Europe Bacterial Biopesticides Market Size, Share, Trends, and Growth Analysis Report, Segmented by Product Type, Mode of Application, Crop Type, and Country – Industry Forecast From 2026 to 2034

Europe Bacterial Biopesticides Market Report Summary

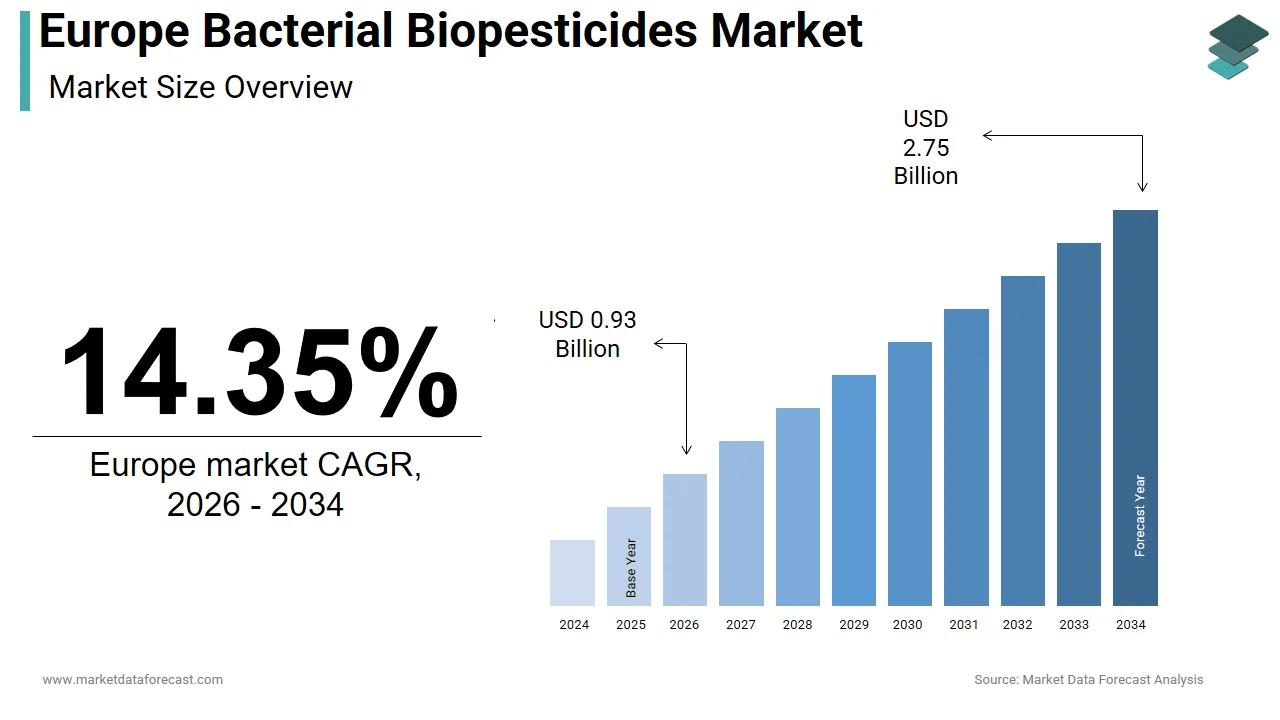

The Europe bacterial biopesticides market was valued at USD 0.82 billion in 2025 and is projected to grow from USD 0.93 billion in 2026 to USD 2.75 billion by 2034, registering a CAGR of 14.35% from 2026 to 2034. Market growth is driven by the increasing adoption of sustainable agricultural practices, stringent regulations on synthetic pesticides, and rising demand for environmentally friendly crop protection solutions. Growing awareness of organic farming, integrated pest management (IPM), and advancements in microbial biopesticide technologies are further supporting market expansion. Government initiatives promoting sustainable agriculture and reduced chemical pesticide usage continue to accelerate the adoption of bacterial biopesticides across Europe.

Key Market Trends

-

Increasing adoption of biological crop protection products across European agriculture.

-

Rising demand for organic farming and sustainable pest management solutions.

-

Growing implementation of integrated pest management (IPM) practices.

-

Expansion of microbial biopesticide research and product innovation.

-

Strengthening regulatory support for reducing synthetic pesticide use and promoting environmentally sustainable agriculture.

Segmental Insights

- Based on product type, the Bacillus thuringiensis segment dominated the Europe bacterial biopesticides market in 2025, driven by its proven effectiveness against a wide range of insect pests, favorable environmental profile, and widespread use across multiple crop types.

- Based on mode of application, the foliar spray segment accounted for the largest market share in 2025, supported by its direct delivery of microbial agents to leaves, stems, and fruits where pests and pathogens are most active, resulting in improved treatment efficiency.

- Based on crop type, the grains and cereals segment held the dominant share of the market in 2025, owing to the extensive cultivation of cereal crops across Europe and increasing adoption of biological crop protection products to improve yield while meeting sustainability goals.

Regional Insights

The Europe bacterial biopesticides market continues to expand across major agricultural economies, supported by organic farming initiatives, environmental regulations, and increasing investment in sustainable agriculture.

- Germany held a significant share of the European market in 2025 and is expected to witness steady growth, driven by advanced agricultural technologies, strong environmental sustainability commitments, and increasing integration of bacterial biopesticides into modern farm management practices.

- France is projected to maintain a strong position in the European market, supported by the continued expansion of organic farming, favorable government policies promoting sustainable agriculture, and increasing adoption of biological crop protection products.

- Italy is expected to strengthen its market presence during the forecast period, leveraging its extensive organic farmland, large specialty crop sector, and growing emphasis on sustainable agricultural production to drive bacterial biopesticide adoption.

Competitive Landscape

The Europe bacterial biopesticides market is highly competitive, with leading agricultural biotechnology companies focusing on microbial product innovation, sustainable crop protection solutions, and expansion of biological product portfolios. Market participants are investing in research and development, strategic collaborations, regulatory approvals, and commercialization of advanced bacterial biopesticides to strengthen their market position. Increasing partnerships with growers and agricultural organizations continue to support market growth.

Prominent companies operating in the Europe bacterial biopesticides market include Koppert Biological Systems, BASF SE, Syngenta AG, Valent BioSciences LLC, and Novozymes A/S.

Europe Bacterial Biopesticides Market Size

The size of the Europe bacterial biopesticides market was worth USD 0.82 billion in 2025. The market is anticipated to grow at a CAGR of 14.35% from 2026 to 2034 and be worth USD 2.75 billion by 2034 from USD 0.93 billion in 2026.

Bacterial biopesticides represent a critical component of integrated pest management strategies in European agriculture, utilizing living microorganisms such as Bacillus thuringiensis, Pseudomonas fluorescens, and Bacillus subtilis to control agricultural pests and diseases. These biological agents offer a targeted and environmentally benign alternative to synthetic chemical pesticides, aligning with the European Union’s stringent regulatory framework aimed at reducing the environmental footprint of farming practices. The adoption of bacterial biopesticides is driven by the need to manage pesticide resistance, ensure food safety, and meet consumer demand for residue-free produce. According to Eurostat, the sales of chemical pesticides in the European Union experienced fluctuations between 2011 and 2021, with recent data highlighting a transition toward lower-risk alternatives. Furthermore, the European Green Deal’s Farm to Fork Strategy explicitly targets a 50% reduction in the use and risk of chemical pesticides by 2030, creating a favorable policy environment for biological alternatives. As per the Research Institute of Organic Agriculture FiBL, the area under organic management in Europe continues to expand, reaching 10.9% of total agricultural land, which inherently relies on approved biological inputs for pest control. The registration of active substances under Regulation EC No 1107/2009 prioritizes low-risk profiles, facilitating faster approval pathways for bacterial strains compared to conventional chemicals. This regulatory support, combined with growing awareness of soil health and biodiversity conservation, positions bacterial biopesticides as essential tools for modernizing European agriculture while maintaining productivity and ecological balance.

MARKET DRIVERS

Stringent Regulatory Restrictions on Synthetic Chemical Pesticides

The implementation of rigorous regulatory frameworks restricting the use of synthetic chemical pesticides is a key factor driving the European bacterial biopesticides market. The European Union has progressively banned or restricted numerous active substances due to concerns over human health, environmental persistence, and non-target organism toxicity. For instance, the non-renewal of approval for neonicotinoids and other broad-spectrum insecticides has created significant gaps in pest management portfolios, compelling farmers to seek effective biological alternatives. According to the European Commission, several dozen synthetic active substances have been non-renewed or withdrawn from the market since 2011 to prioritize safety and sustainability. This regulatory pressure is further amplified by the Sustainable Use of Pesticides Directive, which mandates member states to prioritize non-chemical methods and low-risk products in their National Action Plans. The Farm to Fork Strategy reinforces this trend by setting binding targets for reducing the overall use and risk of chemical pesticides by 50% by 2030. As per data from the European Food Safety Authority, the vast majority of food products tested in the European Union remain compliant with pesticide residue limits, reflecting tighter enforcement and monitoring of chemical inputs. Consequently, agricultural producers are increasingly integrating bacterial biopesticides such as Bacillus thuringiensis into their crop protection regimes to comply with legal requirements while maintaining yield stability. This regulatory-driven transition ensures a steady and growing demand for compliant biological solutions in both conventional and organic farming systems.

Growing Consumer Demand for Residue-Free and Organic Produce

The growing consumer preference for food products free from synthetic pesticide residues and certified organic goods is further fuelling the expansion of the European bacterial biopesticides market. Health-conscious consumers are increasingly scrutinizing food labels and sourcing practices, willing to pay premium prices for produce grown using sustainable and natural methods. According to the European Commission, the retail market for organic food in the EU reached over 46 billion euros in recent years, demonstrating robust growth and consumer commitment to organic principles. Organic farming standards strictly prohibit the use of synthetic chemical pesticides, making bacterial biopesticides indispensable for managing pest and disease pressures in these systems. Major retail chains and supermarkets across Europe have established strict private standards for maximum residue levels, often lower than legal limits, pushing suppliers to adopt biological crop protection strategies. As per a survey by the European Consumer Organisation, over 70% of Europeans consider environmental impact and health safety when purchasing food products. This market pull encourages conventional farmers to adopt reduced-risk inputs like bacterial biopesticides to access premium market segments and maintain buyer relationships. The visibility of bacterial biopesticides as safe and natural solutions enhances brand value for food producers, creating a strong economic incentive for their adoption. This consumer-driven transformation of the food supply chain ensures sustained growth for bacterial biopesticide manufacturers catering to high-value crop sectors such as fruits, vegetables, and vineyards.

MARKET RESTRAINTS

Limited Shelf Life and Stringent Storage Requirements

The inherent biological nature of bacterial biopesticides is impeding the European bacterial biopesticides market growth. Unlike synthetic chemicals that remain stable for extended periods, bacterial formulations contain live microorganisms that require specific temperature and humidity controls to maintain viability and efficacy. Exposure to extreme temperatures, ultraviolet light, or moisture fluctuations during transportation and warehouse storage can rapidly degrade bacterial populations, rendering the product ineffective before application. Most commercial bacterial biopesticides have a shelf life ranging from 6 to 18 months, requiring rigorous cold chain management that increases operational costs for distributors and retailers. According to industry analyses, inconsistent storage infrastructure in some agricultural regions can lead to variable product performance, necessitating better logistics. The sensitivity of bacterial strains to desiccation and oxygen levels necessitates specialized packaging and handling protocols, which are not always available in standard agricultural supply chains. As per agricultural extension reports, farmers often hesitate to invest in biological inputs due to the perceived risk of inconsistent product shelf life. This reliability issue contrasts sharply with the predictable potency of synthetic pesticides, making bacterial biopesticides less attractive to risk-averse growers. The lack of standardized preservation technologies across different formulation types further complicates quality assurance, requiring manufacturers to invest heavily in stabilizers and protective carriers. These logistical and stability challenges restrict the geographic reach and market penetration of bacterial biopesticides, particularly in remote areas with limited infrastructure.

Slower Speed of Action Compared to Synthetic Chemicals

The relatively slower mode of action and delayed visible effects of bacterial biopesticides is further hampering the expansion of the global European bacterial biopesticides market. Bacterial biopesticides typically require ingestion by the pest or colonization of the plant surface to exert their control effect, a process that can take several days to manifest visible results. In contrast, synthetic neurotoxic insecticides often provide instant pest mortality, offering immediate relief during severe infestations. According to agronomic studies, the potential for a lag time between application and pest control is a known challenge that requires strategic preventative planning. Farmers operating on tight economic margins may view this delay as a risk to crop yield and quality, preferring the certainty of chemical solutions. As per field trial data, bacterial biopesticides are most effective when applied preventively or at early stages of pest development, requiring advanced monitoring and planning capabilities that many growers lack. The need for precise timing and repeated applications to maintain control increases labor and operational costs, further detracting from their appeal. Additionally, the variable efficacy of bacterial strains under different environmental conditions, such as rain or high temperatures, adds another layer of uncertainty. This performance gap creates a psychological barrier to adoption, as farmers prioritize immediate threat mitigation over long-term sustainability benefits. Until bacterial biopesticides can demonstrate comparable speed and reliability in high-pressure situations, their uptake will remain limited to proactive and educated segments of the farming community.

MARKET OPPORTUNITIES

Integration with Precision Agriculture and Digital Farming Tools

The convergence of bacterial biopesticides with precision agriculture technologies and digital farming platforms presents a substantial opportunity for the European bacterial biopesticides market. Advanced sensors, drones, and variable rate application machinery enable farmers to monitor pest populations and environmental conditions in real time, allowing for targeted and timely deployment of bacterial biopesticides. This data-driven approach ensures that biological agents are applied when pest thresholds are reached, and environmental conditions favor bacterial survival and activity, maximizing efficacy and minimizing waste. According to reports from the European Parliament, the adoption of digital tools in farming is accelerating, with a growing percentage of large farms in Europe utilizing precision agriculture techniques. Integrating bacterial biopesticide recommendations into farm management software helps growers plan preventive strategies and track application history, improving decision-making and compliance with regulatory standards. Drone-based spraying systems offer novel delivery methods for reaching difficult terrain and ensuring uniform coverage, particularly in high-value crops like vineyards and orchards. As per industry trends, the synergy between biological inputs and digital monitoring enhances the credibility of biopesticides among tech-savvy younger farmers who prioritize measurable outcomes. This technological integration also facilitates traceability and documentation required for organic certification and sustainability reporting, adding value to the overall farming operation. By leveraging precision technology, manufacturers and service providers can offer comprehensive pest management solutions that address the traditional limitations of speed and consistency, driving broader adoption of bacterial biopesticides.

Development of Novel Formulations and Microbial Consortia

Advancements in microbial formulation technologies and the development of multi-strain consortia offer significant opportunities for the European bacterial biopesticides market growth. Researchers and manufacturers are innovating with encapsulation techniques, such as microencapsulation and nano carriers, that protect bacterial cells from environmental stressors like ultraviolet radiation and desiccation, thereby extending shelf life and enhancing field persistence. These protective matrices allow for controlled release of active ingredients, ensuring prolonged efficacy and reduced frequency of application. According to scientific literature, the combination of different bacterial strains with complementary modes of action, such as insecticidal and fungicidal properties, creates synergistic effects that broaden the spectrum of pest and disease control. These consortium-based products address multiple agricultural challenges simultaneously, offering a greater value proposition to farmers compared to single-strain formulations. The European Union’s Horizon Europe program provides funding for research into next-generation biocontrol agents, accelerating the commercialization of innovative products. As per patent filings, there is a surge in intellectual property related to microbial stabilization and combination therapies, indicating strong industry investment in this area. The development of ready-to-use liquid formulations that are compatible with standard spraying equipment simplifies application and reduces labor costs. These technological advancements promise to bridge the performance gap between biological and synthetic pesticides, making bacterial biopesticides more attractive to mainstream conventional growers seeking reliable and efficient crop protection options.

MARKET CHALLENGES

Complex and Lengthy Regulatory Approval Processes

Despite the European Union’s support for low-risk products, the regulatory approval process for bacterial biopesticides remains complex, time-consuming, and costly, which is one of the major challenges to the European bacterial biopesticides market growth. Manufacturers must navigate a multi-tiered authorization system involving data requirements for efficacy, safety, and environmental impact at both European and national levels. According to industry associations, the time to register a new biologically active substance can take several years, with associated costs that represent a barrier to market entry for many smaller developers. This lengthy timeline delays product commercialization and reduces the window for patent protection, discouraging investment in research and development, particularly for small and medium-sized enterprises. The lack of harmonization in data interpretation and additional national requirements in certain member states further complicates the process, creating market fragmentation. As per industry feedback, the uncertainty surrounding regulatory outcomes and potential changes in data requirements create financial risks for developers. The stringent criteria for defining low-risk status, while beneficial, require extensive toxicological and eco-toxicological studies that are resource-intensive. This regulatory burden limits the diversity of products available to farmers and slows the introduction of novel bacterial strains. Additionally, the periodic re-evaluation of approved substances adds ongoing compliance costs for manufacturers. Until the regulatory framework becomes more streamlined and predictable, the pace of innovation and market expansion for bacterial biopesticides will remain constrained, limiting their potential to fully replace synthetic alternatives.

Lack of Technical Knowledge and Application Expertise among Farmers

Insufficient technical knowledge and practical expertise among European farmers regarding the proper handling, timing, and application of bacterial biopesticides hinder their effective utilization and consistent performance, which is further challenging regional market growth. Unlike synthetic chemicals with broad-spectrum activity and forgiving application windows, bacterial biopesticides require precise conditions for optimal efficacy, including specific temperature ranges, humidity levels, and timing relative to pest life cycles. Many growers lack familiarity with these biological nuances and may apply products incorrectly, such as during midday heat or after heavy rain, leading to poor results and disillusionment. According to agricultural extension surveys, a significant portion of farmers still rely primarily on traditional chemical routines and require more comprehensive training on biological control strategies. The complexity of monitoring pest thresholds and understanding microbial behavior creates a knowledge gap that slows adoption. As per educational institutions, curricula for agronomy and plant protection are evolving, but often lag behind the rapid advancements in biological control technologies, leaving advisors needing more up-to-date guidance. Misinformation about compatibility with other inputs and storage requirements further exacerbates misuse. Without comprehensive educational initiatives, demonstration plots, and hands-on support from manufacturers and government agencies, farmers remain hesitant to invest in technologies they do not fully understand. This knowledge deficit perpetuates reliance on familiar chemical inputs and prevents the realization of potential environmental and economic benefits offered by properly applied bacterial biopesticides.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Mode of Application, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

| Market Leaders Profiled | Koppert Biological Systems, BASF SE, Syngenta AG, Valent Biosciences LLC, Novozymes A/S, and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The Bacillus thuringiensis segment held the dominant share of the European market in 2025. The growth of the Bacillus thuringiensis segment in the European market can be credited to its proven and highly specific efficacy against lepidopteran larvae, which are major pests in high-value European crops such as maize, cotton, and vegetables. The crystal proteins produced by this bacterium target the gut lining of specific insect orders, causing rapid mortality without harming beneficial insects, mammals, or humans. This specificity aligns perfectly with Integrated Pest Management strategies that prioritize ecological balance. According to the European Food Safety Authority, Bacillus thuringiensis has a long history of safe use with no recorded adverse effects on non-target organisms, which is making it a preferred choice for regulatory approval. The widespread cultivation of maize in countries like France and Romania, where corn borer infestations are common, drives consistent demand for this biological control agent. As per agricultural extension data, a significant majority of organic maize growers in Central Europe rely on Bacillus thuringiensis as their primary insecticide. Its compatibility with other biological agents allows for seamless integration into complex crop protection programs. The established manufacturing infrastructure and lower production costs compared to newer bacterial strains further cement its leading position. Farmers trust its predictable performance and immediate knockdown effect, which rivals certain chemical alternatives. This reliability, combined with its broad registration across all European Union member states, ensures that Bacillus thuringiensis remains the cornerstone of bacterial biopesticide usage in the region.

However, the Bacillus subtilis segment is projected to grow at the highest CAGR of 10.4% over the forecast period in the European market owing to its dual functionality as both a fungicide and a plant growth promoter. This versatile bacterium colonizes root systems and leaf surfaces, producing antimicrobial compounds that suppress a wide range of fungal pathogens including Fusarium, Rhizoctonia, and Botrytis. As climate change increases the prevalence of fungal diseases in European agriculture, the demand for effective biological fungicides rises sharply. According to research from the Julius Kuehn Institute, Bacillus subtilis strains have demonstrated significant reduction in disease severity in vegetable trials under various conditions. Beyond disease control, Bacillus subtilis produces phytohormones and enzymes that enhance nutrient uptake and root development, offering added value to farmers seeking yield improvements. This multifunctional appeal distinguishes it from single-purpose biopesticides. The growing popularity of protected agriculture in countries like the Netherlands and Spain, where soil-borne diseases are prevalent, creates a fertile ground for adoption. As per industry reports, the use of Bacillus subtilis in hydroponic systems is increasing due to its ability to maintain system hygiene without clogging irrigation lines. This combination of protective and promotional benefits drives rapid adoption among progressive growers looking to optimize input efficiency and crop health simultaneously.

By Mode of Application Insights

The foliar spray segment captured the highest share of the European market in 2025 due to its direct delivery mechanism to the site of pest and pathogen activity on leaves, stems, and fruits. Most bacterial biopesticides, particularly those targeting chewing insects and foliar fungal diseases, require contact with the plant surface to establish colonization or exert toxic effects. Foliar application ensures uniform coverage and immediate availability of the active ingredient where it is most needed. According to agricultural machinery statistics, a large majority of farms in Western Europe are equipped with standard boom sprayers capable of applying liquid biopesticide formulations, making this method highly accessible and cost-effective. The versatility of foliar spraying allows for timely interventions based on real-time pest monitoring, which is crucial for managing dynamic infestations. As per extension guidelines, foliar applications of Bacillus thuringiensis are most effective when timed with early larval stages, a practice well understood by European growers. The ability to adjust dosage and frequency based on weather conditions and pest pressure provides farmers with greater control over treatment outcomes. Additionally, foliar spraying avoids potential soil interactions that might inhibit bacterial activity, ensuring higher efficacy for certain strains. This straightforward application method aligns with existing farming practices, minimizing the learning curve and encouraging widespread adoption across diverse crop types including fruits, vegetables, and ornamentals.

On the other side, the seed treatment segment is emerging as the fastest-growing mode of application in the Europe bacterial biopesticides market and is expected to showcase a CAGR of 11.4% over the forecast period owing to its ability to provide early-season protection and enhance crop establishment. Coating seeds with bacterial strains such as Bacillus subtilis or Pseudomonas fluorescens ensures that beneficial microbes are present at the root zone from germination, protecting young seedlings from soil-borne pathogens and promoting robust root development. This early intervention is critical for preventing yield losses that occur during the vulnerable establishment phase. For instance, the adoption of biologically treated seeds in Europe has shown consistent annual growth, particularly in cereal and oilseed sectors. The precision of seed treatment eliminates waste associated with broadcast applications and ensures uniform distribution of the biopesticide. As per research from Wageningen University, seed-treated crops show improved vigor and stress tolerance, leading to more uniform stands and higher final yields. The convenience of purchasing pre-treated seeds saves farmers time and labor during the busy planting season. This efficiency gain is highly valued by large-scale operators managing thousands of hectares. The integration of bacterial biopesticides into seed treatment workflows aligns with the trend towards precision agriculture, where inputs are optimized for maximum impact with minimal environmental footprint.

By Crop Type Insights

The grains and cereals segment led the market by capturing the highest share of the European market in 2025 due to the extensive land area dedicated to staple crops such as wheat, barley, maize, and rice across the continent. Maize alone covers approximately 9 million hectares in the European Union, making it a primary target for pest management solutions, including bacterial biopesticides like Bacillus thuringiensis for corn borer control. The sheer scale of cereal production creates a massive volume demand for effective and affordable crop protection inputs. According to Eurostat, cereals account for over 50% of the total arable land use in many member states, highlighting the magnitude of this segment. The high economic importance of these staple crops to food security and export revenues drives continuous investment in productivity-enhancing technologies. Bacterial biopesticides offer a cost-effective solution for managing recurring pest issues in large-scale monocultures. As per agricultural surveys, the adoption of biological controls in maize production has increased significantly in response to resistance development against synthetic insecticides. The repetitive nature of cereal cropping systems allows for consistent annual demand, providing stability for biopesticide manufacturers. Furthermore, government subsidies for sustainable cereal production in countries like France and Germany encourage farmers to adopt bio inputs as part of integrated nutrient and pest management plans. This widespread adoption across large-scale commercial farms solidifies the leading position of the grains and cereals segment.

On the other side, the fruits and vegetables segment is projected to record a promising CAGR of 12.2% over the forecast period owing to the high economic value of these crops and strict zero tolerance policies for pesticide residues. Fresh produce such as strawberries, tomatoes, leafy greens, and grapes commands premium prices in European markets, but is highly susceptible to pest and disease damage. Consumers and retailers demand residue-free products, forcing growers to adopt biological control methods that leave no harmful traces. According to industry reports, a large proportion of supermarket contracts now include strict maximum residue limit clauses that are tighter than legal requirements. Bacterial biopesticides such as Bacillus subtilis and Pseudomonas fluorescens are effective against common fungal and bacterial diseases in these crops without leaving chemical residues. The short growth cycles of many vegetables allow for rapid realization of benefits from biological applications, encouraging repeat purchases. As per industry data, the use of biopesticides in protected horticulture is growing annually, driven by the need to maintain product quality and shelf life. The high profit margins in fruit and vegetable production allow growers to absorb the higher costs of biological inputs, making them financially viable. This market pull from downstream buyers ensures that fruit and vegetable growers remain at the forefront of biopesticide adoption.

COUNTRY LEVEL ANALYSIS

Germany Bacterial Biopesticides Market Analysis

Germany held a promising share of the European market in 2025 and is likely to see steady growth in bacterial biopesticide adoption through advanced farm management integration, its advanced agricultural technology sector, and strong commitment to environmental sustainability. The country is a leader in organic farming adoption, with over 11% of its agricultural land under organic management, creating substantial demand for biological pest control solutions. German farmers are increasingly integrating precision agriculture tools with biopesticide applications to optimize efficacy and comply with strict environmental regulations. The Plant Protection Act in Germany imposes stringent limits on chemical pesticide use, compelling growers to seek alternative solutions such as bacterial biopesticides. According to the Federal Ministry of Food and Agriculture, the German government provides significant financial support for sustainable farming practices, including the adoption of biocontrol agents. The presence of major agrochemical companies and research institutions in Germany fosters innovation in microbial formulation technologies, enhancing product efficacy and market acceptance. The country's robust distribution network ensures wide availability of biopesticides across diverse farming regions. Consumer demand for organic and sustainably produced food in Germany is among the highest in Europe, driving retailers to source from farms using biological inputs. This market pull, combined with regulatory push, establishes Germany as a key growth engine for the bacterial biopesticides market in the region.

France Bacterial Biopesticides Market Analysis

France is expected to maintain its competitive edge in the European biopesticides market through continuous expansion of its organic farming sector and policy-driven sustainability efforts over the next few years. The country is one of the largest agricultural producers in the European Union, with significant areas dedicated to cereals, wine grapes, and vegetables, all of which are potential users of biopesticides. The French Ecophyto Plan aims to reduce pesticide use, indirectly promoting the adoption of biological inputs that enhance plant health and reduce dependency on chemical protections. According to national agricultural statistics, the area under organic farming in France covers over 2.7 million hectares, which drives demand for compliant pest management solutions. French farmers are increasingly aware of the benefits of soil health management, leading to greater interest in microbial inoculants like Bacillus subtilis. The country hosts several leading biopesticide manufacturers and research centers that develop strains suited to local soil conditions. Government subsidies for organic conversion and sustainable practices provide financial incentives for farmers to adopt biopesticides. The strong cooperative structure in French agriculture facilitates knowledge sharing and bulk purchasing of bio inputs, accelerating market penetration. Consumer preference for locally produced and environmentally friendly food further supports the growth of the bacterial biopesticides market in France.

Italy Bacterial Biopesticides Market Analysis

Italy is set to strengthen its market presence as a leader in sustainable specialty crop production, leveraging its vast organic farmland to drive biopesticide adoption over the next few years. The country is a leading producer of fruits, vegetables, and wine, sectors that are increasingly adopting organic and sustainable practices to meet premium market demands. Italian farmers face challenges related to climate change-induced disease pressure, making effective biological control agents like bacterial biopesticides highly relevant. According to ISMEA data, Italy has one of the largest organic farming areas in the European Union, with over 2 million hectares under organic management. This extensive organic sector creates a ready market for biological pest control agents that are permitted under organic certification standards. The Mediterranean climate in many parts of Italy supports year-round cultivation, allowing for multiple applications of biopesticides and sustained demand. Italian consumers are highly conscious of food quality and origin, driving retailers to prefer suppliers using sustainable production methods. The government supports agroecological initiatives through national rural development programs, providing funding for the adoption of innovative biological inputs. The presence of numerous small and medium-sized farms in Italy favors the use of cost-effective and easy-to-apply biopesticides. These factors combine to make Italy a dynamic and growing market for bacterial biopesticides in Southern Europe.

Spain Bacterial Biopesticides Market Analysis

Spain is expected to further capitalize on its leadership in high-tech greenhouse production by increasing the density of biopesticide usage to meet global food export standards over the next few years. The country is a major exporter of fresh fruits and vegetables to the rest of Europe, requiring high standards of produce quality and safety that drive the adoption of residue-free production methods. Bacterial biopesticides are widely used in Spanish greenhouses and open-field vegetable production to control fungal diseases and insect pests without chemical residues. According to the Ministry of Agriculture, Fisheries and Food, Spain has seen significant growth in organic farming areas, solidifying its role as a major hub for biological agricultural inputs in the Mediterranean region.

COMPETITIVE LANDSCAPE

The competition in the Europe bacterial biopesticides market is characterized by a mix of established multinational agrochemical corporations and specialized niche biological solution providers. Multinational companies leverage their extensive distribution networks, brand recognition, and financial resources to introduce biopesticides as part of integrated crop management portfolios. These large players often compete based on product stability, formulation technology, and seamless integration with existing chemical inputs. Specialized firms differentiate themselves through deep technical expertise, high-quality microbial strains, and personalized customer support services. They focus on building trust with organic and progressive conventional farmers by providing evidence-based results from local field trials. The market sees intense competition in innovation, with companies constantly developing novel carrier materials and consortium formulations to enhance efficacy and shelf life. Regulatory compliance serves as a significant barrier to entry, favoring established players with resources to navigate complex approval processes. Price competition remains moderate as buyers prioritize product reliability and performance over cost alone. Strategic alliances between biopesticide manufacturers and seed companies or precision agriculture tech firms are becoming common to create comprehensive value propositions. The fragmented nature of European agriculture means that regional players also hold strong positions in specific countries, leveraging local knowledge and relationships to compete effectively against global giants.

KEY MARKET PLAYERS

The leading companies operating in the Europe bacterial biopesticides market include:

- Koppert Biological Systems

- BASF SE

- Syngenta AG

- Valent Biosciences LLC

- Novozymes A/S

TOP PLAYERS IN THE MARKET

- BASF SE leverages its extensive chemical expertise to expand its portfolio of sustainable agricultural solutions, including bacterial biopesticides. The company integrates microbial technologies into its broader crop protection offerings, creating holistic solutions for European growers. BASF invests heavily in research and development to improve the stability and efficacy of its biological products through advanced formulation techniques. Recent actions involve launching new bacterial strains tailored for specific European pests and diseases. The company collaborates with agricultural retailers across Europe to ensure widespread distribution and technical support for farmers. BASF emphasizes the synergy between its chemical and biological products, promoting integrated pest management strategies. By leveraging its established supply chain and brand recognition, BASF accelerates the adoption of biopesticides among conventional farmers. Their focus on scalability and performance consistency helps bridge the gap between traditional and biological farming practices in the European market.

- Novozymes A/S stands as a global leader in biological solutions with a significant footprint in the European agricultural sector. The company leverages its extensive research capabilities to develop high-efficacy bacterial biopesticides, including Bacillus subtilis strains tailored for diverse European soil conditions. Novozymes focuses on integrating its biopesticide products with digital farming tools to provide farmers with precise application recommendations. Recent initiatives include partnerships with major seed companies to offer pre-treated seeds containing their proprietary microbial formulations. This strategy enhances product accessibility and ensures optimal colonization from the earliest growth stages. The company actively participates in field trials across Germany and France to demonstrate yield benefits and disease control. By emphasizing scientific validation and sustainable agriculture goals, Novozymes strengthens its reputation as a trusted provider of innovative biological inputs.

- Koppert Biological Systems specializes in natural pest management and has increasingly expanded into bacterial biopesticides for soil and foliar applications. The company is renowned for its high-quality standards and rigorous quality control processes that ensure viable bacterial counts in every product batch. Koppert focuses on educating farmers and advisors about the benefits of biological pest control through extensive training programs and demonstration projects. Recent efforts include developing consortium products that combine bacterial strains with other beneficial microbes to enhance overall ecosystem functionality. The company works closely with organic farmers and greenhouse operators in countries like the Netherlands and Spain to tailor solutions for specific cropping systems. Koppert’s strong presence in the protected agriculture sector allows it to introduce biopesticides to high-value crop producers who prioritize residue-free production. Their customer-centric approach fosters long-term relationships.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe bacterial biopesticides market primarily employ strategic partnerships and collaborations to expand their distribution networks and enhance product credibility. Companies frequently partner with seed manufacturers to integrate bacterial inoculants directly into seed coatings, ensuring early root colonization and ease of use for farmers. Research and development investments focus on improving formulation stability through advanced encapsulation technologies that extend shelf life and protect bacterial viability during storage and transport. Market participants also engage in extensive field trials and demonstration projects to generate local data proving efficacy under diverse European soil and climatic conditions. Educational initiatives targeting farmers and agronomists are crucial to overcoming knowledge gaps and promoting proper application techniques. Additionally, companies pursue regulatory approvals under the European Plant Protection Product Regulation to facilitate cross-border trade and market access. Mergers and acquisitions allow larger firms to acquire specialized microbial strains and technical expertise, strengthening their product portfolios. Digital integration strategies involve combining biopesticide recommendations with precision agriculture tools to optimize application timing and dosage for maximum efficiency and return on investment.

MARKET SEGMENTATION

This Europe bacterial biopesticides market research report is segmented and sub-segmented into the following categories.

By Product Type

- Bacillus Thuringiensis

- Bacillus subtilis

- Pseudomonas Fluorescens

By Mode of Application

- Foliar Spray

- Seed Treatment

- Soil Treatment

- Post-Harvest Treatment

By Crop Type

- Fruits and Vegetables

- Cereals and Grains

- Oilseeds and Pulses

- Turf and Ornamentals

- Plantation Crops

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe bacterial biopesticides market?

The Europe bacterial biopesticides market covers bacterial crop protection products used to manage pests and support sustainable farming.

How does the Europe bacterial biopesticides market work?

The Europe bacterial biopesticides market works by using beneficial bacteria to control pests while reducing reliance on chemical pesticides.

What drives growth in the Europe bacterial biopesticides market?

The Europe bacterial biopesticides market grows from stricter rules, organic farming demand, and stronger interest in low-residue crop protection.

Which bacterial type leads the Europe bacterial biopesticides market?

Bacillus-based products lead the Europe bacterial biopesticides market because they are widely used, effective, and well accepted in Europe.

Why is integrated pest management important in the Europe bacterial biopesticides market?

Integrated pest management is important in the Europe bacterial biopesticides market because it encourages safer, targeted biological control.

What crops use the Europe bacterial biopesticides market most?

The Europe bacterial biopesticides market is widely used in fruits, vegetables, greenhouse crops, and other high-value farm segments.

How does organic farming support the Europe bacterial biopesticides market?

Organic farming supports the Europe bacterial biopesticides market by increasing demand for biological alternatives to synthetic pesticides.

What role do microbial products play in the Europe bacterial biopesticides market?

Microbial products drive the Europe bacterial biopesticides market by offering safe, effective, and eco-friendly pest management options.

Why are residue-free foods important for the Europe bacterial biopesticides market?

Residue-free foods are important in the Europe bacterial biopesticides market because consumers and regulators prefer cleaner crop protection.

What trends shape the Europe bacterial biopesticides market?

The Europe bacterial biopesticides market is shaped by sustainability goals, biological innovation, and broader adoption of crop protection biology.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com