Europe Electrolyte Drinks Market Research Report Segmented By Type (Hypertonic, Hypotonic, Isotonic), Applications (Sports, Medical Centres), Distribution Channel (Supermarkets/Hypermarkets, Pharmacies and Online Stores), And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic And Rest Of Europe) – Analysis On Size, Share, Trends & Growth Forecast (2026 To 2034)

Europe Electrolyte Drinks Market Size

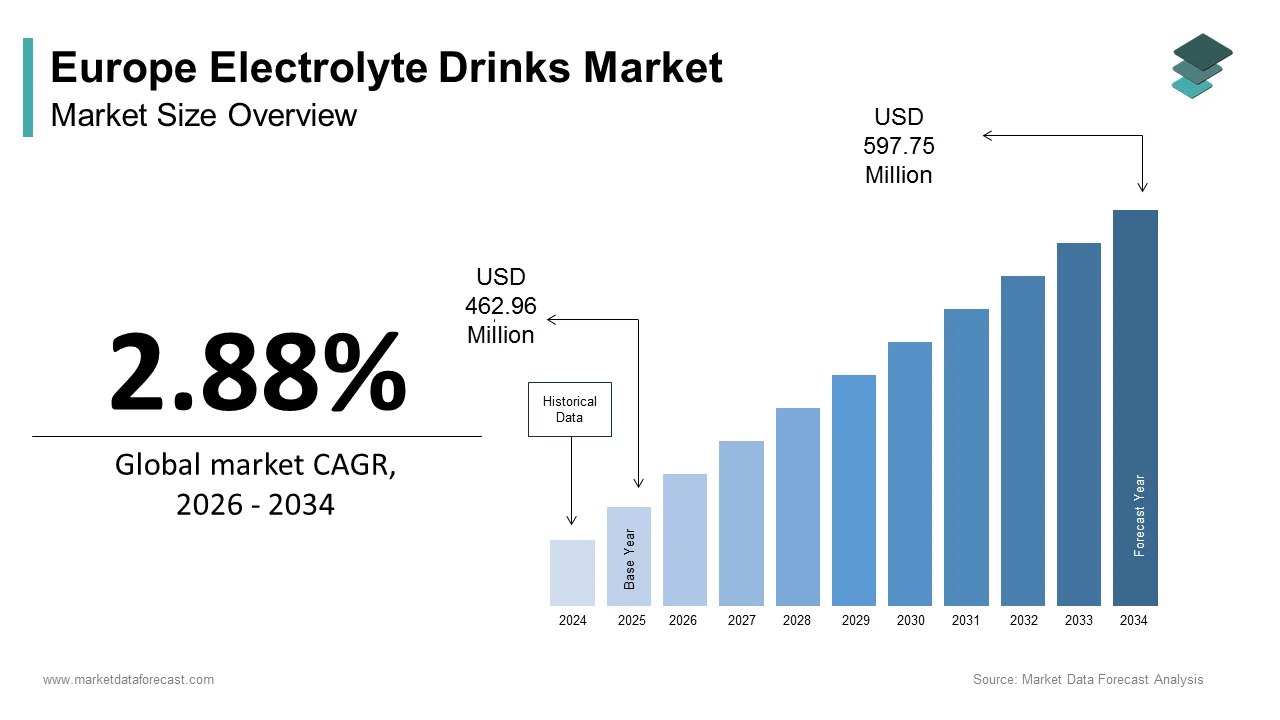

The size of the European electrolyte drinks market was expected to be worth USD 462.96 million in 2025 and is anticipated to be worth USD 597.75 million by 2034, from USD 476.29 million in 2026, growing at a CAGR of 2.88% during the forecast period.

Electrolyte drinks are beverages specifically formulated with water, essential minerals (electrolytes), and usually a small amount of sugar to enhance hydration and replenish the salts lost through sweat, illness, or prolonged physical activity. These products range from traditional sports drinks to clinical oral rehydration solutions (ORS) and emerging wellness tonics, all regulated under the European Union’s framework for foods for particular nutritional uses or general food law, depending on claims made. Unlike sugary soft drinks, electrolyte beverages are increasingly positioned as health-supportive, with formulations evolving toward lower sugar, natural flavors, and added functional ingredients like B vitamins or plant extracts. According to the European Food Safety Authority (EFSA) scientific advice, nutrient profiling is being developed to guide food labeling, rather than registering individual electrolyte formulations. The market is also shaped by public health priorities. European Centre for Disease Prevention and Control (ECDC) data emphasize that widespread gastrointestinal infections, such as Campylobacteriosis, drive consistent demand for Oral Rehydration Solutions (ORS). Additionally, Eurostat indicates that high levels of regular physical activity across the EU have shifted electrolyte drink consumption into the mainstream fitness landscape. This dual role, as both a medical aid and a lifestyle product, defines the unique trajectory of the Europe Electrolyte Drinks Market.

MARKET DRIVERS

Rising Participation in Recreational and Competitive Sports Across Age Groups

Physical activity levels in the region have surged across demographics and are transforming electrolyte drinks from niche athletic aids into mainstream hydration staples, which drives the growth of the Europe electrolyte drinks market. According to sources, European Union citizens are increasingly participating in regular sport and physical activity compared to pre-pandemic levels, with higher engagement in both recreational exercise and sport employment observed across diverse age groups. This trend spans age groups: youth football academies, corporate running clubs, and senior cycling groups all contribute to sustained demand for effective hydration. National initiatives amplify this. France’s “Sport Santé” program promotes physical activity as preventive medicine, while Germany’s statutory health insurers reimburse gym memberships for at-risk patients. In response, brands like Isostar and High5 have expanded beyond elite athletes to target weekend warriors with isotonic formulas that balance taste and function. Supermarkets now dedicate entire aisles to sports nutrition, with electrolyte drinks prominently displayed alongside protein bars. This cultural normalization of fitness, supported by public health policy and retail visibility, has embedded electrolyte beverages into everyday active lifestyles far beyond professional sports.

Integration of Electrolyte Solutions into Public Health Protocols for Dehydration Management

These drinks, particularly oral rehydration solutions (ORS), are increasingly embedded in European clinical and public health guidelines for managing acute dehydration from gastroenteritis, fever, or heat stress, which in turn fuels the expansion of the Europe electrolyte drinks market. The World Health Organization’s standard ORS formula is widely adopted across EU healthcare systems, with national bodies like the UK’s National Institute for Health and Care Excellence recommending it as first-line treatment for mild to moderate dehydration in children and the elderly. Seasonal outbreaks of norovirus and rotavirus in the European Union continue to generate predictable demand for oral rehydration solutions, prompting the integration of electrolyte solutions into public health management protocols for dehydration. Pharmacies stock medical-grade electrolyte powders and ready-to-drink solutions as essential over-the-counter items, often covered by insurance in countries like Sweden and the Netherlands. During intense, high-temperature heatwaves in Southern Europe, public health initiatives often incorporate the distribution of oral rehydration solutions to protect vulnerable populations from dehydration. This institutional endorsement transforms electrolyte drinks from discretionary purchases into critical components of public health resilience.

MARKET RESTRAINTS

Stringent EU Regulations on Sugar Content and Health Claims

The European Union enforces rigorous controls on sugar levels and permitted health claims for beverages, which significantly constrains product formulation and marketing for these specifically formulated beverages, and thereby restrains the growth of the Europe electrolyte drinks market. European regulations require manufacturers to provide transparent sugar data on packaging, but standardized front-of-pack displays currently remain optional rather than mandatory across the Union. National fiscal policies, such as the UK’s beverage levy, use sugar-to-volume ratios to categorize products for taxation, encouraging companies to reformulate their recipes to avoid higher costs. Conventional performance beverages often contain sugar levels that place them directly within the scope of modern health-related taxes. Simultaneously, EFSA permits only limited health claims related to electrolytes, such as “sodium contributes to normal muscle function,” but prohibits broader statements like “prevents cramps” or “boosts endurance” without extensive clinical dossiers. Strict European oversight of health claims ensures that marketing language regarding physical performance must be supported by authorized scientific evidence. These restrictions force manufacturers into a narrow corridor of acceptable taste, sweetness, and messaging, limiting differentiation and consumer appeal in a crowded market.

Consumer Skepticism Over Artificial Ingredients and Perceived Unnecessary Consumption

Many European consumers view electrolyte drinks as overly processed or unnecessary for non-athletic lifestyles, which hinders mass adoption and the expansion of the Europe electrolyte drinks market. Despite advancements in beverage formulations, significant consumer segments continue to express concern over the presence of non-natural additives and sweeteners in functional drinks. Clean-label trends further amplify this perception; ingredients like sucralose, acesulfame K, or synthetic dyes, still common in legacy sports drinks, are increasingly rejected by health-conscious buyers. Moreover, there is widespread misunderstanding about when electrolyte replacement is actually needed; public health bodies emphasize that for light activity or daily hydration, water suffices. This knowledge gap leads to either overconsumption (driving unnecessary sugar intake) or complete avoidance. In Southern Europe, where tap water is abundant and culturally preferred, electrolyte drinks struggle to justify their premium pricing. Until brands successfully communicate evidence-based usage scenarios and reformulate with recognizable ingredients, skepticism will cap market penetration beyond core user groups.

MARKET OPPORTUNITIES

Development of Functional Electrolyte Beverages for Cognitive and Immune Support

European consumers are increasingly seeking beverages that support mental clarity, stress resilience, and immune function, which is likely to promote new opportunities for the Europe electrolyte drinks market. This trend creates a high-potential avenue for next-generation electrolyte drinks fortified with nootropics, adaptogens, and micronutrients. The EU’s aging population and rising workplace burnout have amplified demand for products that address holistic wellness beyond physical hydration. Brands are responding by blending electrolytes with magnesium glycinate for relaxation, vitamin C for immunity, or lion’s mane mushroom for focus—all permissible under current supplement regulations. European consumers, particularly younger generations, are increasingly seeking beverages that offer mental health benefits and cognitive enhancement alongside physical hydration. Regulatory pathways exist for certain claims. EFSA permits “magnesium contributes to normal psychological function,” enabling compliant messaging. Companies like nuun and SOS Hydration have launched “mind+body” variants targeting knowledge workers and students. This convergence of preventive health, cognitive wellness, and clean-label hydration positions functional electrolyte drinks as a premium frontier aligned with Europe’s integrative health evolution.

Expansion into Clinical Nutrition and Elderly Care Settings

These drinks are gaining traction in geriatric and chronic disease management as part of medical nutrition therapy for conditions like sarcopenia, post-surgical recovery, and medication-induced dehydration, which paves the way for fresh prospects for the Europe electrolyte drinks market. Europe’s rapidly aging population, where 21.6% of citizens were aged 65 or older in 2024 according to Eurostat, creates substantial latent demand for easy-to-consume, nutrient-dense hydration solutions. In Germany and the Netherlands, hospital discharge protocols now include electrolyte-fortified beverages for elderly patients at risk of dehydration due to diuretic use or reduced thirst sensation. Clinical guidelines increasingly emphasize the routine use of specialized hydration and nutritional interventions to improve the quality of life for residents in long-term care facilities. These products must meet stringent criteria: low sugar, high bioavailability, and palatable for sensitive palates. This clinically backed channel capitalizes on the public health move toward prevention, delivering stable, high-value growth shielded from retail volatility and perfectly matched to Europe’s aging demographic realities.

MARKET CHALLENGES

Price Sensitivity and Competition from Low-Cost Alternatives

Electrolyte drinks are often priced higher than bottled water or generic soft drinks and are increasingly viewed as non-essential luxuries, amid persistent inflation and cost-of-living pressures across the region, which limits the growth of the Europe electrolyte drinks market. Premium electrolyte beverages continue to maintain a significant price premium over standard mineral water, with specialized functional drinks positioned as high-value, discretionary purchases. This gap becomes critical in price-sensitive markets like Spain, Italy, and Eastern Europe, where disposable income growth has stagnated. While overall EU household consumption grew, high inflation and economic uncertainty have prompted consumers to become more selective, leading to increased price sensitivity in discretionary beverage categories. Many consumers are downtrading to cheaper alternatives or making homemade electrolyte solutions using salt, sugar, and citrus, a practice endorsed by some public health bodies during shortages. Even in affluent regions, private-label electrolyte drinks from retailers like Aldi and Lidl are gaining share by offering lower prices. This economic headwind compresses margins for branded players and threatens volume growth, particularly for premium and organic variants.

Supply Chain Volatility for Key Mineral and Natural Ingredient Sourcing

Instability in the supply of core ingredients due to geopolitical, environmental, and regulatory factors also hampers the expansion of the Europe electrolyte drinks market. High-purity electrolyte salts like potassium citrate and magnesium sulfate are often sourced from limited global producers in China, Chile, and the United States, exposing the market to shipping delays and trade policy shifts. Continued dependency on dominant, external suppliers for raw materials has exacerbated price volatility for critical industrial minerals, causing increased supply chain risks for European industries. Simultaneously, demand for natural flavors like lemon or coconut water, used to replace artificial additives, faces climate-related crop volatility. Adverse weather conditions and prolonged droughts in major European growing regions continue to stress the agricultural supply chain, reducing yields for key natural ingredients. These vulnerabilities lead to formulation inconsistencies, cost spikes, and potential stockouts. Without diversified sourcing or investment in regional mineral refining capacity, the market remains exposed to external shocks that undermine product consistency, affordability, and clean-label integrity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.88% |

| Segments Covered | By Type, Application, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

| Market Leaders Profiled | Otsuka Pharmaceuticals Co., Ltd., Stokely-Van Camp Inc., Wahaha Jihuo, Danone, openPR, The Coca-Cola Company, Pure, Nuun, Coca-Cola, Pepsico, PacificHealth Laboratories, and Otsuka Pharmaceutical Co, Bachelor of Sports Nutrition and Fraser and Neave Limited |

SEGMENTAL ANALYSIS

By Type Insights

The isotonic drinks segment captured the majority share of the Europe electrolyte drinks market in 2025. Optimal physiological compatibility, matching the osmotic pressure of human blood to enable rapid fluid and electrolyte absorption without gastrointestinal distress, drives the prominence of the segment. This balance makes them ideal for moderate to intense physical activity, where both hydration and energy replenishment are required. Consuming carbohydrate-electrolyte isotonic beverages during high-intensity endurance exercise sessions that exceed one hour provides greater performance benefits compared to consuming water alone, as these beverages help sustain energy levels, maintain hydration, and delay the onset of fatigue. Major brands like Lucozade Sport, Powerade, and Isostar have built their portfolios around isotonic formulations, ensuring wide retail presence and consumer familiarity. National sports federations, including the German Olympic Sports Confederation, routinely distribute isotonic drinks during training camps and competitions. Additionally, public health campaigns during heatwaves, such as France’s 2024 “Canicule Plan”, recommend isotonic solutions for at-risk populations. This convergence of scientific validation, institutional endorsement, and mass-market accessibility solidifies isotonic drinks as the cornerstone of electrolyte hydration across Europe.

The hypotonic drinks segment is predicted to witness the highest CAGR of 9.1% between 2026 and 2034, owing to rising demand for low-sugar, rapid-hydration solutions among health-conscious consumers and recreational athletes. Hypotonic beverages contain fewer carbohydrates and electrolytes than isotonic counterparts, enabling faster water absorption, critical for light exercise, daily wellness, or recovery in hot climates. In the European market, new electrolyte drink launches are increasingly adopting hypotonic, low-sugar formulations to align with consumer demand for rapid hydration and clean-label ingredients, shifting away from higher-sugar, traditional options. Brands like nuun and High5 have capitalized on this by offering effervescent tablets and ready-to-drink options that appeal to urban professionals and yoga practitioners. Furthermore, clinical guidelines increasingly recommend hypotonic solutions for mild dehydration in children and the elderly due to a gentler osmotic load. This dual pull from lifestyle wellness and preventive healthcare positions hypotonic drinks as the vanguard of next-generation hydration.

By Application Insights

The sports application segment led the Europe Electrolyte Drinks Market and held a significant share in 2025. The leading position of the segment is attributed to decades of integration into athletic training, competition, and recovery protocols across amateur and professional levels. National sports bodies actively promote electrolyte replacement. Sport England supports grassroots clubs by promoting sustainable practices, including improving energy efficiency and reducing environmental impact, rather than mass-distributing beverage products. French sports authorities prioritize hydration and sustainability at national events in line with national sustainable development charters. Data indicates that a significant portion of the European population remains inactive, while a growing minority engages in regular sport, leading to increased adoption of sports nutrition and practices originally designed for high-performance athletes. Supermarkets and gyms stock extensive ranges, normalizing consumption beyond elite circles. Additionally, major events like the Tour de France and UEFA Champions League feature branded electrolyte partnerships, reinforcing cultural association. This ecosystem of institutional support, retail visibility, and behavioral mimicry ensures sports remain the primary engine of demand.

The medical centres segment is estimated to register the fastest CAGR of 11.3% during the forecast period due to the integration of oral rehydration solutions (ORS) into clinical protocols for gastroenteritis, post-surgical care, and chronic disease management. The World Health Organization recommends oral rehydration solutions as the primary treatment for replacing fluids lost during acute diarrheal episodes, which are frequently reported across Europe. Hospitals and pharmacies now routinely dispense medical-grade electrolyte powders and ready-to-drink solutions, often covered by insurance in countries like Sweden and Germany. Geriatric medical guidelines emphasize the need to monitor and manage electrolyte imbalances, such as low sodium levels, in older patients treated with diuretics to prevent complications. Additionally, during the 2024 European heatwave, public health agencies distributed ORS through clinics to vulnerable populations. This institutional anchoring transforms electrolyte drinks from discretionary purchases into essential clinical tools, driving robust and resilient demand.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest segment in the Europe Electrolyte Drinks Market and occupied a 52.4% share in 2025. The supremacy of the segment is supported by unparalleled accessibility, high foot traffic, and strategic placement in sports nutrition or beverage aisles alongside bottled water and soft drinks. Major retailers like Carrefour, Tesco, and Edeka offer extensive selections, from mainstream brands like Powerade to premium options like High5, catering to diverse consumer segments. According to research, physical supermarkets remain a dominant, high-frequency channel for household food procurement, though consumer behavior is shifting toward a mix of convenience shopping, increased use of discount formats, and digital channels. Promotional campaigns during key periods like summer heatwaves or major sporting events further amplify visibility. Private-label offerings also drive volume, with retailers like Aldi launching affordable electrolyte lines that increase category penetration. This blend of scale, convenience, and promotional power ensures supermarkets remain the primary gateway for mass-market adoption across Europe.

The online stores segment is anticipated to witness the fastest CAGR of 13.7% over the forecast period. The swift expansion of the segment is propelled by digital-native consumers, subscription models, and access to niche and premium brands not available in physical stores. Platforms like Amazon, Holland & Barrett Online, and brand-owned e-commerce sites offer detailed ingredient transparency, customer reviews, and personalized bundles, critical for health-conscious buyers evaluating sugar content or natural ingredients. According to the European Commission’s Eurostat, online shopping has become mainstream among EU internet users, driven by high demand for fashion and rapidly growing interest in health, wellness, and beauty products. The majority of European internet users now regularly make online purchases, with younger to middle-aged adults being the most active shoppers. Brands like nuun leverage direct-to-consumer models with auto-replenishment, reducing purchase friction. With logistics networks improving and same-day delivery expanding in urban centers, online channels are redefining convenience, personalization, and trust in the electrolyte beverage landscape.

REGIONAL ANALYSIS

United Kingdom Electrolyte Drinks Market Analysis

The United Kingdom dominated the Europe Electrolyte Drinks Market by accounting for a 20.1% share in 2025. The dominance of the UK market is credited to a strong sports culture, advanced retail infrastructure, and proactive public health policies. The NHS explicitly recommends oral rehydration solutions for childhood gastroenteritis, embedding electrolyte drinks into clinical practice. In response to rising cases of winter vomiting bugs, health agencies in England have increased efforts to support hydration management, including initiatives to improve access to oral rehydration treatments through GP practices. Simultaneously, the UK’s vibrant fitness scene, supported by initiatives like Sport England’s “This Girl Can” campaign, fuels demand for sports electrolyte beverages. Supermarkets like Tesco and Sainsbury’s dedicate prominent shelf space to both medical and sports variants. The hot summer of 2024 further spiked sales, with isotonic drink volumes rising year-on-year. This dual foundation in healthcare and active lifestyles, supported by responsive retail, solidifies the UK’s leadership position.

Germany Electrolyte Drinks Market Analysis

Germany followed closely in the Europe electrolyte drinks market and held a share of 17.9% in 2025 because of its emphasis on scientific validation, preventive healthcare, and regulatory compliance. The German Nutrition Society endorses electrolyte drinks for endurance athletes and elderly populations at risk of dehydration. A significant portion of the older German population, particularly those aged sixty-five and above, faces increased health risks during warmer months, leading to higher utilization of hydration and care services. Retailers like dm-drogerie and Rossmann offer extensive selections of medical-grade and sports electrolyte products, often with pharmacist guidance. Additionally, Germany’s robust sports federation system distributes isotonic drinks during national competitions. The country’s strict food labeling laws ensure transparency, building consumer trust in product efficacy. This blend of clinical integration, retail sophistication, and regulatory rigor makes Germany a high-value, quality-driven market.

France Electrolyte Drinks Market Analysis

France expanded steadily in the Europe electrolyte drinks market due to state-led public health interventions and strong sports participation. The French government's heatwave plan continues to strengthen mandatory hydration protocols and cooling measures for residents in elderly care homes to reduce heat-related illnesses. Simultaneously, the nation’s cycling and football cultures drive sports drink consumption. The Tour de France features branded hydration partnerships that influence consumer behavior. Retail chains like Carrefour and Monoprix offer both medical ORS and sports variants, often with promotions during the summer. Following widespread heatwaves, Santé Publique France reports that public understanding of dehydration risks among seniors has risen as a result of consistent, targeted health awareness campaigns. This synergy of governmental action and athletic tradition sustains steady demand across age groups.

Spain Electrolyte Drinks Market Analysis

Spain holds a noteworthy share of the Europe electrolyte drinks market owing to climatic conditions and high outdoor activity levels. With average summer temperatures exceeding 35°C in regions like Andalusia, dehydration is a persistent public health concern. Spanish health authorities report a significant increase in emergency hospital visits and deaths due to extreme summer heat, leading to heightened public health warnings and recommendations for hydration. Pharmacies stock medical-grade electrolyte drinks as essential items, while supermarkets promote sports variants during peak tourist season. Football culture further amplifies demand. La Liga clubs partner with brands like Aquarius for player hydration. The Spanish National Statistics Institute indicates that a substantial portion of the population participates in physical exercise or outdoor activities on a regular basis, facilitating consistent recreational activity. This confluence of environmental stress, public health response, and athletic engagement defines Spain’s dynamic market.

Sweden Electrolyte Drinks Market Analysis

Sweden is a lucrative region in the Europe Electrolyte Drinks Market by emerging as a leader in preventive geriatric care and clean-label innovation. The Swedish Public Health Agency includes ORS in national guidelines for elderly care, with municipal health centers distributing electrolyte drinks during winter flu seasons and summer heatwaves. Nursing homes in Sweden are increasingly focused on managing and preventing electrolyte imbalances among residents, particularly by addressing nutritional intake and hydration status. Simultaneously, Swedish consumers favor low-sugar, natural formulations. Brands have gained traction with organic ingredients and minimal additives. The country’s high digital penetration, a significant share of adults shop online, supports direct-to-consumer models for premium variants. This alignment of public health policy, environmental consciousness, and e-commerce fluency makes Sweden a bellwether for future market evolution toward clinical and sustainable hydration.

COMPETITION OVERVIEW

Competition in the Europe Electrolyte Drinks Market is defined by a dual dynamic between global beverage giants, specialized health brands, and pharmaceutical suppliers, all operating under stringent regulatory and nutritional expectations. Differentiation hinges not on price alone but on scientific validation, ingredient transparency, and alignment with public health priorities. Established players like Coca-Cola and PepsiCo compete through sports authority, retail scale, and reformulation agility, while niche brands such as nuun and SOS Hydration focus on clean-label integrity and functional benefits like cognitive or immune support. The medical segment, dominated by pharmacy-grade ORS, operates under separate regulatory pathways, creating a parallel competitive arena where compliance and clinical endorsement outweigh branding. Private-label offerings from retailers like Aldi and Carrefour compress margins in the value segment, forcing branded players to justify premium positioning through superior taste, sustainability, or added functionality. Ultimately, success depends on balancing performance credibility, regulatory compliance, and responsiveness to Europe’s diverse and discerning consumer ecosystems spanning sports, wellness, and clinical care.

KEY MARKET PLAYERS

A few major players of the Europe Electrolyte Drinks Market include

- Otsuka Pharmaceuticals Co., Ltd.

- Stokely-Van Camp Inc

- Wahaha Jihuo

- Danone

- openPR

- The Coca-Cola Company

- Pure

- Nuun

- Coca-Cola

- Pepsico

- PacificHealth Laboratories

- Otsuka Pharmaceutical Co

- Bachelor of Sports Nutrition

- Fraser

- Neave Limited

Top Strategies Used by the Key Market Participants

Key players in the Europe Electrolyte Drinks Market are reformulating products to drastically reduce sugar content and eliminate artificial colors and sweeteners in response to EU nutritional guidelines and consumer demand for clean labels. They are expanding into medical and geriatric channels by developing oral rehydration solutions compliant with European Pharmacopoeia standards for use in hospitals and elderly care. Companies are investing in sustainable packaging innovations, including recyclable bottles and reduced plastic usage, to meet EU environmental targets. Strategic partnerships with national sports federations and public health agencies are being leveraged to build scientific credibility and drive institutional adoption. Additionally, firms are enhancing e-commerce capabilities through direct-to-consumer platforms offering subscription models and personalized hydration bundles to capture digital native shoppers.

Leading Players in the Europe Electrolyte Drinks Market

- The Coca-Cola Company maintains a strong presence in the Europe Electrolyte Drinks Market through its Powerade brand, which offers isotonic and hypotonic formulations tailored to regional sports and wellness demands. The company leverages its extensive distribution network across supermarkets, gyms, and convenience stores to ensure broad accessibility. In recent years, Coca-Cola has reformulated Powerade across European markets to reduce sugar content and eliminate artificial colors, aligning with EU clean-label expectations. It has also expanded its product line to include low-calorie variants with natural flavors like lemon and berry, targeting health-conscious consumers beyond traditional athletes. Strategic partnerships with national sports federations, including UEFA and national Olympic committees, reinforce brand credibility. These initiatives demonstrate Coca-Cola’s commitment to adapting its global portfolio to Europe’s evolving nutritional and regulatory landscape.

- PepsiCo plays a pivotal role in the Europe Electrolyte Drinks Market through its Gatorade brand, renowned for scientific backing and performance-driven formulations. While historically stronger in North America, Gatorade has intensified its European footprint by launching region-specific products such as Gatorade Zero and Gatorade Flow, designed for light activity and rapid hydration. The company has invested in clinical studies validating electrolyte efficacy in collaboration with European sports science institutions, enhancing trust among coaches and athletes. PepsiCo is strengthening its market position by marrying local innovation with sports authority and sustainability, addressing the growing demand for planetary health and performance.

- BASF SE contributes significantly to the Europe Electrolyte Drinks Market not as a finished product brand but as a leading supplier of high-purity electrolyte salts and functional ingredients to both medical and sports beverage manufacturers. Its pharmaceutical-grade sodium citrate, potassium chloride, and magnesium sulfate are integral to oral rehydration solutions used in hospitals and pharmacies across the continent. BASF collaborates with healthcare brands and generic drug producers to ensure compliance with European Pharmacopoeia standards. Recently, the company launched a portfolio of clean-label mineral blends derived from sustainable sources, supporting beverage firms in reducing synthetic additives. BASF secures quality and safety in Europe’s electrolyte drink market by anchoring the upstream value chain, ensuring consistent, compliant, and innovative solutions.

MARKET SEGMENTATION

This research report on the Europe electrolyte drinks market has been segmented and sub-segmented based on type, application, distribution channel, & region.

By Type

- Hypotonic

- Hypertonic

- Isotonic

By Application

- Medical

- Sports centers

By Distribution Channel

- Supermarkets and Hypermarkets

- Online Stores

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com