Global Matcha Market Size, Share, Trends & Growth Forecast Report - Segmented By Grade (Classic, Culinary And Ceremonial), Application, and Region(North America, Europe, APAC, Latin America, Middle East And Africa) - Industry Analysis 2026 to 2034

Global Matcha Market Report Summary

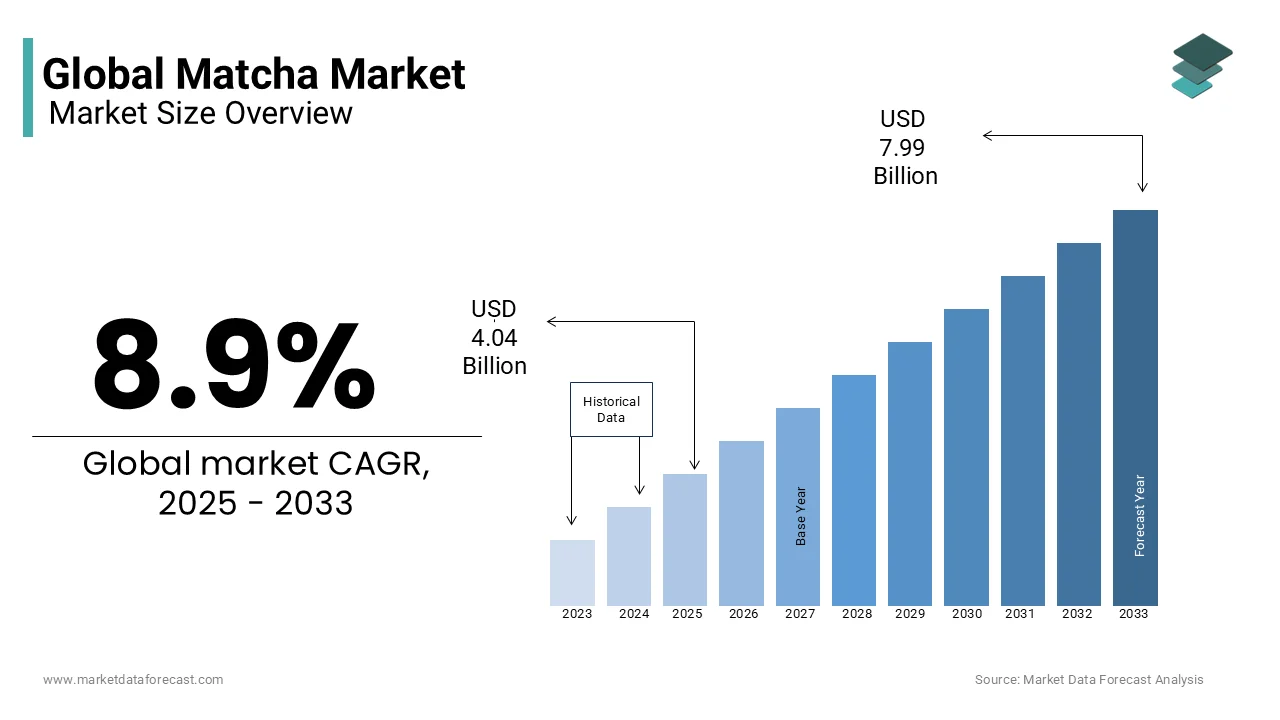

The global matcha market was valued at USD 4.05 billion in 2025, is estimated to reach USD 4.41 billion in 2026, and is projected to reach USD 8.72 billion by 2034, growing at a CAGR of 8.90% during the forecast period from 2026 to 2034. The growth of the global matcha market is driven by increasing consumer preference for functional beverages, rising awareness of the health benefits of green tea, and growing demand for natural and antioxidant-rich ingredients. Matcha is gaining popularity across beverages, bakery, confectionery, dairy, and nutritional supplements due to its rich nutritional profile and versatility. Additionally, expanding café culture, product innovation, and the increasing adoption of clean-label and plant-based products are supporting market growth worldwide.

Key Market Trends

-

Rising consumer demand for functional and antioxidant-rich beverages is driving the adoption of matcha across global markets.

-

Growing popularity of plant-based, clean-label, and natural food ingredients is expanding matcha applications in food and beverages.

-

Increasing use of matcha in bakery, confectionery, dairy products, and nutritional supplements is creating new market opportunities.

-

Expansion of specialty cafés and premium tea culture is boosting demand for high-quality matcha products.

-

Continuous product innovation, including ready-to-drink matcha beverages and flavored formulations, is supporting market growth.

Segmental Insights

-

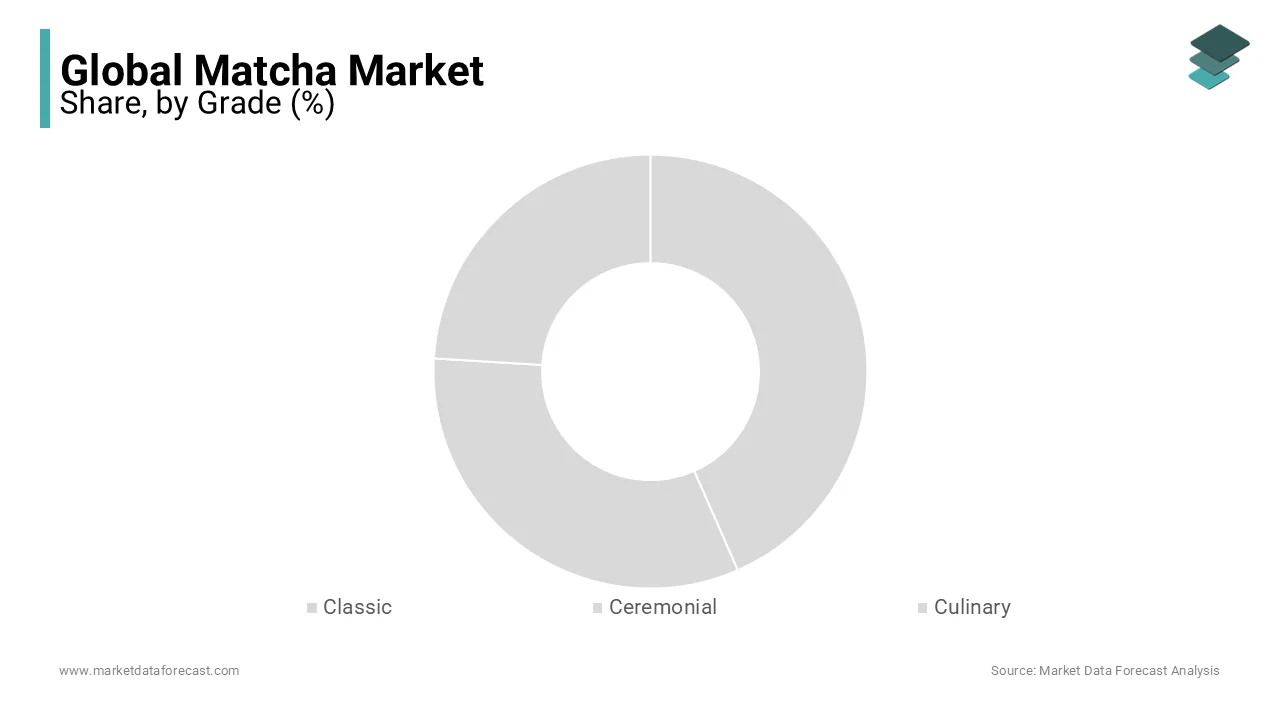

Based on grade, the culinary grade segment dominated the global matcha market by accounting for 56.4% of the market share in 2026. The segment's leadership is attributed to its extensive use in industrial food and beverage manufacturing, bakery products, desserts, smoothies, and ready-to-drink formulations due to its affordability and versatility.

-

Based on application, the matcha beverages segment held the largest share of 54.3% of the global matcha market in 2025. The segment's dominance is driven by increasing consumer preference for healthy beverages, growing café consumption, and rising demand for premium tea-based drinks.

Regional Insights

-

The global matcha market is witnessing strong growth due to increasing health consciousness, expanding functional food consumption, and growing demand for premium tea products.

-

Asia-Pacific dominated the global matcha market by accounting for 42.3% of the market share in 2025. The region's leadership is supported by its long-standing tea culture, high production of premium-quality matcha, and strong consumer demand in countries such as Japan and China.

Competitive Landscape

The global matcha market is highly competitive, with manufacturers focusing on premium product quality, organic certifications, product innovation, and expansion of global distribution networks to strengthen their market presence. Companies are investing in sustainable sourcing, ready-to-drink formulations, and diversified product portfolios to meet the growing demand for functional and natural food ingredients. Key players operating in the global matcha market include ITO EN Ltd., Tata Global Beverages Ltd., Starbucks Corporation, The Hain Celestial Group Inc., Unilever PLC, Aiya Co. Ltd., The AOI Tea Company, McCormick & Company, Inc., Matchaah Holdings Inc., and The Republic of Tea.

Global Matcha Market Size

The global matcha market size was valued at USD 4.05 billion in 2025, and the global market size is expected to reach USD 4.41 billion in 2026 and is anticipated to reach a valuation of USD 8.72 billion by 2034 and is predicted to register a CAGR of 8.90% from 2026 to 2034.

The matcha is a finely ground powder derived from shade-grown Camellia sinensis leaves, distinguished by its vibrant green hue and high concentration of L-theanine and catechins. Unlike standard green tea, Matcha involves the consumption of the entire leaf, creating a unique nutritional profile that has transitioned from a niche element of Japanese tea ceremonies to a cornerstone of the global functional beverage and culinary sectors. The definition now extends beyond traditional preparation to include Matcha-infused confectionery, dairy alternatives, and cosmetic formulations, reflecting its versatility as a superfood ingredient. As per the Food and Agriculture Organization, the specific shading process, which blocks 90% of sunlight for 20 to 30 days before harvest, is important for boosting chlorophyll levels and amino acid content, defining the quality gradient between ceremonial and culinary grades. The current scenario reflects a surge in global demand that outpaces traditional supply capabilities, driving expansion into new growing regions while raising concerns about authenticity and quality control.

MARKET DRIVERS

Rising Global Demand for Functional Beverages and Clean Label Products

The escalating global preference for natural energy sources and clean label functional beverages, as consumers actively seek alternatives to synthetic caffeine and sugar-laden drinks is levelling up the growth of matcha market. Matcha offers a unique combination of caffeine and L-theanine, an amino acid that promotes relaxation without drowsiness, providing a sustained energy release that avoids the jitters associated with coffee. According to data from the International Food Information Council, over 60% of consumers in North America and Europe stated they are actively trying to reduce their intake of artificial ingredients and seek natural sources of energy in 2024. This behavioral shift drives the incorporation of Matcha into ready-to-drink teas, lattes, and smoothies, positioning it as a premium wellness ingredient. The second critical driver is the growing awareness of Matcha's antioxidant properties, specifically its high concentration of epigallocatechin gallate (EGCG), which is linked to metabolic health and immune support. Furthermore, the rise of the "mindful drinking" movement, where individuals replace alcohol with functional non-alcoholic options, has elevated Matcha to a status symbol in social settings.

Proliferation of Matcha in Food Service and Retail Innovation

The deep integration of Matcha into mainstream coffee culture and the rapid expansion of specialty cafe chains globally by normalizing its consumption and making it accessible to a broader audience is additionally propelling the growth of matcha market. Major international coffee retailers have permanently added Matcha lattes and frappes to their core menus, exposing millions of customers to the product daily and demystifying its preparation. This visibility drives retail sales as consumers attempt to replicate cafe experiences at home, purchasing wholesale powders and brewing kits. The second critical driver is the innovation in retail formats, such as single-serve sachets, Matcha-infused snacks, and fortified cereals, which lower the barrier to entry for consumers intimidated by traditional whisking methods. Furthermore, social media platforms like Instagram and TikTok have amplified the visual appeal of vibrant green Matcha drinks, creating viral trends that drive foot traffic to cafes and online stores. This fusion of cafe culture, retail accessibility, and digital virality ensures continuous market expansion.

MARKET RESTRAINTS

High Production Costs and Labor Intensity

The inherently labor-intensive nature of cultivation and processing, resulting in high production costs that limit affordability and mass adoption is solely restricting the growth of matcha market. The requirement to shade tea plants for 20 to 30 days prior to harvest, followed by hand-picking only the youngest leaves, demands substantial manual labor and precise timing, which cannot be easily mechanized without compromising quality. According to agricultural reports from the Shizuoka Prefectural Government, the cost of producing authentic stone-ground Matcha is approximately 10 times higher than that of standard green tea due to these specialized steps. This cost structure forces retail prices to remain premium, excluding price-sensitive consumers and restricting the market to niche segments. The second critical driver of this restraint is the slow traditional stone-grinding process, where granite mills can only produce about 40 grams of powder per hour to prevent heat damage that alters flavor and nutrient profiles.. Furthermore, the scarcity of skilled artisans capable of overseeing the tencha (de-veined leaf) processing adds to the operational constraints. Statistics from labor organizations in Japan reveal an aging workforce in the tea sector, with fewer young people entering the profession, exacerbating the labor shortage. These structural inefficiencies ensure that authentic Matcha remains a luxury good, hindering its penetration into mass-market applications where cost is the primary decision factor.

Quality Adulteration and Lack of Standardization

The widespread prevalence of counterfeit and adulterated products in the global marketplace poses a severe challenge to consumer trust is also hampering the growth of matcha market. Unscrupulous suppliers often mix lower-grade green tea powder with sugar, milk powder, or artificial green food coloring to mimic the appearance and sweetness of high-quality Matcha, selling these inferior blends at premium prices. This deception leads to negative consumer experiences, as the bitter taste and lack of expected health benefits discourage repeat purchases and tarnish the reputation of the entire category. The second critical driver of this restraint is the absence of a universally enforced legal definition for "Matcha," allowing manufacturers to use the term loosely for any powdered green tea, regardless of cultivation or processing methods. Data from industry watchdogs indicates that the lack of clear labeling standards makes it difficult for average consumers to distinguish between authentic stone-ground Matcha and machine-ground imitations. Furthermore, the difficulty in visually identifying adulteration without laboratory testing empowers bad actors to flood the market with cheap alternatives.

MARKET OPPORTUNITIES

Expansion into Emerging Markets and Product Diversification

The untapped potential in emerging countries, across the Asia-Pacific and Latin American regions to diversify its revenue streams beyond saturated Western economies is significantly to create new opportunities for the growth of matcha market. While Japan remains the cultural home and North America a mature market, countries like China, India, Brazil, and Mexico are witnessing a rising middle class with increasing disposable income and a growing fascination with global wellness trends. According to economic data from the World Bank, the middle-class population in these regions is projected to add 150 million new consumers by 2026 by creating a vast new customer base for premium health products. This demographic shift drives demand for functional beverages and exotic ingredients as status symbols and health enhancers. The second critical driver is the adaptation of Matcha into local flavor profiles and culinary traditions, such as incorporating it into traditional sweets, beverages, and savory dishes that resonate with local palates. Furthermore, the expansion of modern retail infrastructure and e-commerce platforms in these regions facilitates easier access to imported goods, overcoming previous distribution barriers.

Sustainability and Direct Trade Initiatives

The growing consumer demand for sustainably sourced and ethically produced ingredients to differentiate itself through regenerative agriculture and direct trade initiatives is also to enhance the growth of matcha market. Conscious consumers are increasingly willing to pay a premium for products that support soil health, biodiversity, and fair wages for farmers, aligning with the holistic ethos of the tea ceremony. This trend encourages producers to adopt organic farming, reduce water usage, and eliminate synthetic chemicals, thereby enhancing the quality and safety of the final product. Furthermore, regenerative practices can improve long-term crop resilience against climate change, securing the future supply of high-quality leaves. Statistics from agricultural pilot programs show that tea farms using regenerative methods reported a 15% increase in soil organic matter and improved yield stability.

MARKET CHALLENGES

Climate Change and Agricultural Vulnerability

The escalating impacts of climate change, including erratic weather patterns, rising temperatures, and unpredictable rainfall by threatening the stability of yields and the delicate quality parameters of the tea leaves is to act as a major barrier for the growth of matcha market. Matcha cultivation requires precise climatic conditions, particularly cool nights and consistent mist during the shading period, to develop the characteristic umami flavor and vibrant green color. According to agricultural climate assessments from the Intergovernmental Panel on Climate Change, tea-growing regions in Japan have experienced a 1.5 degree Celsius increase in average temperatures over the past three decades, leading to earlier harvests and altered chemical compositions in the leaves. This warming trend can reduce the concentration of L-theanine and increase bitterness, degrading the sensory profile that defines premium Matcha. The second significant factor is the increased frequency of extreme weather events such as typhoons and late frosts, which can physically damage crops and devastate annual harvests. Furthermore, shifting pest and disease patterns due to warmer winters force farmers to choose between increased pesticide use, which compromises organic status, or accepting lower yields.

Water Scarcity and Resource Competition

Increasing water scarcity and competition for freshwater resources in key tea-growing regions, as tea cultivation is water-intensive and vulnerable to drought conditions is also another factor to hinder the growth of matcha market. The shading process and the maintenance of lush tea bushes require consistent irrigation, which becomes difficult during prolonged dry spells exacerbated by climate change. As per hydrological data from the World Resources Institute, several prefectures in Japan facing high water stress levels have implemented restrictions on agricultural water usage, directly impacting tea farm operations. This scarcity forces producers to invest in expensive irrigation infrastructure or face reduced yields, driving up production costs. The competition for water with urban populations and other agricultural sectors, which prioritizes drinking water and staple crops over specialty tea during shortages. Additionally, the environmental footprint of water usage is coming under scrutiny from sustainability-focused consumers and regulators, pressuring brands to demonstrate efficient water management. Statistics from lifecycle assessments indicate that the water footprint of Matcha is significantly higher per kilogram than steeped tea due to the whole-leaf consumption ratio.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.90% |

| Segments Covered | By Grade, Application, and Region |

| Various Analyses Covered | Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | ITO EN Ltd, Tata Global Beverages Ltd., Starbucks Corporation, The Hain Celestial Group Inc, Unilever PLC, Aiya-Co. Ltd, The AOI Tea Company, McCormick & Company, Inc, Matchaah Holdings Inc, The Republic of Tea |

SEGMENTAL ANALYSIS

By Grade Insights

The culinary grade segment was accounted in holding 56.4% of the matcha market share in 2026 with the extensive versatility of this grade in industrial food and beverage manufacturing, where its robust flavor profile and cost-effectiveness make it the ideal ingredient for mass-market products. The exponential growth of the ready-to-drink (RTD) tea and functional beverage sectors, which utilize culinary Matcha to infuse lattes, smoothies, and sodas with color and antioxidants without the prohibitive cost of ceremonial grade. According to data from the International Food Information Council, over 68% of new product launches featuring green tea in 2024 utilized culinary grade powder due to its optimal balance of price and performance in complex formulations involving milk and sweeteners. The expansion of the global bakery and confectionery industries, where Matcha is increasingly incorporated into cakes, cookies, ice creams, and chocolates. Furthermore, the lower price point allows large-scale food manufacturers to incorporate Matcha into everyday consumer goods, democratizing access beyond niche health stores.

The ceremonial grade segment is projected to register a CAGR of 13.2% throughout the forecast period with a global surge in interest regarding traditional Japanese tea culture, mindfulness practices, and the premiumization of the wellness sector where consumers seek the highest quality experiences. The increasing demand for authentic, high-purity products that offer maximum health benefits, specifically the elevated concentrations of L-theanine and catechins found only in the youngest, shade-grown leaves reserved for ceremonial use. As per research, sales of premium superfood powders marketed for "meditative rituals" and "pure consumption" grew by 38% in 2024, with ceremonial Matcha leading this niche as consumers become more educated about grade distinctions. The influence of digital content creators and social media platforms that the superior taste, texture, and nutritional profile of ceremonial varieties, distinguishing them from bitter culinary blends. Statistics from digital engagement reports show that hashtags related to "traditional matcha ceremony" and "pure matcha" generated over 250 million impressions in 2024, directly correlating with a surge in direct-to-consumer sales of high-end powders. Additionally, the rise of specialty tea houses and luxury cafes offering traditional whisked Matcha experiences has elevated the status of ceremonial grade from an obscure import to a desirable lifestyle symbol.

By Application Insights

The matcha beverages segment was accounted in holding 54.3% of the global Matcha market share in 2025. The growth of the segment is primarily driven by the seamless integration of Matcha into global coffee shop culture and the booming ready-to-drink tea industry, where it serves as a popular caffeine alternative for millions of consumers daily. The widespread adoption of Matcha lattes and frappes by major international coffee chains and independent cafes, which have normalized the consumption of Matcha as a staple menu item alongside espresso-based drinks. The innovation in bottled and canned Matcha beverages, which offer convenience and portability for on-the-go consumers seeking functional energy boosts without the jitters associated with high-caffeine coffee. Furthermore, the perception of Matcha as a "clean energy" source resonates strongly with health-conscious demographics, prompting frequent purchases in both food service and retail channels.

The personal care segment is likely to witness a fastest CAGR of 15.4% during the forecast period with the "clean beauty" movement and the increasing incorporation of natural, antioxidant-rich ingredients into skincare and cosmetic formulations globally. The scientifically validated efficacy of Matcha's polyphenols, particularly epigallocatechin gallate (EGCG), in reducing inflammation, combating acne, and protecting skin from environmental stressors by making it a highly sought-after active ingredient for serums, masks, and cleansers. The marketing appeal of Matcha's vibrant green color and its association with holistic wellness, which allows brands to create visually striking products that resonate deeply with eco-conscious consumers on social media platforms. Statistics from product launch databases show that new skincare items featuring Matcha increased by 42% in 2024, with many brands highlighting "food-grade" safety and sustainability as key selling points. Additionally, the versatility of Matcha allows for its use in a wide range of personal care items, including soaps, shampoos, and even makeup, broadening its market reach beyond traditional skincare.

REGIONAL ANALYSIS

Asia Pacific Matcha Market Analysis

Asia Pacific was the top performer in the match market by holding 42.3% of share in 2025. The growth of the market in this region is driven by the sophisticated consumer base that distinguishes clearly between grades and demands the highest standards of authenticity and freshness. A key driving factor is the domestic consumption in Japan, where Matcha is not merely a trend but a centuries-old tradition embedded in daily life, religious practices, and hospitality by ensuring a stable and high-volume baseline demand. According to data from the Japanese Ministry of Agriculture, Forestry and Fisheries, domestic per capita consumption of green tea powder in Japan remained steady at 1.2 kilograms annually in 2024, supported by a robust network of local producers and distributors. The rapid modernization of tea culture in neighboring countries like South Korea and China, where younger generations are embracing Matcha as a trendy, healthy alternative to sugary soft drinks and coffee. Furthermore, the region serves as the primary export hub, with advanced logistics networks facilitating the distribution of fresh Matcha to the rest of the world.

North America Matcha Market Analysis

North America was positioned second by holding 28.3% of the matcha market share in 2025 with its role as the primary driver of global Matcha trends through innovative product formats and aggressive marketing in the wellness sector. The massive expansion of the specialty coffee and cafe culture, where major chains have permanently integrated Matcha lattes and refreshers into their core menus by exposing millions of consumers to the product daily. The proliferation of Matcha in the retail grocery sector in the form of ready-to-drink bottles, protein bars, and baking mixes, which has democratized access beyond specialty stores. Additionally, the strong influence of social media influencers and wellness bloggers in the region continues to educate consumers on the benefits of L-theanine, fueling repeat purchases.

Europe Matcha Market Analysis

Europe matcha market growth is likely to grow at an anticipated CAGR in coming years with a growing appreciation for functional foods, stringent quality standards, and a burgeoning cafe culture that embraces alternative beverages. The high demand for certified organic and sustainably sourced Matcha, as European consumers are particularly vigilant about pesticide residues and ethical farming practices. The rising awareness of mental wellness and stress management, with Matcha being widely adopted for its unique ability to provide calm focus, a benefit that resonates strongly in high-pressure urban environments across cities like London, Berlin, and Paris. The integration of Matcha into the gourmet food and confectionery sectors, where pastry chefs and chocolatiers utilize the ingredient to create premium desserts that appeal to discerning palates. Furthermore, the expansion of dedicated tea salons and wellness centers offering traditional preparation methods is educating consumers and driving retail sales of high-grade powders.

Latin America Matcha Market Analysis

Latin America matcha market growth is likely to be driven by the evolving beverage landscape, a young demographic eager to try global trends, and a growing middle class with increasing disposable income. The market status in this region is defined by the adaptation of Matcha into local flavor profiles and consumption habits, such as blending it with tropical fruits, milk, and traditional sweeteners to suit regional tastes. According to data from the Latin American Health and Wellness Institute, the functional beverage market in the region grew by 15% in 2024, with Matcha emerging as a key ingredient in new product launches. The influence of global tourism and international cafe chains entering the market, which introduce Matcha to local populations and normalize its consumption as a fashionable lifestyle choice. Additionally, the rise of local entrepreneurs launching Matcha-focused startups and juice bars is fostering a domestic ecosystem that supports further growth.

Middle East and Africa Matcha Market Analysis

The Middle East and Africa matcha market growth is likely to grow with a nascent but rapidly growing interest in premium health products, luxury dining experiences, and the diversification of beverage options in key urban hubs. The booming luxury hospitality and cafe sector in cities like Dubai, Riyadh, and Doha, where international brands compete to offer the latest global food trends, including high-end Matcha ceremonies and artisanal lattes. The increasing awareness of preventive healthcare and nutrition among the younger population, who are shifting away from traditional sugary teas towards functional beverages that offer tangible health benefits. Furthermore, the expansion of modern retail infrastructure and e-commerce platforms is improving access to imported Matcha products by allowing consumers in remote areas to participate in the trend.

COMPETITIVE LANDSCAPE

The competition in the Matcha market is intensely fierce characterized by a rivalry between established Japanese heritage brands and agile new entrants from various regions vying for dominance through authenticity and innovation. Major players leverage their deep roots in traditional cultivation and proprietary grinding technologies to offer superior taste profiles that define category standards for quality. The landscape sees frequent launches of organic and single-origin products as companies race to capture the growing segment of health-conscious consumers who prioritize transparency and purity. Competitive pressure is heightened by the rise of private label brands from large retailers that offer comparable quality at lower prices forcing established names to justify premium positioning through storytelling and certifications. Sustainability has emerged as a critical battleground where firms compete to prove their environmental credentials through regenerative agriculture and plastic-free packaging.

KEY MARKET PLAYERS

The key players in the matcha market are

- ITO EN Ltd

- Tata Global Beverages Ltd.

- Starbucks Corporation

- The Hain Celestial Group Inc.

- Unilever PLC

- Aiya Co. Ltd

- The AOI Tea Company

- McCormick and Company Inc

- Matchaah Holdings Inc

- The Republic of Tea

Top Players in the Matcha Market

- Ito En Ltd stands as a pioneering force in the global Matcha market by leveraging its extensive expertise in green tea processing and distribution to deliver high-quality products worldwide. The company contributes significantly to the international sector by standardizing quality control measures and introducing innovative ready-to-drink Matcha beverages that appeal to modern consumers. Recently Ito En has strengthened its position by expanding its production facilities in Japan to ensure a stable supply of ceremonial and culinary grade powders amidst rising global demand. They have also launched new organic Matcha lines tailored for health-conscious markets in North America and Europe. These strategic moves ensure they maintain leadership in both traditional and contemporary segments while adhering to strict safety standards. Their continuous investment in research ensures they set industry benchmarks for flavor consistency and nutritional value in every batch.

- Aiya America Inc operates as a leading supplier renowned for producing premium Matcha powder that serves both the food service industry and retail consumers across the globe. Their global contribution involves setting rigorous standards for stone grinding techniques and shade growing practices that define authentic Matcha quality. To fortify their market stance the company recently expanded its direct-to-consumer digital platforms to reach individual buyers seeking ceremonial grade experiences at home. They have also partnered with major coffee chains to introduce exclusive Matcha blends that highlight their unique flavor profiles. Furthermore, Aiya has enhanced its sustainability initiatives by sourcing exclusively from certified organic farms and reducing carbon footprints in logistics. These initiatives demonstrate their commitment to preserving traditional methods while adapting to modern distribution channels to maintain relevance and leadership in a competitive environment.

- Marukyu Koyamaen Co Ltd maintains a formidable presence in the Matcha market through its centuries-old heritage and dedication to producing the highest grade ceremonial powders used in traditional tea ceremonies. The company contributes to the global market by educating international consumers on the nuances of Matcha grades and promoting the cultural significance of proper preparation. Recent actions to strengthen their position include the establishment of new training centers in key export markets to teach baristas and chefs how to utilize their products effectively. They have also introduced limited edition harvests that cater to luxury confectioners and high-end restaurants seeking exclusivity. Additionally, Marukyu Koyamaen has optimized its export logistics to ensure freshness upon arrival in distant markets.

Top Strategies Used by Key Market Participants

Key players in the Matcha market primarily employ strategies focused on vertical integration and quality assurance to control the supply chain from cultivation to final packaging. Companies are heavily investing in organic certification and sustainable farming practices to meet stringent global food safety regulations and appeal to eco-conscious consumers. Another major strategy involves diversifying product portfolios to include ready-to-drink beverages, supplements, and cosmetic formulations that expand usage beyond traditional tea brewing. Brands are also leveraging digital marketing and educational campaigns to differentiate between grades and teach consumers about proper preparation methods. Additionally, participants utilize strategic partnerships with cafes and restaurants to increase brand visibility and normalize Matcha consumption in daily routines.

MARKET SEGMENTATION

This research report on the global matcha market has been segmented and sub-segmented based on grade, Application, & region.

By Grade

- Classic

- Ceremonial

- Culinary

By Application

- Regular Tea

- Matcha Beverages

- Food

- Personal Care

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1.What is the matcha market?

The matcha market covers the production, processing, distribution, and consumption of matcha, a finely ground powdered green tea widely used in beverages, food products, cosmetics, and nutraceuticals.

2.What factors are driving growth in the matcha market?

Growth is driven by rising health consciousness, increasing demand for natural antioxidants, growing popularity of functional beverages, and expanding use in food and personal care products.

3.What are the main applications of matcha?

Matcha is primarily used in beverages such as tea and lattes, followed by applications in bakery products, desserts, ice creams, supplements, and skincare products.

4.Which regions dominate the global matcha market?

Asia Pacific, particularly Japan, dominates the market, while North America and Europe are emerging regions due to increasing consumer awareness and adoption.

5.How does health awareness influence matcha consumption?

Matcha is rich in antioxidants, amino acids, and catechins, which supports metabolism, energy levels, and overall wellness, driving consumer demand.

6.What role does the food and beverage industry play in the matcha market?

The food and beverage industry is the largest end user, using matcha in ready to drink beverages, snacks, confectionery, and functional foods.

7.How important is organic matcha in the market?

Organic matcha is gaining popularity as consumers prefer clean label, pesticide free, and sustainably sourced products.

8.What challenges does the matcha market face?

Key challenges include high production costs, limited supply of premium grade matcha, quality consistency, and price sensitivity.

9.What packaging formats are commonly used for matcha?

Common packaging formats include tins, pouches, sachets, and jars designed to preserve freshness and flavor.

10. What is the future outlook for the matcha market?

The market is expected to grow steadily, supported by health trends, product diversification, and increasing adoption across food, beverage, and wellness sectors.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com