the forecast period due to expanding healthcare infrastructure, increasing government investments in medical imaging, rising healthcare expenditure, growing prevalence of chronic diseases, rapid urbanization, and increasing demand for affordable diagnostic technologies across China, India, Japan, and Southeast Asian countries.

- Latin America continues to experience steady growth owing to expanding diagnostic laboratory networks, improving healthcare accessibility, increasing investments in public and private healthcare facilities, rising awareness regarding early disease diagnosis, and growing demand for portable imaging devices.

- The Middle East and Africa is expected to witness notable growth during the forecast period due to increasing healthcare modernization initiatives, expanding hospital infrastructure, rising government investments in diagnostic imaging, growing adoption of portable ultrasound technologies, and improving access to healthcare services across emerging economies.

Competitive Landscape

The global ultrasound devices market is highly competitive and characterized by the presence of leading medical imaging companies competing through continuous technological innovation, artificial intelligence integration, product miniaturization, and strategic collaborations. Leading companies are focusing on developing portable and handheld ultrasound systems, improving image quality through advanced transducer technologies, expanding cloud-enabled imaging platforms, strengthening global distribution networks, and integrating automation into diagnostic workflows. Continuous investments in research and development, regulatory approvals, and digital healthcare solutions continue to strengthen competitive positioning across the global ultrasound devices market The prominent players operating in the global ultrasound devices market include General Electric Company (U.S.), Koninklijke Philips N.V. (Netherlands), Toshiba Corporation (Japan), Siemens AG (Germany), Hitachi Ltd. (Japan), Samsung Electronics Co., Ltd. (South Korea), FUJIFILM Holdings Corporation (Japan), Esaote S.p.A. (Italy), Mindray Medical International Ltd. (China), and Analogic Corporation (U.S.).

Global Ultrasound Devices Market Size

The value of the global ultrasound devices market is projected to grow to USD 17.36 billion by 2034 and USD 11.14 billion in 2026, growing at a CAGR of 5.7% during the forecast period. The ultrasound devices market size was valued at USD 10.54 billion in 2025.

Ultrasound devices are a broad spectrum of diagnostic imaging systems that utilize high-frequency sound waves to visualize internal body structures in real time. These devices range from large cart-based systems used in hospitals for comprehensive diagnostics to compact handheld units employed for point-of-care assessments. Ultrasound technology is favored for its non-invasive nature, lack of ionizing radiation, and cost-effectiveness compared to computed tomography or magnetic resonance imaging. According to the World Health Organization, more than 3.6 billion diagnostic imaging examinations are performed annually worldwide, with ultrasound representing a significant portion due to its versatility in obstetrics, cardiology, and abdominal imaging. As per the Centers for Disease Control and Prevention, chronic diseases such as heart disease and cancer account for 7 out of 10 deaths in the United States, driving the need for regular diagnostic monitoring where ultrasound plays a pivotal role. Furthermore, as per the American College of Radiology, the importance of portable ultrasound is emphasized in emergency settings for rapid assessment of trauma and internal bleeding. As healthcare systems increasingly prioritize early detection and minimally invasive procedures, the demand for advanced ultrasound technologies continues to rise. The integration of artificial intelligence and cloud connectivity into modern ultrasound platforms further enhances diagnostic accuracy and workflow efficiency, positioning these devices as essential tools in contemporary medical practice.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases and Geriatric Population

The escalating prevalence of chronic diseases coupled with a rapidly aging global population is a key factor propelling the growth of the global ultrasound devices market. Chronic conditions such as cardiovascular diseases, diabetes, and cancer require frequent diagnostic monitoring to manage patient health effectively. According to the World Health Organization, non-communicable diseases kill 41 million people each year, which is equivalent to 74% of all deaths globally. This substantial burden necessitates regular imaging for early detection and treatment planning. Ultrasound is particularly valuable in cardiology for assessing heart function and in oncology for tumor detection and biopsy guidance. As per the United Nations Department of Economic and Social Affairs, the number of persons aged 65 years or older worldwide is projected to increase from 761 million in 2021 to 1.6 billion by 2050. Older adults are more susceptible to chronic conditions and require more frequent medical interventions, including diagnostic imaging. According to the American Heart Association, cardiovascular disease remains the leading cause of death globally, requiring extensive use of echocardiography for diagnosis and management. As the geriatric population grows, the demand for safe and repeatable imaging modalities like ultrasound increases significantly. Healthcare providers rely on ultrasound for its ability to provide real-time insights without exposing patients to harmful radiation, making it ideal for long-term monitoring of elderly patients with multiple comorbidities.

Technological Advancements and Portability of Devices

The ultrasound devices market in various clinical settings is likely to continue its expansion over the next few years due to persistent technological innovation, which is further contributing to the ultrasound devices market expansion. Modern ultrasound systems are becoming smaller, lighter, and more powerful, enabling their use in point-of-care environments such as emergency rooms, ambulances, and remote clinics. According to the National Institutes of Health, the adoption of point-of-care ultrasound has seen a significant upward trajectory in recent years due to improvements in battery life, image quality, and wireless connectivity. These portable devices allow physicians to perform immediate assessments at the bedside, reducing the time to diagnosis and improving patient outcomes. The integration of artificial intelligence algorithms into ultrasound software enhances image interpretation and reduces operator dependency, making the technology accessible to less experienced users. As per the Food and Drug Administration, numerous AI-enabled ultrasound applications have been cleared to assist in automating measurements and identifying abnormalities. Furthermore, the development of wireless probes eliminates cable clutter and improves ease of use in crowded clinical spaces. Telemedicine capabilities embedded in modern ultrasound systems enable remote consultations, allowing specialists to guide examinations from distant locations. This technological evolution democratizes access to high-quality diagnostic imaging, particularly in underserved areas where traditional large-scale equipment is unavailable. As miniaturization continues and processing power increases, the utility of ultrasound devices expands beyond traditional radiology departments into primary care and home health settings.

MARKET RESTRAINTS

High Cost of Advanced Ultrasound Systems

The substantial cost associated with acquiring and maintaining advanced ultrasound systems is a significant restraint to market growth, particularly in resource-constrained healthcare settings. High-end ultrasound machines equipped with specialized probes and advanced software features can cost between 50,000 and 150,000 dollars or more, depending on the configuration. According to the World Bank, many low-income countries spend less than 100 dollars per capita on health annually, limiting their ability to invest in expensive diagnostic equipment. For small private practices and rural clinics, these capital expenditures represent a significant financial burden that may not be immediately offset by reimbursement rates. Additionally, the ongoing costs of maintenance, software updates, and probe replacements add to the total cost of ownership. According to the Healthcare Financial Management Association, budget constraints often force healthcare facilities to delay equipment upgrades, resulting in the use of outdated technology that may compromise diagnostic accuracy. In developing regions, the lack of adequate funding, infrastructure, and trained personnel further hinders the adoption of advanced ultrasound systems. While portable devices offer a lower cost alternative, they may lack the comprehensive functionality required for complex diagnoses. This financial barrier restricts the widespread deployment of state-of-the-art ultrasound technology, leaving many patients without access to optimal diagnostic care. Manufacturers face the challenge of balancing innovation with affordability to make these critical tools accessible to a broader global audience.

Shortage of Skilled Sonographers and Technicians

The global shortage of qualified sonographers and ultrasound technicians is further hindering the expansion of the global ultrasound devices market. Operating ultrasound equipment requires specialized training and expertise to acquire high-quality images and interpret findings accurately. As per the U.S. Bureau of Labor Statistics, employment of diagnostic medical sonographers is projected to grow much faster than the average for all occupations, highlighting a persistent need for new professionals to meet demand. This shortage leads to longer wait times for patients, increased workload for existing staff, and potential burnout. In many developing countries, the situation is even more critical, with the World Health Organization reporting that large portions of the population lack access to basic diagnostic imaging services. Without skilled operators, even the most advanced ultrasound devices cannot deliver accurate diagnostic results. Training programs are often lengthy and expensive, creating a bottleneck in workforce development. Additionally, the complexity of new technologies, such as three-dimensional imaging and elastography, requires continuous professional development, which may not be readily available in all regions. The reliance on highly skilled personnel limits the scalability of ultrasound services, particularly in primary care settings where general practitioners may lack specific training. Until educational infrastructure and certification programs expand to meet demand, the human resource constraint will continue to hinder the full potential of ultrasound technology adoption globally.

MARKET OPPORTUNITIES

Expansion into Point of Care and Home Healthcare Settings

The expansion of ultrasound technology into point-of-care and home healthcare settings presents a substantial opportunity for market growth by decentralizing diagnostic services. Traditionally confined to hospital radiology departments, ultrasound devices are now being integrated into emergency medicine, primary care, and even home monitoring scenarios. According to the American Academy of Family Physicians, point-of-care ultrasound improves diagnostic accuracy and reduces the need for additional testing, leading to cost savings and faster treatment decisions. The rise of telehealth services further supports this trend by enabling remote guidance for ultrasound examinations performed by nurses or paramedics in the field. As per the Centers for Medicare and Medicaid Services, reimbursement policies have been expanded to support the use of point-of-care ultrasound in various settings, encouraging wider adoption among healthcare providers. Portable and handheld devices are particularly well suited for home healthcare, allowing patients with chronic conditions to receive regular monitoring without frequent hospital visits. This shift aligns with the broader industry move towards value-based care and patient-centered models. Manufacturers can capitalize on this opportunity by developing user-friendly devices with intuitive interfaces and automated features that empower non-specialist users. Partnerships with home health agencies and insurance providers can facilitate the integration of ultrasound into routine care plans. As the focus on preventive care and remote patient monitoring intensifies, the demand for accessible and easy-to-use ultrasound solutions in non-traditional settings is poised to grow significantly.

Integration of Artificial Intelligence and Automation

The integration of artificial intelligence and automation into ultrasound devices offers a promising opportunity for the global ultrasound devices market. AI algorithms can assist in image acquisition optimization, automatic measurement, and anomaly detection, reducing the cognitive load on sonographers and minimizing inter-observer variability. According to Nature Medicine, AI-assisted ultrasound has demonstrated comparable accuracy to expert radiologists in detecting certain conditions such as thyroid nodules and breast lesions. This technology enables less experienced users to perform reliable examinations, thereby addressing the shortage of skilled personnel. Automated workflows streamline the documentation process, reducing administrative burden and allowing clinicians to spend more time with patients. As per the Food and Drug Administration, several AI-powered ultrasound tools have been approved that provide real-time feedback during scans, ensuring optimal image quality. Furthermore, AI can analyze large datasets to identify patterns and predict disease progression, supporting personalized medicine initiatives. Cloud-based platforms facilitate the sharing of AI models and updates across devices, ensuring consistent performance improvements. Manufacturers who embed robust AI capabilities into their systems can differentiate their products and offer value-added services such as predictive analytics and decision support. As machine learning models become more sophisticated, the potential for ultrasound to serve as a primary screening tool in various medical specialties expands, opening new revenue streams and improving overall healthcare delivery.

MARKET CHALLENGES

Regulatory Hurdles and Reimbursement Complexities

Navigating complex regulatory landscapes and varying reimbursement policies poses a significant challenge to the global expansion of the ultrasound devices market. Each country has its own set of regulations for medical device approval, which can be time-consuming and costly to comply with. According to the European Commission, the Medical Device Regulation in Europe has introduced stricter requirements for clinical evidence and post-market surveillance, increasing the burden on manufacturers. In the United States, the Food and Drug Administration requires rigorous premarket approval for new ultrasound technologies, particularly those involving artificial intelligence. Additionally, reimbursement policies vary widely across regions and payers, affecting the financial viability of adopting new ultrasound systems. As per the American Medical Association, inconsistent coding and payment structures for point-of-care ultrasound create uncertainty for healthcare providers. In many developing countries, the lack of clear regulatory frameworks and reimbursement mechanisms hinders market entry for international vendors. Manufacturers must invest heavily in regulatory affairs and health economics teams to navigate these complexities. Delays in approval or unfavorable reimbursement decisions can significantly impact product launch timelines and return on investment. Harmonizing regulatory standards and establishing clear reimbursement pathways are essential for fostering innovation and ensuring that advanced ultrasound technologies reach the patients who need them most.

Image Quality Limitations in Obese Patients

Achieving high-quality images in obese patients remains a persistent technical challenge for ultrasound devices, limiting their diagnostic utility in certain populations. Sound waves attenuate significantly as they pass through adipose tissue, resulting in reduced penetration and poorer image resolution. According to the World Obesity Federation, the global prevalence of obesity has reached epidemic proportions, with over 800 million adults currently living with obesity. This demographic trend presents a growing challenge for ultrasound diagnostics, as standard probes may struggle to visualize deep structures adequately. While lower frequency probes offer better penetration, they often sacrifice resolution, making it difficult to detect small abnormalities. Manufacturers are developing specialized transducers and beamforming techniques to improve image quality in difficult-to-scan patients, but these solutions often come at a higher cost. The American Journal of Roentgenology highlights that suboptimal image quality can lead to inconclusive diagnoses, requiring follow-up tests with other modalities such as computed tomography or magnetic resonance imaging. This not only increases healthcare costs but also exposes patients to additional risks such as radiation or contrast agents. Overcoming this limitation requires continuous innovation in transducer materials, signal processing, and algorithm development. Until these technical barriers are fully addressed, the effectiveness of ultrasound in managing the health of the growing obese population will remain constrained.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Device Display, Portability, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leader Profiled | General Electric Company (U.S.), Koninklijke Philips N.V. (Netherlands), Toshiba Corporation (Japan), Siemens AG (Germany), Hitachi Ltd. (Japan), Samsung Electronics Co., Ltd. (South Korea), FUJIFILM Holdings Corporation (Japan). |

SEGMENTAL ANALYSIS

By Technology Insights

The diagnostic ultrasound segment held the dominant position in the ultrasound devices market in 2025 due to its widespread application in routine clinical examinations across various medical specialties, including obstetrics, gynecology, cardiology, and abdominal imaging. The primary driver for this dominance is the non-invasive nature of diagnostic ultrasound, which avoids ionizing radiation, making it safe for repeated use, particularly in vulnerable populations such as pregnant women and children. According to the American College of Radiology, millions of ultrasound procedures are performed annually in the United States, reflecting its status as a first-line diagnostic tool. The versatility of diagnostic ultrasound allows for real-time visualization of soft tissues, blood flow, and organ function, which is critical for early disease detection. The World Health Organization emphasizes that accessible diagnostic imaging is essential for managing maternal and child health globally, further driving demand in developing regions. Additionally, the relatively lower cost of diagnostic ultrasound compared to magnetic resonance imaging or computed tomography makes it economically viable for healthcare providers with limited budgets. Technological advancements such as high-resolution probes and three-dimensional imaging have enhanced diagnostic accuracy, reinforcing its clinical utility. The integration of diagnostic ultrasound into standard care protocols for chronic disease management ensures consistent demand. As healthcare systems prioritize preventive care and early intervention, diagnostic ultrasound remains the cornerstone of modern medical imaging infrastructure, supporting a vast array of clinical decisions and patient monitoring activities worldwide.

On the other side, the therapeutic ultrasound segment is the fastest-growing segment in the ultrasound devices market and is projected to expand at a CAGR of 9.05% over the forecast period owing to its expanding applications in physical therapy, pain management, focused ultrasound surgery, the increasing prevalence of musculoskeletal disorders and the shift towards non-invasive treatment options that reduce recovery time and complications associated with traditional surgery. According to the Centers for Disease Control and Prevention, approximately 21.3% of adults in the United States report having some form of doctor-diagnosed arthritis, which is a leading cause of disability and drives demand for therapeutic interventions like ultrasound therapy. High-intensity focused ultrasound is gaining traction in oncology for tumor ablation, offering a precise alternative to surgical resection. The National Institutes of Health supports research into therapeutic ultrasound for neurological conditions such as essential tremor and Parkinson’s disease, broadening its clinical scope. Furthermore, the rise in sports injuries and an aging population seeking conservative pain management solutions contributes to market expansion. Technological innovations such as image-guided focused ultrasound allow for targeted tissue destruction without incisions, enhancing patient safety and outcomes. As clinical evidence supporting the efficacy of therapeutic ultrasound accumulates, insurance coverage and physician adoption increase, accelerating market growth. The ability to treat conditions without pharmaceuticals or invasive procedures aligns with patient preferences for holistic and minimally invasive care options.

By Device Display Insights

The color display segment occupied the major share of the global market in 2025 due to their superior ability to visualize blood flow and tissue differentiation, which is critical for accurate diagnosis in cardiology, vascular studies, and obstetrics. The clinical necessity of Doppler imaging that uses color coding to represent the direction and velocity of blood flow is further aiding the dominance of color display segment in the global market. According to the American Heart Association, cardiovascular diseases remain the leading cause of death globally, necessitating detailed vascular assessments that only color Doppler can provide effectively. Color displays enhance the contrast between different tissue types, allowing physicians to identify abnormalities such as tumors, cysts, or inflammation with greater precision than black and white systems. The Society of Radiologists in Ultrasound recommends the use of color flow imaging for evaluating thyroid nodules and liver lesions, underscoring its importance in standard diagnostic protocols. Additionally, modern color displays offer higher resolution and brightness, improving visibility in well-lit clinical environments. The integration of advanced image processing algorithms enhances color fidelity and reduces artifacts, ensuring reliable interpretation. As healthcare standards rise, the expectation for comprehensive diagnostic information drives the preference for color display systems in hospitals and diagnostic centers. The ability to capture and store color images for electronic health records further supports their adoption, facilitating better communication among healthcare providers and improving continuity of care for patients with complex conditions.

However, the black and white display segment experiencing renewed growth in specific niche markets, particularly in point-of-care and resource-limited settings and is anticipated to showcase a CAGR of 6.8% over the forecast period owing to the rising demand for cost-effective and durable devices for basic screening and guidance procedures where color flow information is not strictly necessary. According to the World Health Organization, improving access to basic diagnostic tools in low-income countries is a priority, and black and white portable units offer an affordable solution for primary health centers. These devices are widely used for guiding needle biopsies, assessing bladder volume, and performing rapid trauma assessments in emergency settings where speed and simplicity are paramount. The rugged design and lower power consumption of black and white units make them ideal for remote clinics and mobile health units with limited infrastructure. Advances in grayscale imaging technology have significantly improved the clarity and detail of black and white images, narrowing the gap with color systems for certain applications. Furthermore, the lower maintenance costs and ease of use appeal to non-specialist healthcare workers such as nurses and paramedics who require quick and reliable diagnostic support. As global health initiatives focus on expanding basic healthcare coverage, the demand for affordable and functional black and white ultrasound devices continues to rise in emerging markets and rural areas.

By Portability Insights

The trolley or cart-based segment had the leading share of the global market in 2025 due to their comprehensive functionality, superior image quality, and extensive feature sets required for complex diagnostic procedures in hospitals and large diagnostic centers. The primary driver for this dominance is the need for high-performance imaging in specialized departments such as radiology, cardiology, and obstetrics where detailed anatomical visualization is critical. According to the American Hospital Association, large hospital systems account for the majority of advanced diagnostic imaging volumes, requiring robust systems with multiple probe options and advanced software capabilities. Cart-based systems typically support high-end features such as three-dimensional, four-dimensional, and elastography imaging, which are essential for accurate diagnosis of complex conditions. They also offer larger screens and ergonomic designs that reduce operator fatigue during lengthy examinations. The integration of these systems with hospital information networks facilitates seamless data management and reporting. Furthermore, teaching hospitals and academic medical centers prefer cart-based systems for their educational value and ability to handle diverse clinical cases. The established infrastructure in developed healthcare markets supports the widespread deployment of these stationary units. As the complexity of medical cases increases, the demand for high-fidelity imaging provided by trolley-based systems remains strong, ensuring their continued leadership in the overall ultrasound devices market despite the rise of portable alternatives.

However, the compact and handheld segment is the fastest-growing segment in the market and is expected to expand at a CAGR of 13.5% over the forecast period owing to the growing trend towards point-of-care diagnostics, decentralized healthcare delivery, the miniaturization of technology that has enabled the development of pocket-sized devices that connect to smartphones or tablets, offering high-quality imaging at a fraction of the cost of traditional systems. According to the Journal of Medical Internet Research, the adoption of handheld ultrasound by primary care physicians has increased significantly, as it allows for immediate bedside assessment, reducing referral delays and improving patient throughput. These devices are particularly valuable in emergency medicine, rural health, and home care settings where portability and ease of use are essential. The lower price point makes them accessible to smaller clinics and individual practitioners who cannot afford large cart-based systems. Additionally, the integration of wireless connectivity and cloud storage enables remote consultation and data sharing, enhancing collaborative care. Regulatory approvals for handheld devices have expanded their clinical indications, further boosting confidence among users. As healthcare models shift towards value-based care and patient convenience, the demand for versatile and portable ultrasound solutions continues to accelerate, transforming how diagnostic imaging is delivered across various healthcare settings.

REGIONAL ANALYSIS

North America Ultrasound Devices Market Analysis

North America had the major share of the global market in 2025 and is expected to maintain its dominant position in the global ultrasound devices market over the coming years, driven by its robust infrastructure and focus on innovation. The region benefits from a well-established network of hospitals and diagnostic centers that prioritize early detection and minimally invasive procedures. According to the Centers for Medicare and Medicaid Services, national health spending in the United States has reached approximately 5.7 trillion dollars, reflecting the significant investment in medical technologies including advanced ultrasound systems. The presence of major ultrasound manufacturers in the region fosters continuous innovation and competition, leading to the development of cutting-edge features such as artificial intelligence and portable devices. Strict regulatory standards enforced by the Food and Drug Administration ensure the high quality and safety of medical devices, encouraging trust among healthcare providers. Additionally, the high prevalence of chronic diseases such as cancer and cardiovascular conditions drives consistent demand for diagnostic imaging. The adoption of point-of-care ultrasound in emergency departments and primary care settings is widespread, supported by favorable reimbursement policies. With a strong focus on technological advancement and patient-centered care, North America remains the dominant force in the global ultrasound market, setting trends for other regions through its early adoption of new technologies and rigorous clinical standards.

Europe Ultrasound Devices Market Analysis

Europe is anticipated to sustain steady growth in the ultrasound devices market as it balances advanced clinical needs with public health cost-containment measures. The European Union’s Medical Device Regulation imposes rigorous requirements for clinical evidence and post-market surveillance, ensuring high standards for ultrasound equipment. According to the European Commission, the Digital Single Market strategy continues to promote the adoption of interoperable health technologies, facilitating cross-border healthcare and data exchange. Countries such as Germany, France, and the United Kingdom have well-developed healthcare infrastructures with high levels of ultrasound utilization in obstetrics, cardiology, and musculoskeletal imaging. The aging population in Europe increases the demand for diagnostic services, driving the need for efficient and accurate imaging solutions. Furthermore, the emphasis on cost containment in public healthcare systems favors the adoption of portable and cost-effective ultrasound devices that can be shared across departments. Government funding for research and development supports innovation in therapeutic ultrasound and AI integration. The presence of renowned medical research institutions also drives demand for specialized high-end systems. With a focus on patient safety, data privacy, and operational efficiency, Europe continues to be a key market for advanced ultrasound devices, particularly those that offer value through improved workflow and diagnostic accuracy.

Asia-Pacific Ultrasound Devices Market Analysis

The Asia-Pacific region is likely to witness the most rapid growth in the ultrasound devices market over the next several years, supported by massive healthcare expansion and infrastructure modernization. Countries such as China, India, Japan, and Australia are witnessing significant investments in hospital construction and laboratory modernization. According to the World Bank, healthcare expenditure in the Asia-Pacific region has been growing steadily as governments prioritize improving access to quality healthcare services. The large population base and increasing prevalence of infectious and chronic diseases drive high demand for diagnostic testing, necessitating efficient and affordable ultrasound solutions. In China, the Healthy China 2030 initiative promotes the digitalization of healthcare services, including the deployment of portable ultrasound devices in rural areas to improve accessibility. India is seeing a boom in private diagnostic chains that are adopting advanced ultrasound systems to cater to a growing middle class. Japan’s advanced technological landscape supports the adoption of high-end ultrasound with automation and artificial intelligence features. Additionally, medical tourism in countries like Thailand and Singapore drives demand for internationally accredited facilities equipped with state-of-the-art imaging technology. With supportive government policies and a growing middle class, the Asia-Pacific region presents immense opportunities for ultrasound vendors seeking expansion in both premium and value segments.

Latin America Ultrasound Devices Market Analysis

Latin America is poised for a phase of gradual but consistent development in the ultrasound devices market as healthcare systems increasingly prioritize modernization and accessibility. Brazil, Mexico, and Argentina are the largest markets in the region with ongoing efforts to modernize public and private healthcare facilities. According to the Pan American Health Organization, improving diagnostic capacity is a priority for many Latin American countries to address the burden of communicable and non-communicable diseases. The expansion of private hospital chains and diagnostic centers is driving the adoption of ultrasound to enhance operational efficiency and patient service quality. However, economic volatility and budget constraints in the public sector limit the pace of technology adoption compared to North America and Europe. Nevertheless, international collaborations and foreign investments in healthcare infrastructure are facilitating the introduction of advanced ultrasound solutions. The growing awareness of preventive healthcare among the middle class is increasing the volume of outpatient diagnostic tests, creating demand for scalable and user-friendly systems. Portable ultrasound devices are gaining traction due to their lower cost and ease of deployment in remote areas. As healthcare systems continue to evolve and digitize, Latin America offers promising growth potential for ultrasound providers willing to navigate local regulatory and economic challenges while addressing the needs of a diverse population.

Middle East and Africa Ultrasound Devices Market Analysis

The Middle East and Africa are projected to see a rise in demand for advanced diagnostic technologies over the next few years as nations continue to reform their health systems and emphasize early disease detection. Countries in the Gulf Cooperation Council such as Saudi Arabia and the United Arab Emirates are heavily investing in smart healthcare initiatives as part of their economic diversification strategies. According to the World Health Organization, improving health systems and access to essential services is a key goal for many African nations, leading to increased interest in scalable and portable ultrasound technology for underserved areas.

COMPETITIVE LANDSCAPE

The competition in the ultrasound devices market is intense and characterized by the presence of established multinational corporations and specialized regional manufacturers who compete on technology quality and cost efficiency. Major players leverage their extensive research and development capabilities to innovate in artificial intelligence cloud connectivity and miniaturization creating smarter and more portable imaging solutions. The market sees frequent collaborations between device manufacturers and software developers to integrate advanced analytics and automation features directly into ultrasound platforms. Price competition remains significant particularly in the portable and handheld segments where numerous entrants offer affordable alternatives to traditional systems. However differentiation through superior image resolution ergonomic design and comprehensive service support helps premium suppliers maintain higher margins. The shift towards point of care diagnostics has intensified competition as companies race to provide user friendly devices that empower non specialist clinicians. Regulatory compliance across different regions adds complexity requiring companies to maintain flexible and adaptable product portfolios. Supply chain resilience for electronic components has become a key competitive advantage as disruptions can significantly impact production schedules. Companies that successfully balance technological innovation with affordability and strong customer relationships are best positioned to thrive in this dynamic and rapidly evolving market landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global ultrasound devices market include

- General Electric Company (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Toshiba Corporation (Japan)

- Siemens AG (Germany)

- Hitachi Ltd. (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- FUJIFILM Holdings Corporation (Japan)

- Esaote S.p.A. (Italy)

- Mindray Medical International Ltd. (China)

- Analogic Corporation (U.S.)

Top Players in the Global Ultrasound Devices Market

GE HealthCare Technologies Inc

GE HealthCare Technologies Inc is a global leader in medical imaging providing a comprehensive portfolio of ultrasound systems ranging from high end cart based units to portable handheld devices. The company strengthens its market position through continuous innovation in artificial intelligence and cloud connectivity which enhance diagnostic accuracy and workflow efficiency. Recent actions include the launch of advanced software solutions that automate image optimization and measurement tasks reducing operator dependency. GE HealthCare also focuses on expanding its presence in point of care settings by developing rugged and user friendly handheld probes. The company collaborates with healthcare providers to integrate ultrasound data into electronic health records ensuring seamless information exchange. By prioritizing sustainability and digital transformation GE HealthCare delivers reliable and innovative imaging solutions that support diverse clinical needs while maintaining a strong commitment to improving patient outcomes globally.

Koninklijke Philips NV

Koninklijke Philips NV is a prominent player in the ultrasound devices market known for its high quality imaging systems and strong focus on women’s health and cardiology applications. The company offers a wide range of ultrasound platforms equipped with advanced transducer technology and intelligent workflow tools. Philips strengthens its position by investing in research and development to create specialized solutions for emerging markets and remote care settings. Recent initiatives include the expansion of its Lumify mobile ultrasound ecosystem which allows clinicians to perform examinations using smart devices. The company also emphasizes interoperability by integrating its ultrasound systems with broader healthcare IT infrastructure. Philips actively engages in strategic partnerships to enhance its artificial intelligence capabilities and provide predictive analytics. By focusing on value based care and patient centered design Philips continues to deliver cutting edge ultrasound technologies that improve diagnostic confidence and operational efficiency for healthcare providers worldwide.

Siemens Healthineers AG

Siemens Healthineers AG is a key contributor to the ultrasound devices market offering robust and versatile imaging systems designed for various clinical specialties including radiology obstetrics and vascular imaging. The company leverages its expertise in digital health to develop smart ultrasound solutions that incorporate machine learning algorithms for automated assistance. Siemens Healthineers strengthens its market position by expanding its global service network and providing comprehensive training programs for sonographers. Recent actions include the introduction of new probe technologies that offer superior penetration and resolution for difficult to scan patients. The company also focuses on sustainability by designing energy efficient systems and promoting circular economy practices in manufacturing. Siemens Healthineers collaborates with academic institutions to advance clinical research and validate new applications. By combining technological innovation with strong customer support Siemens Healthineers ensures that its ultrasound devices meet the evolving demands of modern healthcare environments and contribute to improved diagnostic standards.

Top Strategies Used by Key Market Participants

Key players in the ultrasound devices market employ several strategic approaches to maintain competitiveness and drive growth. Product innovation is a primary strategy where companies invest in developing artificial intelligence powered features and portable handheld devices to enhance diagnostic accuracy and accessibility. Strategic partnerships with healthcare providers and technology firms allow firms to co develop customized solutions that integrate seamlessly with existing hospital information systems. Geographic expansion is another critical approach enabling companies to establish production facilities and distribution networks in emerging markets to serve local demand efficiently. Additionally companies focus on sustainability initiatives by designing energy efficient systems and promoting recycling programs to align with environmental regulations. Investment in research and development for advanced transducer materials and beamforming technologies helps differentiate products and improve image quality. These strategies collectively help market participants adapt to changing consumer preferences and regulatory requirements while delivering value to customers.

RECENT MARKET HAPPENINGS

- In November 2022, ReCor Medical, Inc. and Otsuka Medical Devices Co., Ltd. submitted Premarket Approval for the Paradise uRDN system to the FDA. This system uses the catheter to be placed in the main renal arteries, which delivers a seven-second ultrasound for lowering blood pressure.

- In November 2022, Royal Philips launched a next-generation compact portable ultrasound solution, the Philips Compact 5000 series, to improve patient outcomes with high-end cart-based ultrasound systems without compromising image quality.

- In November 2022, at the 108th Scientific Assembly of the Radiological Society of North America, Samsung Electronics will introduce the latest artificial intelligence technologies in ultrasound, digital radiography, and mobile computed tomography, improving customer experience to very high levels of satisfaction.

- In November 2022, Advanced Veterinary Ultrasound and Draminski S.A. partnered to introduce better, excellent, rich, and developed systems to market features such as the Draminski Blue, iScan2, and iScan Mini systems.

SEGMENTAL ANALYSIS

The global market for ultrasound devices market has been segmented and sub-segmented based on technology, device display, portability, application and region.

By Technology

- Diagnostic Ultrasound

- 2D Ultrasound

- 3D & 4D Ultrasound

- Doppler Ultrasound

- Therapeutic Ultrasound

- High-intensity Focused Ultrasound

- Extracorporeal Shockwave Lithotripsy

By Device Display

- Color

- Black and White

By Portability

- Trolley/Cart-based

- Compact/Handheld

By Application

- Radiology/General Imaging

- Cardiology

- Obstetrics/Gynecology

- Vascular

- Urology

- Other Applications

- Breast Imaging

- Hepatology

- Anesthesiology

- Emergency Care

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

How much was the global ultrasound devices market worth in 2024?

The global ultrasound devices market was worth USD 9.97 billion in 2024.

Which segment by product had the largest share of the global ultrasound devices market in 2024?

Based on the product, the digital ultrasound segment accounted for the most significant share of the ultrasound devices market in 2024.

Which region had the major share in the global ultrasound devices market in 2024?

Geographically, the North American region was the dominant region in the global market in 2024.

What are a few of the notable players in the ultrasound devices market?

Companies playing a key role in the ultrasound devices market are General Electric Company (U.S.), Koninklijke Philips N.V. (Netherlands), Toshiba Corporation (Japan), Siemens AG (Germany), Hitachi Ltd. (Japan), Samsung Electronics Co., Ltd. (South Korea), FUJIFILM Holdings Corporation (Japan), Esaote S.p.A. (Italy), Mindray Medical International Ltd. (China), and Analogic Corporation (U.S.).

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com