Sweden Cards And Payments Market Size, Share, Trends, & Growth Forecast Report by Cards (Debit Cards, Credit Cards, Prepaid Cards), Payment Terminals (POS And ATM's), Payment Instruments (Credit Transfers, Direct Debit, Cheques And Payment Cards), Industry Analysis From 2025 to 2033

Sweden Cards and Payments Market Size

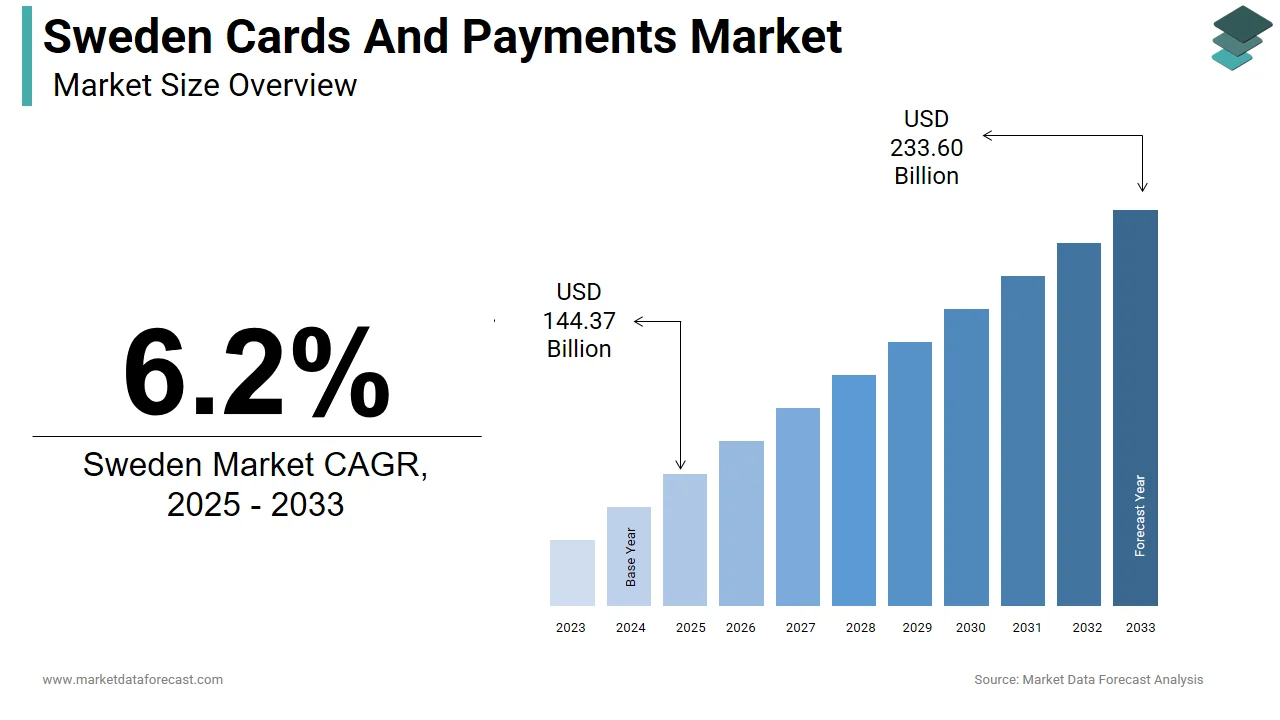

The sweden cards and payments market was valued at USD 135.94 billion in 2024. The sweden market is predicted to reach USD 144.37 billion in 2025 and USD 233.60 billion by 2033, growing at a CAGR of 6.2% during the forecast period.

MARKET DRIVERS

Rapid Growth in E-commerce and Digital Transactions

Spain’s cards and payments market is being significantly driven by the rapid expansion of its e-commerce sector, which has intensified demand for secure and convenient digital payment methods. This surge in online shopping has directly increased the use of debit and credit cards as the preferred mode of payment. Data from Redsys, Spain’s leading payment gateway provider, indicates that in 2023, card payments accounted for a significant portion of all online transactions, with international card networks like Visa and Mastercard dominating the space. Additionally, the Bank of Spain reported that contactless card payments grew by 16% year-on-year, with over EUR 28 billion processed via NFC-enabled cards. The rise in mobile commerce (m-commerce) has further boosted this trend. A report by Comscore found that mobile devices accounted for a significant portion of all digital transactions in Spain, reinforcing the need for seamless card integration across platforms.

Government Support for Financial Inclusion and Digital Transformation

The Spanish government has actively promoted financial inclusion and digital transformation through policy reforms and public-private partnerships, contributing to the expansion of the cards and payments market. According to the European Commission’s Digital Economy and Society Index (DESI) 2023, Spain ranked 12th out of 27 EU countries, showing strong progress in digital connectivity and internet usage. The Bank of Spain also reported that over 98% of adults had access to a bank account in 2023, up from 94% in 2018, largely due to targeted financial inclusion programs. Apart from these, the widespread deployment of Point of Sale (POS) terminals, which exceeded 2.4 million units nationwide in 2023, according to report, has enabled greater acceptance of card-based transactions across small businesses and rural areas.

MARKET RESTRAINTS

High Preference for Cash among Older Generations

Despite Spain's progress toward digitization, a significant portion of the population, particularly older generations, continues to rely on cash for daily transactions, posing a restraint on the cards and payments market. This preference is rooted in familiarity, trust, and concerns about cybersecurity, especially among elderly users who are less comfortable with digital tools. Moreover, small merchants in rural areas often continue to accept only cash, citing high fees or a lack of infrastructure for card payments. This ongoing reliance on cash limits the penetration of electronic payment systems and hampers transaction volume growth for traditional card providers, creating a structural challenge in achieving full digital payment adoption across the country.

Regulatory Complexity and Compliance Costs

Spain’s financial sector operates within a complex regulatory framework influenced by both national legislation and EU-wide directives, such as PSD2 (Revised Payment Services Directive) and GDPR (General Data Protection Regulation). While these regulations aim to enhance consumer protection and security, they also impose significant compliance burdens on banks and fintech firms, slowing down innovation and increasing operational costs. According to a Deloitte 2023 FinTech Report, 41% of Spanish fintech startups identified regulatory compliance as a major barrier to scaling their payment solutions, with many facing delays in product launches due to extensive approval processes. Besides, the Bank of Spain reported in 2023 that compliance-related costs for smaller payment institutions had risen notably since the implementation of stricter anti-money laundering (AML) requirements, reducing profit margins and limiting investment in new payment technologies.

MARKET OPPORTUNITIES

Expansion of Buy Now, Pay Later (BNPL) Services

Spain presents a growing opportunity for Buy Now, Pay Later (BNPL) services, driven by shifting consumer preferences and a young, digitally engaged population. BNPL offers flexible payment options that align with the spending habits of millennials and Gen Z, who prioritize convenience and affordability over traditional credit. A survey found that a considerable portion of online shoppers in Spain had used BNPL services at least once, signaling increasing mainstream adoption. International players, along with local fintech,s have expanded their operations in Spain, integrating seamlessly with major e-commerce platforms including Amazon Spain, El Corte Inglés, and Zalando. According to Visa’s 2023 European Fintech Outlook, more than 35% of Spanish retailers now offer BNPL as a payment option, reflecting growing merchant acceptance. Banks and card issuers can leverage this trend by partnering with BNPL providers to embed installment features into existing card products, thereby enhancing customer engagement and boosting transaction volumes while meeting evolving consumer finance demands.

Rise of Embedded Finance and Super App Integration

Embedded finance—where financial services like payments, lending, and insurance are integrated into non-financial platforms—is gaining traction in Spain, offering a transformative opportunity for the cards and payments market. With increasing smartphone adoption and digital service consumption, super apps and platforms are incorporating payment solutions to streamline user experiences. A 2023 report by McKinsey & Company highlighted that Spain was among the fastest-growing markets in Europe for embedded finance, with transaction values surpassing EUR 3.4 billion in 2023. Platforms have introduced in-app payment capabilities, allowing users to transact without switching between banking apps or using physical cards. Also, BBVA and Banco Santander have launched open banking APIs to enable third-party developers to integrate financial services into their applications, accelerating the adoption of card-based payments across ecosystems. According to Openbank’s 2023 Digital Payments Survey, 46% of Spanish consumers prefer making payments through integrated platforms rather than standalone banking apps, emphasizing the shift in user behavior.

MARKET CHALLENGES

Cybersecurity Threats and Rising Fraud Incidents

As Spain accelerates its transition toward a digital-first payments ecosystem, the frequency and sophistication of cyberattacks targeting financial transactions have surged, posing a major challenge to the cards and payments industry. According to Spain’s National Cryptologic Center (CCN), cybercrime incidents increased in recent years, with online payment fraud accounting for a notable portion of all reported cases. Card-not-present (CNP) fraud remains a critical concern, particularly with the rise in e-commerce transactions. Phishing scams, malware attacks, and data breaches have contributed to declining consumer confidence in digital payments, especially among older users. Moreover, Europol’s 2023 Internet Organised Crime Threat Assessment (IOCTA) identified Spain as one of the top five EU countries affected by online payment fraud, with criminals exploiting weak authentication mechanisms and stolen card credentials. To avoid risks, financial institutions must invest in advanced fraud detection technologies such as AI-driven analytics, biometric verification, and tokenization, which could increase operational costs and slow transaction processing speeds.

Uneven Digital Infrastructure across Regions

While urban centers in Spain, such as Madrid and Barcelona, enjoy robust digital infrastructure and high card payment adoption, disparities persist in rural and remote regions, hindering the uniform growth of the cards and payments market. According to Red.es, Spain’s public agency for digital advancement, only 62% of rural municipalities had reliable broadband access in 2023, compared to 98% in major cities. This digital divide affects both consumers and merchants. Many small businesses in rural areas still rely on cash due to limited access to POS terminals or unstable internet connections required for card transactions. A 2023 report by CEPYME (Confederation of Small and Medium Enterprises) found that a significant percentage of micro-enterprises in rural Spain lacked the necessary infrastructure to process card payments, constraining transaction opportunities. On the consumer side, INE (National Institute of Statistics) data shows that digital payment adoption among residents in rural provinces was 21% lower than in metropolitan areas, primarily due to low digital literacy and lack of access to mobile banking services.

SEGMENTAL ANALYSIS

By Cards Insights

The debit cards segment completely dominates the Sweden cards and payments market and is expected to maintain its position in the coming years. This is due to the extensive use of debit cards for payment of in-store purchases. Most people have linked it to their mobile payment platforms, which elevates the segment’s market share. The most essential factor compelling more customers to pay via mobile phone is that it is considered a simple and convenient method. Another reason for boosting the segment’s market size is the considerable growth in e-commerce. According to industry experts, the widely used payment methods are physical debit cards and Swish online.

Whereas, the credit cards segment holds a relatively smaller portion of Sweden's cards and payments market share.

By Payment Terminals Insights

The POS segment is likely to capture a higher portion of the Sweden cards and payments market during the estimation period. This can be credited to its quality of being contactless payments to provides a better return on investment and ease of access via smartphones. Sweden stands aside from other regional countries because of its unique payment preferences. Moreover, the fixed-line internet infrastructures in the industry are among the most appropriate for extensiveness, access to the internet, and e-commerce websites and platforms for all customer types and socio-demographics. In addition, higher consumption of tailor-made POS throughout a broad range of business use cases would propel the advancement of modern software products that would function as the foundation.

The ATM segment saw a significant drop in its market share in the past few years. As per a study, between 2020 and 2022 ,the number of ATMs throughout Sweden reduced by 12 per cent. The application of cash has been declining consistently for many years. However, in 2023 and recently in 2024, consumers have again started to acknowledge the importance of cash for the community, particularly in a crisis environment when online payment options may not work.

By Payment Instruments Insights

The payment cards segment is the leading category with the maximum portion of the Sweden cards and payments market share. Government policies and the growing inclination of customers are the factors boosting the segment’s market share. Moreover, a wide range of customers have been digitally settling their bills for many years. Apart from this, less than 5 percent stated the usage of products other than digital products, like cash and postal gir,o over the counter to pay bills in February 2024. This shows the significance of this segment across the region. Apart from this, the market also benefited from the reduction in cash usage in stores. On the other hand, the direct debit segment has grown moderately in the past few years.

COUNTRY ANALYSIS

The Sweden cards and payments market is driving forward at a significant growth rate due to the dominance of debit cards and Swish mobile payment. For example, in 2023, the frequency of cash withdrawals from the ATM of Bankomat AB dropped as well as the value of cash in circulation by 10 per cent between 2018 and 2023. Further, the market also saw the rise of both debit cards and Swish because the latter payment method has not been completely added to the physical retail business. However, it was an early adopter of Swish, but currently, its Nordic and other nearby economies have grown further and provide more options to pay instantly. Also, the presence of legacy infrastructure and systems, along with the lack of time updates, has derailed its expansion trajectory.

KEY MARKET PARTICIPANTS

Some of the Dominating players in the Market include

- Swedbank

- Nordea

- Handelsbanken

- ICA Banken

- Ikano Bank

SWEDEN CARDS AND PAYMENTS MARKET NEWS

- In February 2024, it was announced that Swish payments will use Riksbank's payment system RIX-INST to settle all the payments, including the money transfer from one bank to the other. Moreover, RIX-INST is also linked to the TARGET Instant Payment (TIPS), a technical platform of the Eurosystem, providing potential opportunities for more Swedish players to create new payment services and products.

- In February 2024, the Swedish Ministry of Finance introduced a new proposal for an even more extensive ban on the application of credit for gambling.

MARKET SEGMENTATION

This research report on the Sweden cards and payments market has been segmented and sub-segmented based on the following categories.

By Cards

-

Debit Cards

- Credit Cards

- Prepaid Cards

By Payment Terminals

- POS

- ATM's

By Payment Instruments

- Credit Transfers

- Direct Debit

- Cheques

- Payment Cards

Frequently Asked Questions

1. What is the size of the Sweden cards and payments market?

The Sweden cards and payments market exceeds USD 144.37 billion in 2025, with cards and Swish handling over 95% of transactions in a near-cashless economy.

2. What drives growth in the Sweden cards and payments market?

Swish ubiquity and contactless cards fuel the Sweden cards and payments market, alongside e-commerce and instant payment mandates.

3. What are key trends in the Sweden cards and payments market?

Swish P2P and contactless dominate the Sweden cards and payments market, with cash under 1% of retail payments.

4. How dominant are debit cards in the Sweden cards and payments market?

Debit cards lead everyday use in the Sweden cards and payments market, integrated with BankID for seamless auth.

5. What role do credit cards play in the Sweden cards and payments market?

Credit cards support travel and online in the Sweden cards and payments market, competing with Klarna BNPL.

6. How common are contactless payments in the Sweden cards and payments market?

Contactless exceeds 90% of card txns in the Sweden cards and payments market at NFC POS terminals.

7. How does e-commerce impact the Sweden cards and payments market?

E-commerce boosts secure cards and wallets in the Sweden cards and payments market with 3DS2 standards.

8. What opportunities exist in the Sweden cards and payments market?

Embedded payments and BNPL expansions offer growth in the Sweden cards and payments market for fintechs.

9. Who leads the Sweden cards and payments market?

Nordea, SEB, and Swish MobilePay shape the Sweden cards and payments market via networks and apps.

10. What regulations shape the Sweden cards and payments market?

PSD2 and instant payment rules drive innovation in the Sweden cards and payments market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com