Higher Education Market Size, Share, Trends & Growth Forecast Report By Component (Hardware, Solution and Service), Course Type (Arts, Economics, Engineering, Law, Science and others), User Type (State Universities, Community Colleges and Private Schools) & Region, Industry Forecast From 2024 to 2033

Global Higher Education Market Size

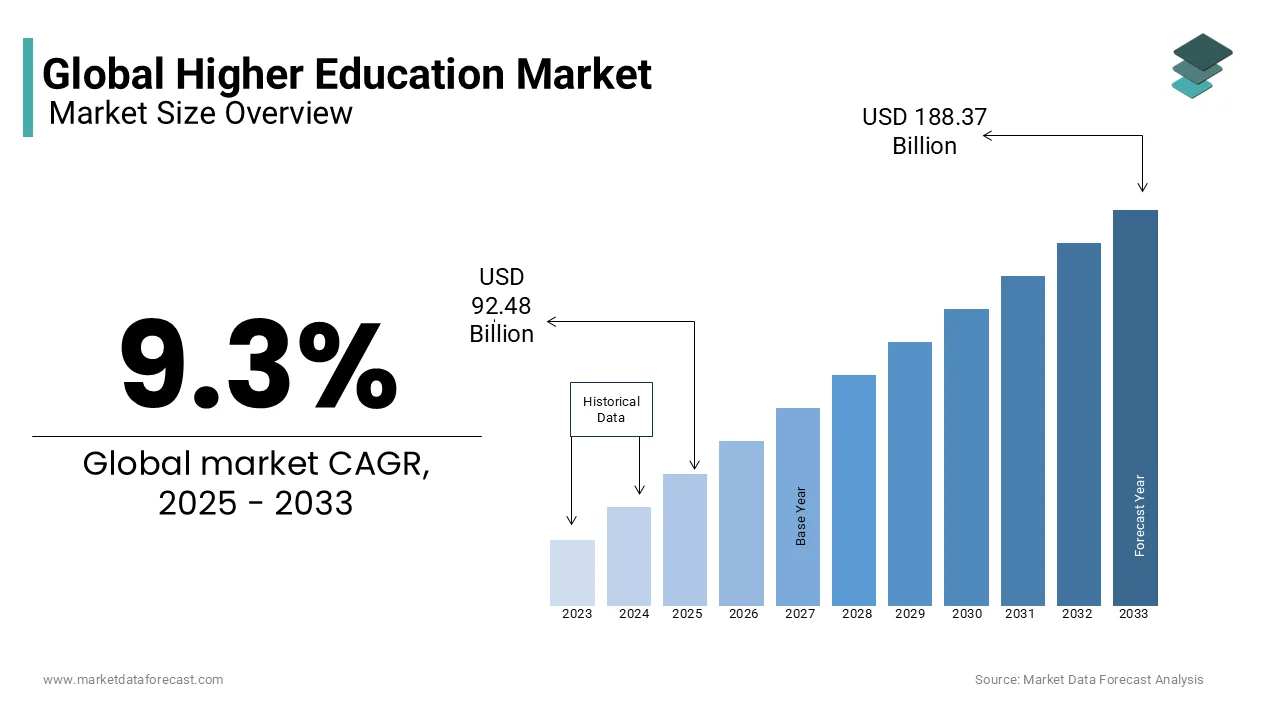

The global higher education market was valued at USD 84.61 billion in 2024. The global market size is predicted to be worth USD 92.48 billion in 2025 and USD 188.37 billion by 2033, growing at a CAGR of 9.3% from 2025 to 2033.

Higher education provides post-secondary academic and vocational instruction, which leads to degrees, diplomas, and certifications recognized by national and international accreditation bodies. As per the United Nations Educational, Scientific, and Cultural Organization, over 220 million students were enrolled in tertiary education globally in 2023, a figure projected to exceed 400 million by 2030 due to demographic expansion and policy-driven access initiatives.

MARKET DRIVERS

Rising Global Demand for Skilled Workforce in Technology-Driven Industries

The rapid evolution of professionals in artificial intelligence, data science, cybersecurity, and renewable energy is a primary factor for the growth of the Higher Education Market. As per the International Labour Organization, 133 million new jobs are expected to emerge in tthe echnology and green economy sectors by 2030. Employers increasingly require candidates with formal qualifications in STEM fields, prompting students to pursue undergraduate and postgraduate degrees to remain competitive. Universities are responding by launching new programs; Stanford University introduced a dedicated undergraduate major in Artificial Intelligence in 2023, while Germany’s Technical University of Munich expanded its renewable energy curriculum to align with national decarbonization goals.

Government-Led Expansion of Access and Equity in Tertiary Education

The public policy initiatives aimed at increasing enrollment rates among underrepresented and rural populations are significantly expanding the growth of the higher education market. As per the United Nations Development Programme, 78 countries implemented free or subsidized tertiary education policies between 2018 and 2023, including Brazil, Indonesia, and South Africa, to promote social equity and national development. Digital inclusion programs are amplifying reach; India’s National Education Policy 2020 led to the creation of the Digital University platform by offering online degrees to over 5 million students in remote areas by 2023.

MARKET RESTRAINTS

Escalating Student Debt and Financial Burden in Developed Economies

The rising cost of higher education in Anglo-American systems has created a severe financial barrier that is significantly hindering the growth of the Higher Education Market. Australia’s Higher Education Support Act recorded a 22% increase in loan defaults between 2020 and 2023, signaling growing repayment challenges. These financial pressures are altering enrollment behavior.

Persistent Inequities in Access and Quality Across Low- and Middle-Income Countries

The systemic disparities in access, infrastructure, and educational quality are degrading the growth of the Higher Education Market. According to UNESCO, only 9% of youth in sub-Saharan Africa are enrolled in tertiary institutions, compared to a global average of 40%, due to limited institutional capacity and geographic barriers. In rural Nigeria, the National Universities Commission reported that 73% of qualified students cannot access university due to insufficient campus infrastructure and funding shortages. Digital divides exacerbate the gap; the International Telecommunication Union found that only 38% of higher education institutions in low-income countries had reliable internet connectivity in 2023, limiting access to online resources and global research networks. Additionally, brain drain undermines institutional stability; the World Bank estimates that over 30,000 African academics emigrated to North America and Europe between 2018 and 2023.

MARKET OPPORTUNITIES

Proliferation of Online and Hybrid Learning Models Post-Pandemic

The global shift toward digital education is ascribed to bolstering the growth of the Higher Education Market. In 2023, 58% of universities worldwide offered at least one fully online degree program, according to the International Association of Universities. Platforms like FutureLearn and 2U have partnered with over 200 universities to deliver accredited online programs, generating new revenue streams. Additionally, adaptive learning technologies powered by AI are enhancing engagement; Arizona State University reported a 23% improvement in course completion rates after integrating AI-driven tutoring systems.

Strategic Expansion of Transnational and Cross-Border Education Programs

The growing acceptance of international academic mobility and offshore campus models is also expected to pose new opportunities for the growth of the Higher Education Market. Simultaneously, universities are establishing international branch campuses to serve local markets; New York University operates degree-granting campuses in Abu Dhabi and Shanghai, enrolling over 5,000 students outside the U.S. In the Middle East, Qatar Foundation hosts branch campuses of Georgetown, Carnegie Mellon, and Northwestern, offering American-accredited degrees to regional students. Similarly, Australia’s Monash University and the U.K.’s University of Nottingham have established permanent campuses in Malaysia and China.

MARKET CHALLENGES

Declining Public Funding and Reliance on Volatile Revenue Streams

The severe financial strain due to diminishing government support and overdependence on tuition and auxiliary income threatens long-term sustainability, which is impeding the growth of the Higher Education Market. As per the Organisation for Economic Co-operation and Development, public expenditure on tertiary education as a percentage of GDP declined in 17 member countries between 2015 and 2023, with Italy and Japan cutting funding by over 12%.

Rapid Technological Disruption and Curriculum Obsolescence

The accelerating pace of technological change is rendering traditional academic curricula obsolete, with higher education institutions to continuously update programs and pedagogical methods. According to the World Economic Forum, 44% of workers’ core skills will be disrupted by 2027, necessitating real-time curriculum adaptation in fields like AI, blockchain, and biotechnology. According to a 2023 study by the European University Association, only 31% of European institutions had integrated generative AI into their teaching frameworks, despite its widespread industry adoption. Meanwhile, alternative education providers such as coding bootcamps and corporate academies are outpacing traditional institutions in delivering timely, industry-aligned training.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.3% |

| Segments Covered | By Offering, User Type, Course, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Xerox Corporation, Smart Technologies, Inc., Panasonic Corporation, EduComp Solutions, Oracle Corporation, Dell, Inc., Three River Systems, Cisco Systems Inc., IBM, Adobe Corporation and Blackboard Inc, Xerox Corporation, Smart Technologies, Inc., Panasonic Corporation, EduComp Solutions, Oracle Corporation, Dell, Inc., Three River Systems, Cisco Systems Inc., IBM, Adobe and Corporation and Blackboard Inc.. |

SEGMENTAL ANALYSIS

By Offering Insights

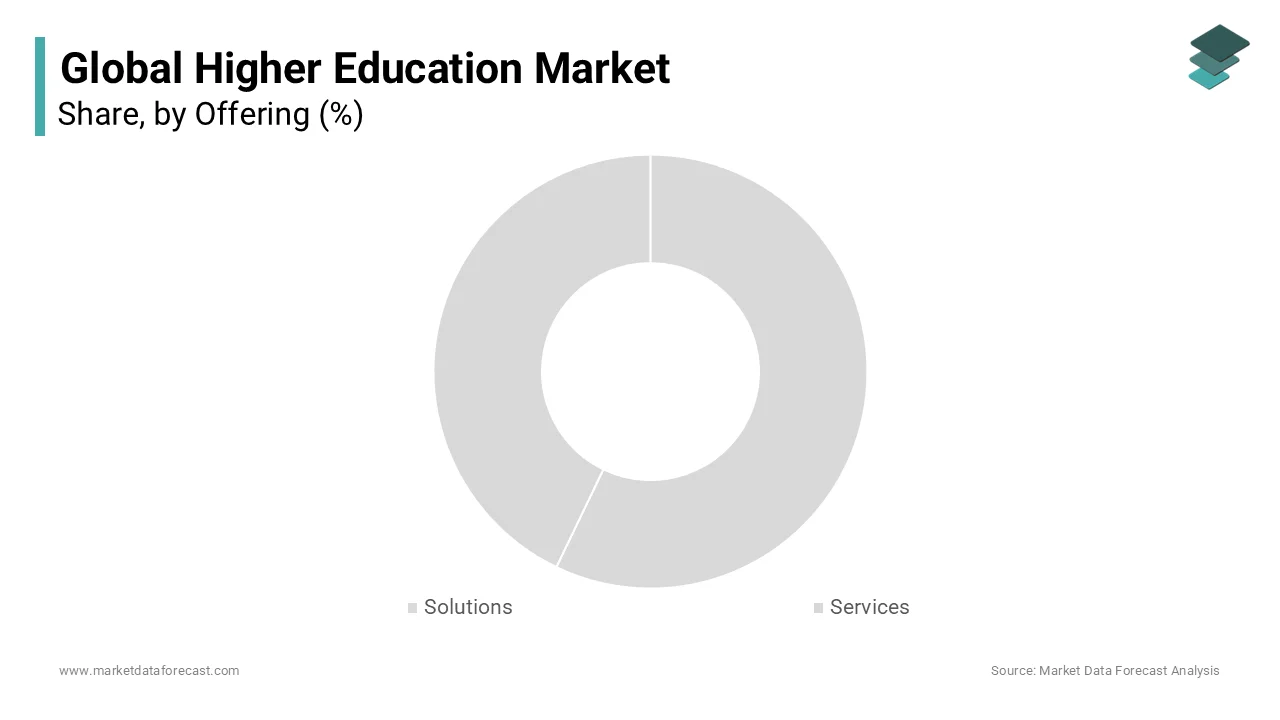

The services segment dominated the higher education market by capturing 54.7% of share in 2024, owing to the increasing reliance on outsourced academic, administrative, and technological support to maintain institutional efficiency and adapt to evolving educational demands. According to the EDUCAUSE Center for Analysis and Research, 81% of U.S. higher education institutions engaged third-party vendors for cloud-based student information systems in 2023. Additionally, the expansion of online and hybrid learning models has amplified demand for instructional design, faculty training, and technical support services.

The solutions segment is projected to expand at a CAGR of 12.8% during the forecast period with the widespread adoption of integrated software platforms that streamline academic operations, enhance student engagement, and enable data-driven decision-making. Platforms like Canvas, Blackboard, and Moodle have become central to course delivery, with Canvas reporting over 30 million active users across 10,000 institutions in 2023. In Africa, the African Virtual University deployed its Open Learning Platform across 29 member countries, enabling standardized digital instruction for over 500,000 students. Another growth factor is the integration of analytics and business intelligence tools; the University of Melbourne uses SAP’s analytics suite to forecast enrollment trends and optimize resource allocation. Additionally, governments are mandating digital solutions; Saudi Arabia’s Ministry of Education requires all public universities to adopt the "Waseel" ERP system for centralized academic and financial management.

By User Type Insights

The state universities segment held a dominant share of the higher education market in 2024 as primary providers of accessible, subsidized, and accredited tertiary education in most countries. These institutions benefit from substantial public funding, extensive infrastructure, and national recognition by enabling them to serve large and diverse student populations. State institutions also lead in research output; the U.S. National Science Foundation found that public universities conducted 59% of federally funded academic research in 2022. Additionally, state universities are central to national digital transformation; India’s National Education Policy 2020 designated 156 state institutions as “Institutions of Eminence,” providing them with autonomy and funding to enhance global competitiveness.

The private schools segment is projected to grow with an expected CAGR of 10.9% in the coming years, with the increasing demand for specialized, flexible, and industry-aligned education in markets where public systems are overburdened or under-resourced. A key factor is the rise of private, for-profit institutions offering career-focused programs in business, technology, and healthcare. Similarly, in Indonesia, private institutions now account for 67% of all higher education enrollments, as per the Ministry of Education, Culture, Research, and Technology. Another driver is foreign investment; the UK’s Navitas and Australia’s Laureate Education have established private colleges in Vietnam, Malaysia, and Ghana to serve growing middle-class populations. In the U.S., private nonprofit universities like Minerva and Southern New Hampshire University have pioneered competency-based and online-first models, attracting non-traditional learners. Additionally, regulatory reforms are enabling growth; India’s 2023 Foreign Educational Institutions Bill allows international universities to operate as private entities, with institutions like MIT and Stanford exploring entry.

By Course Insights

The engineering segment accounted in holding 28.3% of the higher education market share in 2024, with the sustained global demand for technical professionals in infrastructure, manufacturing, information technology, and renewable energy sectors. Universities are responding with expanded capacity and industry partnerships. Germany’s RWTH Aachen University increased its mechanical engineering intake by 40% from 2020 to 2023 to meet automotive and aerospace industry needs. In sub-Saharan Africa, the African Development Bank funded 15 new engineering schools between 2020 and 2023 to address infrastructure gaps.

The science course category is projected to grow at a CAGR of 11.6% during the forecast period, with the rising global investment in research, biotechnology, climate science, and health innovation, which are creating unprecedented demand for advanced scientific training. The University of Cambridge introduced a new Master’s in Climate Change and Sustainability in 2023, which is receiving over 2,000 applications in its first year. Similarly, in South Korea, the Ministry of Science and ICT increased scholarships for science PhD candidates by 25% in 2023 to bolster national R&D capacity. The pandemic also accelerated interest in public health and virology. Johns Hopkins University reported a 47% increase in applications to its epidemiology programs from 2020 to 2023.

REGIONAL ANALYSIS

North America Higher Education Market Insights

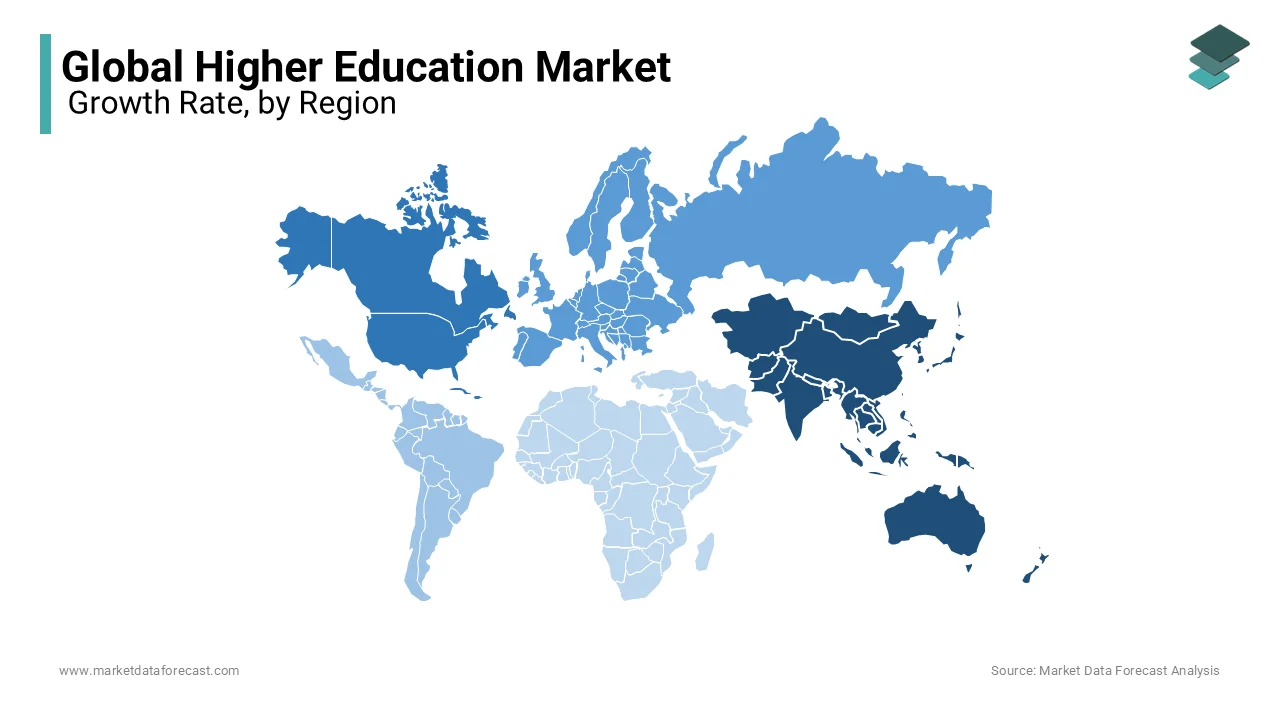

North America was the top performer in the global higher education market with a 32.1% share in 2024. The United States hosts over 4,000 degree-granting institutions by including leading research universities such as MIT, Stanford, and Harvard, which collectively receive over $90 billion in annual R&D funding from federal and private sources, according to the National Science Foundation. The U.S. remains the top destination for international students, hosting 1.05 million in 2023, as reported by the Institute of International Education. Canada complements this ecosystem with a growing reputation for inclusive and high-quality education. The Canadian Bureau for International Education noted that international student enrollment rose to 830,000 in 2023, driven by post-study work opportunities.

Europe Higher Education Market Insights

Europe was ranked second with 27.8% of the Higher Education Market share in 2024. Germany is offering tuition-free education at public universities. Over 2.9 million students, including 420,000 international learners, as per the German Academic Exchange Service. The U.K. remains a major player despite Brexit, with universities generating £42 billion annually and hosting 680,000 international students in 2023, according to Universities UK. France and the Netherlands have expanded English-taught programs to attract global talent.

Asia-Pacific Higher Education Market Insights

Asia-Pacific higher education market is growing with a significant CAGR during the forecast period, with massive youth populations, rising middle-class aspirations, and aggressive government investment. All India Survey on Higher Education recorded a 12.4% enrollment increase from 2021 to 2023, reaching 41.3 million students. Japan emphasizes research excellence, with institutions like the University of Tokyo leading in robotics and AI. Australia and New Zealand attract over 600,000 international students annually, particularly from Southeast Asia. Digital platforms like BYJU’S and Nalanda Open University are scaling online education. With sustained policy focus, APAC is poised to rival North America in influence.

Latin America Higher Education Market Insights

Latin America higher education market is lucratively to grow in the coming years. Brazil’s Ministry of Education reported 8.9 million students in higher education in 2023, with federal universities maintaining high academic standards. Chile has achieved near-universal tertiary access for its youth, as per UNESCO.

Middle East and Africa Higher Education Market Insights

Middle East and Africa (MEA) higher education market is expected to have steady growth opportunities during the forecast period. The UAE’s “Operation Academic Excellence” aims to rank 20 universities among the global top 100 by 2030, with institutions like Khalifa University investing heavily in AI and engineering. Saudi Arabia’s Vision 2030 includes a $50 billion education fund, expanding King Abdullah University of Science and Technology.

KEY PLAYERS IN THE MARKET

Some of the major players in the global higher education market are Xerox Corporation, Smart Technologies, Inc., Panasonic Corporation, EduComp Solutions, Oracle Corporation, Dell, Inc., Three River Systems, Cisco Systems Inc., IBM, Adobe Corporation, and Blackboard Inc. The global higher education market is expanding with increasing mergers and acquisitions, for instance, Cisco Systems' merger with Metacloud, Verizon's with AOL, Inc., IBM's with StoredIQ, and Blackboard's with Schoolwires. In addition, various solution providers, including IBM Corporation and Ellucian, are developing new advanced learning techniques as well as management features in their solution offerings.

TOP LEADING PLAYERS IN THE MARKET

Harvard University

Harvard University has significantly influenced the Asia Pacific higher education market through academic partnerships, executive education programs, and digital learning initiatives. The university collaborates with institutions in Singapore, Australia, and India to co-develop curricula in public health, business, and climate policy. In 2023, Harvard Extension School expanded its online course offerings to include Mandarin and Hindi subtitles, increasing accessibility across China and South Asia. The Harvard Institute for International Development advised the Indonesian government on higher education reform, focusing on research capacity and faculty development. Additionally, the university launched a joint executive program with the National University of Singapore in digital transformation for public sector leaders. Harvard’s Open Learning Initiative has reached over 2.1 million learners in the region through edX, offering free access to courses in data science and ethics.

University of Oxford

University of Oxford has deepened its engagement in the Asia Pacific region through research collaborations, satellite centers, and policy advisory roles. The Blavatnik School of Government partners with public institutions in Malaysia and Thailand to train civil servants in evidence-based policymaking. In 2023, Oxford launched a climate resilience research hub in partnership with the University of Auckland, focusing on Pacific Island nations vulnerable to sea-level rise. The Oxford Internet Institute collaborates with Indian think tanks on digital governance and AI ethics, contributing to national regulatory frameworks. The university also expanded its online learning portfolio through FutureLearn, offering micro-credentials in global health and sustainable development tailored to Southeast Asian professionals. Additionally, Oxford’s Said Business School introduced a regional scholarship program for MBA candidates from ASEAN countries, enhancing access for high-potential leaders. These initiatives reflect a strategic blend of academic rigor and regional relevance, positioning Oxford as a key partner in advancing research, governance, and innovation across the Asia Pacific.

National University of Singapore (NUS)

National University of Singapore (NUS) serves as a regional anchor in higher education, driving innovation, industry integration, and cross-border academic networks across Asia. NUS has established joint research institutes with Tsinghua University, the University of Tokyo, and IIT Bombay, focusing on smart cities, AI, and sustainable energy. In 2023, NUS launched the NUS College, a new honors college integrating liberal arts with STEM to cultivate interdisciplinary leaders. The university strengthened its digital presence by partnering with Coursera to offer online degrees in fintech and data analytics, targeting working professionals across Southeast Asia. NUS also inaugurated the Singapore-Berkeley Building Efficiency and Sustainability in the Tropics (SinBerBEST) center, advancing green building technologies with regional applicability. Its entrepreneurial ecosystem, supported by NUS Enterprise, has incubated over 300 startups since 2020, many addressing regional challenges in healthcare and agritech.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the higher education market are leveraging a range of strategic initiatives to enhance competitiveness and expand influence. Institutions are forming international partnerships to co-develop curricula, conduct joint research, and offer dual-degree programs that increase global appeal. Digital transformation is a priority, with universities investing in online learning platforms, AI-driven tutoring, and cloud-based administrative systems to improve accessibility and efficiency. Many are establishing offshore campuses or regional hubs to serve local markets while maintaining academic standards. Strategic recruitment of international students and faculty enhances diversity and global rankings. Universities are also deepening industry collaboration through sponsored research, internships, and curriculum co-design to ensure graduate employability. Investment in research excellence, particularly in AI, biotechnology, and climate science, strengthens institutional prestige and funding acquisition.

COMPETITION OVERVIEW

The competition in the higher education market is characterized by a complex interplay of institutional prestige, research output, digital innovation, and global reach. Elite universities in North America and Europe maintain dominance through brand equity, endowment strength, and high-impact research, but are increasingly challenged by rising institutions in Asia that combine state support with agile academic models. The race for international students has intensified, with countries like Australia, Canada, and Germany expanding post-study work rights to attract talent. Digital platforms have democratized access, enabling institutions like Arizona State University and the University of London to compete globally through online degrees. Rankings such as QS and Times Higher Education shape perception, driving investments in faculty quality, citations, and employer reputation. Private and for-profit providers are gaining ground by offering career-aligned, flexible programs, particularly in technology and business. Regional accreditation bodies are standardizing quality, while governments incentivize research commercialization and industry collaboration. Sustainability, equity, and lifelong learning are emerging as differentiators.

RECENT MARKET DEVELOPMENTS

- In January 2023, Harvard University launched a digital learning initiative in partnership with India’s Ministry of Education by offering 15 online courses in public health and data science to over 500,000 learners across the country.

- In June 2023, the University of Oxford established a joint research center with the University of Sydney focused on climate adaptation strategies for coastal communities in the Indo-Pacific region.

- In September 2023, National University of Singapore partnered with Alibaba Cloud to develop an AI-powered academic analytics platform for personalized student learning and institutional decision-making.

- In February 2024, MIT expanded its MicroMasters program on edX to include Southeast Asian universities by enabling regional students to earn credit toward a full master’s degree.

- In July 2023, the University of Melbourne introduced a new global mobility framework, which is establishing exchange agreements with 25 universities across India, Vietnam, and Indonesia to enhance student and faculty collaboration.

MARKET SEGMENTATION

This research report on the global higher education market has been segmented and sub-segmented based on offering, user type, course and region.

By Offering

- Hardware

- Solutions

- Services

By User Type

- State Universities

- Community Colleges

- Private Schools

By Course Type

- Arts

- Economics

- Engineering

- Law

- Science

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the current size of the global higher education market?

The global higher education market size was valued at USD 92.48 billion in 2025.

Which regions contribute the most to the global higher education market share?

North America, Europe, and Asia-Pacific are the leading contributors to the global higher education market share, reflecting the concentration of renowned institutions and diverse educational offerings.

What is the impact of the COVID-19 pandemic on the global higher education market?

The COVID-19 pandemic has significantly impacted the higher education market, leading to the rapid adoption of online learning, changes in enrollment patterns, and financial challenges for institutions.

Who are the key players in the higher education market?

Xerox Corporation, Smart Technologies, Inc., Panasonic Corporation, EduComp Solutions, Oracle Corporation, Dell, Inc., Three River Systems, Cisco Systems Inc., IBM, Adobe Corporation and Blackboard Inc,Xerox Corporation, Smart Technologies, Inc., Panasonic Corporation, EduComp Solutions, Oracle Corporation, Dell, Inc., Three River Systems, Cisco Systems Inc., IBM, Adobe Corporation and Blackboard Inc. are some of the major companies in the global higher education market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com