- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

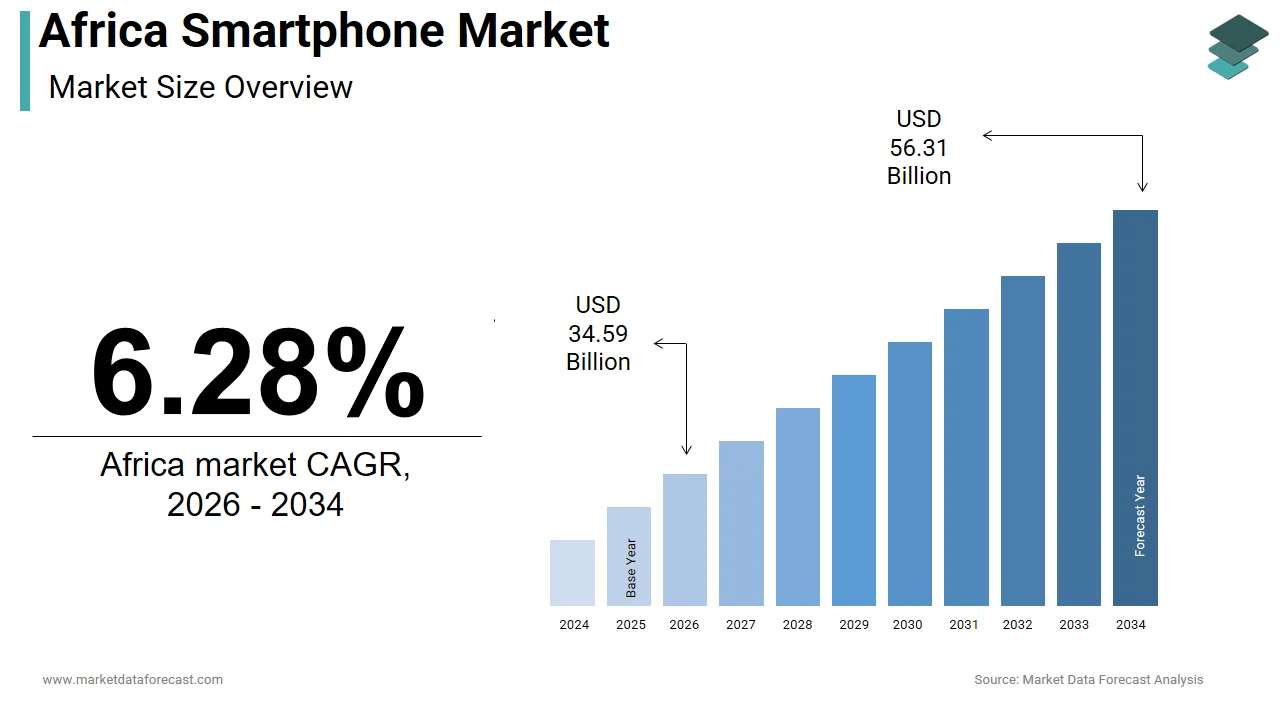

Market Size, 2025

$32.55 BnMarket Estimate, 2026

$34.59 BnMarket Forecast, 2034

$56.31 BnCAGR, 2026–2034

6.28%Africa Smartphone Market Size

The Africa smartphone market was valued at USD 32.55 billion in 2025, is estimated to reach USD 34.59 billion in 2026, and is projected to reach USD 56.31 billion by 2034, growing at a CAGR of 6.28% from 2026 to 2034.

The Africa smartphone market encompasses the distribution, adoption, and technological evolution of mobile computing devices across 54 diverse nations, characterized by fragmented regulatory landscapes, uneven infrastructure development, and rapidly shifting consumer behaviors. Unlike mature markets, Africa’s smartphone ecosystem is deeply intertwined with socio-economic accessibility, where device ownership often serves as the primary gateway to digital services. As of 2023, mobile penetration across the continent reached 52% despite fixed broadband remaining below 5%, illustrating the centrality of mobile devices in digital inclusion. The continent’s youthful demographic fuels demand for affordable, connected devices capable of supporting multimedia and digital platforms.

MARKET DRIVERS

Expansion of Mobile Financial Services Driving Smartphone Adoption

The proliferation of mobile money platforms has fundamentally altered consumer incentives to adopt smartphones across Africa. While basic handsets once sufficed for voice and SMS, the growing complexity of digital financial services now necessitates smartphone capabilities. As of 2023, sub-Saharan Africa accounted for over 70% of global mobile money transactions, with active accounts surpassing 700 million. Platforms require app-based interfaces, biometric authentication, and secure internet connectivity functions, predominantly available on smartphones. In Kenya, smartphone adoption rose significantly, closely mirroring the expansion of mobile banking services. This symbiotic relationship between fintech and device uptake illustrates how digital financial inclusion is not merely a consequence of smartphone growth but a principal catalyst.

Rising Youth Population and Demand for Digital Content

Africa’s demographic structure is uniquely skewed toward youth, making it the youngest continent globally. This cohort exhibits strong preferences for digital entertainment, social media, and online learning, all of which require smartphone-enabled internet access. YouTube, TikTok, and Instagram are among the most accessed platforms, with daily social media usage in hours in urban African centers. Educational initiatives such as Eneza Education and Ubongo Kids have also seen millions of combined users, predominantly engaging via smartphones. This cultural shift toward digital engagement is compelling younger consumers to prioritize smartphone ownership, even at the expense of other expenditures.

MARKET RESTRAINTS

Persistent Low Disposable Incomes Limiting Device Affordability

Despite growing demand, the affordability of smartphones remains a critical barrier across much of Africa. The average selling price of a smartphone in sub-Saharan Africa stood at approximately $120 in 2023, representing over 30% of the monthly income for individuals in low-income brackets, as per the World Bank’s Poverty and Inequality Platform. In nations such as Malawi and Niger, where GDP per capita remains below $600 annually, even entry-level smartphones are considered luxury items. Furthermore, indirect costs such as data plans and electricity for charging exacerbate financial strain. In rural Ethiopia, only a limited share of households have consistent grid access, making device usability intermittent. These economic and infrastructural constraints collectively suppress widespread adoption, particularly among rural and low-income populations.

Underdeveloped After-Sales Service Infrastructure

The scarcity of reliable repair networks and genuine spare parts significantly diminishes consumer confidence in smartphone ownership across Africa. In Nigeria, Africa’s largest smartphone landscape, a notable share of repairs is conducted by informal technicians using counterfeit components. This undermines device longevity and increases tthe otal cost of ownership. Moreover, major manufacturers maintain limited service centers outside capital cities. The absence of standardized warranties and service guarantees discourages investment in higher-end models, perpetuating reliance on low-cost, short-lifecycle devices.

MARKET OPPORTUNITIES

Localization of Hardware and Software for Regional Languages and Needs

A significant untapped potential lies in the customization of smartphones to accommodate Africa’s linguistic and functional diversity. With over 2,000 languages spoken continent-wide, as documented by Ethnologue, the predominance of English and French interfaces excludes vast segments of the population. Devices preloaded with local language support, such as Swahili, Hausa, Amharic, or Yoruba, can dramatically improve usability for first-time digital users. Transition Holdings has capitalized on this by integrating voice assistants and dialer interfaces in regional dialects, contributing to its dominance in markets like Nigeria and Egypt. Furthermore, localized features such as dual SIM slots, extended battery life, and solar charging compatibility address practical challenges, enhancing relevance and driving brand loyalty among underserved communities.

Growth of Indigenous Smartphone Manufacturing and Assembly Hubs

Emerging local production ecosystems present a transformative opportunity to reduce import dependency and tailor devices to regional demands. Kenya, Ethiopia, and South Africa have established assembly plants for brands such as TECNO, Infinix, and Samsung, leveraging government incentives under industrialization agendas. Also, intra-African trade in electronics grew between 2020 and 2023, signaling a shift toward regional value chains. Ethiopia’s Bole Assembly Plant produces a large number of units annually, reducing import duties and retail prices. Localized manufacturing also enables faster product iteration based on consumer feedback and fosters technical employment. The African Continental Free Trade Area further amplifies this potential by reducing tariffs on component imports, enabling scalable, cost-efficient production models that could redefine market dynamics across the region.

MARKET CHALLENGES

E-Waste Management and Environmental Sustainability

The rapid turnover of smartphones has precipitated a mounting e-waste crisis across Africa, with limited regulatory and infrastructural capacity to manage disposal. In 2022, the continent generated significant metric tons of electronic waste, yet only a small percentage was formally recycled. Ghana’s Agbogbloshie dump, one of the world’s largest e-waste sites, receives tons of discarded electronics annually, much of it non-functional smartphones imported from Europe and Asia. Informal recycling methods, including open burning and acid leaching, release toxic substances such as lead and mercury, posing severe health risks. The absence of enforceable producer responsibility laws hampers sustainable practices, threatening both environmental integrity and long-term market credibility.

Cybersecurity Vulnerabilities in Expanding Digital Ecosystems

As smartphone dependency grows, so does exposure to cyber threats, particularly in environments with limited digital literacy and weak regulatory oversight. West Africa experienced a year-on-year increase in mobile-based financial fraud, with Nigeria and Ghana among the most targeted nations. Fake apps mimicking legitimate banking and payment platforms have surged. Many low-cost smartphones lack regular security updates or pre-installed antivirus software, increasing susceptibility. With digital identity systems and mobile health records increasingly reliant on smartphones, the absence of robust cybersecurity frameworks jeopardizes user trust and impedes broader digital transformation efforts across the continent.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Operating System, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | Sudan, Egypt, Kenya, Ethiopia, Ghana, South Africa, Rest of Africa |

| Market Leaders Profiled | Samsung Electronics Co. Ltd, Huawei Technologies Co. Ltd, Apple Inc., Xiaomi Corporation, BBK Electronics Corporation, Lenovo Group Limited, HTC Corporation, HMD Global Oy, Sony Corporation, ZTE Corporation, Google LLC, and Others. |

SEGMENTAL ANALYSIS

By Operating System Insights

The Android segment commanded a substantial share of the smartphone operating system market across Africa in 2025. This dominance is primarily driven by its deep integration with cost-effective hardware manufacturing. Most of the smartphones sold in Africa are priced below $200, and nearly all are powered by Android. Furthermore, Google’s investment in lightweight apps such as Android Go, which function efficiently on devices with as little as 1GB of RAM, has broadened accessibility. Also, Android Go has been pre-installed on over 40 million entry-level smartphones across Nigeria, Kenya, and Ethiopia, enabling first-time users to navigate digital services with minimal data and storage requirements. A further pivotal factor reinforcing Android’s supremacy is its synergy with Africa’s mobile-first financial and educational ecosystems. Mobile money platforms are optimized for Android, requiring app installations and background functionality incompatible with basic operating systems. A large portion of mobile money transactions in sub-Saharan Africa occur on Android devices. Additionally, Android supports sideloading, a critical feature in regions with limited app store penetration, allowing users to install applications via peer-to-peer sharing, a common practice in offline communities. The absence of iOS or Windows equivalents that support such flexibility further entrenches Android’s lead.

The iOS segment is expanding at the fastest CAGR of 9.7% from 2026 to 2034. This growth is fueled by increasing urban affluence and the rising prominence of a tech-savvy upper-middle class in major economic hubs. In cities like Lagos, Nairobi, and Johannesburg, iPhone ownership has become a status symbol, with Apple’s brand equity resonating strongly among professionals and entrepreneurs. An additional driver of iOS growth is the proliferation of refurbished and installment-based iPhone models. In Kenya, second-hand iPhones are widely sold. Platforms such as Jumia and Kimathi Stores offer financing plans with low down payments, making premium devices accessible. Apple’s indirect partnerships with local distributors like MTN and Airtel have further expanded availability. This shift reflects a growing willingness to invest in durable, high-performance devices, particularly among digital content creators, fintech users, and remote professionals relying on cloud-based workflows.

By Distribution Channel Insights

The retailers segment was the prominent channel in the market by securing 54.1% of smartphone distribution across Africa in 2024. This dominance is due to the continent’s reliance on tactile, trust-based purchasing behaviors, particularly in non-urban areas where digital literacy and payment infrastructure remain limited. In countries like Nigeria and Ethiopia, many first-time smartphone buyers prefer in-person consultations, where shopkeepers demonstrate device functions and assist with SIM activation. Retailers also serve as critical after-sales touchpoints, offering immediate troubleshooting and accessory bundling services rarely matched by online platforms. A different key factor sustaining retailer dominance is their integration into informal credit ecosystems. In Accra and Kampala, “buy now, pay later” arrangements at local stores enable consumers to acquire smartphones through weekly installment plans without formal documentation. Moreover, retailers stock a wide array of refurbished, open-box, and locally assembled devices that are absent from official OEM channels. This adaptability to local economic realities ensures retailers remain the backbone of smartphone access, especially in regions where digital trust and logistics infrastructure lag.

The e-commerce segment is the fastest-growing distribution channel in Africa’s smartphone market and is projected to expand at a CAGR of 14.3% between 2025 and 2033. This surge is propelled by rising internet penetration and the proliferation of mobile payment systems that have overcome historical barriers to online transactions. Platforms like Jumia, Takealot, and Kilimall have leveraged this connectivity to offer smartphones with cash-on-delivery options, return guarantees, and bundled data plans, significantly reducing purchase hesitation. A further catalyst is the strategic localization of e-commerce logistics. Jumia, operating in multiple African countries, has established several last-mile delivery hubs and partnered with drone delivery startups to reach remote areas. Additionally, e-commerce platforms are increasingly offering trade-in programs and extended warranties, mimicking the assurances of physical retail. This convergence of trust, accessibility, and convenience is transforming e-commerce from a niche alternative into a mainstream distribution force.

COUNTRY-LEVEL ANALYSIS

Nigeria Smartphone Market Insights

Nigeria led the smartphone market in West Africa by capturing 18.3% of the MEA region’s total shipments in 2024. With a population exceeding 220 million and a youthful demographic 70% under the age of 30, the country represents a high-volume, price-sensitive market where demand is concentrated in the sub-$150 segment. This growth is fueled by the expansion of 4G networks and the affordability of locally assembled devices. The government’s Nigerian Electronic and Technology Development Policy incentivized local manufacturing, leading to an increase in domestic smartphone assembly. Transition and Samsung now operate assembly plants in Ogun State, reducing costs and import duties. However, economic volatility, including a 28% inflation rate in 2023 as per the World Bank, continues to constrain purchasing power, making low-cost, durable devices the dominant choice.

South Africa Smartphone Market Insights

South Africa is distinguished by its relatively advanced telecommunications infrastructure and higher disposable incomes. With 94% 4G coverage and 38 million smartphone users, it serves as a testing ground for premium brands like Apple, Samsung, and Huawei. Mobile internet usage averages 10.2 hours per week per user, driven by high engagement with streaming, banking, and e-commerce platforms. Also, mobile data traffic grew in 2023, reflecting increasing reliance on smartphones for daily transactions. However, economic stagnation and high unemployment, officially at 32.9% as reported by Statistics South Africa, limit mass-market expansion. The market is thus bifurcated: urban professionals adopt high-end devices, while price sensitivity dominates in townships and rural areas, sustaining demand for refurbished and mid-tier models.

Egypt Smartphone Market Insights

Egypt commands a significant share of the MEA smartphone market and is leveraging its population of 110 million as a key growth lever, as highlighted in the 2023 Arab League Economic Development Report. Smartphone penetration reached 65% in 2023, supported by aggressive government digitization initiatives such as the “Digital Egypt” strategy, which aims to connect 90% of public services online by 2025. The National Telecommunications Regulatory Authority confirmed that mobile broadband subscriptions grew by 18% year-on-year, reaching 88 million in 2023. Moreover, Egypt has emerged as a regional manufacturing hub, reducing import costs. Despite these advances, currency devaluation and inflation, exceeding 35% in 2023 as reported by the Central Agency for Public Mobilization and Statistics, have eroded consumer purchasing power, constraining upgrades to higher-tier models.

Kenya Smartphone Market Insights

Kenya occupies a strategic position in East Africa’s smartphone landscape. With 54 million mobile subscriptions and 48% smartphone penetration, Kenya’s market is propelled by one of the world’s most developed mobile money ecosystems. This has driven a year-on-year increase in smartphone adoption, particularly in urban centers like Nairobi and Mombasa. The country also hosts regional offices for major OEMs and e-commerce platforms, facilitating faster product rollouts. However, high import duties, up to 35% on smartphones, keep prices elevated, limiting access in lower-income segments despite growing digital demand.

Ethiopia Smartphone Market Insights

Ethiopia is the fastest-emerging smartphone market in the Horn of Africa. With a population of 120 million and a historically low smartphone penetration of just 28% in 2023, the country represents one of the continent’s largest untapped markets. Until recently, state-controlled telecom monopolies stifled growth, but the 2022 liberalization of the telecommunications sector has catalyzed change. Ethio Telecom now faces competition from Safaricom’s M-Pesa-backed entrant, Corridor Digital, accelerating network expansion. As per the Ethiopian Ministry of Innovation and Technology, mobile internet users surged from 22 million to 38 million between 2021 and 2023. Nevertheless, low disposable income, limited electricity access in rural areas, and only 51% of households are grid-connected as per the World Bank, and ongoing regional instability continues to temper rapid adoption, creating a market poised for future explosion rather than immediate saturation.

COMPETITIVE LANDSCAPE

The competition in the Africa smartphone market is intense and highly differentiated by pricing, distribution, and localization strategies. Global brands like Samsung and Apple compete in the premium segment, while Chinese manufacturers such as Transsion, Xiaomi, and OPPO dominate the mid-to-low-tier markets through hyper-localized offerings. The battlefield extends beyond hardware to ecosystem integration, with companies enhancing software features for mobile money, offline content access, and energy efficiency. Local assembly, after-sales service expansion, and innovative financing models are becoming critical differentiators. Emerging players are challenging incumbents through aggressive e-commerce penetration and influencer marketing. The lack of strong domestic brands intensifies reliance on foreign entrants, but regulatory shifts toward import substitution are encouraging localized production. As consumer expectations evolve, competition is shifting from pure affordability to total value, encompassing durability, support, and digital utilit,y reshaping market dynamics across regions.

KEY MARKET PLAYERS

Some of the noteworthy companies in the Africa smartphone market profiled in this report are

- Samsung Electronics Co. Ltd

- Huawei Technologies Co. Ltd

- Apple Inc.

- Xiaomi Corporation

- BBK Electronics Corporation

- Lenovo Group Limited

- HTC Corporation

- HMD Global Oy

- Sony Corporation

- ZTE Corporation

- Google LLC

TOP LEADING PLAYERS IN THE MARKET

- Transsion Holdings, through its brands TECNO, Infinix, and itel, has established deep market entrenchment by designing smartphones specifically for African consumer needs. The company emphasizes features such as extended battery life, multi-SIM support, and camera optimization for darker skin tones innovations rooted in localized R&D centers across Kenya, Nigeria, and South Africa. In 2023, Transsion launched solar-powered charging kiosks in rural Uganda and Tanzania, enhancing device usability in off-grid areas. It also expanded its after-sales service network to over 1,200 touchpoints across 15 countries, addressing a critical pain point in device maintenance. By partnering with mobile operators like MTN and Airtel for bundled data and device financing, Transsion has strengthened accessibility for low-income users, reinforcing its reputation as a socially attuned technology provider.

- Samsung has reinforced its presence in Africa through a dual strategy of premium innovation and affordable localization. In 2023, the company inaugurated its second smartphone assembly plant in Egypt, increasing regional production capacity and reducing import dependency. It introduced the Galaxy A04s with prolonged battery life and dual SIM functionality tailored for African users, while maintaining its flagship Galaxy S series in urban centers. Samsung also launched the “Smart School” initiative in Nigeria and Kenya, donating smartphones and tablets to educational institutions to foster digital literacy. In collaboration with local telecom providers, it rolled out trade-in programs and micro-financing options. Additionally, Samsung expanded its repair and refurbishment centers in Johannesburg and Accra, enhancing customer retention and reinforcing brand trust in a market sensitive to long-term device reliability.

- Xiaomi has accelerated its footprint in Africa by leveraging aggressive pricing, online-to-offline (O2O) expansion, and strategic partnerships. In 2023, the company deepened its presence in Egypt and South Africa by launching Mi Stores in Cairo and Cape Town, complementing its strong e-commerce presence on platforms like Jumia. Xiaomi introduced the Redmi Note 12 with NFC support, targeting the growing mobile payments sector. It also partnered with Safaricom in Kenya to offer bundled data and device financing, increasing affordability. To address after-sales challenges, Xiaomi certified over 200 local service centers across East and West Africa. Furthermore, the company invested in digital marketing campaigns in local languages and collaborated with African influencers, enhancing brand visibility among youth. These initiatives reflect Xiaomi’s shift from a purely cost-driven model to one emphasizing ecosystem integration and customer experience.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Africa smartphone market are deploying multifaceted strategies to consolidate their positions. Localization of hardware and software remains central, with companies enhancing camera algorithms for darker skin tones and integrating regional languages. Manufacturers are investing in local assembly plants to reduce costs and comply with import regulations. Strategic partnerships with mobile network operators enable bundled data and device financing, improving affordability. Expansion of after-sales service networks addresses consumer concerns about durability and repair. Brands are increasingly leveraging e-commerce platforms while simultaneously establishing physical retail touchpoints to bridge digital and traditional consumer behavior. Additionally, corporate social responsibility initiatives such as donating devices to schools and supporting digital literacy programs are being used to build brand equity and long-term loyalty in a highly competitive, price-sensitive environment.

RECENT MARKET DEVELOPMENTS

- In February 2023, Transsion Holdings launched a solar-powered smartphone charging initiative across rural Tanzania and Uganda, enabling users in off-grid communities to maintain device usability and reinforcing its commitment to inclusive digital access.

- In June 2023, Samsung Electronics inaugurated a new smartphone assembly plant in Beni Suef, Egypt, expanding its local manufacturing footprint to enhance supply chain efficiency and reduce import-related costs in the North African market.

- In September 2023, Xiaomi partnered with Safaricom in Kenya to introduce bundled smartphone and data financing packages, making its Redmi and Note series more accessible to middle-income consumers through flexible payment options.

- In November 2023, Tecno Mobile introduced a continent-wide expansion of its after-sales service network, establishing over 300 new authorized repair centers across Nigeria, Ghana, and Ethiopia to improve customer retention and trust.

- In January 2024, OPPO collaborated with MTN Group to launch a trade-in program across eight African countries, allowing users to exchange old devices for discounts on new models and promoting brand loyalty and upgrade cycles.

MARKET SEGMENTATION

This Africa smartphone market research report is segmented and sub-segmented into the following categories.

By Operating System

- Android

- iOS

- Windows

- Others (Linux)

By Distribution Channel

- OEMs Stores

- Retailer

- E-Commerce

By Country

- Sudan

- Egypt

- Kenya

- Ethiopia

- Ghana

- South Africa

- Rest of Africa