Ireland Cards And Payments Market Size, Share, Trends, & Growth Forecast Report By Cards (Debit Cards, Credit Cards, and Prepaid Cards), Payment Terminals (POS And ATMs), Payment Instruments (Credit Transfers, Direct Debit, Cheques, and Payment Cards), Industry Analysis From 2025 to 2033

Ireland Cards And Payments Market Size

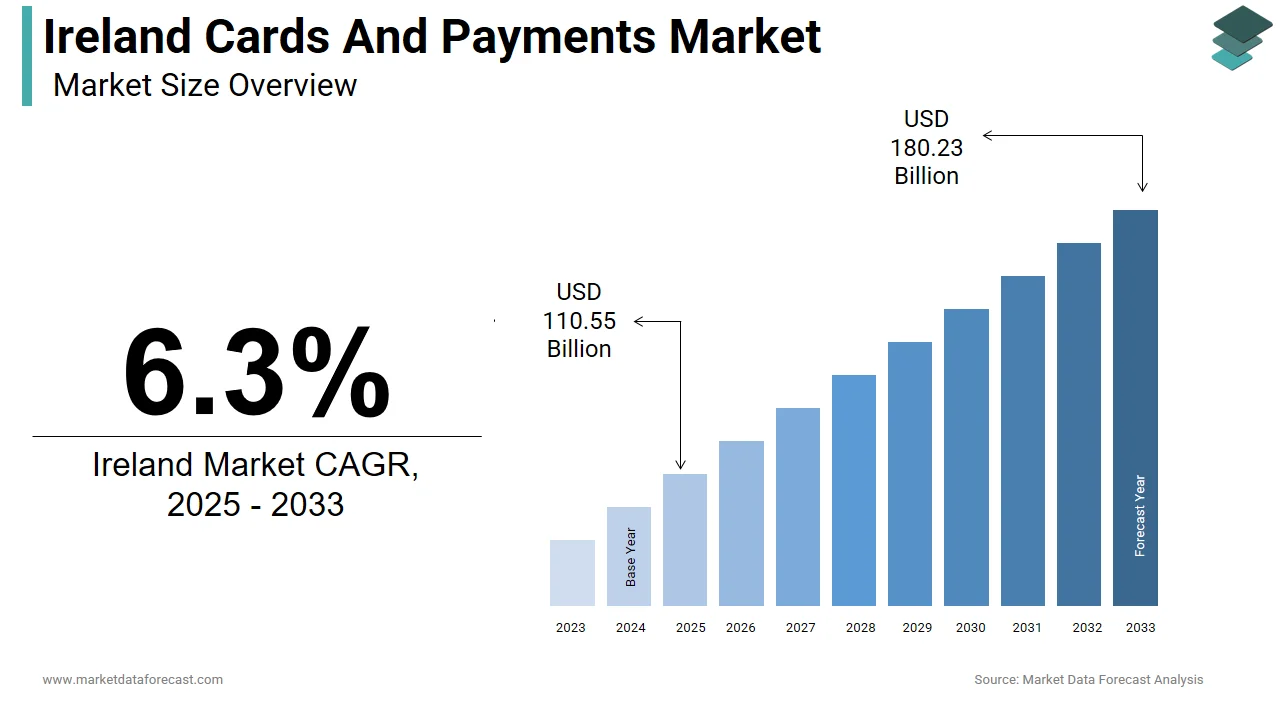

The Ireland cards and payments market size was valued at USD 104 billion in 2024. This market is expected to grow at a CAGR of 6.3% from 2025 to 2033 and be worth USD 180.23 billion by 2033 from USD 110.55 billion in 2025.

The Ireland cards and payments market is steadily growing. Presently, it is heavily dominated by credit and debit cards and uses cash with decent frequency, i.e., about 20 percent of all the sales are settled in cash. As per the research, total card payments in the country stood at 8.54 billion Euros in May 2024, which is 380 million euros more than 8.16 billion euros in April 2024. The value of card Payments in Ireland surged by 4.7 percent. Moreover, the market growth in value is propelled largely by domestic and, to some extent, by non-domestic card payments, rising by 320 million euros, i.e., 4.8 percent, and 60 million euros, 4.1 percent, respectively. Similarly, the card payment amount grew from 213.8 million to 225.4 million by 5.4 percent.

However, the market is expected to face resistance from the Irish Government’s efforts towards mandating cash acceptance at selected retailers. In January 2024, Finance Minister of Ireland Michael McGrath received approval from the government for the General Scheme of the Access to Cash Bill.

MARKET DRIVERS

Strong Digital Infrastructure and High Internet Penetration

Ireland’s advanced digital infrastructure and high internet penetration rates are crucial elements of the cards and payments market, enabling seamless adoption of digital and contactless payment solutions. The Central Bank of Ireland reported that in 2023, card payments accounted for 58% of all retail transactions, with contactless payments growing by 22% year-on-year. Also, Visa Europe’s 2023 Payment Insights Report noted that contactless spending in Ireland rose to EUR 4.1 billion, representing over 60% of all face-to-face card transactions. Mobile wallet usage is also on the rise, with services like Apple Pay, Google Pay, and Samsung Pay gaining traction across retailers and service providers. A 2023 survey by PwC Ireland found that 71% of consumers preferred using contactless cards or mobile wallets for purchases under EUR 50, reflecting a behavioral shift toward convenience-driven payment methods. This robust digital ecosystem encourages financial institutions and fintechs to innovate, expand their offerings, and improve customer engagement through enhanced payment experiences, thereby driving sustained growth in the Irish cards and payments sector.

Increasing E-commerce Activity and Online Spending Growth

The expansion of e-commerce in Ireland has greatly influenced the demand for secure and efficient card-based payment solutions. This surge in digital commerce has directly increased the use of debit and credit cards for online transactions.

Data from Stripe indicated that online card transaction volume grew substantially in 2023 and was driven by both domestic and cross-border trade. Apart from these, the Central Bank of Ireland reported that online card payments reached EUR 19.3 billion in value during 2023, which is marking a year-over-year increase of 14%. Ireland's position as a global hub for multinational tech firms hosting the European headquarters of companies like Google, Meta, and PayPal has further reinforced its digital economy and payment innovation landscape.

MARKET RESTRAINTS

Persistent Cash Usage among Older Demographics and Small Businesses

Despite Ireland's strong digital payment infrastructure, cash remains a preferred mode of payment among older demographics and small businesses, acting as a restraint on the broader adoption of card-based transactions. According to the Central Bank of Ireland’s 2023 Retail Payments Report, 31% of all retail transactions were still conducted in cash, with individuals over 65 being twice as likely to use cash compared to those under 35. Furthermore, small businesses in rural areas often continue to accept only cash due to high merchant fees or limited POS terminal availability. The Irish Small and Medium Enterprises Association (ISME) reported that in 2023, 22% of micro-businesses did not offer card payment optio

ns, particularly in sectors such as hospitality, personal services, and local markets. This persistent reliance on cash limits transaction data visibility and constrains the growth potential of card issuers and payment processors, especially in less urbanized regions.

Regulatory Complexity and Compliance Burden

Ireland’s financial sector operates under a stringent regulatory framework shaped by both national policies and EU directives such as PSD2 (Revised Payment Services Directive) and GDPR (General Data Protection Regulation). While these regulations aim to enhance transparency and consumer protection, they also impose significant compliance costs and operational complexities on banks and fintech firms. In line with the Deloitte 2023 FinTech Survey, 44% of Irish fintech startups identified regulatory compliance as a top barrier to scaling their payment solutions, with delays in licensing and ongoing reporting requirements slowing product development. Additionally, the Central Bank of Ireland reported in 2023 that compliance-related expenses for smaller payment institutions had risen by approximately 16% since the implementation of stricter anti-money laundering (AML) protocols, and is reducing profitability and limiting investment in new technologies.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services

Ireland presents a growing opportunity for Buy Now, Pay Later (BNPL) services, driven by increasing consumer demand for flexible payment options and a digitally engaged younger demographic. BNPL allows shoppers to split purchases into interest-free installments, aligning with the financial preferences of millennials and Gen Z. A 2023 survey by Irish Times Insight found that 29% of online shoppers had used BNPL services at least once, signaling growing mainstream acceptance. Major international players such as Klarna, Afterpay, and PayPal have expanded their operations in Ireland, integrating seamlessly with leading e-commerce platforms including Amazon Ireland, Dunnes Stores, and Littlewoods Ireland. According to Mastercard’s 2023 Fintech Outlook, a growing number of Irish retailers now offer BNPL as a payment option, reflecting increasing merchant adoption. Banks and card issuers can leverage this trend by embedding installment features into existing card products, enhancing customer engagement and boosting transaction volumes while catering to evolving consumer finance demands.

Rise of Embedded Finance and Super App Integration

Embedded finance, where financial services like payments, lending, and insurance are integrated into non-financial platforms, is gaining momentum in Ireland, offering a transformative opportunity for the cards and payments market. With increasing smartphone adoption and digital service consumption, super apps and platforms are incorporating payment solutions to streamline user experiences. A 2023 report by McKinsey & Company highlighted that Ireland was among the fastest-growing markets in Europe for embedded finance, with transaction values surpassing EUR 1.8 billion in 2023, growing at a notable rate since 2020. Platforms like Just Eat, Ryanair, and Vinted have introduced in-app payment capabilities, allowing users to transact without switching between banking apps or using physical cards. Additionally, AIB (Allied Irish Bank) and Revolut have launched open banking APIs to enable third-party developers to integrate financial services into their applications, accelerating the adoption of card-based payments across ecosystems. According to EY Ireland’s 2023 Digital Payments Survey, 52% of consumers prefer making payments through integrated platforms rather than standalone banking apps, emphasizing the shift in user behavior.

MARKET CHALLENGES

Rising Cybersecurity Threats and Fraud Incidents

As Ireland continues its digital transformation, the frequency and sophistication of cyberattacks targeting financial transactions have surged, posing a major challenge to the cards and payments industry. According to Ireland’s National Cyber Security Centre (NCSC), cybercrime incidents increased notably in 2023, with online payment fraud accounting for a major share of all reported cases. Card-not-present (CNP) fraud remains a critical concern, particularly with the rise in e-commerce transactions. The Central Bank of Ireland reported in 2023 that CNP fraud losses totaled EUR 112 million, representing a year-on-year increase of 19%. Phishing scams, malware attacks, and data breaches have contributed to declining consumer confidence in digital payments, especially among older users. Moreover, Europol’s 2023 Internet Organised Crime Threat Assessment (IOCTA) identified Ireland as one of the top ten EU countries affected by online payment fraud, with criminals exploiting weak authentication mechanisms and stolen card credentials. Balancing robust security with seamless user experience remains a key challenge for Ireland’s payments sector as it continues to evolve.

Uneven Adoption across Urban and Rural Areas

While Ireland’s urban centers, such as Dublin, Cork, and Galway, enjoy high levels of digital payment adoption, disparities persist in rural and regional areas, hindering the uniform growth of the cards and payments market. This digital divide affects both consumers and merchants. Many small businesses in rural Ireland still rely on cash due to limited access to POS terminals or unstable internet connections required for card transactions. A 2023 report by the Irish Farmers’ Association (IFA) found that 31% of rural traders lacked the necessary infrastructure to accept card payments, constraining transaction opportunities. On the consumer side, Central Statistics Office (CSO) Ireland data shows that digital payment adoption among residents in rural provinces was lower than in metropolitan areas, primarily due to low digital literacy and lack of access to mobile banking services.

SEGMENTAL ANALYSIS

By Cards Insights

The debit cards segment is by far the most dominant method in the Irish cards and payments market. This is because of the consumer’s inclination towards debit cards when in a physical location, especially popular among those aged under 45. Also, the major reason for people to go to the branch, i.e., 63 per cent, is to withdraw/lodge cash. Further, debit cards are more prevalent in areas of Leinster (54 per cent), Munster (50 per cent), Connacht/Ulster (60 per cent), and Dublin (42 per cent). However, with modest growth in smartphone payments, debit cards saw a slight decline in 2023.

The credit cards segment in the second has also grown considerably in the last few years, as every 1 person in 3 people possess one. Moreover, the segment market growth can be attributed to the preference of current account holders who are believed to stick with their primary financial provider for credit cards, overdrafts, and saving accounts. Another factor supporting the market is low switching behaviour from one service to another.

By Payment Terminals Insights

The POS segment registered the highest growth rate and is expected to further propel during the forecast period for the Ireland cards and payments market. This dominance can be attributed to the sharp increase in contactless payments, which account for about 85 per cent of card-based point-of-sale payments. In terms of per capita contactless payment, Dublin gained the top spot with 394 in the twelve months ending on March 2024. This is more than the national average, i.e., 40 per cent more. Apart from this, the ability to generate higher returns on investment, along with its accessibility, is influencing the segment’s market size. Further, its extensive application in varied industries involving transportation, accommodation, hospitality, and retail has substantially boosted the market growth in recent years.

On the other hand, the ATM segment is witnessing moderate growth and is expected to play an important role in the Ireland cards and payments. For instance, in February 2024, the Bank of Ireland reported an investment of 60 million euros to enhance the nation’s ATM network. This will significantly elevate the segment’s market growth rate as it is the biggest investment in the country’s cash infrastructure in the last 10 years. Besides this, these still command the industry in respect of cash withdrawals and have surged in popularity in 2023. Also, they are utilised by around 78 per cent of adults, which is up five percentage points, and cashback from merchants has dropped slightly.

By Payment Instruments Insights

The payment cards segment holds the maximum portion of the Ireland cards and payments market and is anticipated to continue its position during the forecast period. The segment’s market growth can be credited to the extensive usage through different card transactions in the second quarter of 2023, totalling 10.4 billion euros in value and 3.6 billion in volume including In-person payments in the first, domestic contactless payments in the second, domestic mobile wallet payments in third, online payments in fourth and cash withdrawals in the last. Therefore, the segment is believed to grow further in the coming years as it accounted for around 63 per cent of overall payment volume in 2023. The credit transfers segment has positioned itself at the second spot then the direct debt segment.

REGIONAL ANALYSIS

The Ireland cards and payments market growth witnessed a major rise in payment transactions since the second quarter of 2023. This is primarily propelled by the entry of a new payment service company in the Irish industry and heightened payment transactions in 2023 of 4.14 billion, which is a 36 percent surge from 2022’s 3.05 billion. However, the market in the country is greatly lagging in the accessibility of instant payments and is at 22 position in the European Union’s ranking among its own countries. This is an extremely negative trend from the aspect of customers and companies in the country.

KEY MARKET PARTICIPANTS

Top players in the Ireland cards and payments market include

- Allied Irish Bank

- Bank of Ireland

- Ulster Bank

- Permanent TSB

- Avantcard

IRELAND CARDS AND PAYMENTS MARKET NEWS

- In January 2024, Revolut Press released its partnership with Aer Lingus. Rovolut will provide Revolut Pay payment technology to the consumers of Aer Lingus. This is a one-click service at checkout which will help Revolut increase its customer base and enable its Irish and worldwide to book flights with the airline without the requirement to fill their payment information.

- In December 2023, NomuPay, an Ireland-based company, reported the completion of the purchase of Total Processing, the UK-based merchant services and bespoke payment processing company. The ultimate objective of the company is to expand its reach across Europe, Southeast Asia, Turkey and the Middle East. The acquisition will strengthen the business operation due to Total Processing’s customer-centric approaches.

MARKET SEGMENTATION

This research report on the Ireland cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

- Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What defines the Ireland cards and payments market?

The Ireland cards and payments market encompasses debit, credit, and prepaid cards alongside digital alternatives, driven by consumer shift to non-cash methods.

2. How does the Ireland cards and payments market evolve?

The Ireland cards and payments market advances through rising contactless and mobile integration, reflecting broader digital transformation trends.

3. What drives changes in the Ireland cards and payments market?

Technological adoption and e-commerce expansion propel the Ireland cards and payments market toward diversified payment options.

4. Who leads the Ireland cards and payments market?

Major banks and international networks dominate the Ireland cards and payments market with innovative card and digital offerings.

5. What role do debit cards have in the Ireland cards and payments market?

Debit cards form a core segment of the Ireland cards and payments market, preferred for everyday transactions and accessibility.

6. How prominent are contactless payments in the Ireland cards and payments market?

Contactless features are widespread in the Ireland cards and payments market, enhancing speed and convenience for users.

7. What impact do mobile wallets have on the Ireland cards and payments market?

Mobile wallets integrate seamlessly into the Ireland cards and payments market, offering quick and secure transaction alternatives.

8. How does e-commerce influence the Ireland cards and payments market?

E-commerce boosts demand for reliable cards in the Ireland cards and payments market, supporting online shopping growth.

9. What is BNPL's place in the Ireland cards and payments market?

Buy Now Pay Later options emerge within the Ireland cards and payments market, appealing to flexible spending preferences.

10. Are QR payments growing in the Ireland cards and payments market?

QR code solutions gain traction in the Ireland cards and payments market for retail and peer-to-peer uses.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com