Latin America Media Streaming Market Size, Share, Trends, & Growth Forecast Report – Segmented By Type of Service (Audio Streaming, Video Streaming, and Others (Live Captions, Tapes, And Real-Time Text)), Application (Real-Time Entertainment, Web Browsing & Advertising, Gaming, Social Media, and Online/Distance Learning), End-users (Personal/Household Users, Educational Institutions, and Professional Organizations) and Country (Brazil, Argentina, Chile, and Rest of Latin America) Industry Analysis From 2024 to 2033

Latin America Media Streaming Market Summary

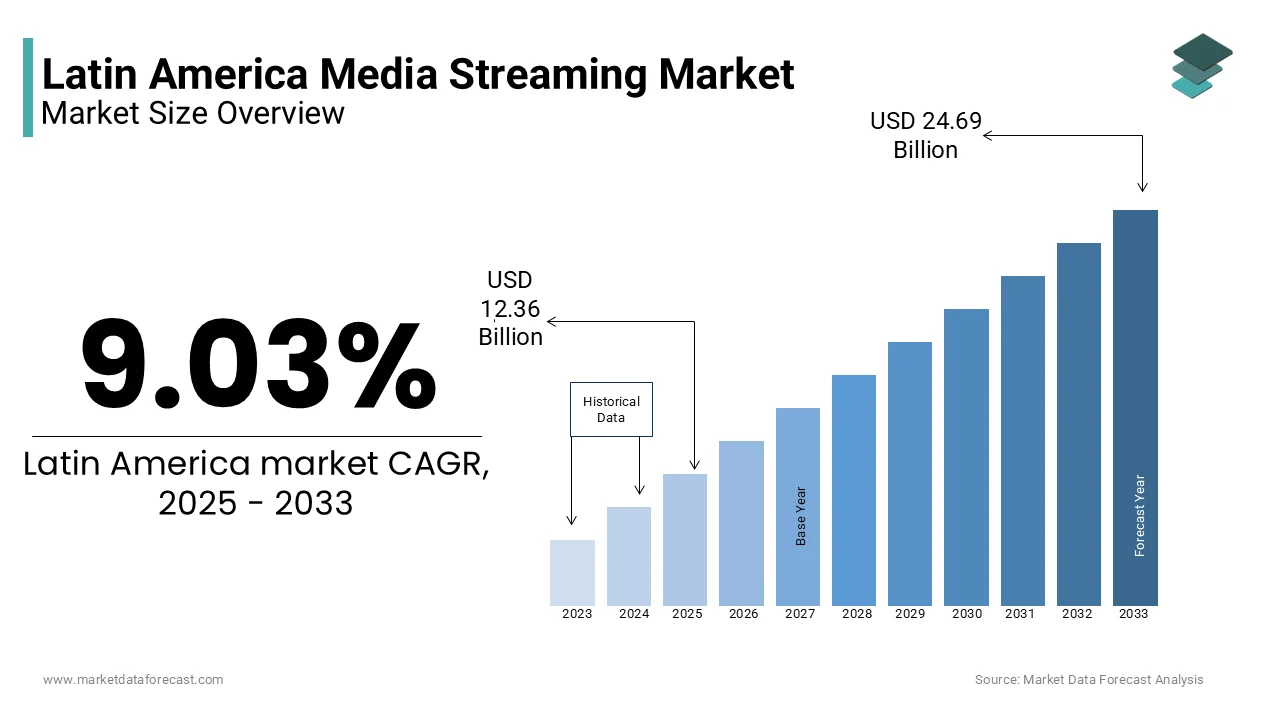

The Latin America media streaming market was valued at USD 11.34 billion in 2024 and is projected to reach USD 24.69 billion by 2033, growing at a CAGR of 9.03% from 2024 to 2033. OTT adoption, mobile device usage, and rising internet penetration are fueling strong regional growth.

Key Market Trends & Insights

- Brazil and Mexico are leading LATAM markets for streaming services.

- Argentina, Brazil, Colombia, Mexico, and Puerto Rico contribute 83% of the total market share.

- Based on service type, the video streaming segment is expected to witness substantial growth.

- Based on application, the real-time entertainment segment led the market in 2024.

- Based on end-users, home users continue to be the largest revenue contributors.

- Despite low broadband access and piracy, OTT platforms are rapidly expanding in LATAM.

Market Size & Forecast

- 2024 Market Size: USD 11.34 Billion

- 2033 Market Size: USD 24.69 Billion

- CAGR (2024–2033): 9.03%

- Brazil & Mexico: Leading contributors to regional growth

- Video Streaming: Key growth segment in the region

Latin America Media Streaming Market Size

The media streaming market in Latin America is anticipated to reach USD 24.69 billion by 2033 from USD 11.34 billion in 2024, at a CAGR of 9.03%. from 2024 to 2033.

Media Streaming Market covers the digital distribution of audiovisual content, including films, series, live sports, and music, delivered via internet-based platforms to consumers across the region. It operates within a rapidly evolving technological and cultural landscape marked by increasing internet accessibility, mobile-first consumption, and a growing appetite for localized content. Internet penetration in Latin America in 2023 is not clearly established at 79%. Also, 43.4% of Brazilian households with TVs had access to a subscription video-on-demand service in late 2022, according to the Brazilian Institute of Public Opinion and Statistics. Moreover, mobile devices dominate streaming viewership in Latin America. These behavioral and infrastructural shifts are redefining media delivery, positioning streaming as the dominant mode of entertainment in both urban and emerging rural markets.

MARKET DRIVERS

Youthful Demographics Driving Demand for Mobile-Friendly Streaming

The region’s youthful demographic structure, which fuels demand for on-demand, mobile-friendly content is a primary driver of the Latin America Media Streaming Market. This cohort increasingly bypasses traditional broadcast television in favor of platforms like Netflix, Disney+, and local services such as Claro Video and Star+ that offer binge-worthy series, live sports, and regional content. Additionally, the rise of social media influencers and digital creators has cultivated a culture of instant gratification and interactive viewing, further reinforcing streaming as the preferred entertainment medium among younger audiences.

Affordable Mobile Data Plans Expanding Streaming Access

The proliferation of affordable mobile data plans, which has dramatically expanded access to streaming services in previously underserved areas, another significant driver. In Colombia, mobile data usage surged consistently since 2020. This affordability has enabled platforms to optimize adaptive streaming technologies that adjust video quality based on bandwidth, ensuring smooth playback even on lower-tier connections. In Peru, where fixed broadband remains limited outside major cities, a large part of streaming is conducted via smartphones. Operators like Movistar and TIM have also bundled streaming subscriptions with data plans, further incentivizing adoption. These developments have transformed mobile networks into primary gateways for digital entertainment across the region.

MARKET RESTRAINTS

Income Inequality Limiting Subscription Affordability

The persistent issue of income inequality, which limits subscription affordability for large segments of the population, is a major restraint in the Latin America Media Streaming Market. According to the World Bank, the Gini coefficient in countries like Brazil and Colombia exceeds 0.53, indicating extreme income disparity. This economic reality makes recurring subscription fees prohibitive for many households, particularly in rural and peri-urban areas. Also, many consumers resort to ad-supported free platforms or unauthorized streaming sites, undermining revenue generation for legitimate providers. Without scalable pricing models or government-backed digital inclusion initiatives, the market faces a structural barrier to universal penetration, constraining growth among economically vulnerable populations.

Fragmented Regulations Affecting Licensing and Compliance

The fragmented regulatory environment across Latin American countries, which complicates content licensing, taxation, and platform compliance, is another critical restraint. Also, a significant number of Latin American nations have established clear digital services tax frameworks applicable to foreign streaming platforms. Meanwhile, content classification and censorship laws vary widely, Colombia promotes local content quotas, while Chile does not. Additionally, intellectual property enforcement remains weak in several countries. These regulatory inconsistencies increase operational complexity and deter longterm investment in localized content development and infrastructure.

MARKET OPPORTUNITIES

Growing Demand for Hyper-Local and Regional Content

The rising production and demand for hyper-local and regional content, which enhances viewer engagement and brand loyalty, is a transformative opportunity. Netflix’s “Narcos” and Disney+’s “Sólo Ases” achieved millions of cumulative hours viewed in the region within their first month of release. Besides, platforms have launched dedicated content hubs focusing on telenovelas, regional music, and indigenous storytelling. These culturally resonant offerings not only differentiate services in a crowded market but also attract advertising and sponsorship from local brands seeking authentic audience engagement, creating a sustainable content economy.

Strategic Bundling with Telecom and Retail Ecosystems

The integration of streaming platforms with telecommunications and retail ecosystems through bundled offerings is another emerging opportunity. Telecom providers are leveraging their extensive customer bases to cross-sell streaming subscriptions, creating synergistic revenue streams. These strategic bundling models lower entry barriers for consumers and enhance platform stickiness, positioning convergence as a key growth lever in the competitive streaming landscape.

MARKET CHALLENGES

Internet Infrastructure Strain Affecting Streaming Quality

The strain on internet infrastructure during peak usage hours, which affects streaming quality and user retention, is a critical challenge facing the Latin America Media Streaming Market. Even in urban centers, sudden spikes in demand, such as during live football matches ,can overwhelm local networks. During the 2022 World Cup, Argentina’s internet traffic surged, causing temporary outages on platforms like Star+. Without substantial investment in fiber expansion and edge computing, service reliability will remain inconsistent, undermining consumer trust and limiting the scalability of high-bandwidth content like 4K and live events.

Subscription Fatigue and Content Fragmentation

The growing consumer fatigue from subscription fragmentation and content siloing is another pressing challenge. In Brazil, churn rates for mid-tier platforms rose in recent years. Consumers are increasingly frustrated by the need to maintain multiple subscriptions to access desired content series on Netflix, and kids’ programming on Disney+. This fragmentation dilutes value perception and encourages password sharing, which affects revenue. Platforms that fail to offer comprehensive libraries or flexible pricing models risk losing market share to consolidated players or ad-supported alternatives, making customer retention a central strategic challenge.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.03% |

| Segments Covered | By Service Type, Application, End-Users, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | Brazil, Argentina, Mexico, and Rest of Latin America |

| Market Leaders Profiled | Amazon Prime Video, Blim, Claro Video, Crackle, HBO, Movistar Play and Netflix |

SEGMENTAL ANALYSIS

By Service Type Insights

The Video Streaming segment was the dominant service type in the Latin America Media Streaming Market by capturing a substantial share of total service-based revenue in 2024. This dominance is primarily driven by the region’s deep cultural affinity for visual storytelling and live entertainment. Like, a large share of internet users in Latin America consume video content daily, with telenovelas, football matches, and reality shows ranking as the most-watched genres. In Brazil, football streaming alone generated substantial number of viewing hours in 2023 during the Brasileirão and Copa Libertadores tournaments. Additionally, the expansion of high-definition and mobile-optimized streaming has improved accessibility, with most of video consumption occurring on smartphones. Platforms and local services have capitalized on this demand by investing heavily in exclusive regional content, solidifying video as the central pillar of digital media consumption.

The fastest-growing segment is Audio Streaming and is projected to expand at a CAGR of 14.9% from 2025 to 2033. This rapid growth is fueled by increasing smartphone penetration and the rising popularity of music, podcasts, and voice-based content among younger demographics. Moreover, a significant share of Latin Americans now use smartphones as their primary internet device, enabling seamless access to audio platforms. In Mexico, Spotify reported millions of active users in 2023, an increase from the previous year. Additionally, podcast consumption has surged. Platforms are also localizing content. With audio requiring less data and offering high engagement during commutes and multitasking, it is becoming a cornerstone of digital media strategy.

By Application Insights

The Real-Time Entertainment segment was the largest application by accounting for 57.3% of total streaming traffic in 2024. This dominance is supported by the region’s strong cultural engagement with live events, particularly sports and music. According to FIFA, the 2022 World Cup final was viewed substantial millions of people across Latin America, with peak concurrent streams exceeding in millions on Star+ and ESPN Play. In Brazil, live concerts streamed via platforms generated millions in views in 2023. Additionally, the rise of digital ticketing and virtual front-row experiences has blurred the line between physical and digital attendance. Platforms are investing in low-latency streaming technologies to minimize delays, with latency reduced on major services. These real-time experiences, combined with social sharing features, create immersive, community-driven viewing, reinforcing the segment’s leadership in engagement and data consumption.

The Online/Distance Learning segment is the fastest-growing application and is anticipated to grow at a CAGR of 13.2% through 2033. This acceleration is driven by institutional digitization and sustained demand for flexible education models post-pandemic. Platforms have adapted content for regional curricula, while universities in Argentina stream degree programs with real-time captioning and interactive Q&A. With government investments in digital classrooms and broadband expansion, streaming is becoming integral to educational equity and lifelong learning across the region.

By End-Users Insights

The Personal/Household Users segment represented the prominent end-user by contributing a substantial share of total streaming consumption in 2024. This dominance is rooted in the widespread adoption of smart devices and the cultural centrality of home-based entertainment. The rise of multi-screen households, where smartphones, tablets, and smart TVs are used simultaneously, has further amplified data usage. Besides, family subscription plans and parental controls have made platforms more accessible to diverse age groups. These behavioral and technological trends confirm that personal entertainment remains the primary driver of streaming demand across the region.

The Educational Institutions segment is the fastest-growing end-user and is projected to grow at a CAGR of 12.8% from 2025 to 2033. This growth is driven by public and private investments in digital education infrastructure and hybrid learning models. Large number of schools and universities in Latin America adopted streaming platforms for instruction between 2021 and 2023. Additionally, universities offer streaming lectures, thesis defenses, and career workshops to enhance student engagement. With governments prioritizing digital inclusion and lifelong learning, educational streaming is evolving from a contingency tool to a permanent component of institutional strategy.

COUNTRY-LEVEL ANALYSIS

Brazil Media Streaming Market Insights

Brazil held the largest share of the Latin America Media Streaming Market at 41.5% of total regional revenue in 2024. The country’s market status is defined by its massive population, robust digital infrastructure, and vibrant content production ecosystem. With over 157 million internet users, Brazil is the region’s largest digital consumer base. The country leads in original content creation. Additionally, football streaming rights have become a major revenue driver. Mobile data affordability has also surged. These factors position Brazil as both a consumption and content innovation hub in Latin America.

Mexico Media Streaming Market Insights

Mexico is a pivotal market due to its large, young population and strategic content hub status. The country’s market status is defined by high mobile usage and growing demand for Spanish-language content. Mexico is a production powerhouse. The government’s initiative has expanded broadband to large number of rural users. Additionally, live sports, particularly Liga MX football, drive peak streaming traffic. These factors position Mexico as a key growth engine and content exporter in the regional streaming landscape.

KEY MARKET PLAYERS

Amazon Prime Video, Blim, Claro Video, Crackle, HBO, Movistar Play and Netflix are the leading players in the Latin American media streaming market.

TOP LEADING PLAYERS IN THE MARKET

Netflix

Netflix has solidified its leadership in the Latin America Media Streaming Market through aggressive localization, original content production, and adaptive technology deployment. The company has invested heavily in Spanish and Portuguese-language originals. In Brazil, “Sintonia” and “Ilha de Ferro” achieved record engagement, while Mexican series like “Club de Cuervos” have gained cross-border popularity. Netflix has also optimized its streaming algorithms for low-bandwidth environments, enabling HD playback on 3G networks in rural areas. It introduced mobile-only subscriptions in Colombia and Peru to target cost-sensitive users, significantly expanding its reach. Additionally, the platform collaborates with local telecom providers like Claro and Movistar to offer zero-rated access, ensuring broader penetration across diverse socioeconomic segments.

Disney+

Disney+ has rapidly expanded its footprint in Latin America by leveraging its global content library and strategic acquisitions such as Star+ to strengthen sports and general entertainment offerings. Since its 2020 launch, the platform has localized over 95% of its content with Spanish and Portuguese dubbing, including region-specific subtitles for indigenous languages in Guatemala and Bolivia, as reported by the Disney Latin America Content Division. The integration of ESPN’s live sports, particularly football, NBA, and UFC, under the Star+ bundle has driven subscriber growth, with over 15 million regional users by mid-2024. Disney+ also launched educational partnerships in Chile and Argentina, offering curated content for schools. Its investment in local originals, including the Colombian series “Las Detectives” and the Brazilian film “Minha Vida em Marte”, reflects a commitment to cultural relevance. These initiatives position Disney+ as a premium, family-oriented platform with cross-generational appeal.

Amazon Prime Video

Amazon Prime Video distinguishes itself in the Latin America Media Streaming Market through integration with Amazon’s e-commerce ecosystem and innovative pricing models. The platform offers Prime Video as part of bundled subscriptions with free shipping and digital music, increasing customer stickiness in countries like Mexico and Brazil. It has also invested in regional sports rights, securing exclusive streaming of LFA (Liga de Fútbol Americano) games in Mexico and select Brasileirão matches in partnership with broadcasters. Amazon’s AI-driven recommendation engine personalizes content discovery, improving engagement, particularly among younger demographics. Additionally, it supports local filmmakers through the “Prime Video Direct” program, enabling independent creators in Peru and Colombia to monetize content directly. These strategies underscore Amazon’s hybrid approach, combining global scale with hyper-local engagement.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Latin America Media Streaming Market are deploying multifaceted strategies centered on content localization, technological adaptation, and strategic bundling. Companies are investing heavily in original regional productions to enhance cultural relevance and viewer loyalty, particularly in genres like telenovelas, football, and urban music. Platforms are optimizing streaming efficiency for low-bandwidth environments, enabling seamless playback on mobile networks across rural and underserved areas. Strategic partnerships with telecommunications providers allow zero-rated access and bundled data plans, lowering entry barriers. Subscription models are being diversified, including mobile-only, ad-supported, and short-term passes to accommodate economic variability. Integration with e-commerce and payment platforms enhances accessibility, particularly where credit card penetration is low. Additionally, firms are expanding into adjacent sectors such as live sports, education, and podcasting to increase engagement. Cybersecurity and data compliance are being strengthened to meet evolving regulatory demands. These strategies collectively aim to balance scalability, affordability, and cultural resonance in a fragmented, fast-evolving market.

COMPETITION OVERVIEW

The competition in the Latin America Media Streaming Market is intensifying as global platforms contend with regional players and evolving consumer expectations. While multinational giants like Netflix, Disney+, and Amazon Prime Video dominate through content investment and technological scale, local services such as Claro Video, Vix, and HBO Max Latin America leverage regional expertise and telecom integration to maintain relevance. The market is characterized by price sensitivity, content fragmentation, and infrastructure disparities, forcing operators to innovate in delivery models and pricing. Differentiation is increasingly achieved through live sports rights, hyper-local originals, and mobile-first experiences. Regulatory divergence and digital inequality further complicate scalability. Success hinges on balancing global resources with local agility, as platforms compete not only on library size but on accessibility, cultural alignment, and user experience. The competitive edge now lies in ecosystem integration, adaptive technology, and sustainable content pipelines tailored to Latin America’s diverse linguistic and socioeconomic landscape.

MARKET SEGMENTATION

This research report on the Latin American media streaming market has been segmented and sub-segmented based on type of service, applications, end users, and regions.

By Service Type

- Audio Streaming

- Video Streaming

- Others (Live Captions, Tapes, And Real-Time Text)

By Application

- Real-Time Entertainment

- Web Browsing & Advertising

- Gaming

- Social Media

- Online/Distance Learning

By End-Users

- Personal/Household Users

- Educational Institutions

- Professional Organizations

By Country

- Mexico

- Brazil

- Argentina

- Chile

- Rest of Latin America

Frequently Asked Questions

What are the primary factors driving the growth of the media streaming market in Latin America?

Key factors include increasing internet penetration, the rising popularity of smart devices, a growing middle class with higher disposable income, and a shift in consumer preference from traditional TV to on-demand content.

What are the main challenges faced by streaming platforms in Latin America?

Challenges include internet connectivity issues in rural areas, high competition among platforms, content localization, and piracy.

How are streaming platforms addressing the issue of content localization in Latin America?

Streaming platforms are investing in local content production, offering subtitles and dubbing in Spanish and Portuguese, and partnering with regional content creators to make their offerings more appealing to local audiences.

How are regulatory policies affecting the media streaming market in Latin America?

Regulatory policies vary by country, with some governments implementing measures to support local content production and others imposing taxes on digital services. These policies can impact the operational strategies and pricing models of streaming platforms.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com