Global Carotenoids Market Size, Share, Trends & Growth Forecast Report - Segmented By Type (Astaxanthin, Canthaxanthin, Lutein, Beta-Carotene, Lycopene, & Zeaxanthin), Application (Food & Beverages, Dietary Supplements, Animal Feed And Pharmaceuticals And Others), Sources (Natural And Synthetic), And Region(North America, Europe, Asia-Pacific, Latin America, Middle East And Africa) - Global Industry Analysis, Size, Share, Growth, Trends And Forecast 2026 To 2034

Market Size, 2025

$1.79 BnMarket Estimate, 2026

$1.87 BnMarket Forecast, 2034

$2.66 BnCAGR, 2026–2034

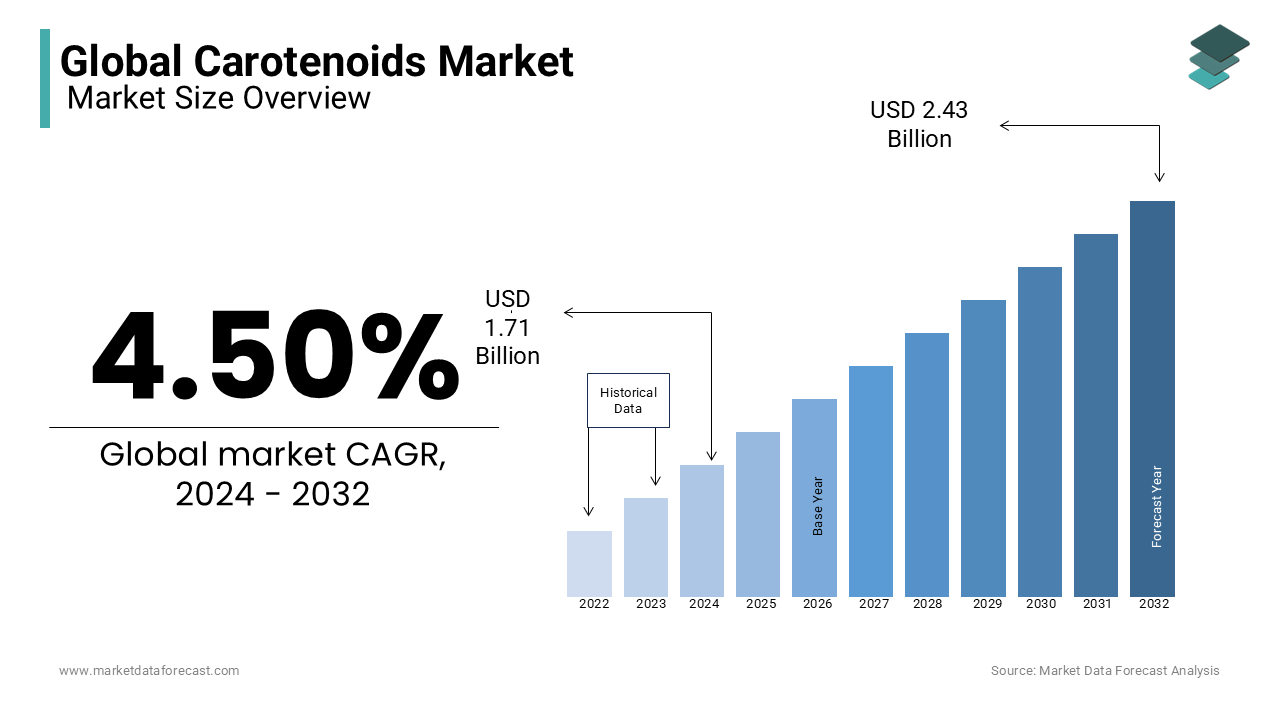

4.50%Global Carotenoids Market Size

The size of the global carotenoids market was expected to be worth USD 1.79 billion in 2025 and is anticipated to be worth USD 2.66 billion by 2034, from USD 1.87 billion in 2026, growing at a CAGR of 4.50% during the forecast period.

Carotenoids are naturally occurring pigments synthesized by plants, algae, and photosynthetic bacteria, responsible for the vibrant red, yellow, and orange hues in numerous fruits and vegetables. Beyond their chromatic role, they serve as precursors to vitamin A and exhibit potent antioxidant properties. As per the Food and Agriculture Organization of the United Nations, over 750 distinct carotenoid structures have been identified in nature, though fewer than 50 are commonly consumed in the human diet. According to a study, millions of people globally suffer from vitamin A deficiency, emphasizing the physiological indispensability of provitamin A carotenoids.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Driving Carotenoids Demand

The global surge in chronic disease prevalence, particularly age-related macular degeneration and cardiovascular ailments, is fuelling the growth of the carotenoids market. The epidemiological evidence substantiates protective roles for lutein and zeaxanthin. According to the World Health Organization, approximately 196 million people were living with age-related macular degeneration in 2020, projected to rise to 288 million by 2040. This escalating burden has intensified consumer and clinical reliance on ocular health supplements. Concurrently, lutein’s substantiated role in maintaining normal vision under prolonged screen exposure is a vital factor as global digital device usage climbs, with a substantial number of smartphone users worldwide. These converging health imperatives are compelling manufacturers to integrate carotenoids into mainstream wellness products.

Clean-Label and Natural Ingredient Trends Accelerating Market Growth

The intensifying consumer pivot toward clean-label as well as plant-derived ingredients in food and beverage applications accelerates the expansion of the carotenoids market. As per the research, a portion of American consumers actively seek products with recognizable, naturally sourced components. Carotenoids such as beta-carotene and lycopene satisfy this criterion while simultaneously replacing synthetic dyes like Red 40 and Yellow 5, whose safety profiles are increasingly scrutinized. The U.S. Food and Drug Administration received citizen petitions urging reevaluation of artificial colorants, reflecting mounting regulatory and public skepticism. Consequently, multinational food producers have reformulated flagship products using carotenoid-based color solutions, which embed these compounds deeper into global supply chains and amplify procurement volumes.

MARKET RESTRAINTS

Stability Challenges and High Production Costs Restraining Market Growth

The intrinsic instability of these compounds during processing and storage, leading to degradation and diminished bioactivity, is a major impediment to the carotenoids market. As per research, thermal processing can reduce lycopene content in tomato puree and beta-carotene in carrot juice, depending on time-temperature parameters. This vulnerability necessitates costly encapsulation technologies and modified atmospheric packaging, inflating production expenses. According to a study, oxidative degradation of carotenoids accelerates under exposure to light and oxygen, with unprotected lutein in aqueous solutions losing potency within several hours under ambient conditions. Such physicochemical fragility constrains formulation versatility and escalates quality control burdens, particularly for small and mid-tier manufacturers lacking advanced stabilization infrastructure.

Supply Chain Volatility Due to Seasonal and Geographic Dependence

The geographic and seasonal volatility of natural carotenoid sources, which introduces supply chain fragility, is degrading the growth of the carotenoids market. As per the study, climate anomalies have reduced global yields of key carotenoid-rich crops in major producing regions. Drought conditions in California’s Central Valley, which supplies a portion of the U.S. processed tomato output, led to a contraction in harvest volume in 2022, as per research. Parallel disruptions in India’s carrot belt due to unseasonal rainfall further exacerbated raw material scarcity. These agroclimatic instabilities compel manufacturers to absorb price premiums or shift to synthetic or fermentation-derived alternatives, which affects the market’s natural positioning and margin structures.

MARKET OPPORTUNITIES

Technological Advancements in Precision Fermentation Unlocking Sustainable Opportunities

The rapid expansion of precision fermentation platforms capable of biosynthesizing high-purity carotenoids without agricultural constraints is paving the way for new opportunities for the carotenoids market. As per the study, investment in microbial production of phytonutrients surged, with companies scaling yeast-based lycopene and astaxanthin lines. These bioengineered variants offer purity and year-round consistency, circumventing crop failure risks. According to research, fermentation-derived carotenoid production requires less land and less water than conventional agriculture, aligning with corporate ESG mandates. This technological pivot is unlocking scalable and sustainable carotenoid streams previously unattainable via botanical extraction.

Growing Role of Personalized Nutrition and Nutrigenomics in Carotenoids Market Expansion

The integration of carotenoids into personalized nutrition regimens, propelled by advances in nutrigenomics and direct-to-consumer genetic testing, is also a key factor providing new opportunities for the carotenoids market. According to the study, millions of Americans have undergone DNA-based health assessments, with a percentage receiving dietary recommendations involving antioxidant optimization. Companies routinely prescribe lutein and beta-carotene supplementation based on genetic polymorphisms affecting carotenoid metabolism, such as BCMO1 gene variants. As per research, a share of the global population carries at least one allele associated with reduced carotenoid conversion efficiency. This scientific tailoring is transforming carotenoids from generic supplements into biomarker-driven therapeutics, which opens premium-priced and clinically validated market segments previously inaccessible to mass-market nutraceuticals.

MARKET CHALLENGES

Regulatory Fragmentation and Compliance Barriers Hindering Market Growth

The absence of globally harmonized regulatory thresholds for carotenoid dosing and health claims is hindering the growth of the carotenoids market. It is creating formulation ambiguities and market access delays. As per the study, only a few member nations have established upper intake limits for beta-carotene, while lutein lacks standardized maximum levels in a portion of jurisdictions. According to research, inconsistent regulatory frameworks have led to product recalls in five EU member states due to non-compliant lutein concentrations. Simultaneously, there has been an increase in dossier rejections for carotenoid-containing supplements in Canada, citing insufficient evidence for structure-function claims. This regulatory fragmentation impedes multinational product launches and escalates compliance costs disproportionately for SMEs.

Consumer Misperceptions and Misinformation Undermining Market Potential

Consumer misperception regarding carotenoid efficacy, fueled by inconsistent messaging and pseudoscientific marketing, is additionally expected to impede the growth of the carotenoid market. As per a study, only a portion of surveyed adults in OECD countries could accurately identify the primary health benefit of lycopene, while a notable share erroneously believed all carotenoids function identically. According to research, a percentage of consumers purchasing lutein supplements for cognitive support were unaware that clinical evidence primarily supports ocular, not neurological, endpoints. This knowledge deficit, compounded by influencer-driven misinformation on social media platforms, erodes trust and triggers post-purchase dissonance. Consequently, brands face escalating educational burdens and reputational risks despite scientifically substantiated formulations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.5% |

| Segments Covered | By Type, Application, Source, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC; PESTLE Analysis. Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | BASF SE, Brenntag, Kemin Industries, Cyanotech Corp, ExcelVite Sdn. Bhd, Chr. Hansen, D.D. Williamson, Allied Biotech, Divis Laboratories, DSM Nutritional Products, Naturex SA, Lycored, and Others. |

SEGMENTAL ANALYSIS

By Type Insights

The beta-carotene segment was the prominent segment in the carotenoids market by occupying 38.4% of the market share in 2025. Dual functionality, serving as both a vibrant natural colorant and the most efficient precursor to retinol, or vitamin A, is contributing to the growth of the beta-carotene segment of the global market. As per the study, millions of preschool-aged children and a large number of pregnant women globally suffer from vitamin A deficiency, a condition mitigated through beta-carotene fortification.

The astaxanthin segment is expected to exhibit rapid growth with a CAGR of 16.2% between 2026 and 2034. The acceleration of the astaxanthin segment is due to its unparalleled antioxidant capacity, stronger than vitamin C and more potent than vitamin E, according to a study. Athletes and active agers are primary adopters. As per the study, a portion of fitness supplement users in North America prioritize cellular protection ingredients, with astaxanthin featured in a percentage of newly launched sports recovery formulations. Simultaneously, aquaculture demand surges. According to research, global salmonid production rose notably in metric tons, which cements its indispensability in premium aquafeed.

By Application Insights

The dietary supplements segment held 42.6% of the carotenoids market share in 2025. The dominance of the dietary supplements segment is propelled by escalating consumer self-care paradigms and physician-endorsed micronutrient prophylaxis. As per the study, a portion of American adults consumed dietary supplements daily. Lutein and zeaxanthin supplements alone generated a significant amount in U.S. retail sales, driven by ophthalmologist recommendations to mitigate blue light retinal stress. It is a concern that a portion of adults spend several hours daily on digital screens. Furthermore, insurance reimbursement trends in Germany and Japan cover carotenoid-containing ocular supplements for patients, which institutionalizes long-term demand.

The pharmaceutical application segment is projected to achieve the fastest CAGR of 14.8% from 2026 to 2034. The rapid growth of the pharmaceutical application segment is fueled by clinical validation of carotenoids as adjuvant therapies, particularly lycopene in prostate oncology and astaxanthin in metabolic syndrome management. As per a study, men supplementing with 30 mg/day of lycopene demonstrated a lower incidence of high-grade prostate lesions over five years.

By Source Insights

In 2025, the natural-sourced carotenoids segment dominated the carotenoids market by capturing a substantial share 2025. The intensifying clean-label mandates and retailer procurement policies are majorly contributing to the growth of the natural-sourced carotenoids segment in the global market. Walmart mandates that a portion of private-label food and supplement products must eliminate synthetic dyes, which is impacting a substantial amount of annual purchases. Parallelly, as per the study, UK organic food sales surged, with carotenoid-rich botanical extracts. According to research, a percentage of millennial shoppers perceive naturally derived as synonymous with clinically safer, higher bioavailability in plant-extracted beta-carotene versus synthetic equivalents when consumed with dietary lipids.

The fermentation-derived carotenoids segment is expected to register with a CAGR of 18.4% during the forecast period, owing to precision fermentation’s ability to decouple production from climatic volatility and land constraints. According to a study, one cubic meter of bioreactor space yields the equivalent carotenoid output of 2.3 hectares of farmland, with water consumption reduced. Companies supply pharmaceutical-grade lutein with isomeric purity, unattainable via botanical extraction. Investment inflows reflect confidence; synthetic biology funding in carotenoid pathways exceeded, which validates scalability and purity advantages over traditional agriculture.

REGIONAL ANALYSIS

North America Market Analysis

North America led the carotenoids market by capturing 31.5% of the market share in 2025. The prominence of North America in the global market is primarily driven by consumption-based and formulation-led factors. In addition, a portion of global carotenoid patent filings originates from U.S. institutions, as per the study. Regulatory clarity from the FDA’s GRAS affirmation of lutein and zeaxanthin has enabled many product launches, according to research. Canada has streamlined approvals, reducing market entry timelines. Importantly, the National Institutes of Health allocated funds to clinical trials evaluating carotenoids in neurodegenerative disease mitigation, which strengthens North America’s role as both consumer and scientific nucleus.

Europe Market Analysis

Europe was another key region in the carotenoids market by occupying 28.8% share in 2025 due to regulatory sophistication and premiumization. The European Food Safety Authority’s health claim approvals have created legally defensible marketing frameworks absent elsewhere. Germany alone accounts for a portion of European carotenoid supplement sales, propelled by statutory health insurance reimbursements for age-related macular degeneration prevention, covering millions of beneficiaries, as per a study. France has enacted regulations under the AGEC law to mandate environmental labeling for certain products, including information on recyclability and environmental impact.

Asia-Pacific Market Analysis

Asia-Pacific is quickly emerging in the carotenoids market, owing to being the epicenter of volume growth and demographic-driven demand. India and China collectively consume a portion of global beta-carotene output for fortification programs, reaching millions of beneficiaries under national nutrition mandates tracked. Simultaneously, Vietnam and Indonesia are scaling up aquaculture-integrated astaxanthin use. Rising middle-class health expenditure, projected to grow annually through 2030, ensures structural demand expansion.

Latin America Market Analysis

Latin America has seen a steady expansion in the carotenoids market as it is transitioning from raw material exporter to value-added formulation hub. Brazil leads with a portion of regional consumption, spurred by a regulatory update permitting higher lycopene dosages in functional juices. Mexico’s sugar tax policy has redirected beverage innovation toward nutrient-dense, low-sugar alternatives, with carotenoid-fortified waters growing in retail value. Chile has implemented comprehensive food labeling laws that have led to widespread product reformulation. These laws mandate front-of-package warnings based on nutrient content (calories, sugar, saturated fat, and sodium). Investment in microalgae pilot facilities in Argentina and Colombia signals regional ambition to capture upstream value.

Middle East & Africa Market Analysis

The Middle East and Africa are likely to grow in the carotenoids market with the growth potential, anchored in public health imperatives and import substitution. Nigeria's National Agency for Food and Drug Administration and Control (NAFDAC) regulates mandatory vitamin A fortification of several food staples, including sugar, oil, wheat flour, and margarine. While vitamin A deficiency is a persistent public health concern in Nigeria, particularly among children, the program does not solely target them through specific fortified products. Instead, it uses widely consumed staples to reach a broad portion of the population. Saudi Arabia’s Vision 2030 health diversification plan includes funds allocated to local nutraceutical manufacturing, with carotenoid encapsulation facilities operational in Riyadh and Jeddah. Regional production of marigold-derived lutein in Kenya and Ethiopia is scaling, which reduces import dependency.

COMPETITION OVERVIEW

The carotenoids landscape is characterized by a tripartite rivalry among biotech innovators, chemical synthesis giants, and agri-extraction specialists. Competition pivots not on price but on purity, stability, and regulatory compliance. Players differentiate via clinical substantiation, investing heavily in human trials to validate ocular, dermal, and metabolic benefits. Patent thickets around delivery systems and fermentation strains create high entry barriers. Regional regulatory fragmentation demands localized compliance teams. Mergers target complementary capabilities: biotech meets extraction, synthesis meets encapsulation. Talent acquisition in nutrigenomics and metabolic modeling is intensifying, which signals a shift from ingredient supplier to health solution architect.

Key Market Players

Major Key Players in the Global Carotenoids Market are BASF SE, Brenntag, Kemin Industries, Cyanotech Corp, ExcelVite Sdn. Bhd, Chr. Hansen, D.D. Williamson, Allied Biotech, Divis Laboratories, DSM Nutritional Products, Naturex SA, Lycored, and Others.

Top Strategies Used by Key Market Participants

Leading players deploy vertical integration to control raw material volatility, investing in algae farms and marigold contract farming. They prioritize encapsulation and stabilization R&D to overcome carotenoid degradation, securing patents for lipid-based delivery matrices. Strategic co-development with food and pharma brands enables custom premixes, which embed carotenoids into proprietary formulations. Regulatory lobbying shapes health claim approvals. Geographic expansion targets fortification-driven markets like India and Nigeria, aligning with public health mandates. Digital traceability platforms enhance supply chain credibility, which appeals to ESG-focused buyers.

Leading Players in the Market

DSM-Firmenich

DSM-Firmenich leverages vertically integrated biotechnology platforms to produce high-purity astaxanthin and beta-carotene via fermentation. The entity recently inaugurated an algae biorefinery by enhancing capacity for pharmaceutical-grade lutein. It collaborates with global aquaculture leaders to co-develop stabilized carotenoid premixes, reducing pigment degradation in feed.

BASF SE

BASF dominates through synthetic and nature-identical carotenoid manufacturing, particularly canthaxanthin and lycopene for animal feed and beverages. The company partnered with Brazilian juice manufacturers to reformulate color systems using encapsulated beta-carotene, resisting thermal degradation. BASF’s digital formulation, too, enables clients to model pigment stability under varying pH and heat, which accelerates product development cycles and reduces trial waste.

Kemin Industries

Kemin focuses on natural extraction, sourcing lutein from non-GMO marigolds and astaxanthin from Haematococcus pluvialis algae grown in proprietary photobioreactors. Kemin’s microencapsulation technology extends carotenoid shelf life by months in ambient conditions. The firm also launched a clinician education portal detailing carotenoid pharmacokinetics by positioning itself as a science-backed partner rather than a commodity supplier, which deepens trust among pharmaceutical formulators.

SEGMENTATION ANALYSIS

This research report on the global carotenoids market has been segmented and sub-segmented based on type, application, source, and region.

By Type

- Astaxanthin

- Canthaxanthin

- Lutein

- Beta-Carotene

- Lycopene

- Zeaxanthin

By Application

- Food & Beverages

- Dietary Supplements

- Cosmetics

- Animal Feed

- Pharmaceuticals

By Source

- Natural

- Synthetic

By Region

- North America

- Europe

- Asia and the Pacific

- Middle East and Africa

- Latin America

Frequently Asked Questions

1. What factors are driving the growth of the carotenoids market?

Growing consumer awareness about health and nutrition, increasing demand for natural food colorants, and rising use of dietary supplements are major growth drivers.

2. What are carotenoids commonly used for?

Carotenoids are widely used as natural coloring agents, antioxidants, nutritional supplements, and feed additives in various industries.

3. What are the major types of carotenoids available in the market?

Common carotenoids include beta-carotene, lutein, lycopene, astaxanthin, zeaxanthin, and canthaxanthin.

4. How is the food and beverage industry influencing carotenoid demand?

The growing preference for clean-label and natural ingredients is increasing the use of carotenoids as natural colorants and nutritional additives in food products.

5. Why are natural carotenoids gaining popularity?

Natural carotenoids are preferred due to their health benefits, antioxidant properties, and increasing consumer preference for plant-based and organic products.

6. How are carotenoids used in animal feed applications?

Carotenoids are added to animal feed to enhance pigmentation, improve animal health, and increase nutritional value in poultry, aquaculture, and livestock products.

7. What role do carotenoids play in dietary supplements?

Carotenoids are used in supplements to support eye health, skin health, immune function, and overall wellness due to their antioxidant properties.

8. What are the major challenges faced by the carotenoids market?

High production costs, limited raw material availability, and stability issues during processing and storage are major challenges.

9. Which distribution channels are commonly used for carotenoid products?

Supermarkets, pharmacies, specialty stores, online platforms, and direct sales channels are commonly used for distribution.

10. What is the future outlook for the global carotenoids market?

The market is expected to witness steady growth due to increasing demand for natural ingredients, rising health consciousness, and expanding applications across multiple industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com