Global Zika Virus Vaccines Market Size, Share, Trends & Growth Forecast Report By Type (Therapeutic Vaccines, Preventive Vaccines), End-user and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Global Zika Virus Vaccines Market Report Summary

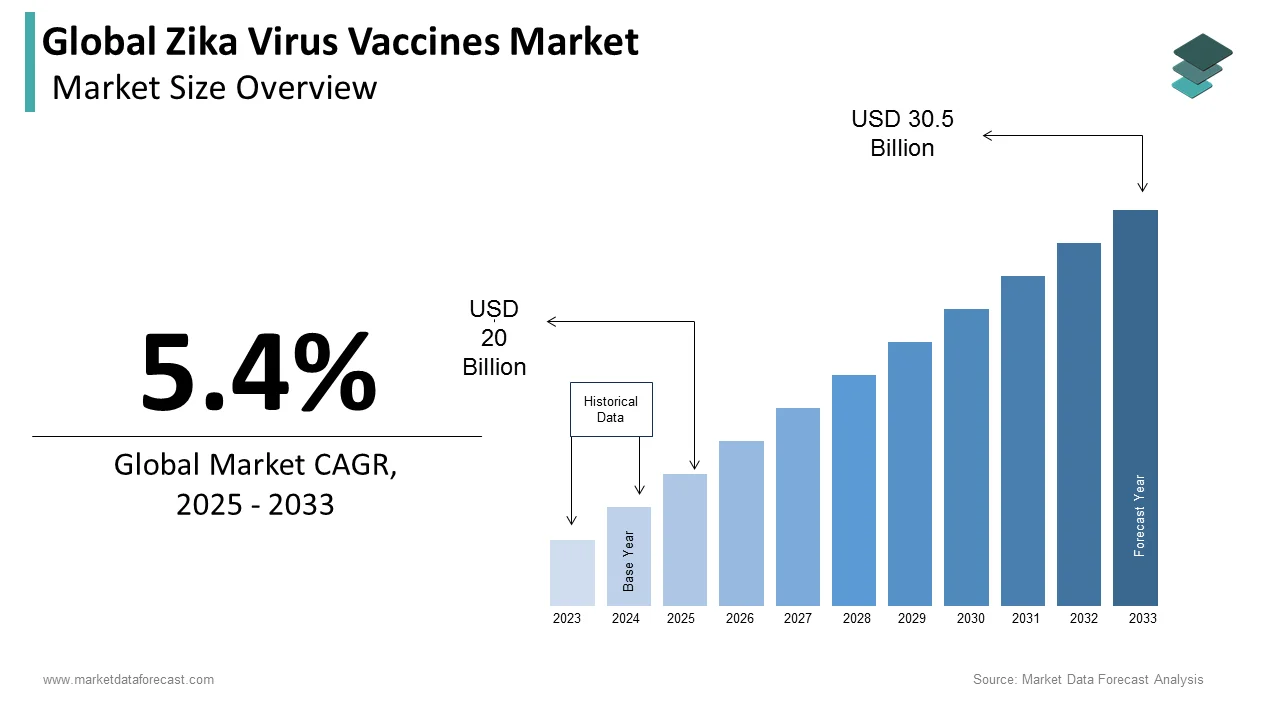

The global Zika virus vaccines market was valued at USD 20 billion in 2025 and is projected to grow from USD 21.08 billion in 2026 to USD 32.11 billion by 2034, registering a CAGR of 5.4% from 2026 to 2034. Market growth is driven by increasing awareness of mosquito-borne viral diseases, ongoing vaccine research and development efforts, and growing investments in global infectious disease preparedness. Concerns regarding the neurological complications associated with Zika virus infections, particularly congenital abnormalities in newborns, continue to support demand for preventive vaccination strategies. Furthermore, advancements in vaccine technologies and collaborative public health initiatives are contributing to market expansion worldwide.

Key Market Trends

- Increasing investment in infectious disease vaccine research and development.

- Growing focus on preventive vaccination strategies against mosquito-borne diseases.

- Rising collaboration between government agencies, research institutions, and vaccine manufacturers.

- Expansion of clinical trials for next-generation viral vaccines.

- Strengthening global emphasis on epidemic preparedness and outbreak prevention programs.

Segmental Insights

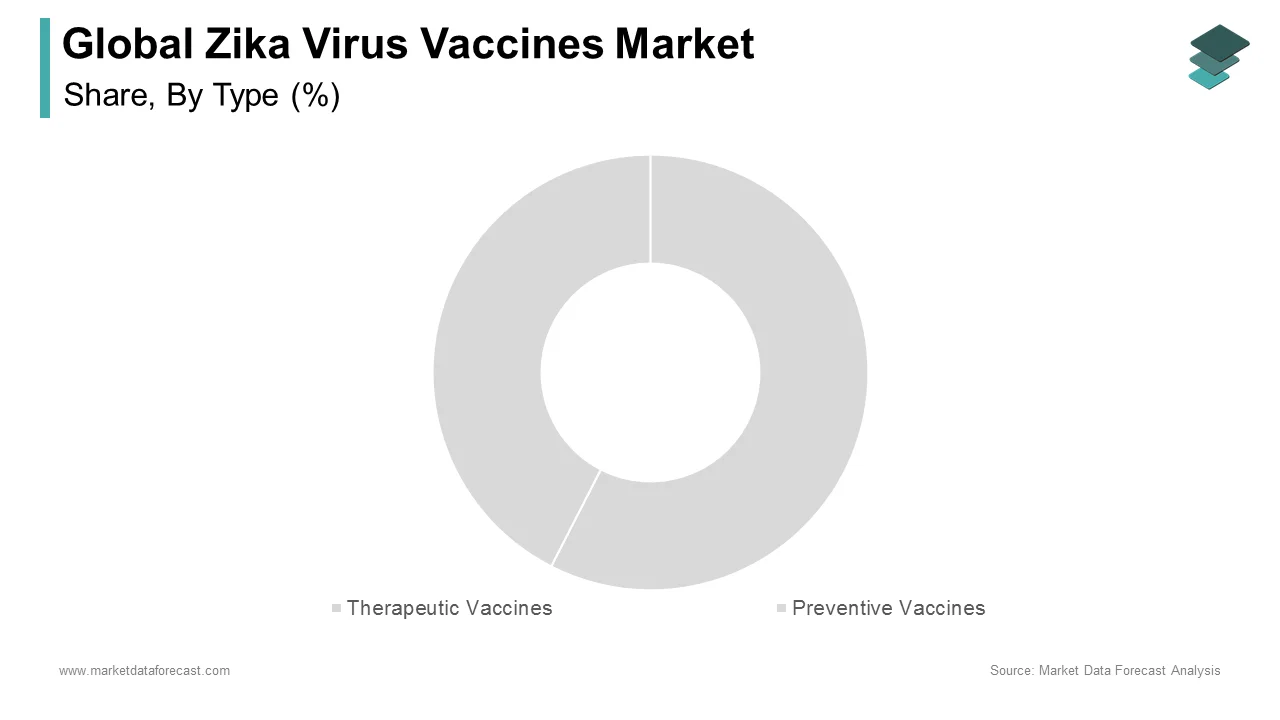

Based on type, the preventive vaccines segment dominated the global Zika virus vaccines market in 2025 by accounting for 65.4% market share, driven by increasing efforts to prevent disease transmission and reduce the risk of Zika-related complications.

Based on end user, the hospitals segment held the largest share of the market with 50.2% in 2025, supported by their capacity to manage large-scale vaccination programs, provide specialized care, and coordinate public health immunization initiatives.

Regional Insights

The global Zika virus vaccines market is witnessing steady growth across major regions, supported by increasing disease surveillance programs, vaccine development initiatives, and public health investments.

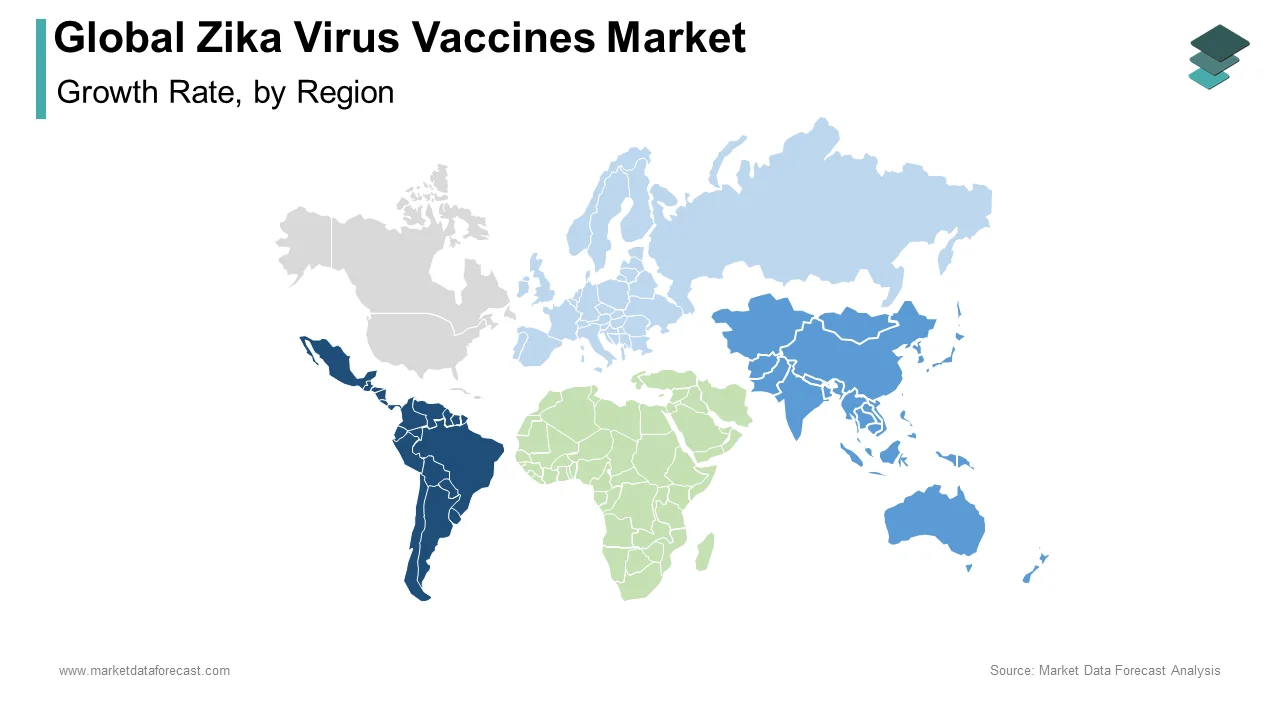

- North America dominated the global market in 2025 with 45.3% share, driven by strong research capabilities, significant funding for infectious disease prevention, and active participation in vaccine development programs.

- Europe maintains a stable position in the market, supported by robust regulatory frameworks, collaborative vaccine research initiatives, and increasing public health preparedness measures.

- Asia-Pacific is emerging as a key growth region due to rising awareness of mosquito-borne diseases, expanding healthcare infrastructure, and increasing investments in vaccine development and immunization programs.

Competitive Landscape

The global Zika virus vaccines market is characterized by the presence of pharmaceutical companies, biotechnology firms, and vaccine developers focusing on innovative vaccine technologies and infectious disease prevention strategies. Market participants are emphasizing research collaborations, clinical trial advancements, and expansion of vaccine development pipelines to strengthen market positioning. Strategic partnerships with public health organizations and investments in emerging vaccine platforms are shaping competitive dynamics across the market.

Prominent companies operating in the global Zika virus vaccines market include Takeda Pharmaceutical Co. Ltd., NewLink Genetics Co., Immunovaccine Inc., GeneOne Life Science Inc., GlaxoSmithKline PLC, Inovio Pharmaceuticals, Inc., Bharat Biotech International Ltd., Hawaii Biotech Inc., and Sanofi S.A.

Global Zika Virus Vaccines Market Size

The global zika virus vaccines market was worth US$ 20 billion in 2025 and is anticipated to reach a valuation of US$ 32.11 billion by 2034 from US$ 21.08 billion in 2026, and it is predicted to register a CAGR of 5.4% during the forecast period 2026 to 2034.

Zika virus vaccines are a specialized segment within the global immunization landscape focused on developing prophylactic solutions against the Zika virus, a mosquito-borne flavivirus primarily transmitted by Aedes species. Although the acute phase of the 2015 to 2016 epidemic has subsided, the persistent threat of congenital Zika syndrome and neurological complications such as Guillain-Barré syndrome maintains scientific and public health urgency. The World Health Organization identifies Zika as a continuing public health concern due to its potential for re-emergence in susceptible populations. According to the CDC, during the peak outbreak year of 2016, US Territories reported over 36,000 cases (mostly locally acquired), while the US States reported 5,168 cases (mostly travel-associated). Globally, the number of suspected cases was not merely "thousands" but estimated in the millions (e.g., Brazil alone estimated 440,000–1,300,000 cases). The Pan American Health Organization indicates that more than 80 countries and territories have experienced evidence of mosquito-borne transmission. Clinical trials are currently evaluating various vaccine candidates, including DNA-based mRNA and inactivated virus platforms. The primary target demographic includes women of childbearing age and travelers to endemic regions. Regulatory agencies such as the European Medicines Agency and the US Food and Drug Administration continue to monitor development progress. The market is driven by the need for herd immunity to prevent future outbreaks. Research institutions and pharmaceutical companies collaborate to overcome scientific hurdles related to immune response durability and safety profiles. This sector remains critical for global health security against emerging infectious diseases.

MARKET DRIVERS

Persistent Risk of Congenital Abnormalities and Neurological Complications

The severe health consequences associated with Zika virus infection, particularly congenital Zika syndrome, are paramount drivers of the global Zika virus vaccines market. Congenital Zika syndrome causes microcephaly and other severe brain defects in infants born to infected mothers. According to the World Health Organization, there is a strong scientific consensus that Zika virus infection during pregnancy is a cause of these birth defects. Data from the Brazilian Ministry of Health revealed that over 3000 cases of microcephaly were reported in 2016 alone, a significant increase from previous years. This tragic outcome creates an urgent moral and medical imperative for preventive measures. The long-term care costs for children with congenital disabilities place a substantial burden on healthcare systems and families. As per the Centers for Disease Control and Prevention, the Zika virus can also trigger Guillain-Barré Syndrome, a rare neurological disorder that can lead to paralysis. The fear of these devastating outcomes drives government funding and private investment into vaccine research. Public health authorities prioritize vaccines that can protect women before and during pregnancy. The emotional and social impact of the epidemic has galvanized international support for rapid vaccine deployment. Stakeholders recognize that vaccination is the most effective strategy to prevent transmission to fetuses. This health crisis context ensures sustained interest and resource allocation for Zika vaccine candidates despite fluctuations in active case numbers.

Expansion of Vector Habitat Due to Climate Change

Climate change and urbanization are expanding the geographic range of Aedes mosquitoes, which is also propelling the expansion of the Zika virus vaccines market. These mosquitoes are primary vectors for Zika virus transmission, thereby increasing the at-risk population and driving vaccine demand. Rising global temperatures allow these mosquitoes to survive in higher latitudes and altitudes previously considered safe. According to the European Centre for Disease Prevention and Control, the suitable habitat for Aedes albopictus has expanded significantly across Europe in recent decades. Warmer climates accelerate the mosquito life cycle and increase the frequency of biting, enhancing transmission efficiency. Urbanization creates ideal breeding grounds with stagnant water in containers and poor waste management. The World Meteorological Organization states that extreme weather events, such as heavy rainfall and flooding, create temporary breeding sites that boost mosquito populations. These environmental changes mean that regions without prior exposure to Zika are now vulnerable. Travelers returning from endemic areas can introduce the virus to local mosquito populations, sparking autochthonous transmission. As per the Pan American Health Organization, the risk of spread remains high in areas with competent vectors and low population immunity. This expanding threat landscape necessitates proactive vaccination strategies rather than reactive responses. Governments in temperate zones are increasingly aware of the need for preparedness. The anticipation of future outbreaks in new regions stimulates market interest and regulatory readiness for vaccine approval.

MARKET RESTRAINTS

Declining Incidence Rates and Shifting Public Health Priorities

The significant decline in reported cases since the 2016 peak has led to reduced urgency and shifting public health priorities, which is a major restraint on the Zika virus vaccines market. As per the World Health Organization, the number of confirmed Zika cases dropped dramatically in subsequent years as population immunity increased and vector control measures were implemented. With fewer active infections, governments and health organizations have redirected resources toward other pressing health crises, such as the COVID-19 pandemic and seasonal influenza. This shift in focus results in decreased funding for Zika-specific research and development programs. Pharmaceutical companies face challenges in justifying the high costs of clinical trials when the immediate commercial return appears limited. The lack of large-scale outbreaks makes it difficult to conduct efficacy trials that require high incidence rates to demonstrate protection. According to the Centers for Disease Control and Prevention, current surveillance data show only sporadic cases in most previously affected regions. This low disease burden reduces the perceived immediate need for a licensed vaccine among policymakers and payers. Investors may hesitate to commit capital to a market with uncertain short-term demand. The perception of Zika as a contained threat rather than an ongoing emergency dampens market momentum. Sustaining interest and funding in the absence of a visible crisis requires strong advocacy and long-term strategic planning.

Complexities in Clinical Trial Design and Ethical Considerations

Designing clinical trials for these vaccines is also a significant scientific and ethical barrier that constrains the expansion of the Zika virus vaccine market. The primary target population for many candidates is women of childbearing age, including pregnant women, who are often excluded from early-phase trials due to safety concerns. According to the World Health Organization, conducting trials in pregnant women requires rigorous ethical oversight and extensive preclinical data to ensure fetal safety. This necessity prolongs the development timeline and increases costs. Furthermore, the fluctuating nature of Zika outbreaks makes it difficult to predict where and when efficacy trials can be conducted. Researchers need sites with high transmission rates to statistically validate vaccine effectiveness, but these hotspots are unpredictable. As per the National Institutes of Health, the phenomenon of antibody-dependent enhancement poses a theoretical risk where prior immunity to related flaviviruses like dengue could worsen Zika infection. This potential interaction complicates safety assessments and requires careful monitoring. Recruiting participants in areas with declining incidence is challenging due to lower perceived risk. Ethical considerations regarding placebo use in pregnant populations add another layer of complexity. Regulatory agencies demand robust data on long-term immunity and safety before approval. These scientific and ethical hurdles slow down the progression of candidates from Phase 2 to Phase 3 trials, delaying market entry and commercialization.

MARKET OPPORTUNITIES

Integration with Combination Vaccines for Flaviviruses

The development of combination vaccines that protect against multiple flaviviruses, such as dengue, yellow fever, and Zika simultaneously, is a major opportunity in the Zika virus vaccines market. Since these viruses share similar vectors and geographic distributions, a multivalent vaccine would offer comprehensive protection and improve compliance. According to the World Health Organization, co-circulation of dengue and Zika is common in many tropical regions, making separate vaccinations logistically challenging. A combination vaccine would reduce the number of injections required, lowering healthcare costs and increasing acceptance among travelers and residents. Pharmaceutical companies are exploring chimeric vaccine platforms that can elicit immune responses against several viruses at once. As per the National Institute of Allergy and Infectious Diseases, research into tetravalent dengue vaccines has provided valuable insights that can be applied to Zika inclusion. This approach appeals to public health programs aiming for broad-spectrum vector-borne disease control. Travel medicine clinics would benefit from offering a single solution for tourists visiting endemic areas. The commercial potential of a combination product is higher than that of a standalone Zika vaccine due to the larger addressable market. Regulatory pathways for combination vaccines are becoming more defined, facilitating development. Collaborations between experts in different flavivirus fields are accelerating innovation. This strategic direction offers a viable path to commercial viability despite the low standalone demand for Zika immunization.

Government Funding and International Collaborative Initiatives

Sustained government funding and international collaborative initiatives pave the way for advancing vaccine candidates through the development pipeline, which is likely to boost the expansion of the Zika virus vaccines market. Recognizing Zika as a global health security threat, organizations such as the Coalition for Epidemic Preparedness Innovations provide financial support for late-stage clinical trials. According to the World Health Organization, international cooperation is essential for sharing data, biological samples, and clinical trial infrastructure. Governments in endemic countries are increasingly investing in local manufacturing capabilities to ensure vaccine accessibility. The European Union has funded several research consortia focused on arbovirus vaccines, fostering innovation across member states. As per the Centers for Disease Control and Prevention, public-private partnerships facilitate the translation of academic research into commercial products. These collaborations reduce the financial risk for individual companies and accelerate regulatory approvals through harmonized standards. Global health initiatives prioritize equitable access, creating markets in low and middle-income countries through tiered pricing models. The establishment of stockpiles for emergency response provides a guaranteed purchase mechanism for manufacturers. International travel regulations may eventually mandate proof of vaccination for entry into certain regions, driving demand. Continued diplomatic and scientific engagement keeps Zika on the global health agenda. Leveraging these funding streams and partnerships allows developers to overcome resource constraints. This supportive ecosystem enables the completion of necessary studies and prepares the market for eventual licensure and distribution.

MARKET CHALLENGES

Uncertainty Regarding Long-Term Immunity and Correlates of Protection

Scientific uncertainty surrounding the duration of vaccine-induced immunity and the identification of reliable correlates of protection remains a major challenge in the Zika virus vaccine market. Unlike some viruses, where antibody levels directly correlate with protection, the immune response to Zika is complex and not fully understood. According to the World Health Organization, it remains unclear how long protection lasts after natural infection or vaccination, raising questions about the need for booster doses. This uncertainty complicates dosing regimens and long-term efficacy predictions. Clinical trials must follow participants for extended periods to gather durability data, which delays regulatory submission. As per the National Institutes of Health, animal models do not always accurately predict human immune responses, leading to discrepancies in preclinical and clinical results. The potential for waning immunity could undermine public confidence and require costly revaccination campaigns. Determining the minimum antibody threshold needed for protection is critical for licensure but remains elusive. Variability in individual immune responses adds another layer of complexity. Without clear correlates of protection, regulators may require large-scale efficacy trials rather than surrogate endpoint approvals. This scientific gap increases development risks and costs. Manufacturers must design flexible trial protocols to adapt to emerging immunological data. Addressing these knowledge gaps is essential for creating a viable and effective vaccine product.

Regulatory Hurdles and Lack of Standardized Guidelines

Navigating the regulatory landscape for these vaccines is a significant hurdle for the Zika virus vaccine market. This is due to the lack of standardized global guidelines and evolving requirements. Since no Zika vaccine has been licensed yet, regulatory agencies are developing frameworks in real time, creating uncertainty for developers. According to the European Medicines Agency, sponsors must provide extensive data on safety in pregnant women and potential interactions with other flavivirus infections. The absence of established precedents means that each candidate faces unique scrutiny and potentially changing expectations. As per the US Food and Drug Administration, demonstrating safety in diverse populations, including children and the elderly, requires complex trial designs. Harmonizing regulatory requirements across different jurisdictions is difficult, delaying global launch strategies. Manufacturers must engage in continuous dialogue with multiple agencies, increasing administrative burdens. The fast-track designation processes are available but require compelling preliminary data. Regulatory bodies are cautious due to the theoretical risk of antibody-dependent enhancement, demanding rigorous long-term safety monitoring. This caution extends the review timeline and increases compliance costs. Small biotechnology firms may struggle to meet these demanding regulatory standards without substantial resources. The dynamic nature of regulatory science for emerging diseases creates a moving target for developers. Establishing clear and consistent international guidelines is crucial to streamlining the approval process and facilitating timely market entry for life-saving vaccines.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Application, Type, Dermatoscopes, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Takeda Pharmaceutical Co. Ltd., NewLink Genetics Co., Immunovaccine Inc., GeneOne Life Science Inc., GlaxoSmithKline PLC, Inovio Pharmaceuticals, Inc., Bharat Biotech International Ltd., Hawaii Biotech Inc., and Sanofi S.A., and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The preventive vaccines segment led the Zika virus vaccines market and captured a 65.4% share in 2025. This leading position of the segment was mainly attributed to the protection of women of childbearing age and fetuses. They serve as the primary strategy for controlling transmission and protecting vulnerable populations from infection. The fundamental goal of public health initiatives is to establish herd immunity before outbreaks occur, making prophylactic immunization the standard approach. A key driver for the dominance of preventive vaccines is the critical need to protect women of childbearing age and their fetuses from congenital Zika syndrome. This severe condition causes microcephaly and other neurological defects that have lifelong consequences. According to the World Health Organization, the risk of birth defects is highest when infection occurs during the first trimester of pregnancy. Preventive vaccination offers the only reliable method to ensure immunity before conception or early pregnancy. Public health campaigns in endemic regions focus heavily on educating women about the importance of pre-pregnancy immunization. Data from the Pan American Health Organization indicates that millions of women live in areas with ongoing Zika transmission risk. Governments prioritize funding for preventive candidates that demonstrate safety in animal models of pregnancy. The ethical imperative to prevent irreversible fetal damage drives regulatory agencies to expedite reviews of safe preventive options. Healthcare providers recommend vaccination as part of preconception care packages. This proactive approach reduces the burden on neonatal intensive care units and special education services. The clear clinical benefit of preventing vertical transmission ensures that preventive vaccines remain the central focus of research and development efforts. Stakeholders recognize that treating established infections is far less effective than preventing them entirely.

The integration of Zika vaccines into national immunization programs serves as a major factor sustaining the leadership of the preventive segment. Countries with high Zika prevalence are developing strategies to include the vaccine in routine childhood or adolescent schedules once licensed. As per the Centers for Disease Control and Prevention, incorporating new vaccines into existing infrastructure maximizes coverage and cost efficiency. Preventive vaccines align with the operational models of public health systems that rely on scheduled visits for multiple immunizations. This systematic delivery ensures high uptake rates among target demographics without requiring individual patient initiation. Governments allocate budgets for mass procurement and distribution logistics specifically for preventive agents. The World Health Organization supports member states in strengthening their cold chain capacities to handle new vaccine introductions. School-based vaccination campaigns are being planned in several Latin American countries to reach adolescents before they enter reproductive years. These structured programs create predictable demand volumes that attract pharmaceutical manufacturers. The stability provided by government contracts encourages long-term investment in production facilities. Preventive vaccines also offer economic advantages by reducing healthcare costs associated with treating complications. Policy makers view prevention as a sustainable solution for managing arboviral threats. This institutional support cements the position of preventive vaccines as the cornerstone of Zika control strategies globally.

The therapeutic vaccines segment is anticipated to witness the fastest CAGR of 12.5% during the forecast period. This swift growth is propelled by the emerging understanding of Zika persistence and the need for treatments for infected individuals. The growing recognition that the Zika virus can persist in certain body fluids and tissues for extended periods is driving demand for therapeutic vaccines. Recent studies indicate that the virus may remain detectable in semen and other compartments long after acute symptoms resolve. According to the National Institutes of Health, persistent viral reservoirs could contribute to chronic neurological symptoms and sexual transmission risks. Therapeutic vaccines aim to boost the immune system’s ability to clear these residual viruses. Patients suffering from post-Zika syndrome report fatigue, joint pain, and cognitive issues that lack effective treatments. Clinical trials are exploring candidates that enhance T cell responses to eliminate infected cells. This unmet medical need creates a niche market for therapeutic interventions. Researchers are investigating whether therapeutic vaccination can reduce the duration of viremia and the severity of complications. The potential to improve the quality of life for chronically affected individuals attracts specialized funding. Pharmaceutical companies see an opportunity to differentiate their portfolios by addressing chronic phases of the disease. As scientific evidence mounts regarding viral persistence, the clinical justification for therapeutic approaches strengthens. This segment offers hope for patients who were infected during previous outbreaks and continue to suffer. The novelty of this approach drives innovation and accelerates research activities in academic and industrial settings.

The application of therapeutic vaccines for managing severe neurological complications such as Guillain-Barré syndrome represents a significant growth driver. Although rare, these complications cause significant morbidity and require intensive medical care. As per the European Centre for Disease Prevention and Control, Zika infection is a confirmed trigger for Guillain-Barré syndrome in susceptible individuals. Current treatments are supportive rather than curative, highlighting the need for targeted immunotherapies. Therapeutic vaccines could modulate the immune response to prevent nerve damage or promote recovery. Early phase trials are assessing the safety of administering vaccines to patients with recent neurological onset. The high cost of long-term rehabilitation for paralysis patients creates economic pressure to find effective interventions. Healthcare systems are interested in therapies that reduce hospital stays and disability rates. Research collaborations between neurologists and immunologists are advancing this field. The potential to halt disease progression makes therapeutic vaccines attractive for emergency use authorizations. Regulatory pathways for orphan drugs may facilitate faster approval for these specific indications. Investors are drawn to the high-value proposition of treating severe complications. As clinical data emerges demonstrating efficacy in neurological contexts, the segment will experience accelerated growth. This specialized application expands the market beyond simple prevention into active disease management.

By End-User Insights

In 2025, the hospitals segment was the largest in the Zika virus vaccines market and occupied a 50.2% share because of its capacity to handle large-scale vaccination campaigns and manage complex cases. They serve as the primary nodes for public health implementation and emergency response. Hospitals possess the necessary infrastructure and staffing to execute mass vaccination campaigns efficiently during outbreaks or routine programs. They have dedicated cold storage facilities, trained nursing staff, and administrative systems for tracking patient records. According to the World Health Organization, hospitals are the preferred sites for introducing new vaccines due to their ability to monitor adverse events immediately. This capability is crucial for maintaining public trust and ensuring safety compliance. Large urban hospitals can process thousands of doses daily, reducing wait times and increasing coverage. Government contracts often designate major medical centers as distribution hubs for regional vaccination efforts. The centralized nature of hospital operations allows for standardized protocols and quality control. Electronic health records in hospitals facilitate accurate documentation of vaccination status, which is essential for epidemiological surveillance. During emergencies, hospitals can rapidly scale up operations by repurposing outpatient departments. Their reputation as trusted medical institutions encourages higher patient acceptance rates. Public health authorities rely on hospitals to reach diverse demographic groups, including pregnant women and children. The logistical advantage of hospitals ensures they remain the dominant channel for vaccine administration. Their role extends beyond injection to include education and counseling services. This comprehensive service model supports sustained market leadership in the end-user landscape.

The role of hospitals in managing high-risk pregnancies and Zika-related complications drives their dominance as an end user. Pregnant women with suspected or confirmed Zika infection require specialized monitoring and diagnostic services available primarily in hospital settings. As per the Centers for Disease Control and Prevention, serial ultrasounds and amniocentesis are recommended for infected pregnancies to detect fetal abnormalities. These procedures are performed in hospital obstetrics departments where immediate intervention is possible if complications arise. Hospitals provide multidisciplinary care involving obstetricians, infectious disease specialists, and neonatologists. This integrated approach ensures that vaccination decisions are made in the context of overall maternal health. Women receiving care in hospitals are more likely to be offered preventive vaccines as part of their prenatal protocol. The presence of neonatal intensive care units allows for immediate management of infants born with congenital Zika syndrome. Hospitals serve as referral centers for complex cases from smaller clinics. This concentration of high-risk patients creates a consistent demand for vaccines within hospital pharmacies. Insurance reimbursements for hospital-based services often cover vaccination costs more readily than in outpatient settings. The clinical necessity of hospital care for severe cases reinforces their central position in the market. Their ability to provide a continuum of care from prevention to treatment sustains their leadership.

The research institutes segment is likely to experience the fastest CAGR of 14.2% from 2026 to 2034 due to the intense focus on developing next-generation vaccine candidates and understanding viral pathogenesis. Research institutes are conducting a significant portion of the clinical trials and preclinical studies required for Zika vaccine development. These entities possess specialized laboratories and expertise in virology, immunology, and clinical research methodology. According to the National Institutes of Health, academic and private research institutes are leading the innovation in mRNA and DNA vaccine platforms for Zika. They collaborate with pharmaceutical companies to test novel adjuvants and delivery systems. The need for rapid data generation to support regulatory filings drives increased activity in these facilities. Research institutes often receive government grants specifically earmarked for emerging infectious disease research. This funding enables them to purchase advanced equipment and recruit top talent. The competitive landscape encourages institutes to accelerate their timelines to publish findings and secure patents. Multi-center trials coordinated by research networks enhance statistical power and generalizability of results. Institutes are also exploring challenge studies in controlled environments to evaluate efficacy quickly. The dynamic nature of research requires the flexible infrastructure that institutes provide. Their role in bridging basic science and clinical application is critical for market advancement. As more candidates enter late-stage trials, the volume of work in research institutes increases. This trend ensures their status as the fastest-growing segment in the end-user category.

Strategic collaborations between research institutes and global health organizations are accelerating growth in this segment. Entities such as the Coalition for Epidemic Preparedness Innovations partner with institutes to fund and coordinate vaccine development. As per the World Health Organization, these partnerships facilitate knowledge sharing and resource pooling across borders. Research institutes benefit from access to international clinical trial sites and biological samples. These collaborations reduce financial risks and streamline regulatory processes through harmonized standards. Institutes participate in global consortia aimed at creating platform technologies applicable to multiple flaviviruses. This broadens their research scope and increases funding opportunities. The emphasis on open science encourages data transparency and faster progress. Institutes host conferences and workshops that bring together stakeholders from academia, industry, and government. These interactions foster innovation and identify gaps in current knowledge. Training programs for researchers in endemic countries build local capacity and expand the global network. The visibility gained through international partnerships attracts additional private investment. Research institutes are becoming hubs for policy dialogue on vaccine equity and access. Their ability to leverage global networks enhances their influence and operational scale. This collaborative ecosystem drives sustained growth and innovation in the Zika vaccine sector.

REGIONAL ANALYSIS

North America Zika Virus Vaccines Market Analysis

North America dominated the global Zika virus vaccines market and accounted for a 45.3% share in 2025. The dominance of this market was driven by robust research infrastructure and substantial government funding. The United States is a leader in vaccine development with major pharmaceutical companies and academic institutions headquartered in the region. As per the Centers for Disease Control and Prevention, although local transmission is rare, the threat of imported cases requires vigilance. The National Institutes of Health allocates millions of dollars annually for Zika research, including clinical trials. Regulatory agencies like the Food and Drug Administration have established fast-track pathways for Zika vaccines. The presence of advanced biotechnology clusters in Boston and San Francisco fosters innovation. Private investment in vaccine startups is strong due to favorable venture capital environments. The market is characterized by high spending on R&D and sophisticated healthcare infrastructure. Public awareness remains high due to past travel-associated cases. Collaboration between government agencies and the private sector accelerates product development. The region serves as a testing ground for new technologies before global rollout. Strong intellectual property protections encourage commercialization. The focus on biodefense and pandemic preparedness includes Zika in strategic planning. This comprehensive ecosystem ensures North America remains a key player in the global market.

Europe Zika Virus Vaccines Market Analysis

Europe maintains a steady growth in the Zika virus vaccines market due to strong regulatory frameworks and collaborative research initiatives. The European Medicines Agency provides clear guidelines for vaccine approval, facilitating market entry. As per the European Centre for Disease Prevention and Control, the risk of local transmission exists in southern regions due to the presence. The European Union funds extensive research through Horizon Europe programs focusing on arboviruses. Countries like France and Germany have advanced vaccine manufacturing capabilities. Public health systems emphasize preparedness for emerging infectious diseases. Clinical trials are conducted across multiple member states, ensuring diverse population data. The region benefits from high healthcare spending and universal coverage models. Academic institutions collaborate extensively with industry partners. Public trust in vaccination is generally high, supporting future uptake. Regulatory harmonization across the EU simplifies cross-border studies. The focus on global health security drives investment in vaccine stockpiles. European companies are active in developing platform technologies for rapid response. The region plays a critical role in setting international standards for vaccine quality. This strategic importance sustains its market share and influence.

Asia-Pacific Zika Virus Vaccines Market Analysis

The Asia Pacific is an emerging region in the Zika virus vaccines market owing to increasing incidence rates and expanding healthcare infrastructure. Countries like India, Thailand, and Singapore report periodic outbreaks linked to mosquito vectors. As per the World Health Organization, the tropical climate supports year-round transmission in many areas. Governments are investing in local vaccine production to reduce dependency on imports. Public health campaigns are raising awareness about preventive measures. The growing middle class increases demand for travel vaccines and private healthcare services. Clinical trial capabilities are improving with modern facilities in China and Australia. Regional collaborations facilitate data sharing and joint research projects. The presence of low-cost manufacturing hubs attracts global pharmaceutical companies. Regulatory agencies are strengthening their oversight to ensure safety and efficacy. Urbanization and climate change exacerbate vector proliferation, driving urgency. International aid organizations support capacity building in less developed nations. The market is driven by the need to protect large populations in dense urban areas. Economic growth enables greater healthcare expenditure. This dynamic environment presents significant growth opportunities for vaccine developers.

Latin America Zika Virus Vaccines Market Analysis

Latin America was the second largest region in the Zika virus vaccines market and captured a 22.4% share in 2025. Countries such as Brazil, Colombia, and Mexico continue to monitor transmission risks closely. As per the Pan American Health Organization, sporadic cases still occur, necessitating sustained vigilance. Local governments prioritize vector control and public education alongside vaccine readiness. The region has experienced firsthand the devastating impact of congenital Zika syndrome driving strong political will for prevention. Manufacturing capabilities are being developed in countries like Brazil to ensure supply security. Clinical trials have been conducted locally, providing relevant efficacy data. Public health systems are integrating Zika preparedness into routine care. International partnerships support technology transfer and funding. The high burden of disease creates a clear market need. Community engagement is strong due to personal experiences with the outbreak. Regulatory bodies are aligning with international standards to facilitate approvals. The region serves as a primary site for post-marketing surveillance. Economic constraints challenge widespread adoption, but tiered pricing models offer solutions. This historical context ensures Latin America remains central to global Zika vaccine strategies.

Middle East and Africa Zika Virus Vaccines Market Analysis

The Middle East and Africa region is likely to grow in the Zika virus vaccines market during the forecast period due to increasing travel connectivity and vector presence. While reported cases are lower than in the Americas, the risk of introduction is significant. As per the World Health Organization, Aedes mosquitoes are widespread in many African countries, suggesting silent circulation may occur. Limited surveillance data masks the true burden of disease. Governments are strengthening laboratory capacities to detect outbreaks early. International health regulations require preparedness for emerging threats. Vaccine introduction faces challenges due to fragmented healthcare systems and funding gaps. However, global health initiatives are targeting arboviral diseases in the region. Climate change is expanding suitable habitats for vectors in new areas. Public awareness is growing through regional health organizations. Collaborative efforts with European and American institutions support research and training. The potential for large-scale outbreaks drives interest in preventive solutions. Local manufacturing is limited, but import dependencies are being addressed through regional trade agreements. The market is in early stages but holds long-term potential. Investment in health infrastructure is gradually improving access to vaccines. This evolving landscape presents opportunities for strategic market entry.

COMPETITIVE LANDSCAPE

The competition in the global Zika virus vaccines market is characterized by intense research and development activities among pharmaceutical giants and specialized biotechnology firms. Since no vaccine has yet received full licensure, the race focuses on clinical trial progress and regulatory milestones. Major players differentiate themselves through proprietary platform technologies such as chimeric viruses, DNA plasmids, and mRNA constructs. Strategic alliances with academic institutions and government bodies are common to secure funding and expertise. The market exhibits high barriers to entry due to complex scientific challenges and stringent regulatory requirements. Companies compete based on safety profiles, particularly regarding pregnant women and potential antibody-dependent enhancement risks. Speed to market is critical, prompting aggressive investment in accelerated trial designs. Geographic diversity in clinical sites helps gather robust data across different populations. Intellectual property disputes may arise as multiple entities explore similar mechanisms. The lack of immediate commercial revenue drives reliance on grants and public funding. Collaborative pre-competitive research is increasingly vital to address shared scientific hurdles. This dynamic environment fosters innovation while requiring substantial financial and operational resilience from participants.

KEY MARKET PLAYERS

Some of the most prominent companies leading the global zika virus vaccines market profiled in this report are

- Takeda Pharmaceutical Co. Ltd.

- NewLink Genetics Co.

- Immunovaccine Inc.

- GeneOne Life Science Inc.

- GlaxoSmithKline PLC

- Inovio Pharmaceuticals, Inc.

- Bharat Biotech International Ltd.

- Hawaii Biotech Inc.

- Sanofi S.A.

TOP PLAYERS IN THE MARKET

- Sanofi Pasteur leverages its extensive experience in flavivirus vaccine development to advance its Zika virus candidate. The company utilizes its proven yellow fever vaccine platform to create a chimeric Zika vaccine that aims to induce robust immune responses. Recent clinical trials have focused on evaluating safety and immunogenicity in healthy adults across multiple regions. Sanofi actively collaborates with global health organizations to align its development pipeline with public health needs. The company invests heavily in manufacturing infrastructure to ensure scalable production capabilities for future demand. Its strategic focus includes optimizing dosing regimens to enhance efficacy while maintaining safety profiles. Sanofi also engages in regulatory discussions to streamline approval pathways for emergency use. By integrating Zika research into its broader arbovirus portfolio, the company strengthens its position as a leader in infectious disease prevention. This comprehensive approach ensures readiness for potential outbreaks and sustained market relevance.

- Bharat Biotech has emerged as a significant contributor to the global Zika virus vaccines market through its innovative DNA vaccine candidate. The company initiated early-phase clinical trials in India, demonstrating promising safety and immunogenicity data. Bharat Biotech focuses on developing cost-effective solutions suitable for large-scale deployment in endemic regions. Recent actions include expanding its research facilities to accelerate preclinical studies and process optimization. The company collaborates with international academic institutions to validate its findings and enhance scientific credibility. Its strategy emphasizes rapid response capabilities to emerging infectious threats. Bharat Biotech also explores combination vaccines targeting multiple mosquito-borne diseases to increase commercial viability. By prioritizing accessibility and affordability, the company addresses critical gaps in global health security. Its proactive engagement in clinical development positions it as a key player in the evolving landscape of Zika prevention technologies.

- GlaxoSmithKline applies its advanced adjuvant technology to enhance the efficacy of its Zika virus vaccine candidates. The company focuses on creating formulations that provide long-lasting immunity with fewer doses. Recent research efforts involve testing various antigen designs to optimize immune response durability. GlaxoSmithKline collaborates with government agencies and non-profit organizations to secure funding for late-stage trials. The company integrates its Zika program into its broader pandemic preparedness strategy, ensuring resource allocation continuity. Strategic partnerships with contract research organizations facilitate efficient clinical trial execution across diverse populations. GlaxoSmithKline also invests in regulatory science to navigate complex approval requirements for novel vaccine platforms. Its commitment to scientific excellence and global health equity drives continuous innovation. By leveraging its established manufacturing network, the company ensures potential rapid scale-up. This multifaceted approach reinforces its leadership in developing high-quality preventive solutions for vector-borne diseases.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Zika virus vaccines market primarily employ strategic collaborations and partnerships to share research costs and accelerate development timelines. Companies invest heavily in advanced platform technologies such as mRNA and DNA vectors to enhance vaccine efficacy and safety profiles. Regulatory engagement is crucial as firms work closely with agencies to define clear pathways for approval and emergency use authorization. Diversification of product pipelines allows manufacturers to mitigate risks associated with a single disease focus by integrating Zika candidates with other flavivirus vaccines. Geographic expansion into endemic regions facilitates local clinical trials and builds trust with affected communities. Investment in manufacturing scalability ensures readiness for sudden demand surges during outbreaks. Public-private partnerships provide essential funding and technical support for late-stage trials. Intellectual property protection strategies safeguard innovations while enabling licensing opportunities. Continuous monitoring of epidemiological trends guides strategic decision-making and resource allocation. These combined approaches enable companies to navigate scientific and commercial challenges effectively.

MARKET SEGMENTATION

This research report on the global zika virus vaccines market has been segmented and sub-segmented based on type, end-user, and region.

By Type

- Therapeutic Vaccines

- Preventive Vaccines

By End-User

- Hospitals

- Clinics

- Research Institutes

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the global zika virus vaccines market?

The global zika virus vaccines market involves development and distribution of vaccines to prevent zika virus infection and its related complications globally

2. What drives growth in the global zika virus vaccines market?

Growth is driven by rising zika outbreaks, government funding, advances in mRNA and DNA vaccines, and increasing awareness of congenital zika syndrome risks

3. Which vaccine types are most common in the global zika virus vaccines market?

mRNA, DNA, and inactivated vaccines are leading formulations in development and deployment in the global zika virus vaccines market

4. How do vaccine platforms impact the global zika virus vaccines market?

Innovations in vaccine platforms improve efficacy, reduce side effects, and accelerate development, boosting the global zika virus vaccines market

5. What regions have highest demand in the global zika virus vaccines market?

Tropical regions in South America, Southeast Asia, and Africa drive demand due to endemic presence and outbreak risks in the global zika virus vaccines market

6. Who are key players in the global zika virus vaccines market?

Companies like Sanofi, Pfizer, Bharat Biotech, Moderna, and Inovio lead vaccine development and commercialization globally

7. How do government initiatives influence the global zika virus vaccines market?

Government grants and public health campaigns support R&D and immunization, accelerating market growth worldwide

8. What challenges affect the global zika virus vaccines market?

Challenges include virus mutation, regulatory hurdles, vaccine hesitancy, and logistical distribution issues in the global zika virus vaccines market

9. How does vaccine efficacy affect the global zika virus vaccines market?

High efficacy builds public trust and regulatory approval, essential for widespread adoption in the global zika virus vaccines market

10. How important is vaccine safety in the global zika virus vaccines market?

Safety profiles determine regulatory approvals and public acceptance critical to success in the global zika virus vaccines market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com