- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

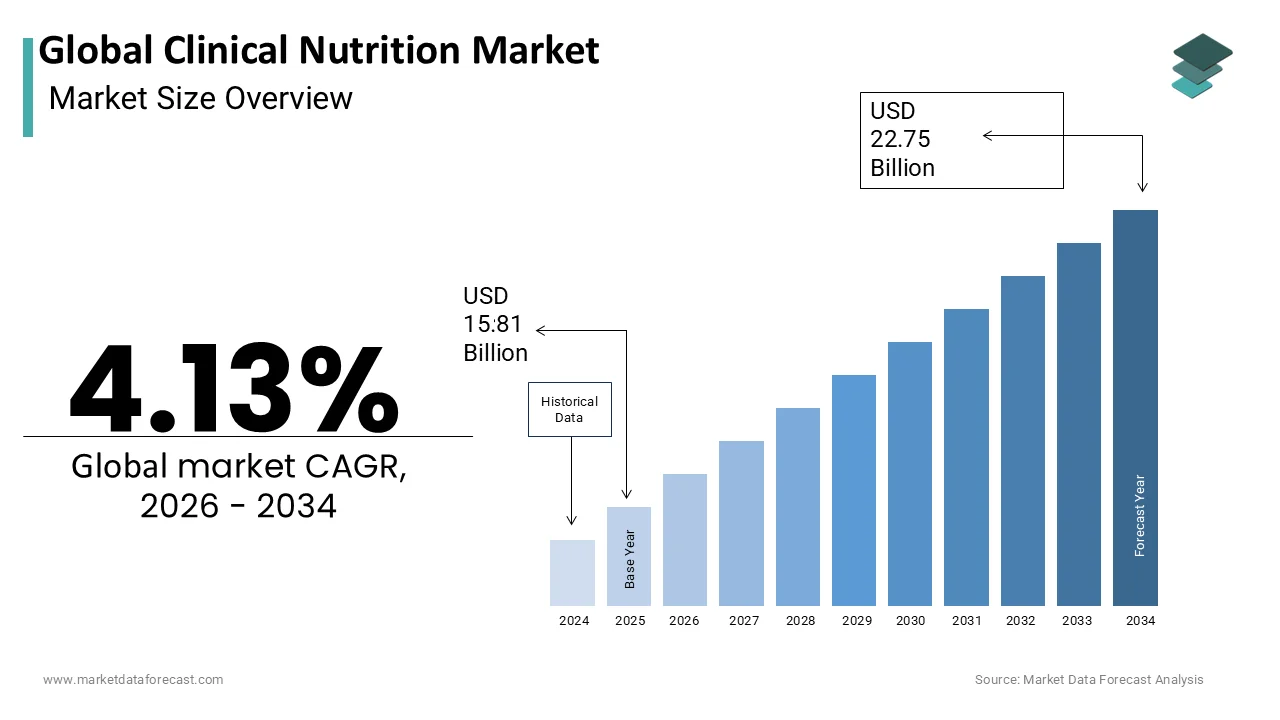

Market Size, 2025

$15.81 BnMarket Estimate, 2026

$16.46 BnMarket Forecast, 2034

$22.75 BnCAGR, 2026–2034

4.13%Global Clinical Nutrition Market Summary

Market Size & Growth

- The Global Clinical Nutrition Market was valued at USD 15.81 billion in 2025.

- It is projected to reach USD 16.46 billion in 2026 and USD 22.75 billion by 2034.

- The market is expected to grow at a CAGR of 4.13% from 2026 to 2034.

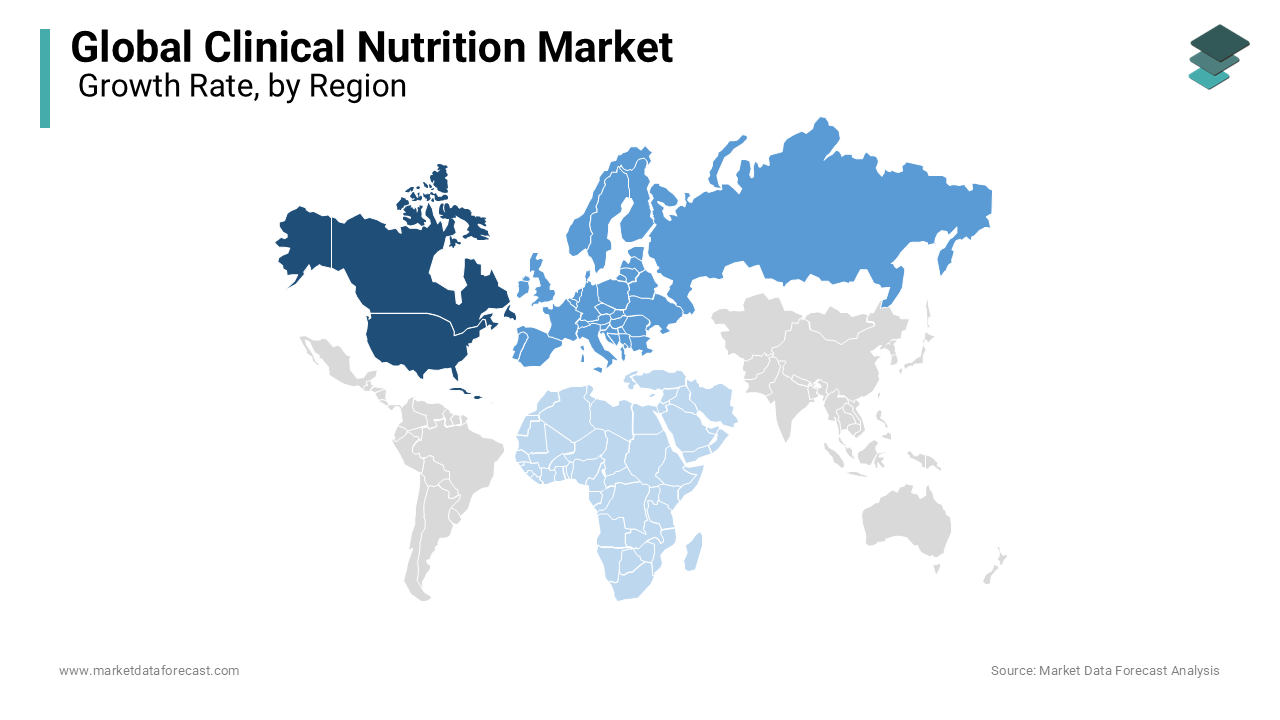

- North America led the market with a 39.3% revenue share in 2025.

Key Market Segments

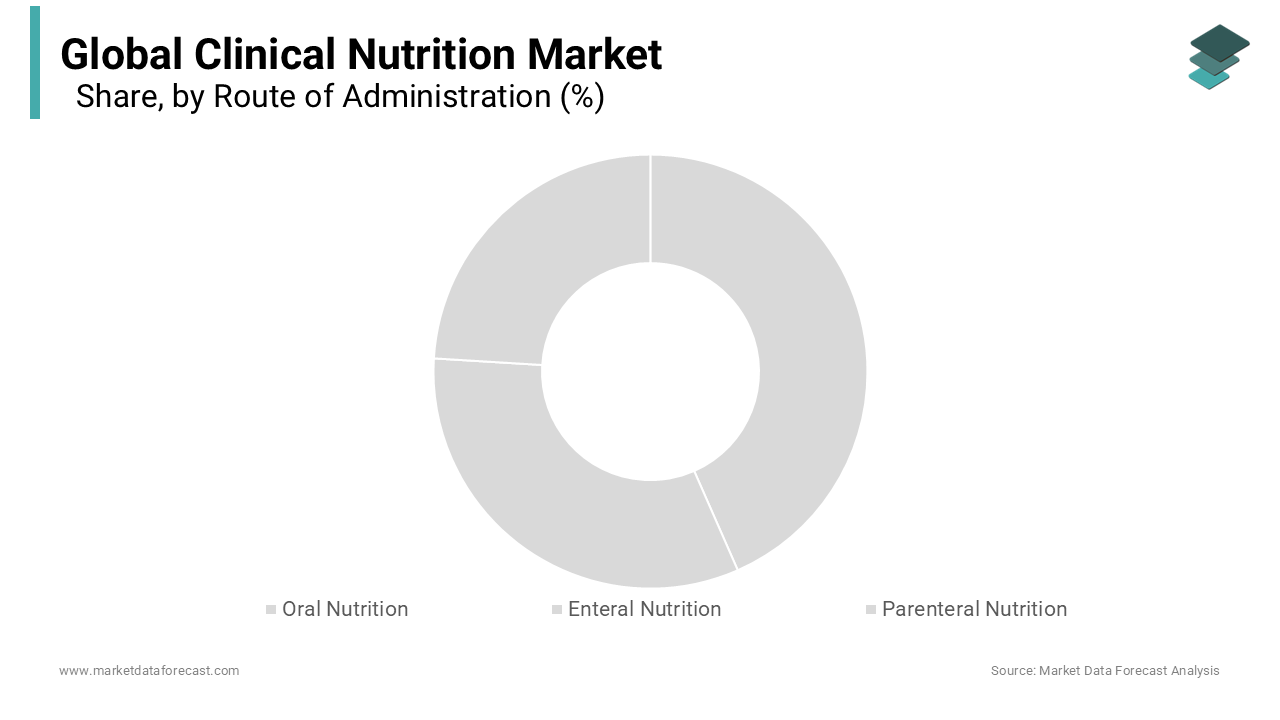

- By Route of Administration: Oral Nutrition, Enteral Nutrition, Parenteral Nutrition.

- By Therapeutic Areas: Cancer, Malabsorption, Diarrhea, Food Allergies, Maldigestion, Diabetes, Short-Bowel Syndrome, Acute Lung Injury, Acute Respiratory Distress.

- By Ingredients Type: Vitamins, Minerals, Carbohydrates, Amino Acids.

- Oral Nutrition held the largest share at 53.5% in 2025; Enteral Nutrition is the fastest-growing route at a CAGR of 8.3%.

- Cancer was the largest therapeutic area, capturing 27.6% share in 2025; ALI/ARDS is the fastest-growing therapeutic area at a CAGR of 9.6%.

Key Drivers

- Rising prevalence of chronic diseases such as cancer, diabetes, and cardiovascular conditions increases demand for nutritional support; 85% of advanced cancer patients exhibit signs of malnutrition per the American Society of Parenteral and Enteral Nutrition.

- Growing geriatric population with heightened nutritional vulnerability; 20–30% of community-dwelling seniors and over 60% of institutionalized elderly are malnourished, per the European Society for Clinical Nutrition and Metabolism.

- Expansion of home-based and community clinical nutrition programs, driven by telemonitoring platforms and portable feeding pumps.

Key Players

Nestle Nutrition, Abbott Laboratories Inc., Gentiva Health Services Inc., Mead Johnson & Company, Kendall, Ajinomoto Co. Inc., Hospira Inc., Hero Nutritionals Inc., Lonza Ltd, Baxter International Inc., B. Braun Melsungen AG, H.J. Heinz Company, American Home Patient Inc., and Fresenius Kabi.

Global Clinical Nutrition Market Size

The Global Clinical Nutrition Market is projected to grow from USD 15.81 billion in 2025 to USD 16.46 billion in 2026 and reach USD 22.75 billion by 2034, registering a CAGR of 4.13% during the forecast period from 2026 to 2034.

Clinical Nutrition refers to the specialized nutritional formulations designed to address the dietary needs of individuals with medical conditions that impair normal nutrient intake, absorption, or metabolism. These products, ranging from enteral tube feeding formulas to oral nutritional supplements (ONS) and parenteral nutrition, are administered under medical supervision to manage malnutrition associated with chronic diseases, surgical recovery, critical illness, and age-related physiological decline. Unlike general dietary supplements, clinical nutrition products are formulated with precise macronutrient and micronutrient profiles tailored to specific pathologies such as cancer, gastrointestinal disorders, renal failure, and neurodegenerative conditions.

As per the Global Clinical Nutrition Council, up to 50% of hospitalized patients in Europe and North America are either malnourished or at risk upon admission, underscoring the critical role of early nutritional intervention. With rising awareness among healthcare providers and evolving reimbursement frameworks, clinical nutrition is transitioning from a supportive measure to an integral component of evidence-based medical care, particularly in intensive care units, oncology centers, and geriatric facilities.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Requiring Nutritional Support

The escalating global burden of chronic diseases such as cancer, diabetes, and cardiovascular conditions is a primary catalyst for the expansion of the clinical nutrition market. These illnesses often induce metabolic imbalances, reduced appetite, and malabsorption, necessitating specialized nutritional interventions to maintain body composition and support treatment efficacy. According to the World Health Organization, non-communicable diseases account for 74% of all global deaths, a wasting syndrome that leads to severe muscle and fat loss. The American Society of Parenteral and Enteral Nutrition reports that 85% of advanced cancer patients exhibit signs of malnutrition, directly impacting chemotherapy tolerance and survival rates. Renal disease also drives demand. As healthcare systems increasingly recognize nutrition as a modifiable factor in disease progression, the integration of clinical nutrition into standard care pathways is accelerating, particularly in oncology and metabolic disorder management.

Growing Geriatric Population with Heightened Nutritional Vulnerability

Demographic aging is a pivotal force driving demand for clinical nutrition, as older adults are disproportionately susceptible to malnutrition due to physiological decline, polypharmacy, and comorbid conditions. This demographic shift is particularly pronounced in high-income nations. Age-related conditions such as sarcopenia, dysphagia, and cognitive impairment significantly impair nutritional intake, with the European Society for Clinical Nutrition and Metabolism estimating that 20–30% of community-dwelling seniors and over 60% of institutionalized elderly individuals are malnourished. In the United States, the National Health and Nutrition Examination Survey found that 15% of adults over 60 consume insufficient protein, increasing frailty and fall risks. Clinical nutrition products, particularly high-protein ONS, have been shown to improve muscle strength and functional outcomes. As healthcare systems grapple with the rising costs of geriatric care, preventive nutritional support is gaining recognition as a cost-effective strategy to enhance quality of life and reduce institutionalization.

MARKET RESTRAINTS

Inadequate Reimbursement Policies in Public and Private Health Systems

The inconsistent and often insufficient reimbursement coverage across public and private health systems is a critical barrier to the widespread adoption of clinical nutrition. Despite robust clinical evidence supporting the efficacy of nutritional interventions, many insurers and government programs do not classify clinical nutrition products as essential medical treatments, instead categorizing them as dietary supplements. In the United States, Medicare Part B covers enteral nutrition only under strict criteria, such as confirmed gastrointestinal dysfunction, leaving many elderly or chronically ill patients to bear out-of-pocket costs. Emerging economies face even greater gaps. This lack of financial support discourages prescriber engagement and limits patient adherence, undermining the potential of clinical nutrition to reduce long-term healthcare burdens.

Low Awareness and Underdiagnosis of Malnutrition in Clinical Settings

Malnutrition remains significantly underdiagnosed and undertreated in healthcare environments, impeding the uptake of clinical nutrition solutions. This diagnostic gap stems from fragmented care models, a lack of standardized screening tools, and limited training for non-dietitian clinicians. Besides, patients often fail to recognize early signs of malnutrition, attributing fatigue and weight loss to aging or illness progression. In low-resource settings, the absence of dedicated clinical dietitians exacerbates the issue. Without systemic integration of nutritional assessment into routine care, clinical nutrition remains an overlooked intervention, despite its proven impact on recovery, immunity, and treatment outcomes.

MARKET OPPORTUNITIES

Expansion of Home-Based and Community Clinical Nutrition Programs

The shift toward decentralized healthcare delivery is creating significant opportunities for home-based clinical nutrition, driven by patient preference, cost efficiency, and advancements in delivery infrastructure. As healthcare systems seek to reduce hospital readmissions and optimize bed utilization, outpatient and home enteral nutrition (HEN) programs are gaining traction. Technological enablers such as portable feeding pumps, telemonitoring platforms, and smart packaging with usage tracking are improving compliance and safety. Besides, community pharmacies and home health agencies are increasingly stocking and dispensing clinical nutrition products, improving accessibility. These developments signal a structural shift toward patient-centered, community-integrated nutritional care.

Development of Disease-Specific and Personalized Nutrition Formulations

Advancements in nutrigenomics, metabolomics, and artificial intelligence are enabling the creation of highly targeted clinical nutrition products tailored to individual pathologies and genetic profiles. Unlike generic formulas, disease-specific formulations address the unique metabolic demands of conditions such as cancer, liver disease, and phenylketonuria. In oncology, specialized immunonutrition formulas containing arginine, omega-3 fatty acids, and nucleotides have been shown to reduce postoperative complications. Similarly, in renal failure, low-phosphorus, acid-base-balanced formulas help delay dialysis initiation. Companies like Nestlé Health Science and Danone Nutricia are investing in AI-driven platforms to analyze patient data and recommend personalized regimens. With regulatory bodies such as the FDA recognizing the therapeutic value of medical foods, the pathway for innovation is expanding. As precision medicine gains momentum, clinical nutrition is poised to evolve from a supportive measure to a targeted therapeutic modality.

MARKET CHALLENGES

Regulatory Heterogeneity and Classification Ambiguity Across Regions

The clinical nutrition market faces significant operational complexity due to divergent regulatory frameworks that classify products inconsistently across jurisdictions, affecting market access and commercial strategy. In the United States, the FDA regulates medical foods under a distinct category requiring physician supervision and intended for the dietary management of a disease, yet they are not subject to premarket approval. Conversely, the European Union lacks a harmonized definition for medical foods, leading to fragmented national regulations. In contrast, countries like Japan and South Korea have well-defined approval pathways for Foods for Specified Health Use (FOSHU) and Health Functional Foods, respectively, enabling faster market entry. This regulatory patchwork complicates global product development, forcing manufacturers to reformulate or reposition products for different markets. Besides, the absence of standardized claims approval processes leads to marketing limitations; for example, immune-support claims are permitted in Canada but restricted in Germany. Until greater harmonization is achieved, companies must navigate a labyrinth of compliance requirements, delaying innovation and increasing time-to-market.

Supply Chain Vulnerability for Specialty Ingredients and Formulation Stability

The production of clinical nutrition products is highly dependent on a limited pool of specialized raw materials, such as hydrolyzed proteins, medium-chain triglycerides (MCTs), and rare amino acids, whose supply is susceptible to geopolitical, climatic, and logistical disruptions. Additionally, certain amino acids used in renal and metabolic formulas are synthesized in China, which produces a notable share of the world’s supply. Furthermore, clinical nutrition formulations require stringent stability testing due to their complex emulsions and sensitive bioactive compounds; temperature excursions during transport can degrade protein integrity and alter nutrient bioavailability. These vulnerabilities necessitate costly dual sourcing, advanced packaging, and redundant logistics networks, challenging the scalability and affordability of life-saving nutritional therapies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Route Of Administration, Therapeutic Areas, Ingredients Type, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter's Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Nestle Nutrition, Abbott Laboratories Inc., Gentiva Health Services Inc., Mead Johnson & Company, Kendall, Ajinomoto Co. Inc., Hospira Inc., Hero Nutritionals Inc., Lonza Ltd, Baxter International Inc., B. Braun Melsungen AG, H.J. Heinz Company, American Home Patient Inc., and Fresenius Kabi. |

SEGMENTAL ANALYSIS

By Route of Administration Insights

The oral nutrition segment led the clinical nutrition market by accounting for a 53.5% share in 2025. This dominance is primarily driven by its accessibility, ease of use, and applicability across diverse patient populations, particularly those with mild to moderate malnutrition or chronic conditions requiring long-term dietary management. The widespread adoption of oral nutritional supplements (ONS) in outpatient and community settings, where patients can self-administer without medical supervision, is a key factor underpinning their growth. Additionally, patient preference plays a critical role. The expansion of retail and e-commerce channels has further broadened access, with major pharmacies like Walgreens and Boots stocking specialized products for diabetes, renal disease, and oncology. With growing emphasis on preventive care and aging-in-place models, oral nutrition remains the most scalable and patient-friendly route, solidifying its central role in clinical nutrition delivery.

The enteral nutrition segment is the fastest-growing in the clinical nutrition market and is projected to expand at a CAGR of 8.3% in the coming years. This accelerated growth is driven by the rising number of critically ill and post-surgical patients requiring tube feeding in hospital and long-term care settings. The increasing prevalence of gastrointestinal disorders and neurological conditions that impair swallowing, such as stroke, amyotrophic lateral sclerosis (ALS), and advanced dementia, is a primary factor. Additionally, intensive care units (ICUs) are increasingly adopting early enteral nutrition protocols to preserve gut integrity and reduce infection risks. Technological advancements have also enhanced adoption; modern feeding pumps with closed-loop systems and anti-reflux valves improve safety and compliance. With aging populations and rising ICU admissions, enteral nutrition is becoming an indispensable component of acute and chronic care.

The enteral nutrition segment had a considerable share of the worldwide market in 2025 and is predicted to grow at a noteworthy CAGR during the forecast period. The segmental growth is majorly driven by the growing patient population suffering from diseases such as cancer, neurological diseases, and severe burns. Factors such as the growing patient population suffering from chronic diseases, the growing aging population, and increasing R&D efforts by the market participants to develop enteral feeding devices and enteral clinical products that are more effective and safer to use are expected to boost the segment’s growth rate.

By Therapeutic Areas Insights

The cancer therapeutic area segment represented the largest segment in the clinical nutrition market by capturing 27.6% share in 2025. This lead position is due to the high prevalence of malnutrition among oncology patients, driven by tumor-induced metabolic changes, treatment side effects, and reduced food intake. According to the American Society of Clinical Oncology, up to 80% of advanced cancer patients experience significant weight loss, with 20.40%. meeting the criteria for cachexia a condition characterized by involuntary muscle wasting that diminishes treatment tolerance and survival. Clinical nutrition, particularly immunonutrition formulas enriched with arginine, omega-3 fatty acids, and nucleotides, has been shown to improve outcomes. Besides, the global rise in cancer incidence ensures sustained demand. Hospitals are increasingly integrating nutritional screening into oncology care pathways. As cancer care shifts toward multidisciplinary models, clinical nutrition is emerging as a cornerstone of supportive therapy, reinforcing its dominant market position.

The ALI/ARDS segment is emerging as the fastest-growing therapeutic area in the clinical nutrition market, with a projected CAGR of 9.6% in the coming years. This surge is driven by the heightened recognition of nutritional support as a critical intervention in respiratory failure management, particularly in intensive care settings. The physiological demand for specialized formulas that modulate inflammation and support lung function is a key factor. Patients with ARDS often require prolonged mechanical ventilation, during which muscle wasting and oxidative stress accelerate, necessitating high-protein, antioxidant-rich nutrition. The global impact of respiratory pandemics has further amplified demand. Additionally, the Surviving Sepsis Campaign guidelines now recommend immunonutrition for severe respiratory infections, increasing clinical adoption. As critical care protocols evolve, ALI/ARDS is transforming from an emergent indication into a structured domain of clinical nutrition.

By Ingredients Type Insights

The vitamins segment accounted for the largest share of the global clinical nutrition market in 2025, and the segment’s lead is expected to continue during the forecast period. Factors such as the increasing number of people suffering from vitamin deficiencies, the growing patient population suffering from various diseases and increasing awareness among people regarding nutrition management, and rising demand for personalized nutrition plans are promoting the growth of the segment.

The amino acids segment is estimated to hold a considerable share of the global clinical nutrition market during the forecast period. The growing demand for specialized nutrition products and increasing high protein needs by gimmers and people who participate in sports regularly are contributing to the segmental growth. The rising awareness among people regarding the role that protein plays in being healthy is favoring the segment’s growth rate. The growing efforts by market participants to develop effective nutritional products favor segmental growth.

REGIONAL ANALYSIS

North America Clinical Nutrition Market Insights

North America led the global clinical nutrition market with a 39.3% share of revenue in 2025. The region’s dominance is anchored in its advanced healthcare infrastructure, high prevalence of chronic diseases, and well-established reimbursement mechanisms for medical nutrition. The United States, in particular, has a mature market supported by strong regulatory clarity from the FDA, which recognizes medical foods as a distinct category for the dietary management of specific diseases. The aging population further amplifies demand; the U.S. Census Bureau projects that by 2030, one in five Americans will be over 65, a demographic highly susceptible to malnutrition. The integration of nutritional screening into electronic health records (EHRs) through systems like Epic and Cerner has improved early detection and intervention. Besides, major players such as Abbott, Baxter, and Nestlé Health Science maintain robust R&D and distribution networks across the country. The expansion of home healthcare services, supported by Medicare’s coverage of enteral nutrition, has enabled decentralized care models. With high physician awareness and growing patient advocacy, North America remains the most developed and innovation-driven market for clinical nutrition.

Europe Clinical Nutrition Market Insights

Europe is another key player in the clinical nutrition market. The region’s market is characterized by a strong emphasis on evidence-based medicine, structured healthcare systems, and increasing policy support for nutritional care. Countries such as Germany, France, and the UK have integrated clinical nutrition into national clinical guidelines, with the British Association for Clinical Nutrition and Metabolism advocating for universal malnutrition screening in hospitals. Reimbursement varies across nations; Germany and Sweden offer comprehensive coverage for enteral and oral supplements, while Southern and Eastern European countries lag in funding. The EU’s Horizon Europe program is funding research into personalized nutrition for chronic diseases, fostering innovation. Additionally, the rise of home-based care in aging societies like Italy and Spain is driving demand for portable feeding systems and ONS. With regulatory harmonization efforts underway, Europe remains a pivotal market for clinical nutrition advancement.

Asia-Pacific Clinical Nutrition Market Insights

Asia-Pacific is the fastest-growing region in the clinical nutrition market. The region’s expansion is fueled by rising healthcare expenditure, increasing hospital infrastructure, and growing awareness of nutrition’s role in disease management. Japan, China, and South Korea are leading the transformation, with Japan’s aging society driving demand for geriatric nutritional support. India is witnessing rapid growth in private hospitals that incorporate clinical nutrition into oncology and gastrointestinal care. The Indian Council of Medical Research has issued national guidelines on malnutrition screening, promoting standardization. Additionally, local manufacturers such as Danone Nutricia and Meiji are launching culturally adapted formulations, including rice-based and lactose-free options. With rising physician education and government initiatives like Ayushman Bharat improving access, APAC is transitioning from a nascent to a high-potential market for clinical nutrition.

Latin America Clinical Nutrition Market Insights

Latin America is reflecting a market in early but accelerating development. Brazil and Mexico are the primary drivers, with Brazil accounting for a key share of regional demand due to its large population and growing private healthcare sector. A key growth factor is the rising incidence of chronic diseases. Additionally, partnerships between multinational companies and local distributors are expanding access to enteral and oral products in urban centers. However, fragmented reimbursement and limited insurance coverage remain barriers. Despite these challenges, the expansion of telehealth and home care services, particularly in Colombia and Chile, is creating new avenues for clinical nutrition delivery. With increasing medical awareness and infrastructure investment, Latin America is poised for sustained growth.

Middle East and Africa Clinical Nutrition Market Insights

The Middle East and Africa collectively represent a small share of the global clinical nutrition market, with growth concentrated in the Gulf Cooperation Council (GCC) countries. The UAE and Saudi Arabia are at the forefront, driven by state-of-the-art healthcare facilities, high government spending, and medical tourism. In Saudi Arabia, Vision 2030 includes healthcare modernization, with a focus on non-communicable diseases. However, in sub-Saharan Africa, access remains limited. Malnutrition in critical illness is often overlooked, despite high rates of infectious diseases like HIV and tuberculosis that exacerbate nutrient depletion. Nigeria and South Africa are emerging as regional hubs, with private clinics offering enteral nutrition for cancer and ICU patients. With increasing urbanization and healthcare investment, MEA is evolving into a fragmented yet strategically important market for clinical nutrition expansion.

KEY MARKET PLAYERS

Some of the key market participants in the global clinical nutrition market profiled in this report are Nestle Nutrition, Abbott Laboratories Inc., Gentiva Health Services Inc., Mead Johnson & Company, Kendall, Ajinomoto Co. Inc., Hospira Inc., Hero Nutritionals Inc., Lonza Ltd, Baxter International Inc., B. Braun Melsungen AG, H., J. Heinz Company, American Home Patient Inc. and Fresenius Kabi.

TOP LEADING PLAYERS IN THE MARKET

Abbott Nutrition

Abbott Nutrition has established a strong presence in the Asia Pacific clinical nutrition market through its broad portfolio of science-based medical nutrition products, including Ensure, Glucerna, and Juven. The company has strategically partnered with hospitals, clinics, and government health programs across Japan, Australia, India, and Southeast Asia to integrate its products into standard care pathways for diabetes, oncology, and geriatric care. In 2023, Abbott launched a digital nutrition support platform in Singapore that enables remote monitoring of patient adherence to oral nutritional supplements, enhancing care continuity. It also expanded its manufacturing footprint in Malaysia to meet regional demand and ensure supply chain resilience. Collaborations with medical associations, such as the Indian Society of Parenteral and Enteral Nutrition, have strengthened clinical credibility. Additionally, Abbott introduced culturally adapted formulations, including low-lactose and rice-based variants, tailored to local dietary preferences. By investing in healthcare professional education and digital health integration, Abbott is reinforcing its leadership in evidence-based clinical nutrition across diverse APAC healthcare ecosystems.

Nestlé Health Science

Nestlé Health Science has significantly advanced its footprint in the Asia Pacific clinical nutrition market by focusing on innovation, medical engagement, and condition-specific formulations. The company’s portfolio, including Resource, Peptamen, and Fortimel, is widely used in hospitals and home care settings across South Korea, China, and Australia for managing malnutrition in cancer, gastrointestinal, and critical care patients. In 2023, Nestlé Health Science launched a specialized immunonutrition product for post-surgical recovery in Japan, developed in collaboration with Tokyo University Hospital. It also initiated a clinical training program in Thailand for dietitians and physicians on early nutritional intervention in ICU patients. The company strengthened its digital capabilities by integrating its nutrition solutions with hospital electronic health record systems in Taiwan. Furthermore, Nestlé Health Science invested in local R&D centers in Shanghai and Singapore to accelerate the development of region-specific products. By aligning scientific rigor with localized healthcare needs, the company is positioning itself as a strategic partner in advancing nutritional therapy standards across the Asia Pacific.

Baxter International Inc.

Baxter International has deepened its engagement in the Asia Pacific clinical nutrition market by focusing on enteral and parenteral nutrition solutions for acute and chronic care settings. The company’s home and hospital-based feeding systems, including its automated compounding platforms and closed enteral feeding sets, are increasingly adopted in Japan, South Korea, and Australia due to their precision and safety. In 2023, Baxter launched a smart enteral pump with wireless dose tracking in New Zealand and expanded its distribution network in Indonesia through a partnership with a local healthcare distributor. It also conducted clinical workshops in collaboration with the Australian and New Zealand Intensive Care Society to promote best practices in critical care nutrition. The introduction of ready-to-use, sterile nutritional bags has improved infection control in ICU environments across urban hospitals in the region. Additionally, Baxter enhanced its patient support services by launching multilingual tele-nutrition hotlines in the Philippines and Vietnam. By combining advanced delivery technologies with clinical education and localized service models, Baxter is strengthening its role in improving access to safe and effective clinical nutrition across diverse APAC healthcare infrastructures.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the clinical nutrition market are deploying multifaceted strategies to strengthen their competitive positioning, including product innovation, geographic expansion, digital health integration, strategic collaborations, and clinician education. Companies are investing in R&D to develop disease-specific formulations with enhanced bioavailability, such as immunonutrition for cancer and metabolic support for critical care. Expansion into high-growth regions like the Asia Pacific and Latin America is being accelerated through local manufacturing, regulatory submissions, and partnerships with regional distributors. Firms are integrating digital tools such as mobile apps, tele-nutrition platforms, and EHR-linked monitoring systems to improve patient adherence and clinical outcomes. Collaborations with hospitals, medical societies, and government agencies are enhancing credibility and standardizing nutritional care protocols. Additionally, manufacturers are expanding their service offerings, including home delivery, nurse support, and remote pump monitoring, to differentiate beyond product alone. Regulatory agility is prioritized to navigate complex classifications of medical foods and secure reimbursement. These strategies collectively enable companies to build end-to-end solutions that align with evolving healthcare delivery models and patient-centered care.

COMPETITION OVERVIEW

Competition in the clinical nutrition market is intensifying as global leaders, regional specialists, and pharmaceutical entrants vie for influence in a sector increasingly recognized as integral to patient outcomes. Multinational corporations such as Abbott, Nestlé Health Science, and Baxter dominate through extensive portfolios, scientific validation, and established distribution networks. However, Asia and Latin America regional players are gaining traction by offering cost-effective, locally adapted formulations. The competitive landscape is shifting from product-centric to solution-oriented models, where success depends on integration with clinical workflows, digital monitoring, and educational support. Differentiation is achieved through condition-specific innovation, such as immunonutrition for oncology or pulmonary formulas for respiratory failure. Regulatory expertise is critical, as varying classifications of medical foods across regions impact market access. In hospital settings, tenders and formulary inclusion are key battlegrounds, while in outpatient care, brand trust and patient support services determine loyalty. Mergers and acquisitions, such as Danone’s integration of Nutricia, reflect consolidation to expand global reach. As healthcare systems emphasize value-based care, companies that demonstrate measurable clinical and economic benefits, such as reduced hospital stays and complication rates, are gaining preferential positioning. The future of competition lies in the seamless integration of nutrition into multidisciplinary care pathways.

RECENT MARKET DEVELOPMENTS

- In February 2023, Abbott Nutrition launched a digital patient adherence platform in Singapore, enabling real-time tracking of oral supplement consumption and remote consultations with dietitians to improve treatment continuity in chronic disease management.

- In May 2023, Nestlé Health Science introduced a new immunonutrition formula for postoperative recovery in Japan, developed with Tokyo University Hospital, to enhance clinical outcomes in gastrointestinal surgery patients.

- In July 2023, Baxter International expanded its enteral nutrition distribution in Indonesia through a strategic partnership with local healthcare provider Kimia Farma, improving access to sterile feeding solutions in secondary hospitals.

- In October 2023, Danone Nutricia launched a low-lactose, rice-based oral nutritional supplement in India, tailored to local dietary preferences and digestive sensitivities, increasing patient compliance in geriatric and diabetic populations.

- In April 2025, DynaTouch, a kiosk solutions provider, acquired KioWare, a kiosk management software company. This acquisition is anticipated to allow DynaTouch to offer more comprehensive kiosk solutions and strengthen its market presence.

MARKET SEGMENTATION

This market research report on the global clinical nutrition market has been segmented based on the route of administration, therapeutic areas, ingredients type, and region.

By Route of Administration

- Oral Nutrition

- Enteral Nutrition

- Parenteral Nutrition

By Therapeutic Areas

- Malabsorption

- Diarrhea

- Cancer

- Food Allergies

- Maldigestion

- Diabetes

- Short-Bowel Syndrome

- Acute Lung Injury

- Acute Respiratory Distress

By Ingredients Type

- Vitamins

- Minerals

- Carbohydrates

- Amino Acids

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa